Recent trading activity

Since the start of the week, Bordeaux has maintained its dominant trading position, with 46.3% of total trade value since Monday. Château Mouton Rothschild 2019 and Château Angélus 2016 have seen trading activity over the week.

Burgundy has accounted for 21.9% of trade, primarily driven by the trading activity of Domaine de la Romanée-Conti’s Grands Échezeaux Grand Cru 2009 and Domaine Armand Rousseau, Gevrey-Chambertin Premier Cru, Clos Saint-Jacques 2020.

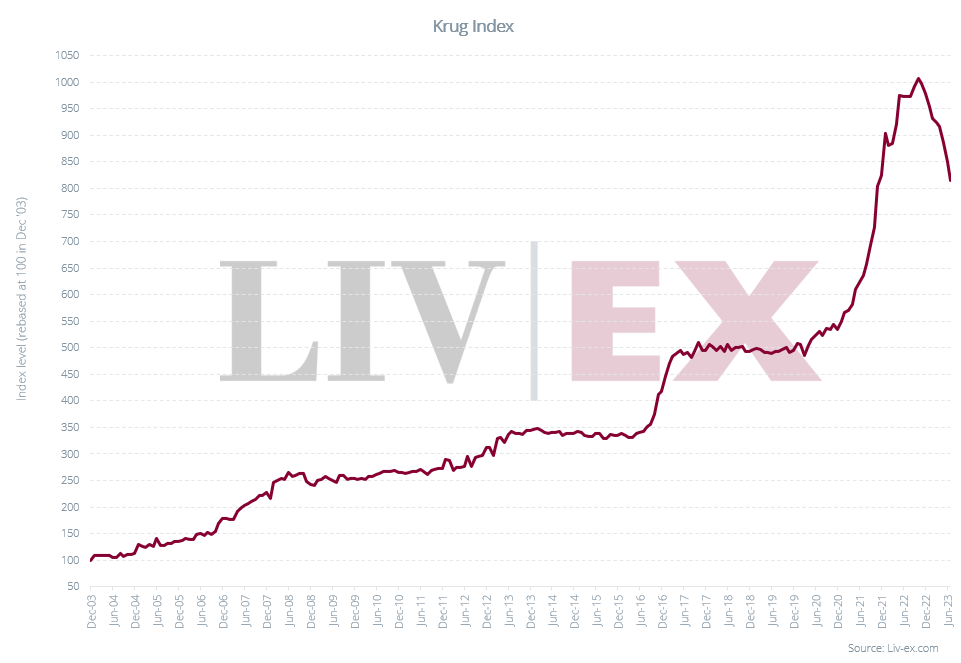

Making sense of Krug prices amid index decline

Krug recorded a 4.3% decline in July, following a 4.0% drop in June, surpassing the Champagne 50 index’s more modest 0.2% decrease in July. This decline could correspond to a price correction, possibly the aftermath of the post-Covid surge in Champagne sales.

Looking at the performance of the last 10 vintages of Krug, all but one vintage (1990) have recorded declines year-to-date. Notably, the 2008 vintage has fallen the most, down 19.3% year-to-date.

However, July brought stability in the indices of four vintages: 2004, 2003, 2000 and 1990 remained unchanged month-on-month. The 1995 vintage actually rose by 2.5%, while the most significant decline was seen in the 1996 vintage, which fell by 2.8%.

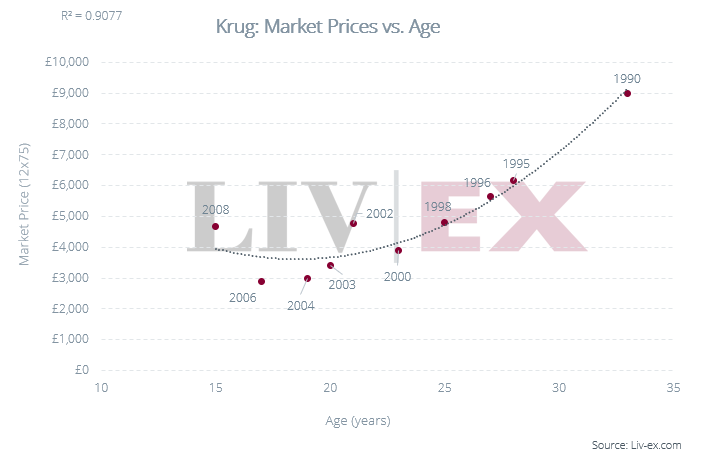

Krug back vintages – where is the value?

Using Liv-ex’s ‘Fair Value’ methodology, Krug Market Prices show a strong 90.8% correlation with age, meaning the wine tends to increase in value with time.

Based on the graph above, we can see that the 2006, 2004, 2003 and 2000 vintages are offered below the fair value price. Among these, the two cheapest options (2006 and 2004) both scored 97 points from Antonio Galloni, outperforming the 1990, 1995, 1998, 2002 and 2003 vintages.

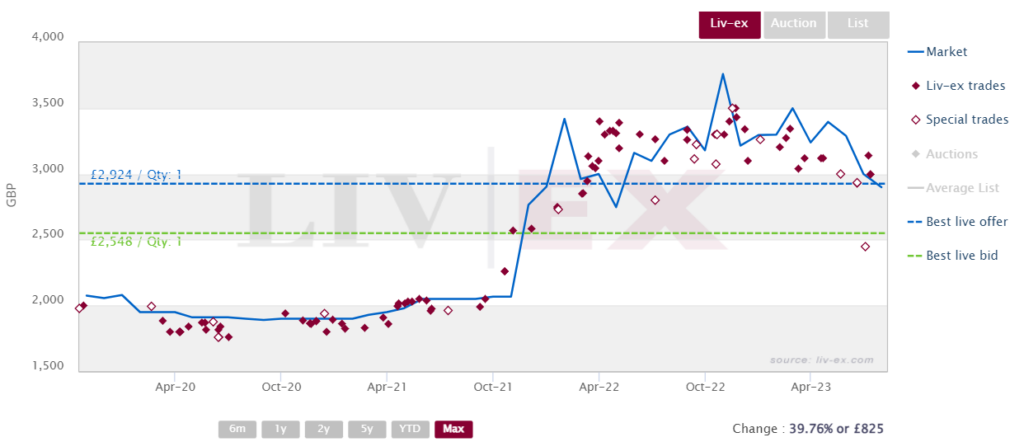

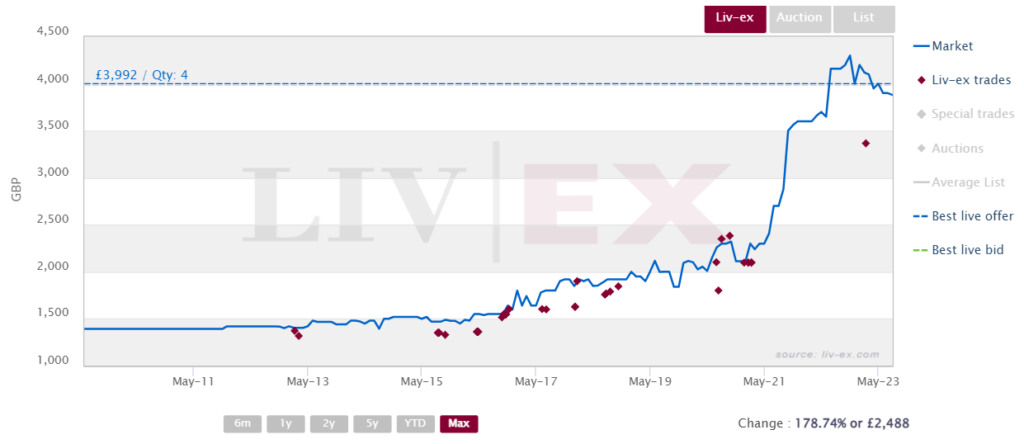

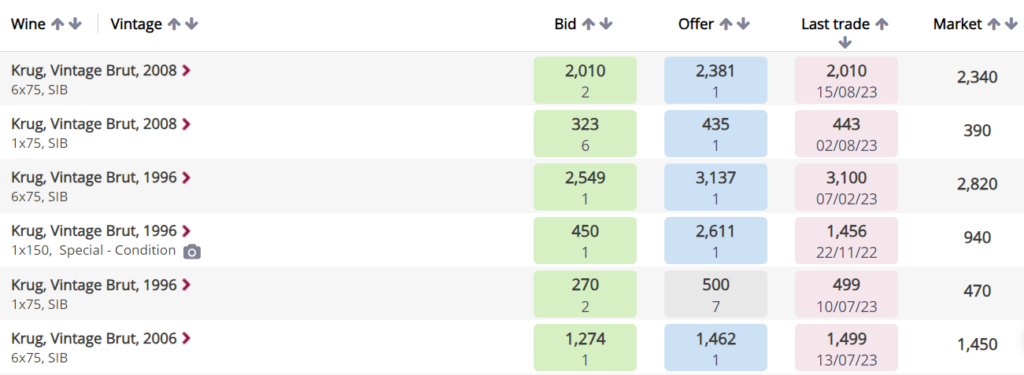

Krug 2006 trades on Liv-ex

Looking at Krug 2006 trades on Liv-ex, the last time it changed hands was at £2,998 per case, 3.4% above its Market Price of £2,900 per 12×75, suggesting prices may be rebounding slightly. However, even at this price, the wine is deemed to offer value according to the chart above. The Fair Value chart further suggests that even at a price of £3,680 per case, this wine would be considered to offer relative value.

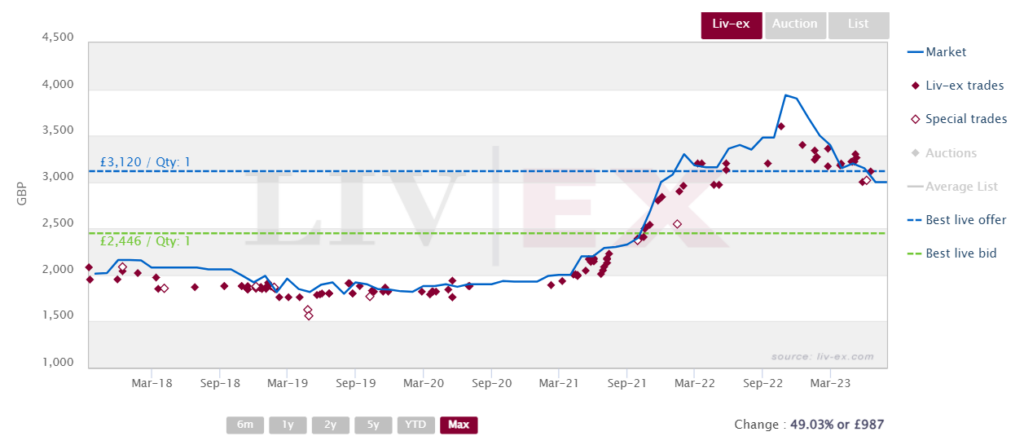

Krug 2004 trades on Liv-ex

A similar trend can be seen in the 2004 vintage, which last traded at £3,114 per 12×75, 3.8% higher than its Market Price. Liv-ex’s Fair Value methodology implies that the wine could reach a price of up to £3,621 per case and still offer relative value, so its current price represents an opportunity for buyers.

Krug 2000 trades on Liv-ex

Interestingly, the 2000 vintage is an exception, as it is currently trading below its Market Price. The wine has a current Market Price of £3,880 per case but last traded at £3,366 (13.3% below it). However, Liv-ex’s Fair Value methodology implies that the wine could reach a price of up to £4,141 per case and still offer relative value.

Amidst the Champagne market’s downturn, reflected in the negative month-on-month performance of the Champagne 50 index, there are signs that the pace of decline is moderating. It’s worth noting that the market remains very active, with some wines trading at even more favourable prices than what the Fair Value graph would suggest is fair. This market dynamic presents opportunities for buyers and sellers alike.

There are currently 96 LIVE opportunities for Krug on Liv-ex. Log in to the exchange to view them and trade.

In case you missed it:

Here’s what we’ve been reading:

- Liv-ex: The most traded wines in H1 2023

- Decanter: Australia’s wine industry faces years of oversupply after exports plunge

- Reuters: UK inflation pressure stays strong despite fall in headline rate

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines.