August Market Report

- All the major Liv-ex indices fell in July

- The Italy 100 showed stability, with wines from Tuscany and Piedmont increasing in value.

- Technical Analysis of the Champagne 50 index

- What are the best second wines of Bordeaux 2022 according to critics?

- A look back at Jean-Michel Cazes’ legacy at Château Lynch-Bages

- Where Château Lafite Rothschild: Where to next?

Navigating the storm

Emerging opportunities from the current downturn

*data taken on the 14th of August 2023.

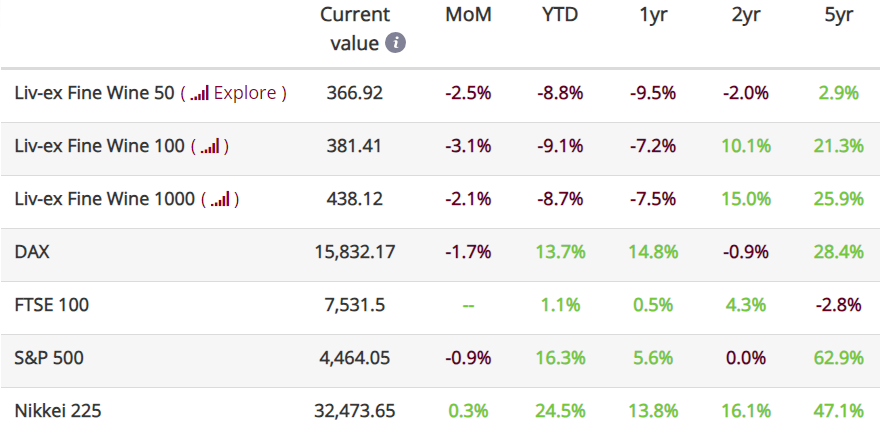

Last month saw further falls across the board, with all major Liv-ex indices declining in July.

The Liv-ex Fine Wine 100, the industry benchmark, was down 3.1% from the previous month to close at 381.41 and the Liv-ex Fine Wine 50 (which tracks the movement of First Growths) fell by 3.5% month-on-month. Year-to-date, the picture is much the same: all indices are down, with the Liv-ex Fine Wine 1000 falling 2.1% once again last month and 8.7% since the start of 2023.

July saw a monthly increase in trading activity in both value and volume as sellers adjusted prices to clear. The market breadth also expanded month-on-month, with 1,865 individual labels (LWIN 11s) trading on Liv-ex over the course of the month*.

There is little doubt that after a seven-year (almost uninterrupted) bull market favouring sellers, the ball is now firmly in the buyer’s court. The question is, are they ready to play and at what level?

* Liv-ex members can see price movements of individual wines in the LX100 in-app using the Indices Explorer.

Major Market Movers

The Italy 100 shows stability

While the broader market faced challenges, with the Liv-ex Fine Wine 1000 down 2.1% month-on-month, the Italy 100 index showed resilience, experiencing only a marginal 0.4% decline in July. Many wines from Piedmont and Tuscany saw price increases during this period, pointing to a pocket of stability in an otherwise turbulent market.

* All Liv-ex indices are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are the firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of over 620 of the world’s leading fine wine merchants. Because Liv-ex doesn’t itself trade, this data is truly independent and reliable.

Bartolo Mascarello, Barolo, 2016 was the biggest riser, up 20.5% in July. It was followed by Gaja, Barbaresco, 2017 (18.0%), along with Bruno Giacosa, Barolo, Falletto Le Rocche del Falletto di Serralunga d’Alba Riserva, 2000 (15.2%) and Fontodi, Flaccianello delle Pieve, Colli della Toscana Centrale, 2012 (11.9%).

Giacomo Conterno, Barolo, Monfortino Riserva, 2004 was also up 10.1%. The wine was awarded 100 points by Antonio Galloni (Vinous) in 2011 and again in 2021. In his more recent tasting note, Galloni calls the wine ‘one of the finest Monfortinos ever made’.

Chart of the Month

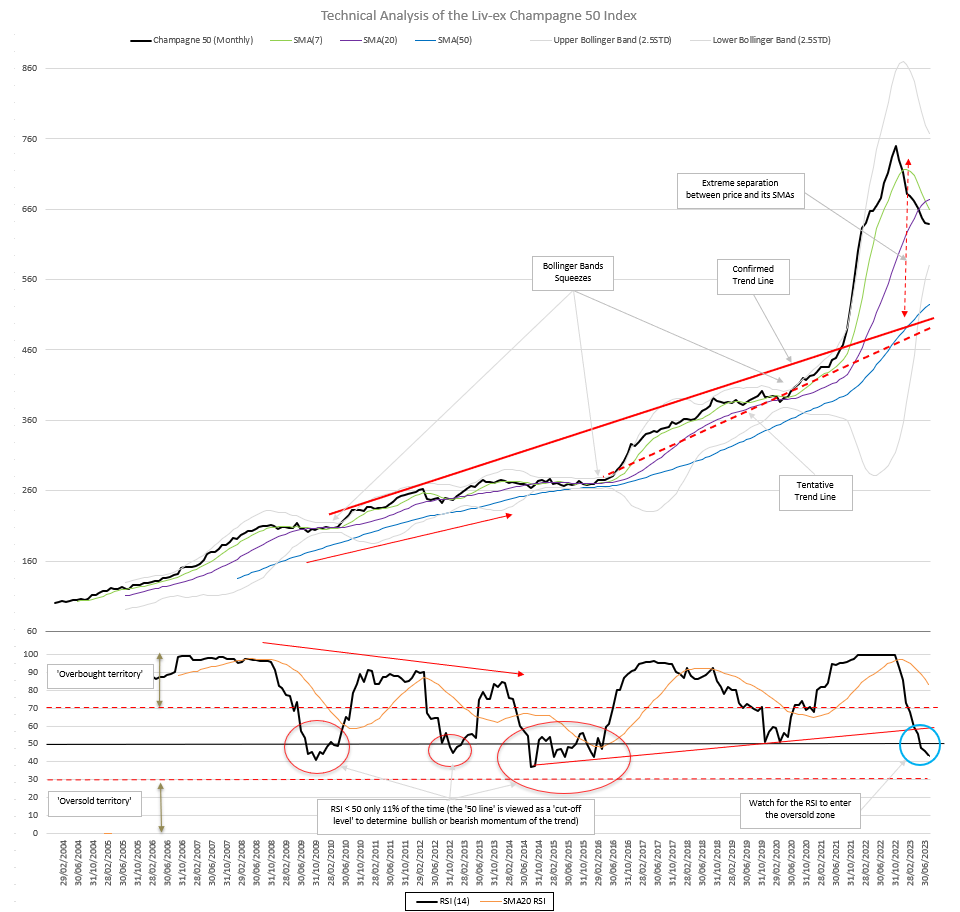

Technical Analysis of the Champagne 50 Index

What is technical analysis?

Technical analysis is a method of forecasting future market movements by studying previous movements, on the basis that historical trading activity can be a valuable indicator of the future This tool is common in financial markets and is applied here to Liv-ex indices in order to evaluate investments and identify trading opportunities.

The Champagne 50 undergoes a corrective phase following potentially excessive growth

Historically, the Champagne 50 index has been a perfect example of a trend-following market with very few corrections since 2003. This is evidenced by a long-term trendline (in red in the first chart above) and the price of the index going up steadily. The bullish trend has been well-supported by its Simple Moving Averages (SMAs, in green, purple and blue above), which can help isolate trends (or lack thereof) within a market by smoothing out price movements.

However, from April 2020 through to October 2022, the index price increased rapidly, moving away from its SMAs. A healthy positive trend would typically see prices and the accompanying 7-month Simple Moving Average (SMA7) rise at a 45-degree angle, unlike the sharp rise in the index price witnessed over those two years.

The Champagne 50’s Relative Strength Index (RSI), an indicator measuring whether an asset may be overbought or oversold, has been above the ‘50 line’ 89% of the time since its inception, which is commonly interpreted in technical analysis as the confirmation of an uptrend. The RSI had also been hovering around 95 and 100 for some time, which typically suggests the index is overbought and thus may undergo a corrective phase.

The widening of the Champagne 50’s Bollinger Bands – a visual representation of price volatility – from 2021 to 2022 raised concerns about potentially excessive volatility.

The subsequent price action since the Champagne 50’s peak in October 2022 has confirmed signs of excessive growth in the index’s trajectory since 2015. The first Fibonacci retracement level (23.6%), a horizontal line on the graph indicating where support and resistance of a trend is likely to occur, is at 596, though the index still had some distance to reach that point.

From a strong bullish trend to a bearish momentum

At present, the index’s momentum has clearly shifted towards bearish territory. This shift is made evident by the RSI, which not only breached its support line but is also trending towards the oversold zone (below 30).

Earlier this year, it could be thought that an opportune level for purchasing the index might follow a corrective phase. However, the ongoing correction exhibits no indications of having concluded, quite the opposite in fact.

What to look out for in the next index update?

In order to assess whether the index’s corrective phase is nearing a conclusion, the RSI’s relationship with the ’30 line’ (oversold territory) needs to be monitored, as does the price’s behaviour around the 23.6% Fibonacci level (596). A dip below this line could lead to an accelerated price drop.

The criteria for invalidating the long-term bullish strategy of the index are as follows:

- A price breach beneath the SMA50

- A bearish crossover between the SMA50 and SMA20 (bearing in mind that the SMA50 will progressively adjust upwards)

- A sudden break in the upward trendline we’ve delineated.

Critical Corner

The best second wines of Bordeaux 2022, according to critics

In the realm of Bordeaux wines, châteaux produce their flagship wines, known as the ‘first wine’ or ‘grand vin’, the pinnacle of their wine production. These wines are produced with meticulous care, featuring the finest grape selections and employing the most advanced winemaking techniques. The resulting wines represent the epitome of the châteaux’s reputation and craftsmanship.

Second wines, often referred to as ‘second labels’, come from the same estates (the second-best grapes) but can also be sourced from separate plots within the vineyard. Despite this distinction, they are produced with the same level of expertise and care as the first wine and can be a great alternative purchase to the more expensive grand vin. Price dependent of course.

First vs second wines: A difference in quality and complexity (and in affordability)

The châteaux’s first wine is superior in quality – more ageworthy and more intricate in flavour profile. These wines tend to exhibit the full potential of the estate’s terroir and winemaking capabilities. This is reflected in the higher scores received for the grand vin. In contrast, second wines offer a taste of the châteaux’s signature style but may lack the same depth and aging potential.

Châteaux’s first wines are considered their most prestigious offering, and with that comes a significant price tag. For those seeking a taste of Bordeaux’s excellence without breaking the bank, second wines provide an accessible entry point while maintaining the essence of the chosen château’s heritage.

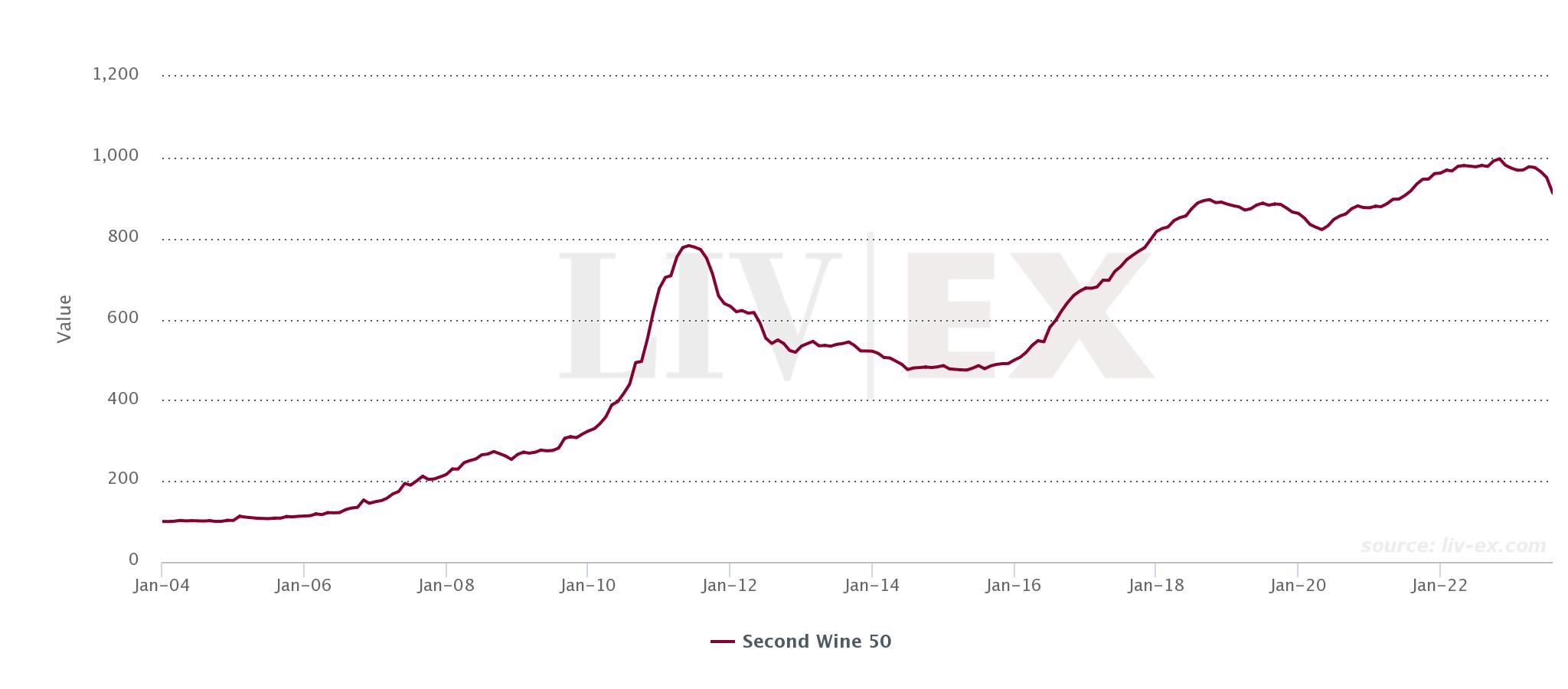

The Liv-ex Second Wine 50 index

The Second Wine 50 index, which monitors the performance of the ten most recent physical vintages of five second wines of Bordeaux First Growths, has demonstrated a promising upward trend with a 2.8% increase over the past five years. It has recorded a 6.3% decline year-to-date, mirroring the rest of the fine wine markets’ falling prices, suggesting that the golden age of second wines may be coming to an end.

Indeed, with Chinese wine consumption plummeting, the demand which drove prices up from the late 2000s onwards is dwindling. At the time, the price of some second wines of the most prestigious brands (Carruades de Lafite, Le Petit Mouton de Mouton Rothschild) were skyrocketing regardless of vintage, with Carruades de Lafite 2006 peaking at £3,875 per dozen in 2011 despite only receiving 90 points from Robert Parker. Meanwhile, Château Léoville-Las-Cases 2006, a Second Growth with 95 points from Robert Parker, peaked at £1,400 per dozen in 2011 and is now available at a Market Price of £1,550 per case.

Amid the current turbulent market conditions, buyers may be placing more attention on quality rather than brand name alone, bringing more attention to second wines’ critic scores, for example.

What were the highest-rated second wines of Bordeaux 2022?

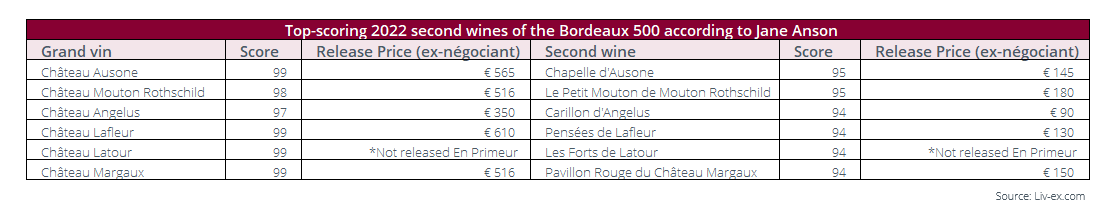

According to William Kelley (The Wine Advocate), ‘the quality of second wines is especially high [in 2022]’. Looking at Wine Advocate scores for any second wine in the Bordeaux 500, the top-scoring one is Pensées de Lafleur 2022, the second wine of Château Lafleur in Pomerol, which received a score of 95 points. Following behind are six other second wines, all having received a score of 93 points (see table below).

Looking at Jane Anson’s scores, her top-scoring second wine from the vintage is Chapelle d’Ausone 2022, the second wine from Château Ausone, which she gave a score of 95 points.

Neal Martin’s top-rated second wine is Les Forts de Latour 2022, the second wine from Château Latour, with 95 points. It’s worth noting that this wine has not yet been released, as Château Latour has withdrawn from the En Primeur system, and won’t be available to buy for a few years.

Despite some variations in the scores from Jane Anson, the Wine Advocate, and Neal Martin, three second wines have earned a place among the top-rated wines across these critics’ reviews: Pensées de Lafleur 2022, Les Forts de Latour 2022, and Le Petit Mouton de Mouton Rothschild 2022.

While Château Latour does not release its wines En Primeur, Château Lafleur and Château Mouton Rothschild do. Pensées de Lafleur 2022 was released at €130 per bottle compared to €610 for the grand vin. Le Petit Mouton de Mouton Rothschild 2022 was also released at a lower price of €180 per bottle compared to €516 for the grand vin.

This pricing distinction makes the second wine a more accessible option for buyers looking to purchase wines with the essence of the prestigious châteaux without the higher investment needed to acquire their first wines.

News Insight

Jean-Michel Cazes’ legacy at Château Lynch-Bages

In June, Bordeaux proprietor and ambassador Jean-Michel Cazes passed away, leaving behind an impressive legacy.

As the owner of Château Lynch-Bages and Ormes de Pez in Bordeaux, Jean-Michel Cazes transformed the Bordeaux wine industry through his pioneering efforts in wine tourism and the co-creation of AXA Millesimes, a group of estates acquired by the French insurance business including Châteaux Pichon-Baron, Suduiraut and Petit Village in Bordeaux.

Cazes’ impact on Bordeaux as a whole cannot be understated, but here we will focus on Lynch-Bages and how the estate has performed in the last 20 years, which can partly be attributed to the improvements he made while he was at its head.

A look at Château Lynch-Bages prices indexed over the past 20 years shows a steady increase with few dips and troughs, even amid a challenging macroeconomic environment such as the 2008 financial crisis.

The effects of a price correction following excellent 2009 and 2010 vintages (and corresponding strong price hikes) can also be seen on the chart above, followed by more consistent growth from 2016 onwards.

Additionally, Château Lynch-Bages has demonstrated its strength by consistently outperforming the Left Bank 200, a sub-index of the Bordeaux 500 which comprises 10 vintages of 20 wines from the Left Bank.

In the 1855 Classification, Château Lynch-Bages was established as a Fifth Growth. However, in the latest edition of the Liv-ex Classification, which considers trading activity as well as price, it fell into the Second Tier of wines, a testament to Cazes’ dedication to elevating the estate’s reputation and quality.

In the Power 100 rankings, which measures trade activity and performance by value and volume, year-on-year price performance and average price of wines in a brand, the Lynch-Bages estate secured the 62nd position in 2021 and 87th position in 2022.

The estate’s pursuit of excellence yielded praise from critics and experts worldwide. In 1988, Lynch-Bages 1985 was named Wine of the Year by the Wine Spectator. More recently, Jane Anson crowned the 2014 vintage as her wine of the year. The 2022 release received a score of 95-97 points from Neal Martin.

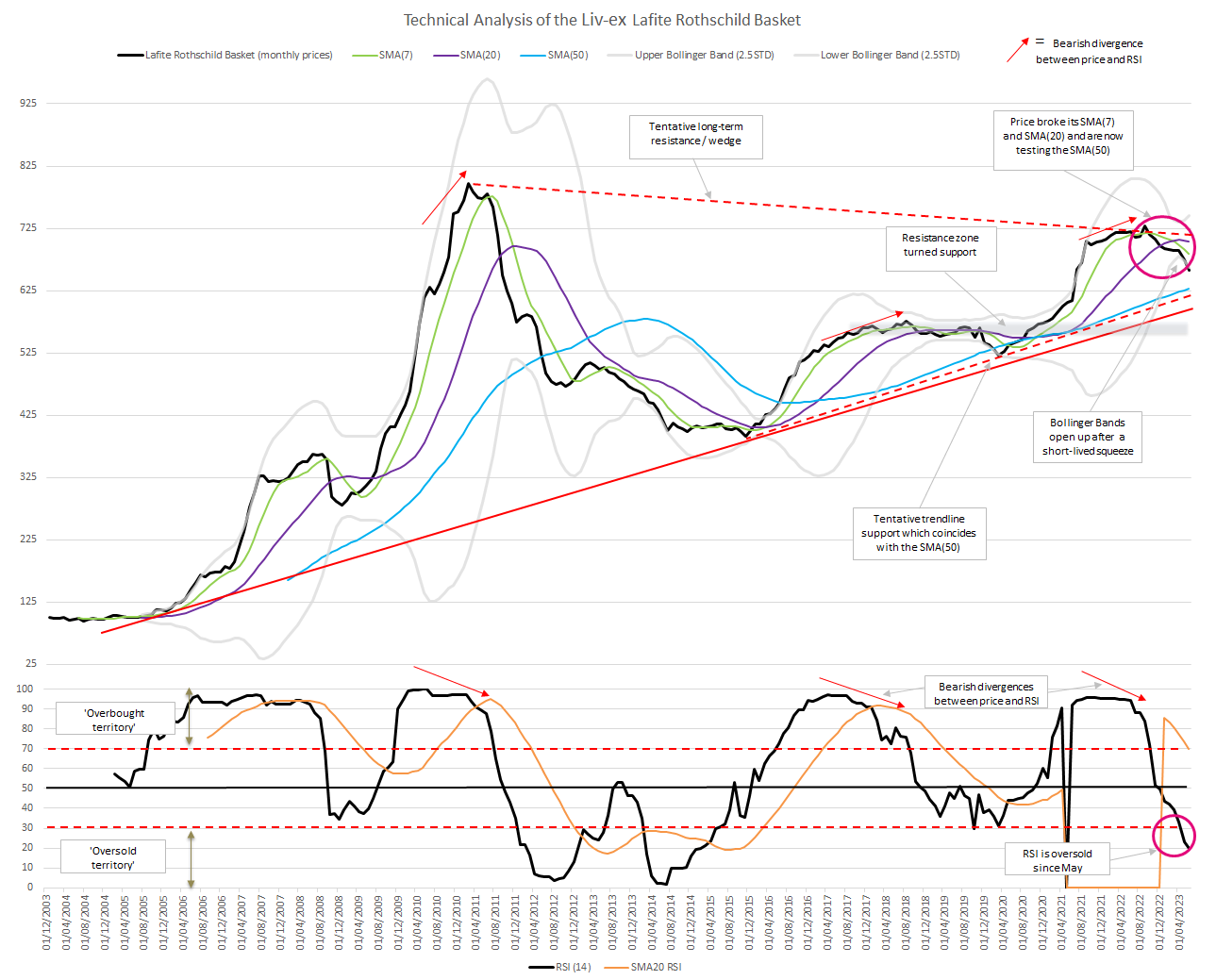

Final Thought: Château Lafite – where to next?

Year-to-date, the last ten physical vintages of Château Lafite Rothschild have seen their index value decline. Is this the end of the downward trend, or can it go any lower? We turn to Technical Analysis to shed some light on the price movements of this prestigious label.

The graph above shows that since reaching its all-time peak in February 2011, the Lafite index has been unable to achieve a new high. Instead, it has been consolidating within what could shape up as a prolonged wedge pattern or resistance, suggesting uncertainty in the market.

In September 2022, the Lafite index reached a high of 720, outperforming performing its Simple Moving Average (the 7-month SMA). After that, it underwent a period of correction, and its value went down.

This correction began when the Relative Strength Index (RSI) broke the 20-month SMA and then went below the ‘70 level’ in November 2022, which is considered a valid sell signal. As the RSI dropped, it fell sharply into the oversold or ‘acceleration’ zone (below the ‘30 level’), reflective of feelings of insecurity in the market.

The value of the Lafite index broke two averages in 2022, the SMA7 and SMA20, one after the other. Right now, it’s being tested against another longer-term average, the SMA50, which coincides with the tentative ascending trendline.

Looking at the recent movements of Lafite’s value, the Bollinger Bands (BB) are beginning to open up again after a short-lived ‘squeeze’, ending a period of low volatility (as seen in grey on the chart above). The index’s price recently dropped outside the lower BB, a relatively rare occurrence which can indicate the market may be oversold.

The current trendline reflects the uncertainty in the broader fine wine market but could also be partly explained by a strong decline in wine imports and sales in Mainland China, a traditionally large consumer of Lafite. Unless buyers come strongly into the market now, the index level is likely to fall to the next support levels, around 550. What happens after that remains to be seen.

Fill in the form below to claim your complimentary copy of the report.

[insert form code here]