- Increased market confidence, ready money and a sense of dwindling stocks (real or not) led to a surge in the secondary fine wine market, powering a new bull run.

- Blue chip labels rebounded with Lafite Rothschild leading in terms of performance.

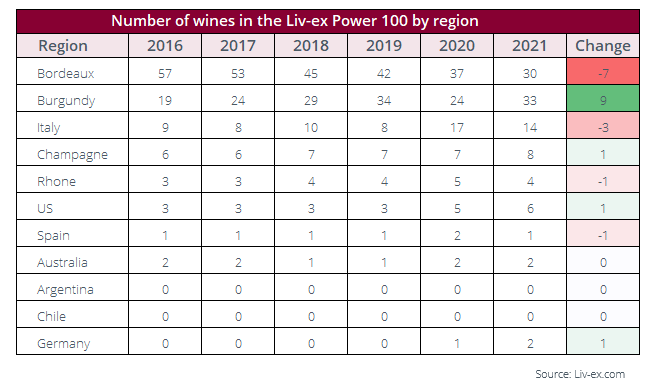

- Burgundy was on the rise once more with strong price performances from its leading estates.

- Champagne continued to build momentum as several of its key brands rose this year.

- Italy lost some brands from the top 100 but held on to its 15% trade share, while Sassicaia cemented its place in the top 10.

- The US led the rest of the world with Californian brands dominating.

Print and read offline instead.

Each brand receives digital badges or medals in a variety of formats to mark and celebrate its position in the rankings.

Download the digital badges or medal for the Power 100 here.

Introduction

Last year’s Power 100 revealed a traditional fine wine landscape that had been (or at least appeared to be) completely up-ended. For years, since the end of the China-driven bull run in 2011, the market had been broadening and diversifying, led first by demand for Burgundy, then Champagne, Italy, the US, Rhône and so on.

In 2019 the story was all about Burgundy which reached a record trade share of 19.6% (by value). In 2020, however, with prices for the leading domains plateauing and buyers seeking value elsewhere, the region’s trade share stalled.

Into its place moved Italy which became the ‘hot topic’ of last year’s Power 100, while boasting an all-time trade share high of 15.3%.

Ten Italian wines qualified for the first-time last year, while Sassicaia, Gaja, Ornellaia and Masseto all ranked in the top 10 – their highest positions ever.

The 2020 list, with huge leaps made by wines from outside the traditional strongholds of Bordeaux and Burgundy, showed just how much the market was changing. Like the latest James Bond release, it was very much a list that reflected the times. The 2020 Power 100 list was a snapshot of the period October 2019 to September 2020 and this is important to bear in mind when considering how the list turned out.

At the end of 2019 the fine wine market was facing strong headwinds. All of the major markets were gripped by one form of crisis or another. Hong Kong was rocked by political protests, China and the US were at loggerheads over trade tariffs, as were the US and European Union, while uncertainty over Brexit weighed heavily on the UK’s future prospects.

And all of this was before the coming of the Covid-19 pandemic. This cocktail of obstacles impacted the secondary market in different ways. Asia, the big driver of Burgundy, was subdued, while added tariffs on French wines threw US buyers into the arms of Italian labels and Champagne which were exempt.

Like any market, the fine wine secondary is strongly influenced by global events. From a relatively bleak outlook at the end of 2019, through the doldrums of the early days of the pandemic in 2020, the fine wine market has ended up powering through into a fresh bull run.

Considering the events of October 2020 to September 2021, therefore, helps explain the extensive changes to this year’s list and what labels have returned to prominence and which have settled back to lower positions.

After an initial setback during the uncertainty of the pandemic, the fine wine market rebounded in the summer of 2020 and has not looked back. Financial stimulus from governments and central banks worldwide combined with buyers with extra cash in hand (unable to travel or go out) led to a boom in wine buying at all levels.

The tension regarding the future of post-Brexit trade has also eased (at least for now) and the election of Joe Biden as President of the United States last November has resulted in the complete removal of tariffs on all European wines.

The news in March that the tariffs were being temporarily suspended (followed by their complete removal in June) caused a spike in US buying of Bordeaux and Burgundy.

The overall impact of ready money, thirsty collectors and emptier cellars has been a greater focus on fine wine ‘classics’. Although Bordeaux continues to lose secondary market share overall to the likes of Tuscany, Piedmont, Champagne, the Rhône and California, the First Growths and other leading wines on the Left and Right Banks have shown their strengths as desirable labels once more this year.

It is also important to remember that stocks of the world’s great wines are dwindling. This year’s vintage in much of Europe has been widely lamented as pitiful both in quantity and (it would seem) quality.

This is especially bad for Burgundy which has been experiencing shrinking harvests for the better part of a decade now, vineyards hit time and again by destructive bouts of frost and hail.

And yet demand for the region’s grands and premiers crus continues to mount.

Meanwhile, in Bordeaux there are also looming ‘shortages’. This is a result of the deliberate action of the châteaux who are releasing less stock En Primeur.

For the most part this is not helping drive prices in the secondary market as buyers are well aware that there is plenty of unsold stock. This is part of the reason for Bordeaux’s ever-smaller share of trade by value.

On the other hand, for the most bankable estates (such as the First Growths) there is a mounting sense of a scramble for remaining stocks – at least of ‘on’ vintages.

As such, while the overall trend of the secondary market remains very much one of diversification and broadening, it has also been a year of rebalancing and the return of the blue chips.

Top ten

A glance at the top 10 wines in the list shows that there has been a near complete change from last year.

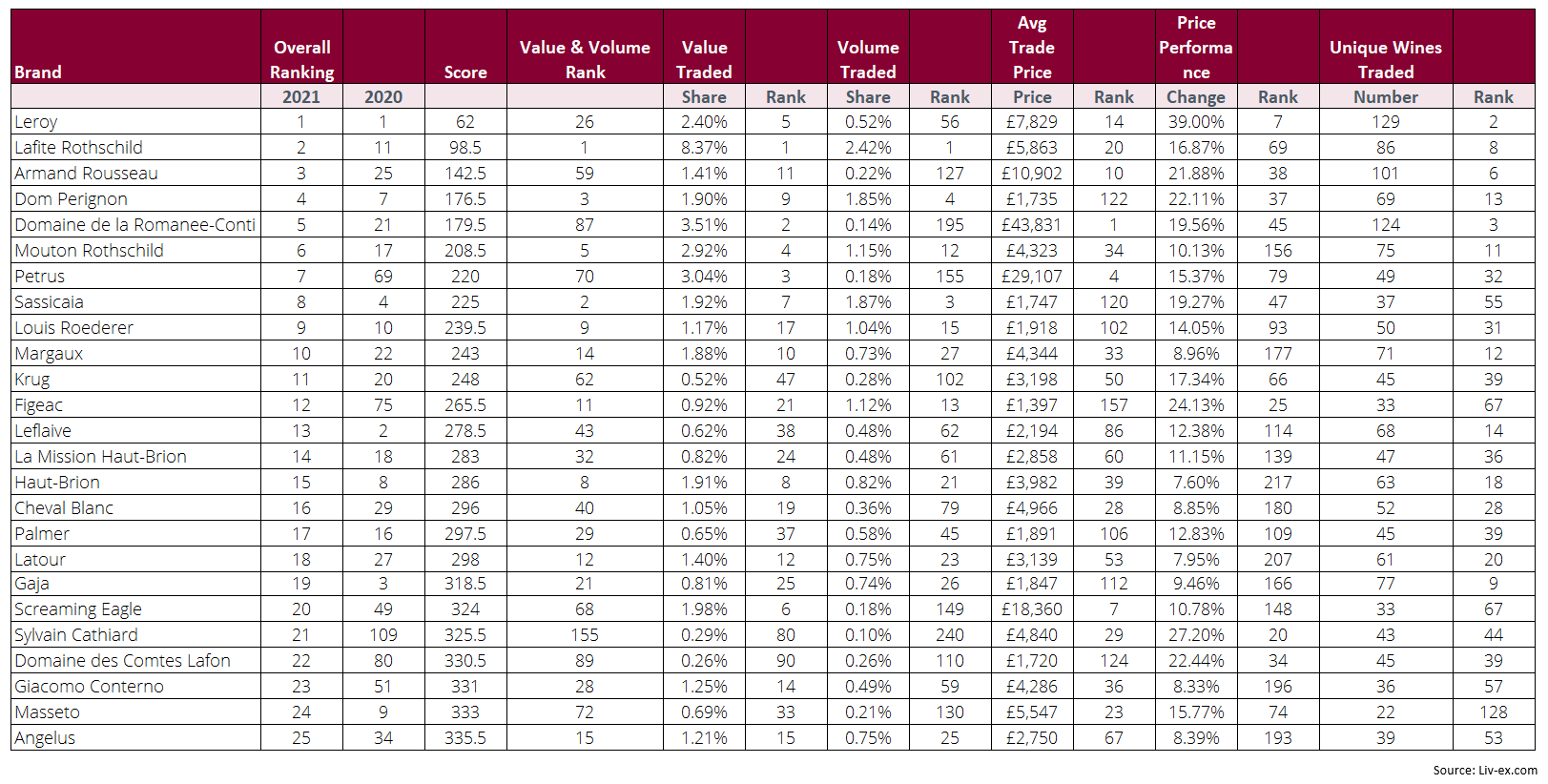

The only unchanged component (indeed the only label that remains unchanged on the list from last year) is Domaine Leroy, which has retained its number one position.

Three other brands, Dom Pérignon, Sassicaia and Louis Roederer, are the only survivors from last year’s ‘storming of the Bastille’.

The six other places at the top are all taken back by the habitual market leaders. Château Lafite Rothschild for example has marched back from 11th place to second; while fellow First Growths Mouton-Rothschild and Margaux have also risen.

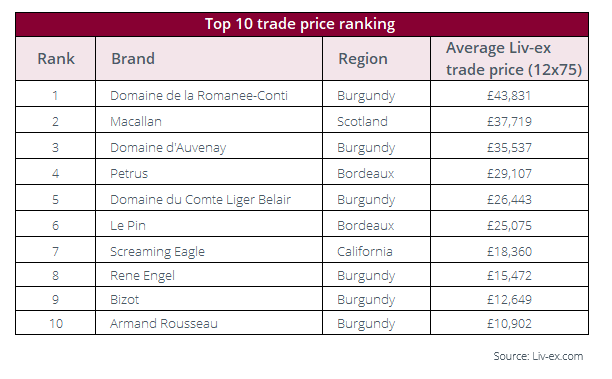

Armand Rousseau (a former list-topper) is back up to third and fellow Burgundian Domaine de la Romanée-Conti is back into the top 10 after a strong year of demand pushing prices once more.

Petrus, which had fallen all the way to 69th in the rankings last year, has bounced all the way back to 7th due to strong average prices and high trade by value.

The fact that Dom Pérignon, Louis Roderer and Sassicaia have remained in place shows that demand for top Champagne and Italian wines has not abated. Yet there is no denying that this top 10 shows that buyers have flocked back to the blue chip labels at the first opportunity, seeking comfort and safety in bankable names while increasingly aware of their diminishing physical presence.

Download digital badges or medals for the Power 100 here.

Bordeaux

The past year for Bordeaux has been mixed. On the one hand, the First Growths and certain other estates have charged back into the limelight, but at the same time more Bordeaux dropped out of the list this year and its overall trade share by value continues to decline.

In addition to Lafite, Mouton and Petrus’s top positions, Figeac raced up the charts from 75th place last year to 12th this year.

The Right Bank estate is starting to emerge as an increasingly strident brand and one that is hotly tipped for some form of promotion in the up-coming St-Emilion classification.

A total of 26 Bordeaux labels rose in the rankings overall this year (across all 421 qualifying wines, not just the top 100). There were also 13 Bordeaux wines that qualified for the first time. Like all other regions, buyers are expanding their pool of domains they’re prepared to buy from, bringing more wines to the secondary market.

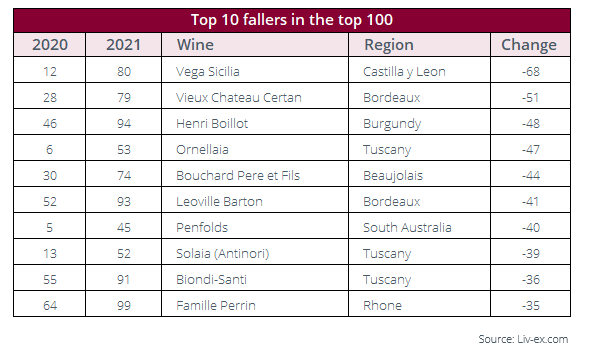

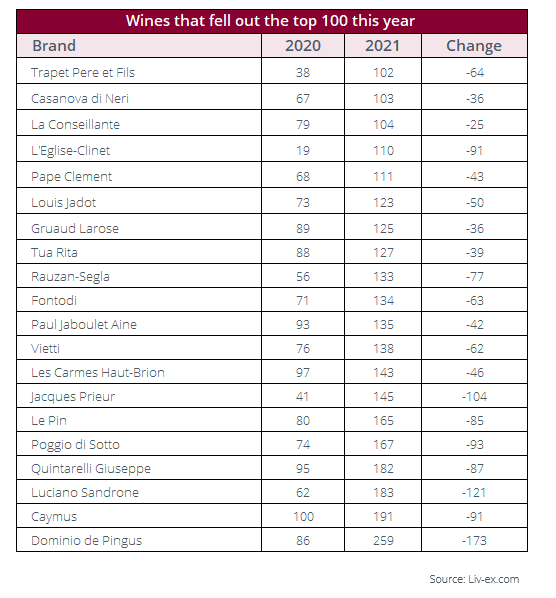

On the other hand, 52 Bordeaux wines went down in the rankings and 10 labels dropped out of the top 100 altogether. Among them, very surprisingly, was Le Pin, which dropped all the way to 165th – 85 places in total. This is a very odd result given the dominance of blue chip labels this year but Le Pin appears to have been off buyer’s radars of late and its price performance ranking (a key determinant in the rankings) was 340th.

Download digital badges or medals for the Power 100 here.

Burgundy

In 2020 Burgundy seemed to have taken a step back from the brink of global domination. The list in 2019 was all about how far and fast the region was rising but as prices topped out, so its momentum stalled and a total of 10 Burgundian labels dropped out of the Power list last year.

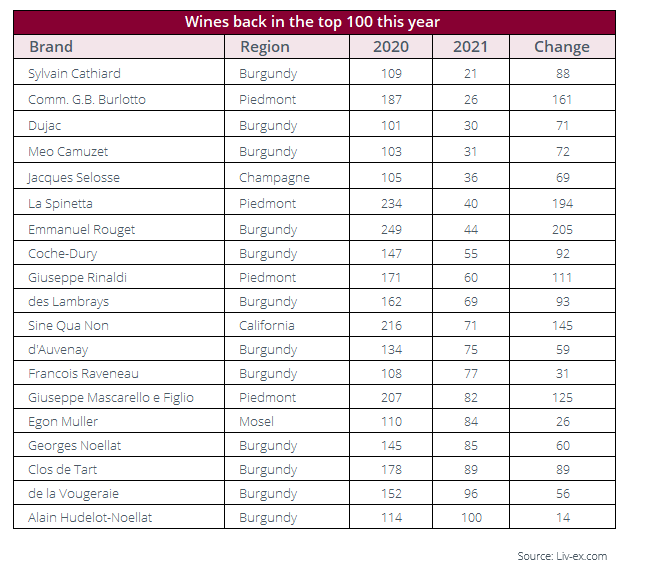

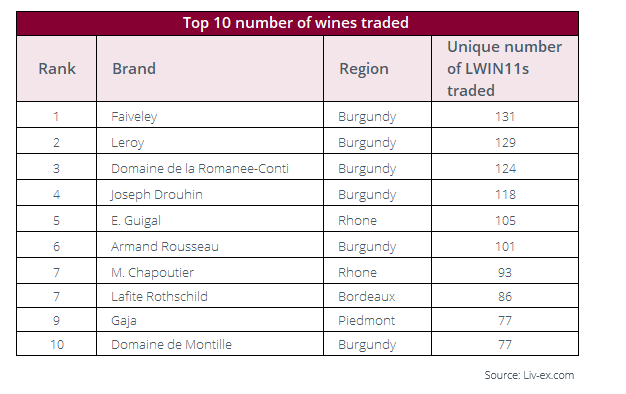

Burgundy though is definitively back. Its share of trade by value in the period October 2020 -September 2021 was 20.7%. Eight wines have jumped back into the list this year and, as already discussed, sustained demand for the most blue chip of labels has seen Leroy retain its position while Armand Rousseau and DRC return to the upper echelons.

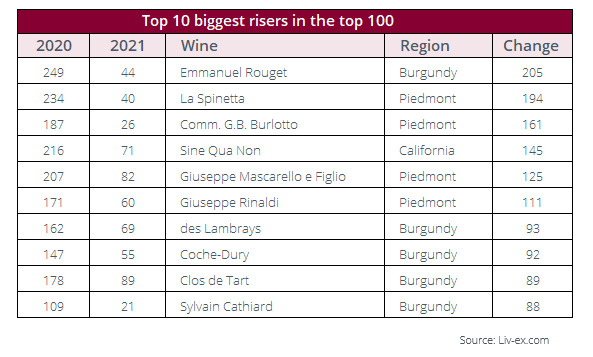

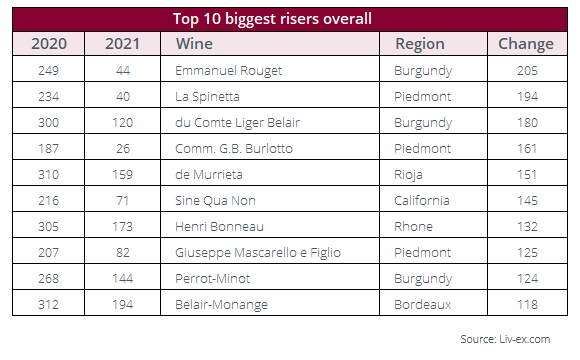

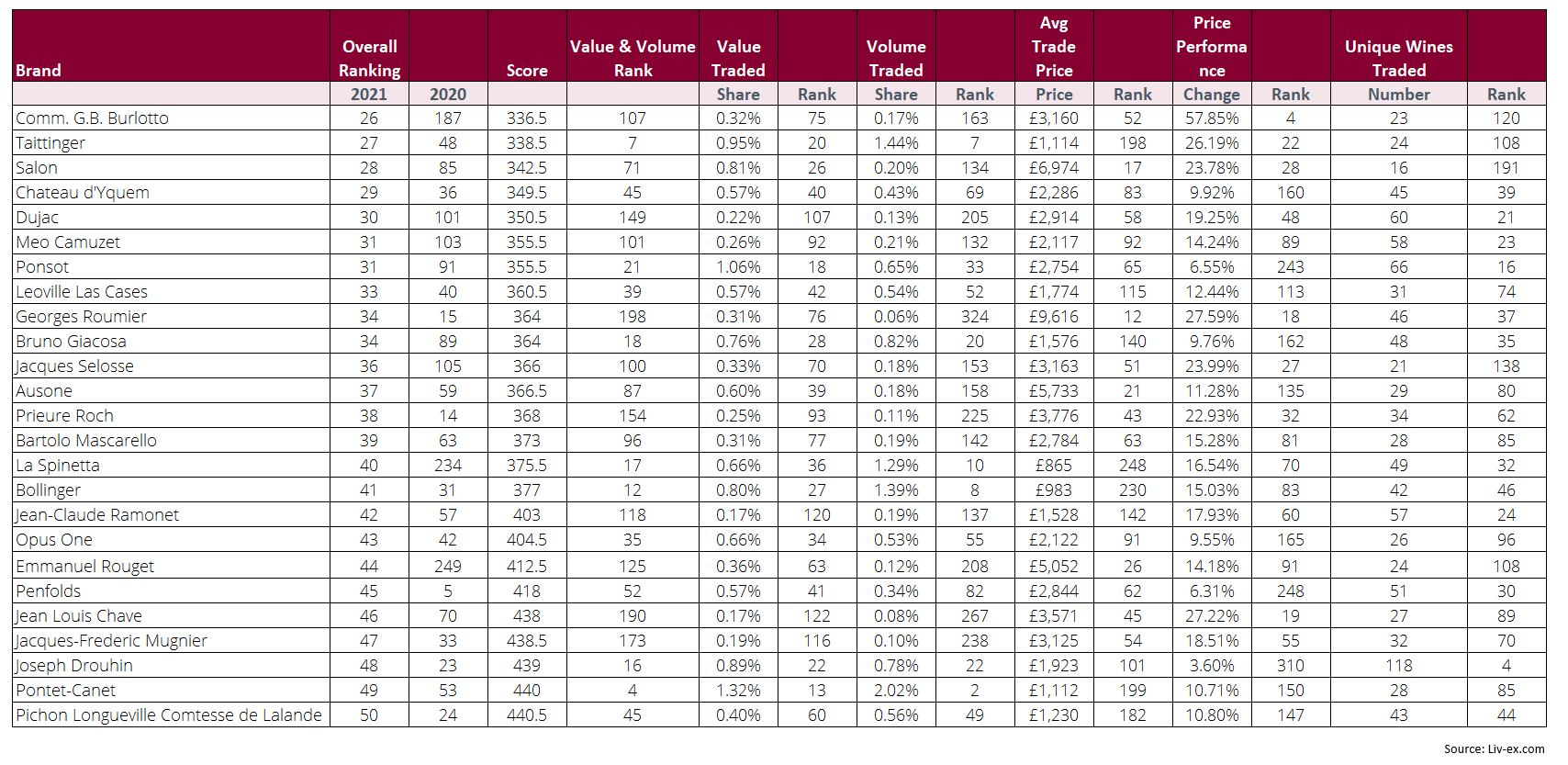

Some of the biggest risers this year are Burgundians. Emmanuel Rouget for example vaulted 205 spots from 249th in 2020 to 44th this year.

Other names returning to the 100 include Clos des Lambrays, Coche-Dury, Clos de Tart and Sylvain Cathiard. Earlier this year it was pointed out that Morey-St-Denis was a source of under-valued grand cru Burgundy and the market appears to have taken note.

Download digital badges or medals for the Power 100 here.

Champagne

Champagne is now well-established as a driving power in the fine wine market. Its overall share of trade by value between October 2020 and September 2021 has not changed much from the average of the last few years – 8%.

Nonetheless, its two brands at the very top of the list, Dom Pérignon and Louis Roederer (Cristal), both improved on their positions from last year; Dom Pérignon rising to fourth place overall and Louis Roederer inching up from 10th to 9th. Krug too, which unveiled its long awaited 2008 vintage this year, climbed nine places to 11th.

More Champagne brands rose than fell overall and no brands from last year exited the top 100. One wine in fact rose onto the list, Jacques Selosse all the way to 36th.

With strong bands, pricing, distribution and availability, Champagne keeps providing steady returns and accessibility for new and established buyers of fine wine.

Download digital badges or medals for the Power 100 here.

Italy

Last year’s list was all about Italy, the new, surging power in fine wine. The country’s share of secondary market trade rose from 8% to a new high of 15% and from eight wines in the Power 100 to 17 – many of them at all-time highs or brand new entrants.

As was the case with Burgundy in 2019, however, rapid rises are often followed by a sharp halt as the market adapts to new wines and higher prices.

This is somewhat the case with Italy this year. Three wines, Luciano Sandrone, Poggio di Sotto and Quintarelli Giuseppe, have fallen out of the top 100 – dropping quite sharply.

Overall, as with Bordeaux, more Italian labels have declined than risen throughout the list of qualifiers. On the other hand, 21 wines qualified for the first time and many of those wines that have stayed on the list have further entrenched themselves in the new hierarchy.

Sassicaia for example lost a few places but remains the seventh most traded label by value and third most by volume, with a price performance ranking of 47th.

Gaja, likewise, is a top 30 producer for trade by value and volume as is Bruno Giacosa. Furthermore, between the two key producing areas of Tuscany and Piedmont, Italian trade by value for October 2020 to September 2021 was still 15% – so it has not yielded ground overall.

Download digital badges or medals for the Power 100 here.

Rest of the World

Across the rest of the world, the main area of importance is the US. Like Italy, trade in US wines – overwhelmingly Californian – is on the rise.

California’s trade share for the period in question was 7.6% of the total, well above the Rhône (4.1%) and just ahead of Piedmont (6.3%).

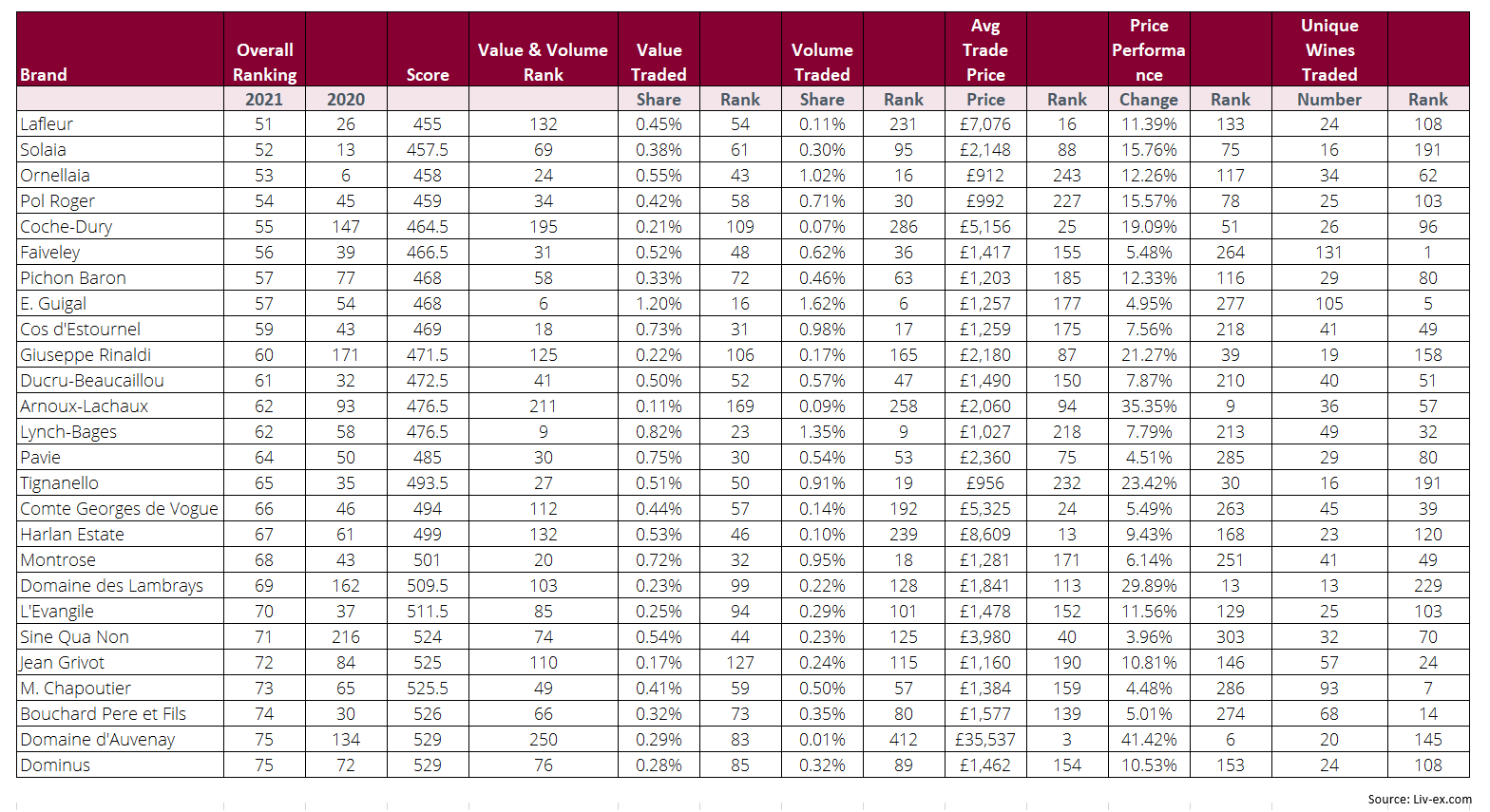

The US gained one new entrant into the top 100 this year – Sine Qua Non making a big jump to 71st place, buoyed by its strong average trade price and overall value traded.

The US, therefore, had a strong trading period that has kept it in firmly touch with the other ‘second tier’ regions.

The same can not be said for Australia. After a record-breaking year in 2020, China’s introduction of sizeable tariffs of 180% to 200% on wine imports in response to apparent ‘dumping’ of low value stocks hit trading activity hard.

Having risen to an all-time high of fifth place last year, leading label Penfolds Grange fell to 45th in the rankings this year.

It’s not all doom for Australia though, three wines; Torbreck, Clarendon Hills and Henschke (driven by demand for Hill of Grace), all rose on the back of strong trade.

Download digital badges or medals for the Power 100 here.

Conclusion

As discussed at the beginning, this year’s list looks and feels as if there has been a rebalancing of the market.

Blue chip labels are back on top where one would expect them to be. Bordeaux is a steady but no longer domineering presence, Burgundy as the next premier wine region feels active, as do Champagne, Italy and the US which are as strong or stronger than they have ever been.

And it continues to be a broader market. October 2020 to September 2021 saw another sizeable increase in the number of wines and brands trading and therefore the number eligible for inclusion.

In the previous year, new records were set with 8,734 wines trading, from 1,420 producers and 325 of those producers qualifying for the Power 100.

This year it was 11,839 wines traded (+35.6%), from 1,668 producers (+17.5%), with 421 candidates considered (+29.5%).

And the scope of the fine wine market is becoming ever wider too. Brand new candidates that qualified this year included Weingut Moric in Burgenland, Château Musar in Lebanon, Dow’s and Warre’s Ports, Jim Barry in Australia, Jo. Jos. Prüm, Frostmeister Geltz Zilliken and Willi Schaefer in the Mosel, Alvaro Palacios and Clos Mogador in Catalonia and many others.

We have also seen the first appearance of spirits; Scotch brands Glenfarclas and the Macallan and Hennessy Cognac – a sign of things to come?

At the time of writing the fine wine secondary market is at an all-time high, having surpassed the previous peak set in summer of 2011. It has done so on the back of renewed vigour in the classic staples of fine wine collecting and investment but also supported by the broadest market yet seen.

The kings may have been restored to their thrones but the number of contenders for the crown only appears to be growing.

Download digital badges or medals for the Power 100 here.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £80m worth of wine and the ability to trade with 550 other wine businesses worldwide. They also organise payment and delivery through their storage, transportation, and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Methodology

To calculate the rankings, we took a list of all wines that traded on Liv-ex in the last year (from 1 October 2020 to 30 September 2021) and grouped these by brand. As is now standard, Burgundy labels with both maisons and domains were combined as one.

We then identified brands that had traded at least three wines or vintages, and had a total trade value of at least £10,000.

Brands were ranked using four criteria: year-on-year price performance (based on the Market Price for a case of wine on October 1st 2020 with its Market Price on September 30th 2021); trading performance on Liv-ex (by value and volume); number of wines and vintages traded; and average price of the wines in a brand.

More than 11,839 different wines were traded on the exchange in this period. These were grouped into 1,668 brands, of which 421 qualified for the final calculation. The individual rankings were combined with a weighting of 1 for each criteria, except trading performance, which had a weighting of 1.5 (because it combined two criteria).

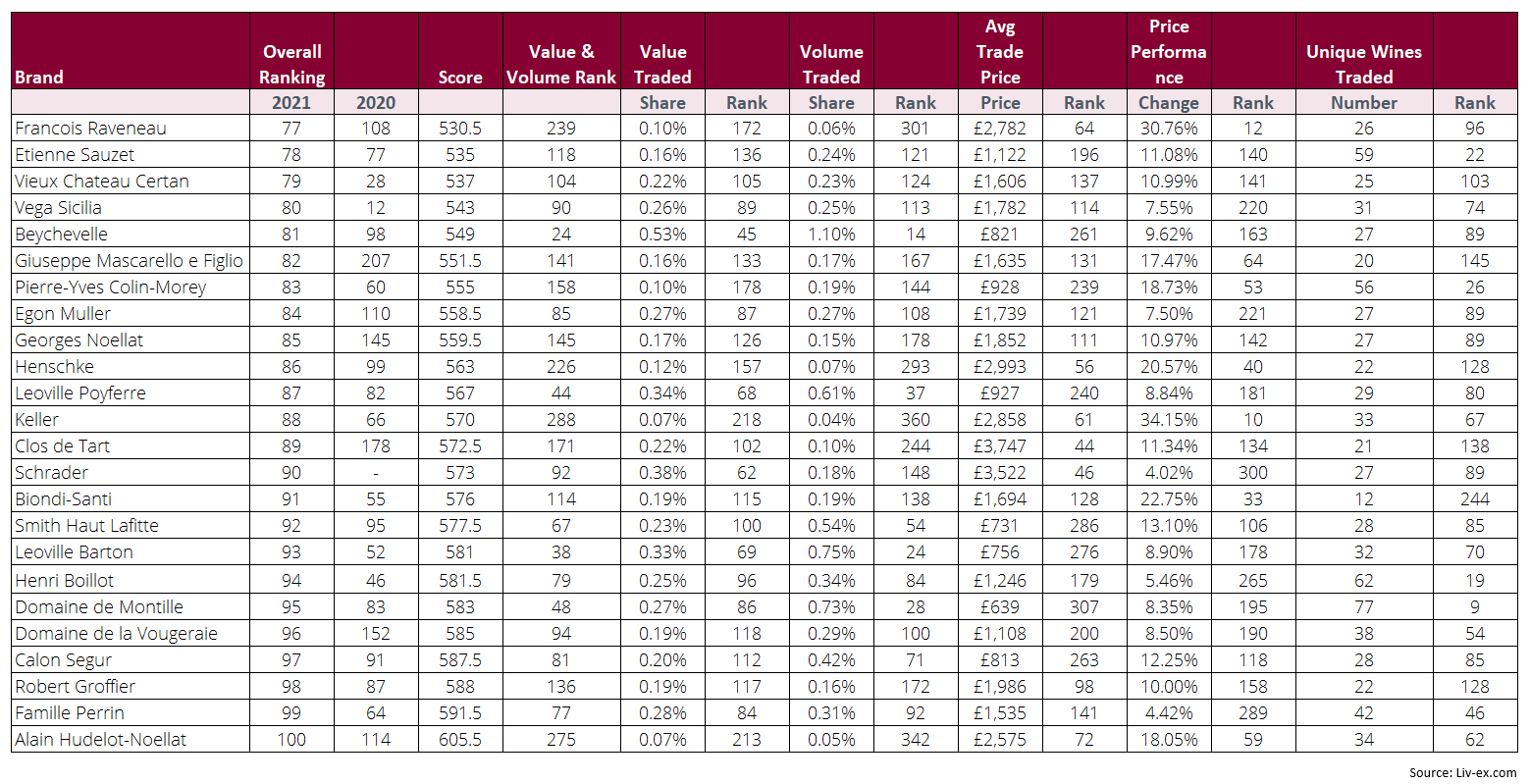

Full ranking table

Digital Badges

This year, Liv-ex has created digital badges or medals to celebrate each brand’s Power 100 ranking. They are available in standard social media sizes for easy sharing (#Power100) and .eps format for adding to web pages.

Download the digital badges for the Power 100 here.