The Fine Wine Market in Q1 2023

Introduction

The first quarter is acquiring a reputation for being a turbulent quarter. This time last year, the Russian invasion of Ukraine had exacerbated inflation concerns, while the knock-on effect of war caused oil, gas and metals to rise in price which further impacted struggling global supply chains. To add to the situation, China — a major buyer on the secondary market — endured a severe wave of Covid-19, turning its mega-cities into ghost towns.

One year on, the world is once again witnessing major turbulence but this time, it’s financial in nature. The collapse of Silicon Valley Bank sent shockwaves through markets, closely followed by the controversial UBS takeover of its rival Credit Suisse. Surprisingly, the impact of these events on markets has been minimal. The Federal Reserve reiterated its confidence in the US banking system and raised interest rates by 0.25% for two consecutive months, and the ECB followed suit, raising them by 0.50% in February and March.

In the UK, while a recession is still on the cards at some point this year, the decline in GDP is less dramatic than predicted, in part due to falling energy prices. Inflation still presents a risk and was stronger than forecasted last quarter. Jeremy Hunt’s UK budget faced criticism from the UK drinks industry due to alcohol duty increases in line with inflation.

Following plans from the government to raise the retirement age, France has been plunged into a chaos of strikes and protests. The disruption in transport and supply chains is strongly felt, as railways and refineries are among the sectors striking.

China’s annual inflation rate fell to 1.0% in February, from 2.1% in the prior month. This was the lowest number since February 2022. The unexpected drop was caused by weak consumer demand and a fall in commodity prices, as consumers stayed cautious despite the lifting of Covid-19 restrictions. Nonetheless, hope is on the horizon in China, with both outward and inward tourism slowly returning, albeit it more gradually than many hoped.

Among all this turbulence, the fine wine market has remained remarkably steady. But as we enter the second quarter, a cautious tone remains stubbornly in place.

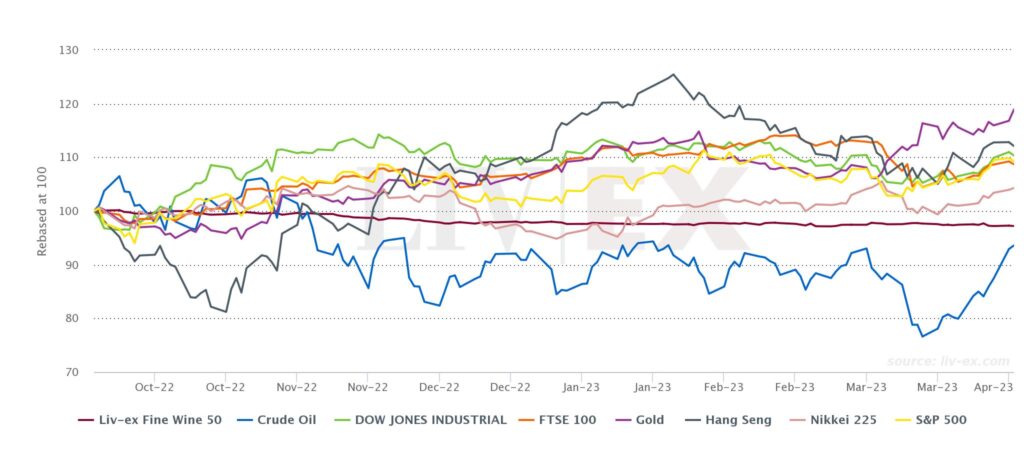

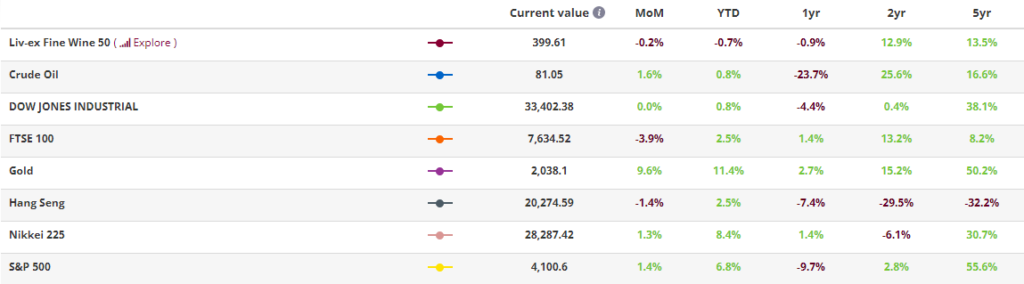

Fine wine 50 vs equities

As the chart above shows, the major markets all traded lower through to the third week of March, when regulatory action in the US and Switzerland calmed nerves following Silicon Valley Bank’s collapse. Over the past fortnight equities have rallied hard, with some now near all-time highs.

While the fine wine market (represented by the Liv-ex Fine Wine 50) has not experienced the same gains in Q1, it continues to offer stability in periods of economic uncertainty and volatility.

Over one year, the Liv-ex 50 is down just 0.9%. Meanwhile, the S&P 500 and Dow Jones Industrial are down 9.7% and 4.4% respectively. Crude Oil – which has had a tumultuous year since Russia’s invasion of Ukraine – has fallen 23.7%.

Buy and sell with speed and confidence…

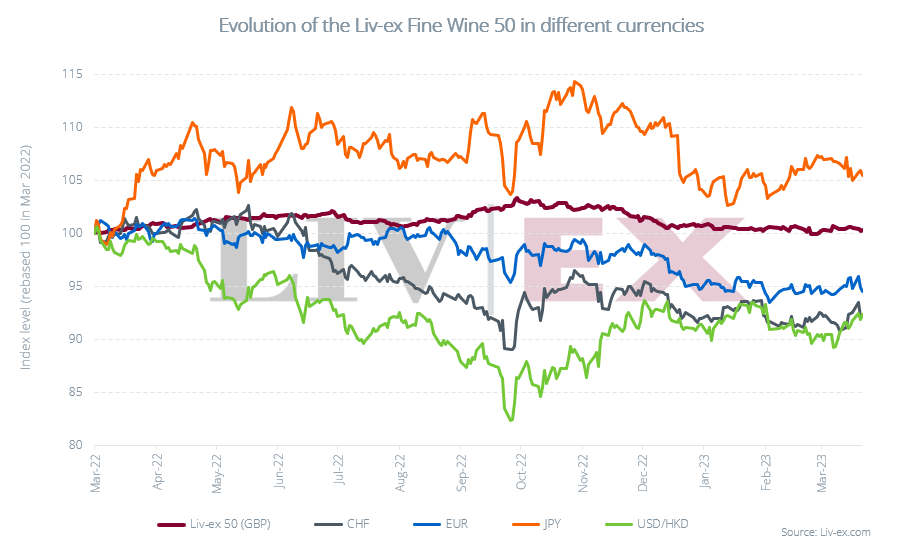

Currency overview

Fine wine was able to weather some of the currency fluctuations throughout the quarter. The Liv-ex Fine Wine 50, which is measured in sterling, fell just 0.7% in Q1.

Driven by changes in rate hike expectations, the US dollar was weaker against most of its currency peers. As such, wine prices for buyers in USD/HK rose slightly (1.1% in Q1). However, due to the ongoing strengthening of sterling, they are now up 12.2% since their low in late September 2022, when then UK Chancellor Kwasi Kwarteng’s mini budget propelled the pound to a record low.

Prices also rose for buyers in Japanese yen this quarter (1.2%), although these are down 7.8% from the highs achieved in October 2022. As reported by Bloomberg, the yen is making a comeback as a preferred foreign-exchange haven, after banking crises in the US and Switzerland hurt the dollar and franc’s standing as go-to assets for turbulent times.

Despite fluctuations for the Swiss franc (money managers ditched the currency at the fastest rate in two years in the run up to the dramatic takeover of Credit Suisse by UBS), the Liv-ex 50 ran flat for buyers in Swiss francs (0.1%).

Euro-based buyers also saw minimal price movements (-0.2%) as data showed that German business morale unexpectedly improved in March, pushing the euro higher.

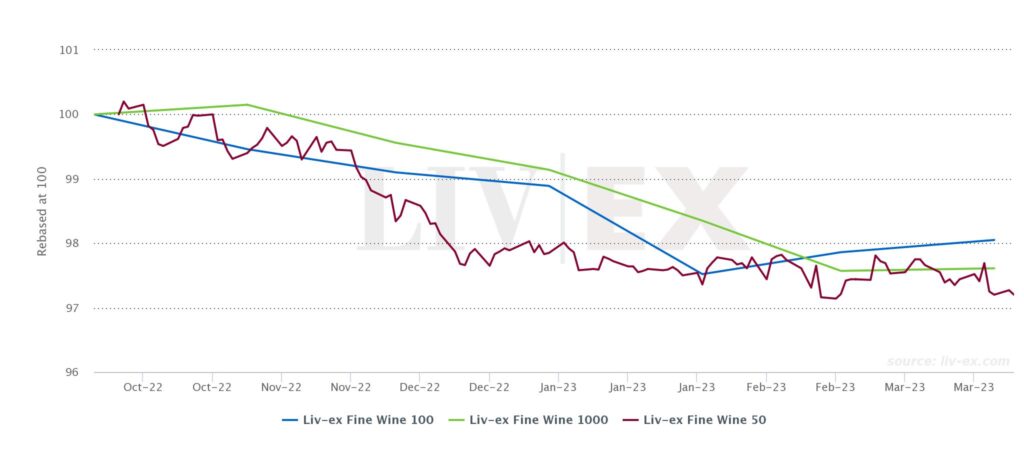

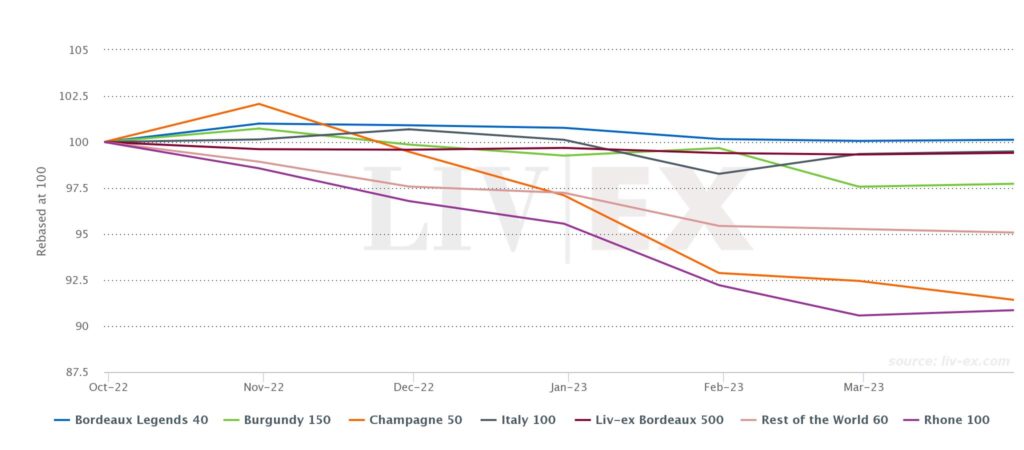

Liv-ex 1000 sub-indices

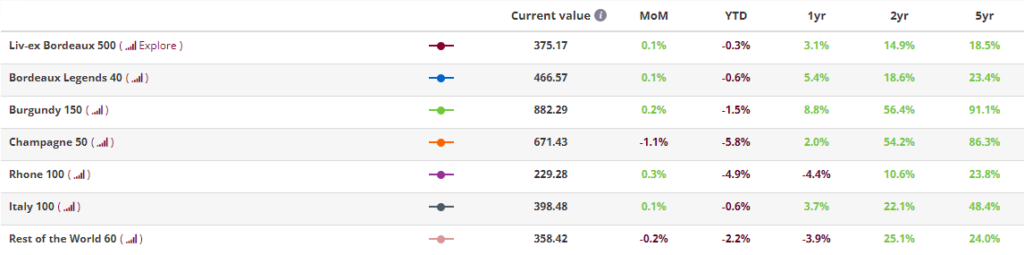

However, despite modest improvements in March, it is important to note that all of the major Liv-ex indices are down year-to-date. The benchmark Liv-ex 100 index, which tracks the 100 most-traded fine wines on the secondary market, is down 0.8%. The Liv-ex Fine Wine 50, which tracks the First Growths, is down 0.7% and the broadest measure of the market, the Liv-ex Fine Wine 1000, is also down 1.5%.

While these declines aren’t quite as steep as some of the falls in the bond and equities markets, their relative stable performance masks some bigger causes for concern. Among the Liv-ex 1000’s sub-indices, for example, the Champagne 50 has fallen 5.8% year-to-date. Back in November 2022, it was the best-performing sub-index and had risen four months in a row. However, in March it recorded its fifth consecutive month of decline.

Furthermore, the Rhone 100 index, which has historically been termed ‘solid as a rock’, was the second-worst performer in Q1 (- 4.9%).

As mentioned in our report on the fine wine market in 2022, the Burgundy 150 and Champagne 50 have driven the fine wine market over the past year, while the rest of the regions have stalled. But as these market drivers begin to turn and regions that previously represented stability start to falter, one might start to question if a market pause is on the cards.

That being said, technical analysis of the Burgundy 150 and the Rhone 100 found that both indices continue to display ongoing bullish trends. However, there are some indicators that, if validated in the months ahead, could point to a change of direction.

Find out how Liv-ex data tools can increase your efficiency and profitability

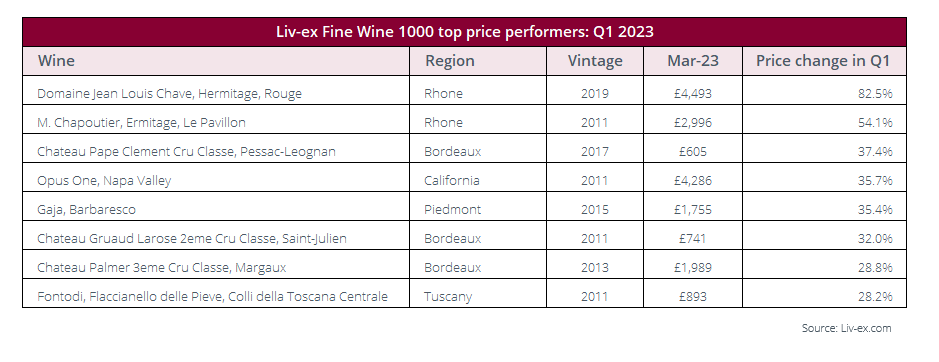

Top price performers

Despite the overall fall in Rhone prices this quarter, two of the best price performers were from the region: Domaine Jean Louis Chave Hermitage Rouge 2019 and M. Chapoutier Ermitage Le Pavillon 2011 were up 82.5% and 54.1% quarter-on-quarter respectively.

Several Bordeaux vintages from ‘off’ years were also among the top price performers, including Chateau Pape Clement 2017 (37.4%), Chateau Gruaud Larose 2011 (32.0%) and Chateau Palmer 2013 (28.8%).

Historically, Bordeaux’s off-vintages have seen the biggest price rises as they often provide a (relatively) affordable point of entry to famous regions and brands. This is something Asian buyers have taken full advantage of in recent years, with several ‘off’ vintages featuring among the top-traded vintages from the region in 2022.

The prices shown in the table above are Liv-ex Mid-Prices. The Mid-Price is the mid-point between the highest live bid and lowest live offer on the market. These are the firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 600 of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable. Prices given are for 12x75cl trades, or 6x75cl converted to a 12x75cl price.

Trading overview in Q1 2023

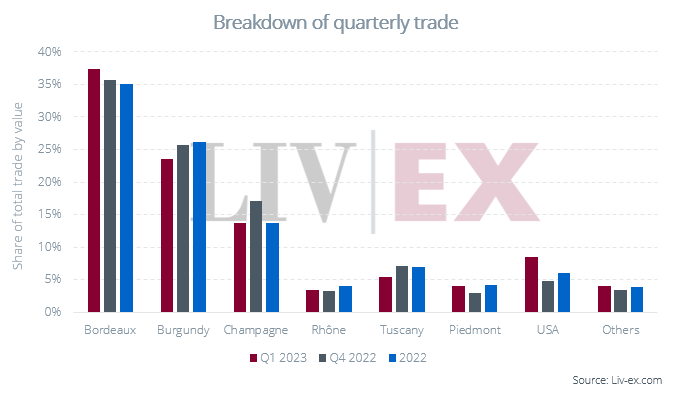

Bordeaux’s trade by value also improved this quarter at 37.3% of the total, up from 35.7% in Q4. This is also above its 2022 average of 35.1%. Demand was driven by Europe and the UK, with each accounting for 37.4% of the Bordeaux’s buyers.

USA wines also had a positive quarter with 8.5% of trade by value, well above its 2022 average of 6.1%. More to follow on this below.

Meanwhile, the Rhone (3.5%), Piedmont (4.0%) and the ‘Others’ category (4.0%) also saw small improvements on the previous quarter.

These increases came at the expense of Burgundy and Champagne. Both regions had a strong Q4 (in terms of trade share and price performance) but as mentioned above, have stalled this quarter. As such, their trade shares fell to 23.5% and 13.7% respectively.

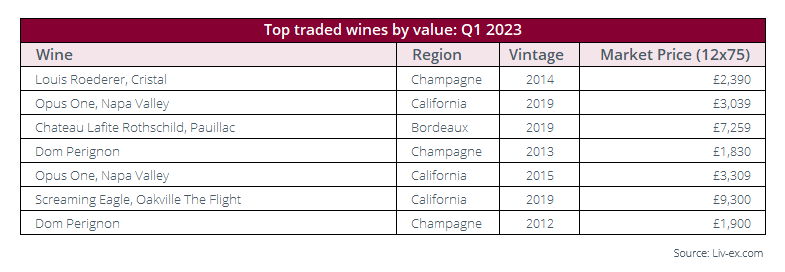

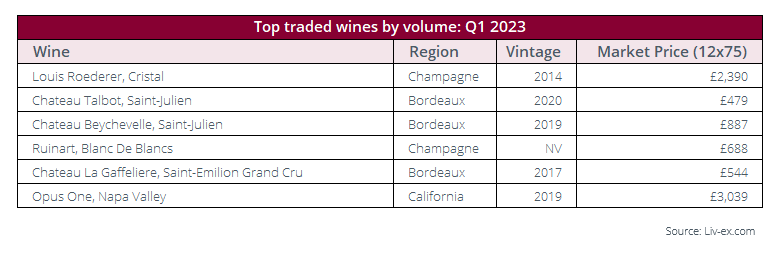

Top traded wines in Q1 2023

Given the fall in Champagne prices, it is perhaps unsurprising that buyers are flocking towards the region in search of discounts. Louis Roederer’s Cristal 2014 remained the top-traded wine by both value and volume this quarter. Interestingly, its Market Price of £2,390 has fallen since February, when it was £2,440 per 12×75. Dom Perignon’s 2013 and 2012 vintages were also among the top-traded wines by value this quarter.

As mentioned above, the USA has been in demand, totalling 8.5% of trade by value. Liv-ex members also predicted that California would see increased demand in 2023. Indeed, two vintages of Opus One (the 2019 and 2015) featured among the top-traded wines by value this quarter. Both wines (along with the 2010 vintage) traded at all-time highs earlier in March.

Another prediction by Liv-ex members was the resurgence of Bordeaux in 2023. 7% of respondents forecasted a revival for the region and predicted that there would be increased demand in 2023.

Perhaps unsurprisingly, trade favourite Lafite Rothschild 2019 was among the top-traded wines by value. Several Bordeaux chateaux also featured in the top-traded by volume list.

The recently-released Chateau Talbot 2020 placed second, while Chateau Beychevelle’s 2019 and Chateau La Gaffeliere’s 2017 also featured.

According to a recent Liv-ex survey, global wine collectors are looking for greater transparency, liquidity and control. As the fine wine market begins to experience greater uncertainty and volatility (especially in Burgundy and Champagne), collectors might return to Bordeaux in the months ahead.

Given its relatively stable start to the year (the Bordeaux 500 and Bordeaux Legends 40 only fell 0.3% and 0.6% respectively, compared to 1.5% for the broader Liv-ex 1000) and reputation for offering liquidity, the region has never looked more attractive in the run up to En Primeur.

The prices shown in the table above are Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. It is always presented for a 12×75 case unless otherwise stated. To calculate the Market Price, we look at list prices from a large group of trusted international merchants. Preference is given to prices from stockholders over brokers, to cases over single bottles, and to recent prices over older prices. The algorithm behind it runs every day, evaluating a pool of over 1 billion data points to determine the most accurate Market Prices for 240,000+ wines.

Gain access to Liv-ex tools and analysis

Conclusion

Once again, Q1 has been a turbulent quarter, but this time it was more financial in nature. The collapse of Silicon Valley Bank and the USB takeover of Credit Suisse sent shockwaves through the markets, and their related currencies took the biggest hit. As such, fine wine prices rose slightly in these weaker currencies.

However, this market volatility once again allowed fine wine to prove its worth as an asset that offers stability in periods of economic uncertainty. That being said, fine wine’s seemingly still waters run deep.

While main Liv-ex indices only suffered small declines, their performance masked some potential causes for concern. The previous ‘winner’ of the fine wine market (the Champagne 50) recorded its fifth consecutive month of decline and is the biggest faller year-to-date – down 5.8%.

Similarly, the Rhone 100, which is often considered one of the most stable regions in the fine wine market, recorded the second-biggest fall, at -4.9%.

With this uncharacteristic volatility in the fine wine market, it is perhaps unsurprising that the trade has been quite risk averse year-to-date. The steady price increases and rising trade for Bordeaux’s wines might suggest that buyers are returning to more familiar regions known for their stability and liquidity.

That being said, caution remains the buzzword this quarter. Although there are signs that the fine wine market is beginning to gather momentum (albeit tentatively), questions still remain as to whether Bordeaux can retain this favour as we head into En Primeur season.

No doubt, this year’s campaign will carry more weight than previous years. The market sentiment surrounding it will play a crucial role in the health of the fine wine market going forward. A well-priced campaign will add a much-needed boost to the market. However, an ill-judged one could add to the markets’ disillusion and confidence. What remains certain is that all eyes will be on Bordeaux in Q2.

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.

Become a member today

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 600 of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable. Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.