Print and read offline instead.

In this report:

- Fine wine prices maintained their level in June despite growing volatility in mainstream markets.

- June saw heightened demand for Bordeaux, Burgundy and wines from the Rest of the World.

- The majority of the best-performing wines from Bordeaux came from ‘off’ vintages.

- Antonio Galloni reviewed the 2019 vintage from Domaine de la Romanée-Conti.

- LVMH acquired Californian winery Joseph Phelps, which has been expanding its international presence and enjoying increased secondary market trade.

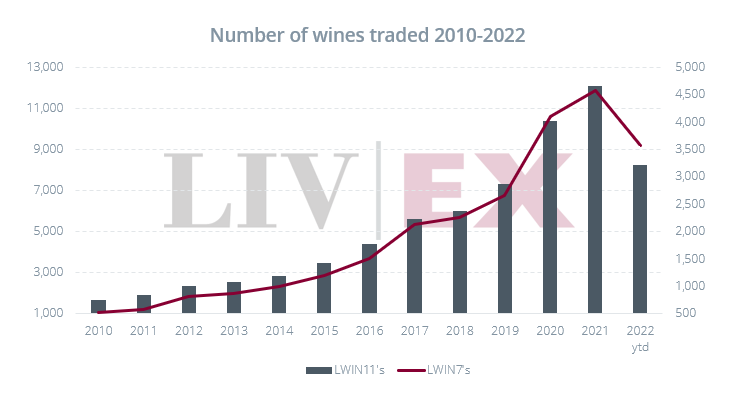

- The number of wines traded in the first half of the year is already 70% of 2021’s record total.

Steady progress for fine wine amid rising turbulence

The turbulence in mainstream markets, caused by inflationary pressure, rising interest rates and recession fears has so far escaped the fine wine market. The pertinent question though is whether fine wine might also turn bearish.

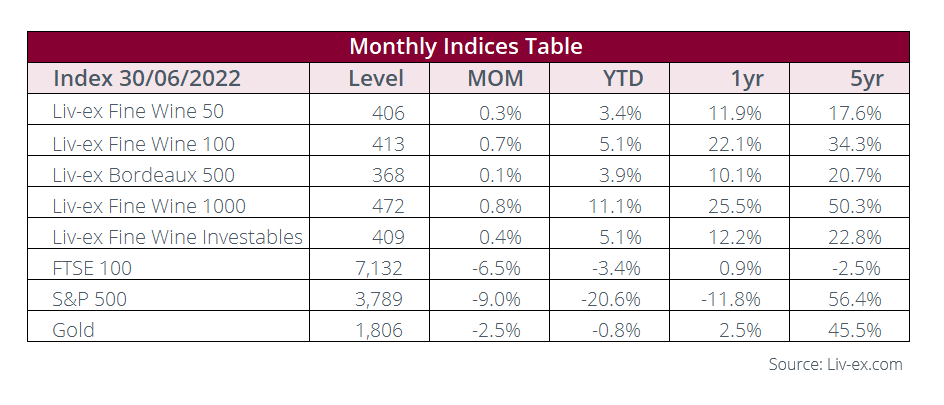

The Liv-ex 100 index rose 0.7% in June for the fourth month in a row, driven by Sterling’s weak performance. However, the index fell in both Euro and Dollar terms.

The Liv-ex 1000 index went up 0.8%, which marked its smallest increase since February 2021. The Champagne 50 was its best-performing sub-index in June, up 1.6%, followed by the Burgundy 150 and the Rest of the World 60, both up 1.3%. Only the Bordeaux Legends 40, which tracks the performance of exceptional old Bordeaux vintages, dipped by 0.7%. Still, the Liv-ex Fine Wine 50, which monitors the movements of the First Growths, increased just 0.3%.

Bordeaux dominated the news for most of the month. The 2021 En Primeur campaign delivered some limited successes but failed to stimulate demand overall. The pricing, which remained largely unchanged on the 2020 vintage, was the core issue for merchants and their clients across the globe, while the smaller volumes released did little to help. Our closing remarks can be found here.

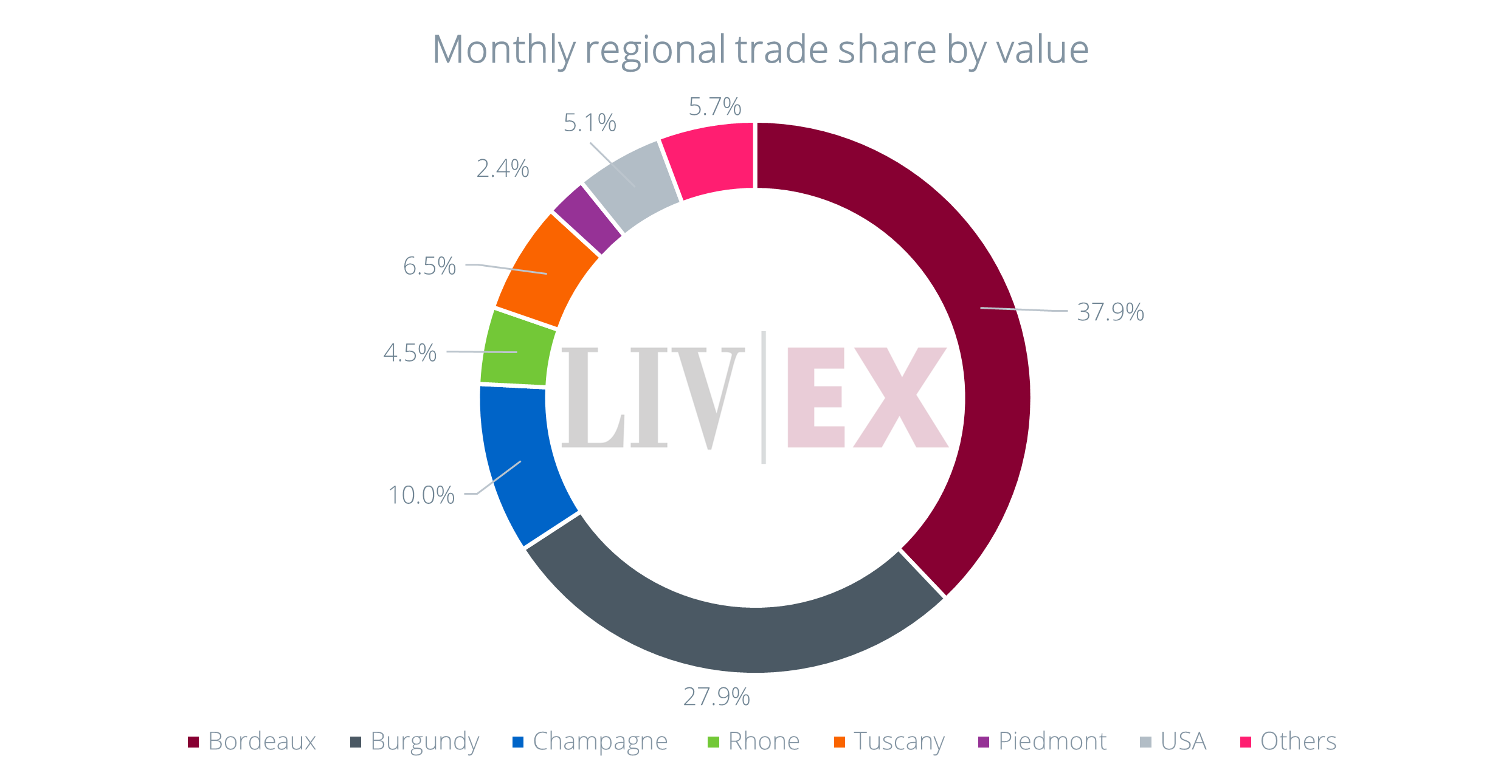

Chart of the Month – Regional trade share in June

The chart below shows the regional breakdown of secondary market trade by value in June this year.

Bordeaux accounted for a larger share of trade, 37.9%, up from 34.3% in May. Its most traded vintages were 2019 (15.6%), 2009 (11.1%) and 2018 (9.3%).

Burgundy’s trade share climbed from 27.3% to 27.9%, while the ‘others’ increased from 5.3% to 5.7%, led by activity around wines from Australia (1.8%) and Spain (1.4%).

All other regions experienced declines in trade share. The most notable being Champagne’s dip from 11.9% to 10%, and Piedmont’s drop from 3.2% to 2.4%.

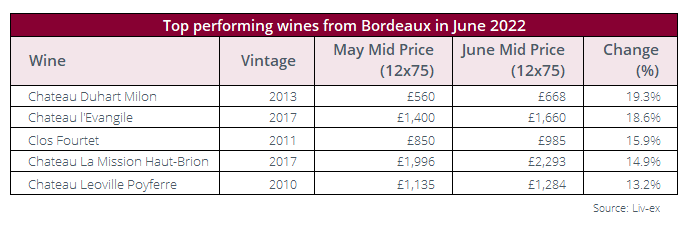

Major Market Movers – The best performing wines from Bordeaux

As stated above, Bordeaux’s trade share rose to 37.9% in June. However, much of this trade was driven by activity around older vintages rather than the 2021s that were offered en primeur.

The 2019s have continued to find sustained trade throughout the year (as mentioned above) but the best-performing Bordeaux wines in June came from the ‘off’ vintages 2017, 2013 and 2011.

Usually among the least expensive vintages in a producer’s back catalogue, there are often opportunities here for buyers to acquire (ready to drink) wines from leading estates at prices well below those commanded by ‘on’ vintages.

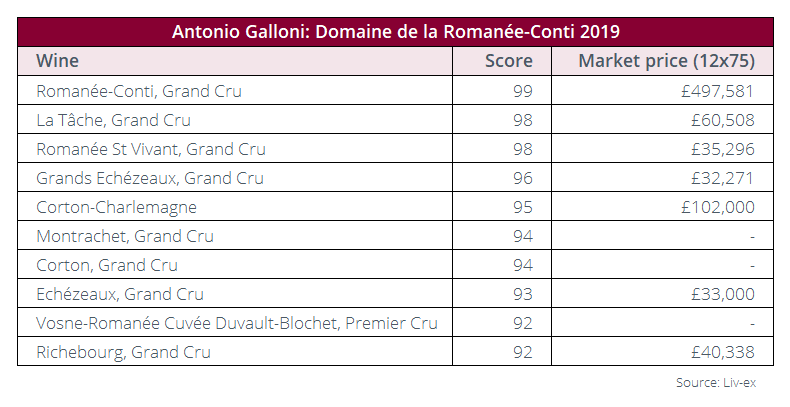

Critical Corner – Galloni reflects on Domaine de la Romanée-Conti’s 2019 vintage

Antonio Galloni published his impressions of the 2019 vintage from Domaine de la Romanée-Conti on Vinous at the end of June.

He said it was a ‘poignant’ tasting, being the last from the domain to be hosted by Aubert de Villaine who officially retired as co-manager in March of this year.

Comparing the 2019s to other vintages de Villaine said, ‘we have to go back to ’65… 1865’.

‘Well, they are pretty special,’ said Galloni who stated his personal preference for the Grands Echézeaux and Romanée St Vivant, as well as the new Corton-Charlemagne which he thought ‘showed better than the Montrachet’.

‘The one question mark is the Richebourg,’ he added, which he found ‘tight and austere’ and ‘lacking depth’. Perhaps, he continued, it was picked a little too early but it was certainly ‘the outlier in 2019’.

News insight – Joseph Phelps acquired by luxury goods powerhouse LVMH

The French luxury giant LVMH has purchased Joseph Phelps Vineyards in California’s Napa Valley for an undisclosed sum. This is the latest acquisition by the luxury group, which also owns Dom Pérignon, Château d’Yquem, and Château Cheval Blanc among others.

Earlier this week, the drinks business also reported that Château Cheval Blanc had bought neighbouring estate Château La Tour du Pin Figeac, with the aim of bolstering its white wine production.

In California, the group’s holdings already include the sparkling house Domaine Chandon, a majority share in the cult winery Colgin Cellars, and Newton Vineyard.

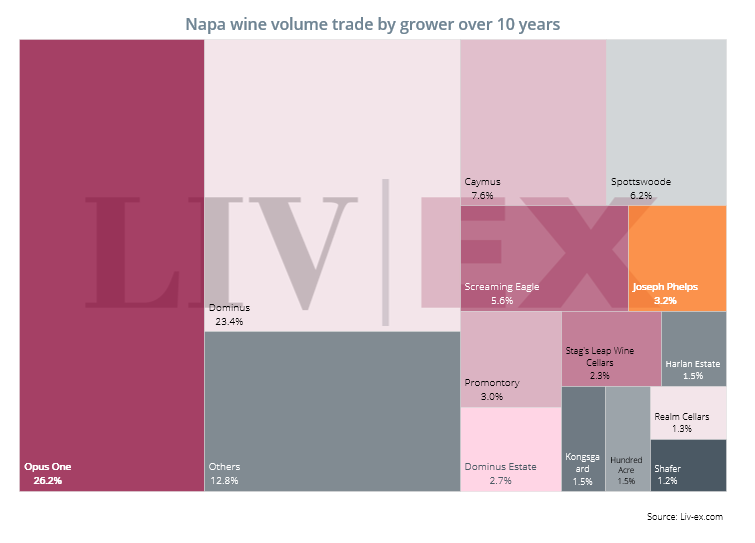

How will the new ownership affect the Phelps’ brand? The winery has been expanding its international presence recently and joined La Place de Bordeaux in 2019. Here it was following in the footsteps of the likes of Opus One, Vérité and Inglenook – a move likely designed to further strengthen its brand power and pricing strategy.

Joseph Phelps is most famous for its Bordeaux-style blend, ‘Insignia’, created in 1974 and considered an innovation at the time. According to Robert Mondavi, ‘at that time we were purists, we were making Cabernet, Pinot Noir. He [Joe] came up in 1974 with his Insignia… what we called Meritage; he was the forerunner of that. And people realised that here’s someone who has a vision; he helped stimulate us to go in the same direction’.

On the secondary market, Joseph Phelps has been enjoying rising trade by volume and value. The first trade for the estate’s wines was in 2007, when two cases of the 98-point (Robert Parker) Insignia 1995 changed hands. Over the past decade, Joseph Phelps has become the sixth most traded Napa Valley brand by volume, taking 3.2% of the region’s trade share.

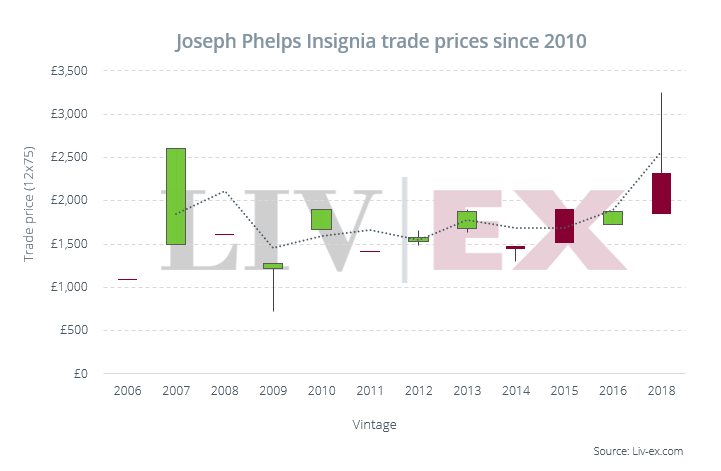

Its most active vintage has been the 2018 (which was released last year), representing 47.5% of its total trade by value. The 2018 Insignia has also been among the wines with the greatest price variation, along with the 100-point 2007 vintage, as can be seen in the chart below.

Prices for top Californian wines are well-known to be expensive, with the average price for wines traded so far this year being £5,604 per case (12×75). However, the average price for a case of Insignia is £1,655 (12×75), while the Joseph Phelps Cabernet Sauvignon is £476 on average; clear value propositions for buyers on the hunt for Californian wine.

It remains to be seen how the new investment will affect the secondary market performance of the brand but it is increasingly in the spotlight as demand for Californian wines grows.

*Green represents price increases; red represents price decreases.

Final Thought – The fine wine market in the first half of the year

The fine wine market has continued to broaden in 2022. Data from the first half of the year shows which wines and regions are reflecting the shifting demands and changing shape of the secondary market.

Increasing number of wines trading

The number of wine labels (measured as LWIN7s) traded in the first half of 2022 is already 78% of the record level achieved in the whole of last year. Meanwhile, the number of wines traded measured as LWIN11s (wines by vintage) is 70% of the 2021 record. At its current rate, it seems likely trade will surpass that landmark by the end of Q3.

Most fine wine regions have traded more wines in H1 2022 versus H1 2021. The number of Champagnes traded year-on-year is up the most – 11.9%. The market’s broadening is also coming from the USA (+9.9%), Burgundy (+8.7%), Italy (+6.7%), and regions included in the ‘others’ category.

But for some, the broadening has stalled. Bordeaux fell back, with the number of wines traded down 3.7% year-on-year. The number of Rhône wines has, so far, run flat.

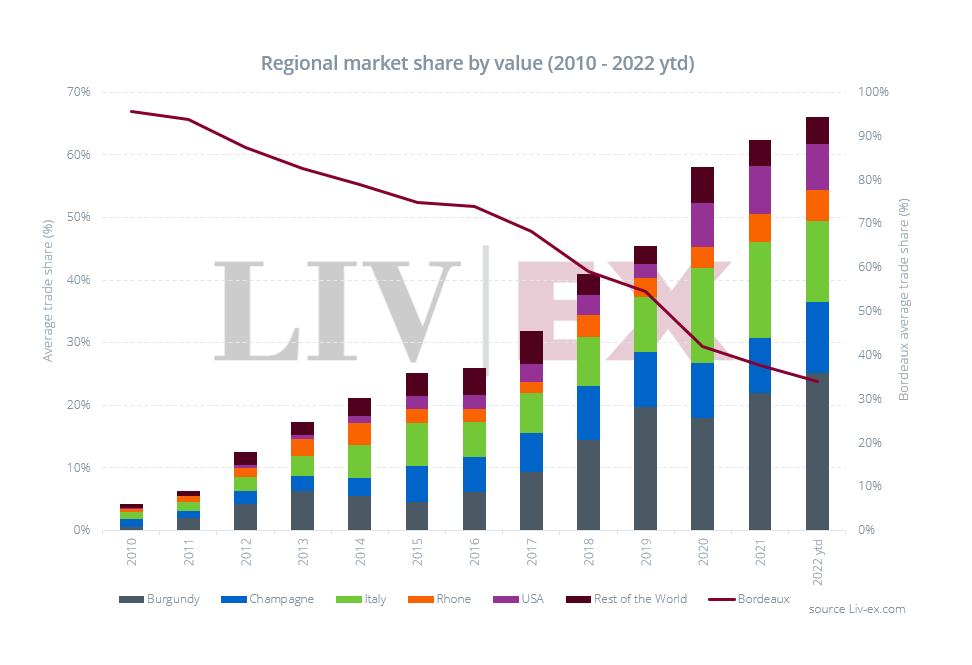

Bordeaux continues to lose trade share

The increase in wines seeing active trade, and the regions they are coming from, has in turn impacted regional trade share.

Bordeaux has continued to lose market share to other regions, and now sits at its lowest level – 33.9% year-to-date. Two years ago, Italy emerged as a big contender, almost doubling its trade share between 2018 and 2020, to take a 15.3% slice of the market in 2021. Year-to-date, however, it has fallen back to 13%.

The USA, which tripled its trade share between 2019 and 2020, has not grown any further. Year-to-date, it stands at 7.3%, slightly down on the 7.6% share achieved in the first half of last year.

The Rhône (4.9%) and the ‘others’ (4.4%) have made small gains, but it is Champagne and Burgundy that have enjoyed the biggest growth.

Champagne’s trade share now sits at 11.4%, up from 8.8% at this same point in 2021. Burgundy accounts for 25.1% of the market, up from 22.0% in 2021. In some markets, such as the UK, Burgundy is the most traded region, with a market share suprassing 35%.

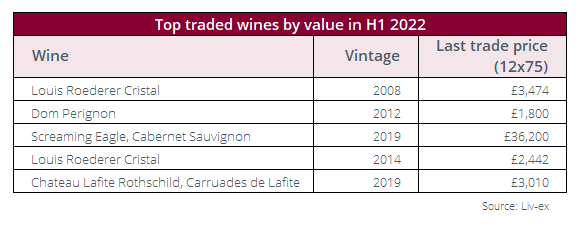

Champagnes lead most traded wines by value in H1

A snapshot of the five most traded wines by value so far this year is representative of the broader market trends. Three of the top five spots are Champagnes, corresponding with its growing trade share. Louis Roederer’s Cristal is the second most traded wine (LWIN7) by both value and volume this year. Its 2008 and 2014 vintages feature in the rankings, together with Dom Pérignon 2010.

The 2019 vintages of Screaming Eagle Cabernet Sauvignon and Château Lafite Rothschild’s Carruades de Lafite have also made it into the top five. Overall, the 2019 is the most traded vintage by value this year.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 580+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.