Last year was a very strong year for the secondary fine wine market. As detailed in our end of year report, new records were set as the market’s leading indices, the Liv-ex Fine Wine 100 and Fine Wine 1000 both reached new highs amid an unbroken, 18-month run of gains.

2022 began where 2021 left off, bolstered by a good campaign for the 2020 Burgundy vintage. The Liv-ex 100 and the Liv-ex 1000 indices were up by 1.9% and 3.5% respectively.

However, the market showed signs of slowing in February, with the smallest gains for the Liv-ex 100 and Liv-ex 1000 since May 2020. The Liv-ex 100 performed better in March, up 0.7%, while the Liv-ex 1000 was up 2.0%.

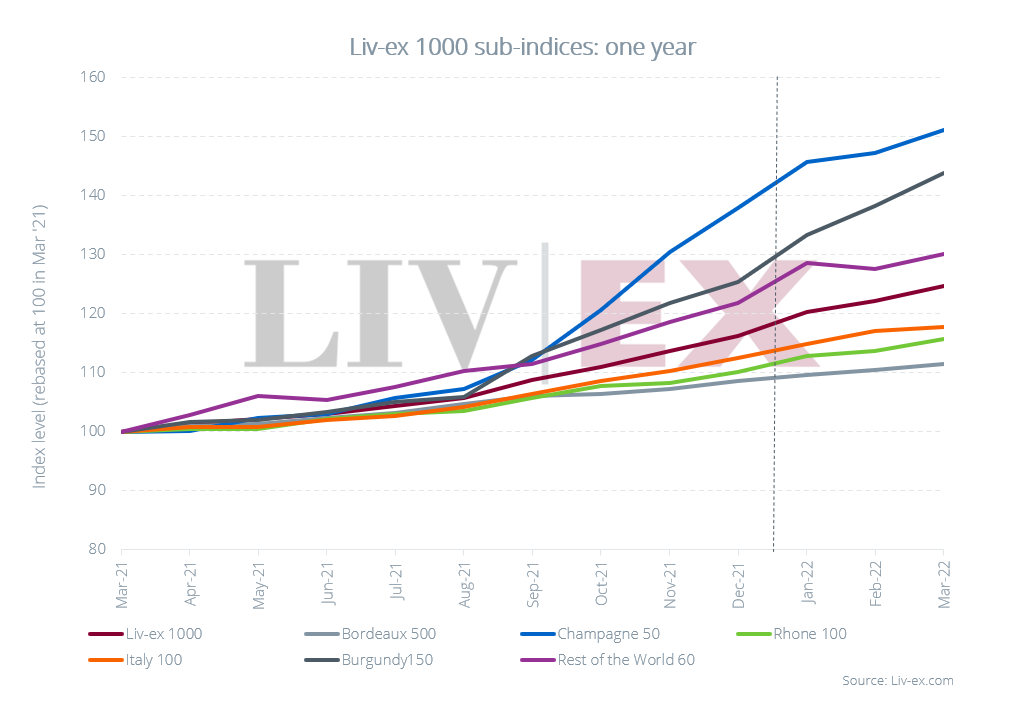

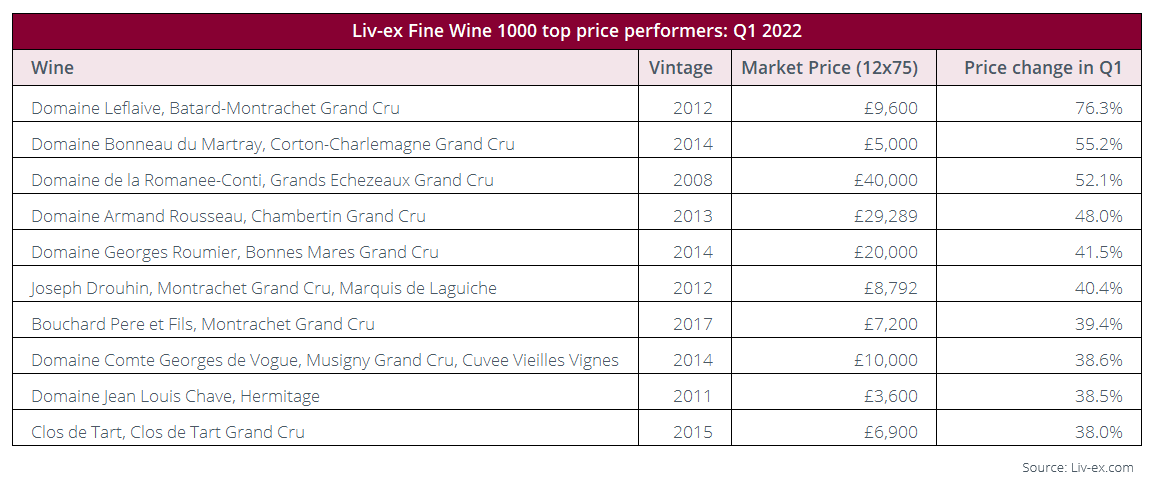

Over the quarter, Liv-ex’s leading indices, the Fine Wine 50, Fine Wine 100 and Fine Wine 1000 rose 2.3%, 2.9% and 7.3% respectively.

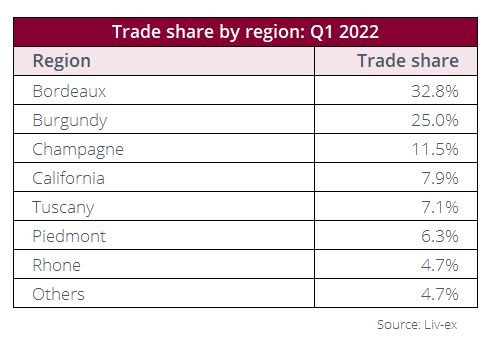

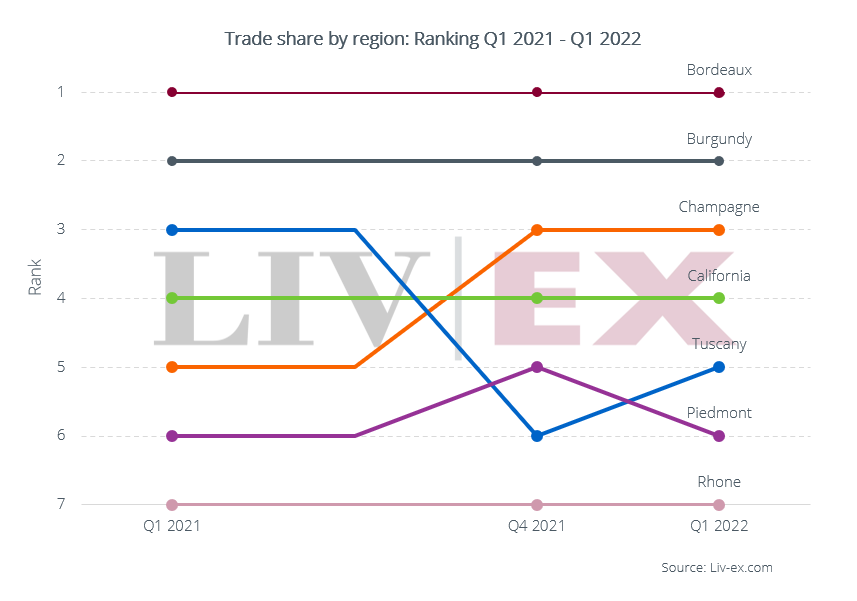

While the Q1 gains in the Liv-ex 100 were more gentle than in 2021, the performance for the Liv-ex 1000 was striking, reflecting robust gains in both Burgundy and Champagne.

But, can the fine wine market’s performance continue to be divorced from the wider global economic and political situation?

Rising inflation and interest rates were already on the minds of many at the end of last year. The Russian invasion of Ukraine on 24th February has only exacerbated these concerns, as the rising cost of oil, gas and metals impact further on a struggling global supply chain.

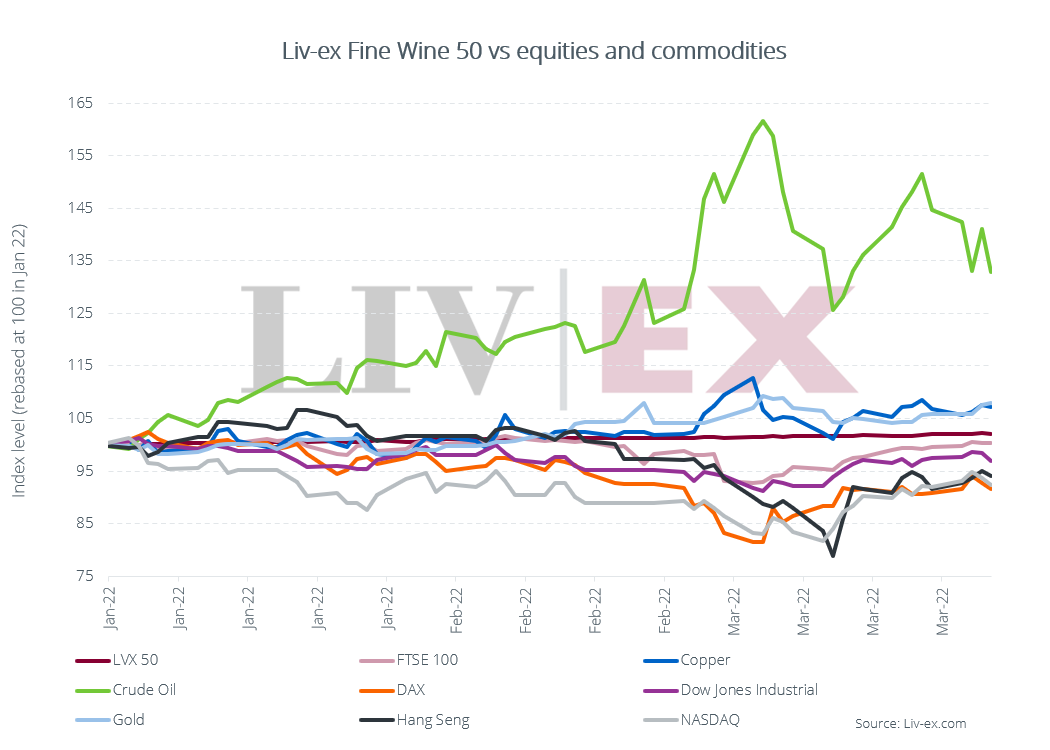

The price of a barrel of crude oil is still over US$100 a barrel (though releases from the US reserves announced on 31st March helped curb the price creep) and the price of a ton of nickel or copper has also ballooned (see chart below).

On top of war in Europe and the rising cost of living there is the rapidly worsening Covid situation in China, a major buyer on the secondary fine wine market – where fresh lockdowns have once more turned the country’s mega-cities into ghost towns.