April Market Report

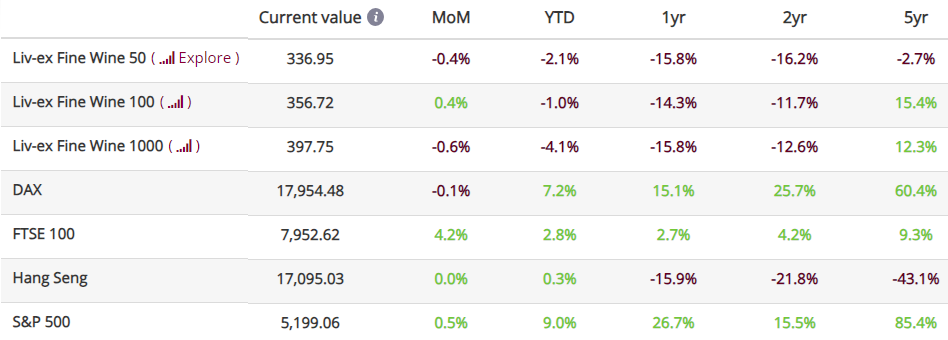

- Spring has sprung, and so has the Liv-ex Fine Wine 100: the industry benchmark rose 0.4% in March, its first positive movement in twelve months.

- Screaming Eagle 2021 led the top-traded wines of the quarter by value following its release in early 2024.

- As Antonio Galloni explores Domaine de la Romanée-Conti’s 2021 vintage, we examine the success of the producer’s different Grand Crus.

- Is now the time to turn to Tuscany? Technical analysis of the regional performance of the Italy 100.

- After the flurry of March La Place releases, we explore the market’s reaction to the wines.

- What’s bring down the Rest of the World 60 index?

Introduction

Here comes the sun

*data taken on the 12th of April 2024. The FTSE 100 was last updated on the 31st of March. The Liv-ex Fine Wine 50 is updated daily.

Spring has sprung, and so has the Liv-ex Fine Wine 100: the industry benchmark rose 0.4% in March, its first positive movement in twelve months.

While this rise may be a promising sign of stability, it wasn’t reflected in the rest of the market. The Liv-ex Fine Wine 50, which tracks the movements of the First Growths and is updated daily, fell 0.6% month-on-month.

Likewise, the Liv-ex Fine Wine 1000, the broadest measure of the fine wine market, fell 0.6% in March. That said, this decline was much milder than the one it recorded in February (1.3%). Of its sub-indices, the Rhône 100 fared best, rising 0.4% month-on-month, while the Champagne 50 dipped 2.2%.

Trade value and volume on the exchange took a slight dip in March, as did the number of individual wines (LWIN11s) traded.

One quarter into 2024, the Liv-ex 1000 is down 3.5%, primarily driven by the Burgundy 150 which is down 5.5% year-to-date, the Rhône 100 down 4.8% and the Rest of the World 60, down 3.6%.

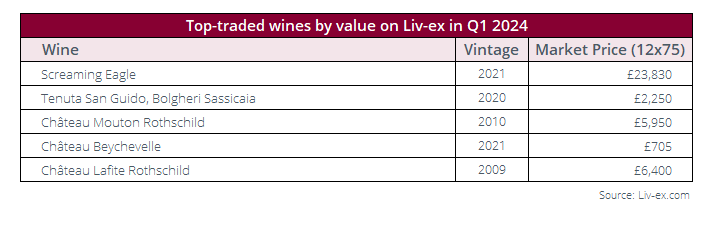

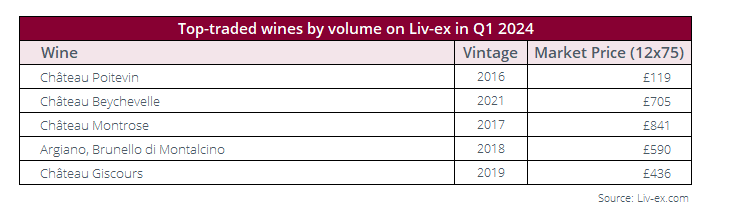

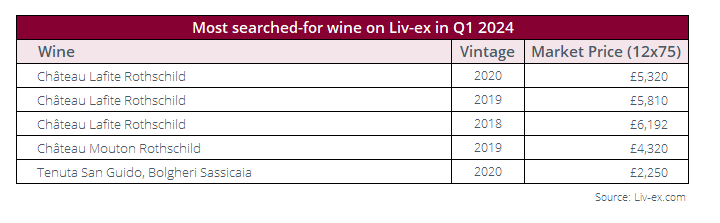

What were the most popular wines in Q1 2024?

Screaming Eagle 2021 led the top-traded wines of the quarter by value following its release in early 2024. Interestingly, the second wine on the list was Sassicaia 2020. The 100-point 2021 vintage was released in February at £2,500 per case, a price offering value considering the wine’s high scores. The 2020, which boasts more modest scores from Antonio Galloni and Monica Larner, comes cheaper; it has a current Market Price of £2,250 per 12×75, below its release price of £2,400.

The rest of the list was Bordeaux-focused, with two First Growths from outstanding vintages, Château Mouton Rothschild 2010 and Château Lafite Rothschild 2009. The last wine, however, was Château Beychevelle 2021, which has seen a flurry of trading activity since its release in bottle. It also featured among the most-traded wines by volume last quarter.

The only non-Bordeaux wine on the list of most-traded wines by volume was The Wine Spectator’s 2023 Wine of the Year, Argiano, Brunello di Montalcino 2018. Three months after the announcement, the wine is still seeing plenty of trade on the secondary market.

The list was topped by a Médoc wine, Château Poitevin 2016, and completed by a Second, Third and Fourth Growth, all with Market Prices under £1,000 per case. The vintages range from great years in Bordeaux (2016, 2019) to ‘off’ vintages like 2017 and 2021, which have been recommended by various critics as earlier drinking wines while buyers wait for the 2019, 2020 and 2022 to age.

Looking at the most searched-for wines in the first quarter of 2024, Château Lafite Rothschild occupied the three top spots with the 2020, 2019 and 2018 vintages, followed by Château Mouton Rothschild 2019. None of these made it into the top-traded wines by value or volume, which suggests that while there is considerable interest in these younger First Growths, buyers are focusing on older vintages which are ‘safer values’ and already have some bottle age.

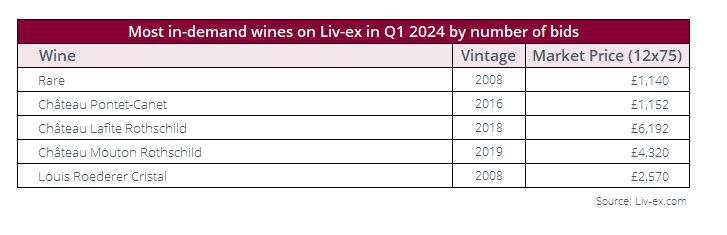

However, the most in-demand wines, measured by the number of bids, in the first quarter of the year tell a different story: both Château Lafite Rothschild 2018 and Château Mouton Rothschild 2019 featured on the list, implying there is demand for these wines from buyers. The fact that this did not necessarily translate into high volumes or value of trades suggests that buyers are not willing to pay the prices offered.

Two 2008 Champagnes, Rare 2008 and Louis Roederer Cristal 2008, also featured on the most bid-for wines of the quarter.

Major Market Movers

A Tuscan triumph

As mentioned in the introduction to this report, the Liv-ex Fine Wine recorded a 0.4% rise in March, the first in 12 months. In our latest indices update, we looked at the wines that buoyed the index to its success and found a mix of California, Rhône, Burgundy, Tuscany, Champagne and Bordeaux in the top ten.

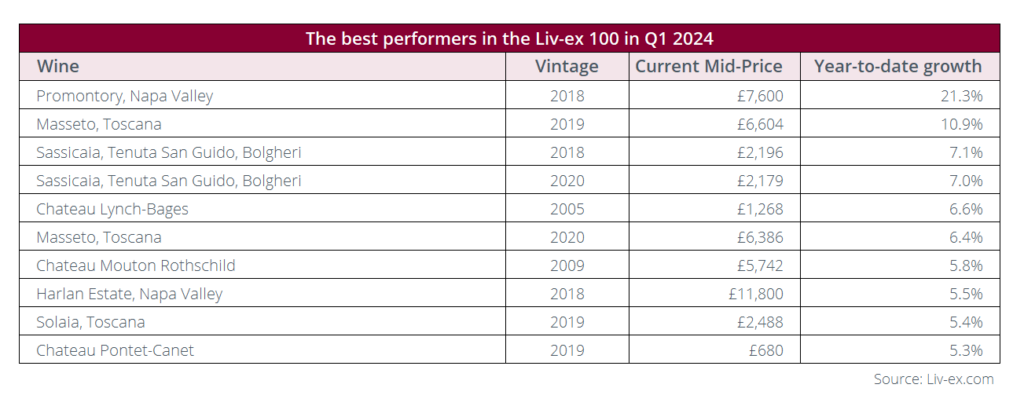

Looking at the first three months of the year, however, shows a much clearer picture. The table below shows that Tuscan wines accounted for five of the top ten best performers in the Liv-ex 100 in the first quarter of the year. More on this later.

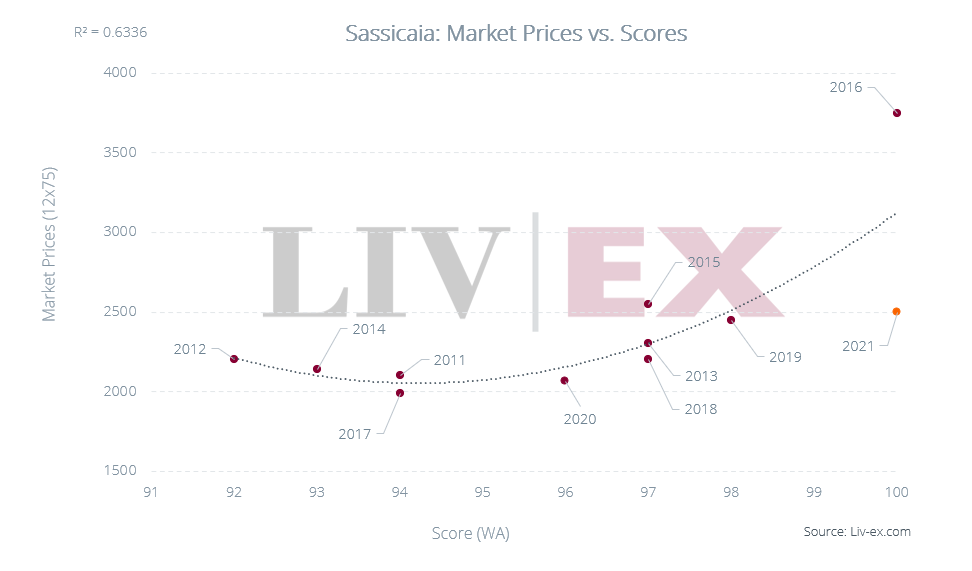

All these ‘Super Tuscan’ wines were recent vintages: Masseto 2019 and 2020, Solaia 2019 and Sassicaia 2018 and 2020. Sassicaia Market Prices are 63.4% correlated to Wine Advocate scores, and our pricing analysis of the recently released Sassicaia 2021 identified the 2018 and 2020 as attractive options for buyers seeking value based on their scores and lower Market Prices.

Two 2018 Californian wines also featured among the best performers in Q1 2024, including Promontory 2018 which topped it. The wine, which boasts a 100-point score from Antonio Galloni, stood out as one of the most attractive of the last ten vintages of Promontory following the release of the 2019. Harlan Estate 2018 was the other Californian on the list and was also scored 100 points by Lisa Perrotti-Brown MW. More on California’s place in the Rest of the World 60 can be found in the Final Thought section of this report.

Last but not least, Bordeaux was represented by Château Mouton Rothschild 2009 and Château Pontet-Canet 2019, both of which are trading well below their respective release prices of £7,800 and £732 per case.

Critical Corner

Galloni on Domaine de la Romanée -Conti

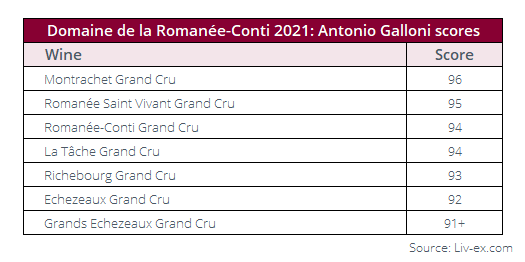

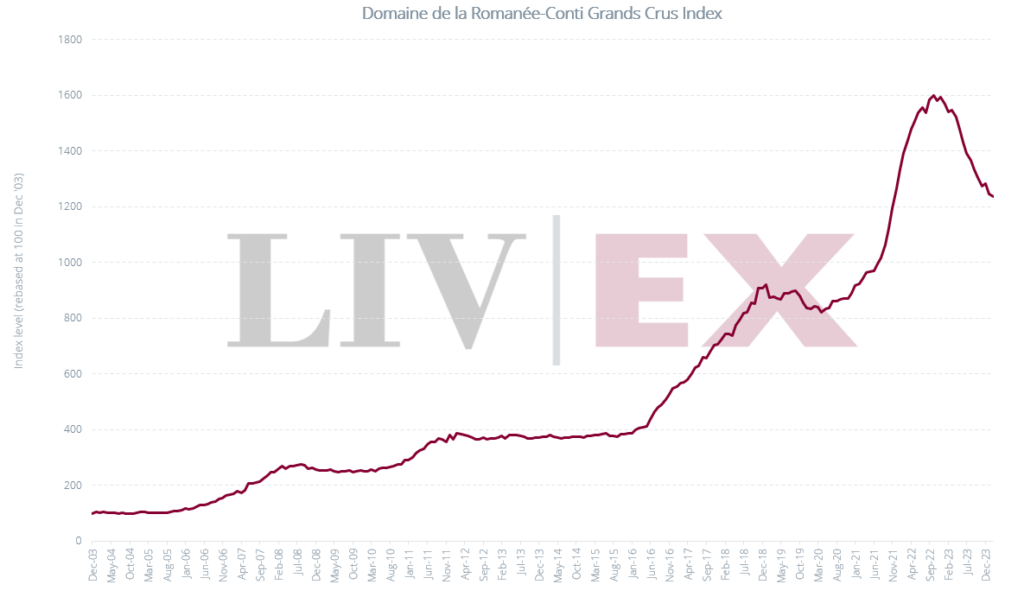

Last month, Antonio Galloni (Vinous) published his ‘survey’ of Domaine de la Romanée-Conti’s 2021 vintage.

Unlike the previous vintage’s ‘decidedly exuberant’ wines, the critic described the 2021s as ‘much lighter and more translucent, as Burgundy used to be’. Despite the challenging growing season, including April frosts on the vineyards’ upper slopes, Galloni found balance in these wines, in which ‘whole clusters are impeccably integrated’.

His scores reflect the vintage’s difficulties, with no wines above 96 points. Galloni’s top pick was the Montrachet Grand Cru, which he called ‘superb’, followed by the Romanée Saint Vivant which left him impressed.

As well as 2021’s small yields and (relatively) lower quality, Domaine de la Romanée-Conti also has challenging market conditions to contend with. The fine wine market is currently over a year into a corrective phase which has seen prices pull back hard, including in Burgundy’s most famed estate.

A glance at the chart below, showing Domaine de la Romanée-Conti’s Grands Crus indexed, shows just how quickly the wines have retraced the ‘explosive growth’ they experienced just a few years prior. Their prices are now back to their 2021 levels, but buyers still seem more reticent to pay what they did back then.

We don’t yet know the release prices of Domaine de la Romanée-Conti’s 2021s, but it would be wise to consider buyers’ tighter purse strings and risk aversion as well as the wines’ lower critic scores. One also fears that the quality of the recently-released 2022s from other producers may overshadow the preceding the vintage.

That said, perhaps scarcity and the Domaine’s name and reputation for excellence will be enough to counter the adverse market conditions. Other Burgundy producers certainly seem to think so: Domaine Leflaive recently released its 2021 Chevalier-Montrachet Grand Cru at £12,780 per case, up 25.3% on the 2020, while Domaine Armand Rousseau’s Chambertin Grand Cru 2021 was released at £24,840 per 12×75, up 21.8% on the 2020. While both are yet to trade on the secondary market, their current Market Prices sit considerably above their release prices. Will buyers bite? Only time will tell.

Chart of the Month

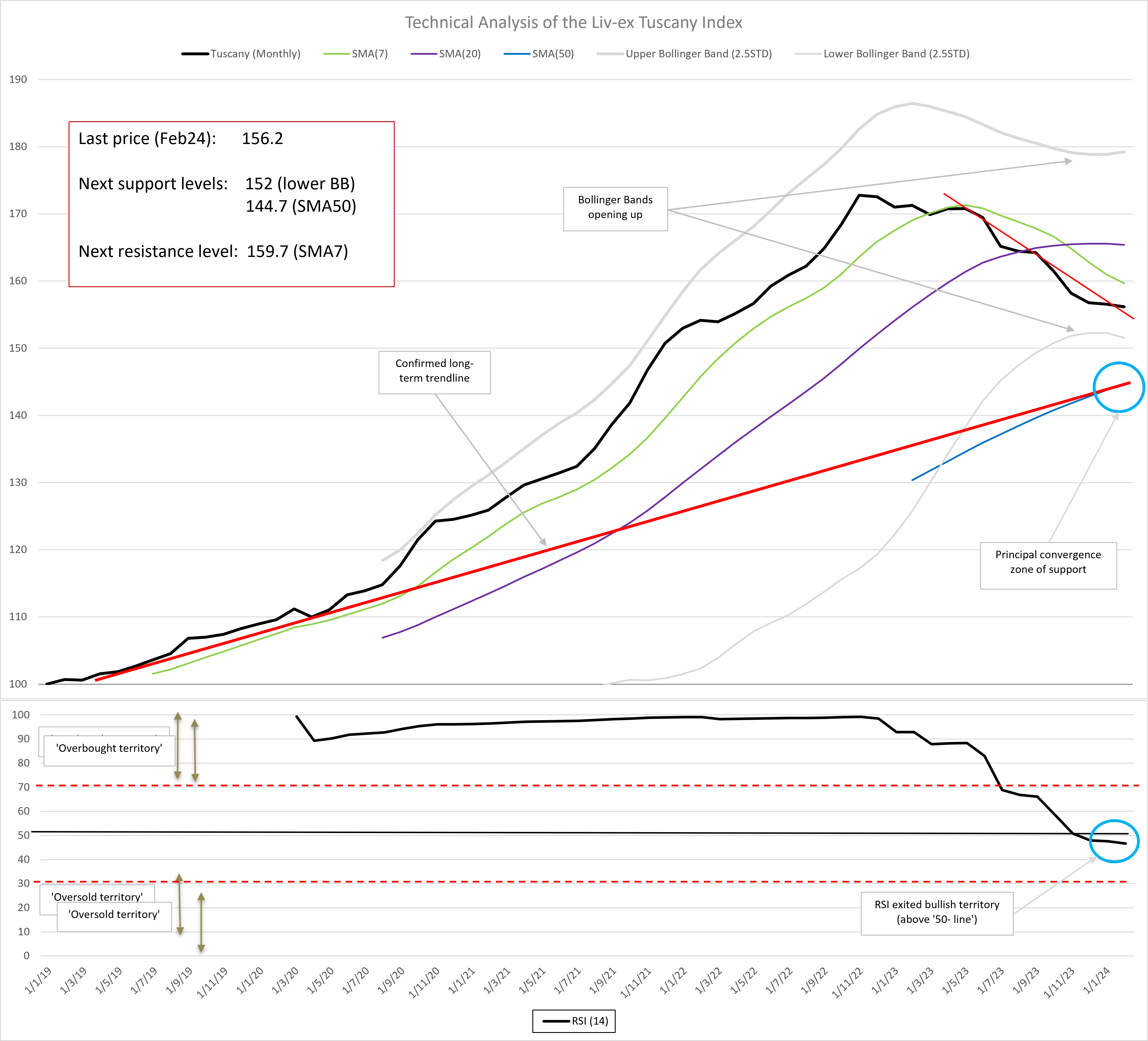

Italy 100 regional analysis; the time to turn to Tuscany?

The Italy 100, over the last two years, has been the best performing sub-index of the Liv-ex Fine Wine 1000. It has fallen by just 2.8% over that period, while the Liv-ex Fine Wine 1000 has fallen by 12.6%.

The Italy 100 covers the ten most recent vintages of the ten most traded Italian wines on the global marketplace. Five of these are ‘Super Tuscans (Tignanello, Solaia, Sassicaia, Ornellaia and Masseto). Four are Piedmontese wines (Bartolo Mascarello Barolo, Bruno Giacosa Barolo Falletto Vigna Le Rocche Riserva, Conterno Monfortino and Gaja Barbaresco). The index hit its peak in November 2022, since when it has retraced 7.2%. Over this period, the Piedmont components combined have fared far better than their Super Tuscan counterparts; falling by a little over 2.1% compared to 9.6% for the Super Tuscans further South.

Here, our Technician analyses the basket of Tuscan wines to determine whether the market should anticipate a reversal or continuation of its recent bearish trend. We’ll publish similar analysis later this month examining the basket of Piedmont wines within the index.

A ’rounded top’ shape is clearly evident in the chart below. This is followed by a steady drop, rather than a zig-zag pattern that would signify a market which is regularly re-testing the price as it falls. It remains to be seen therefore whether the ongoing retracement is a correction or a more significant reversal of the long-term bullish trend.

Because of the smooth shape described above, the Simple Moving Average over seven months (SMA7) is a reliable trend indicator. The SMA7 line continues downward. The Bollinger Bands are beginning to widen which suggests the decline might continue.

The Relative Strength Index (RSI) hasn’t exhibited any bearish divergence, and now sits below the ’50 line’ indicating bearish momentum. Looking ahead, this bearish trend is set to continue until the index recaptures its SMA7, currently at 159.7 (the next resistance level). The widening Bollinger Bands suggest we should expect the bearish momentum to accelerate. The area of support is 144.7 where the SMA50 converges with the long-term ascending trendline.

News Insight

March Madness in the fine wine market

March brought along a flurry of La Place releases, from Bordeaux and Beyond.

Restraint seemed to be the word when it came to pricing as only Clos des Lambrays 2021 was released higher than the previous vintage. Château d’Yquem 2021, Promontory 2019 and Ornellaia 2021 were released at the same price as their predecessors, and Krug 2011 and Château Latour 2017 came out lower than the 2008 and 2015 vintages, respectively.

But has this more cautious pricing been enough for the wines to find their place on the market?

Only three of them have traded on the secondary market so far, two of them just once, which is rather telling of the dampened demand they are facing. That said, Tignanello 2021 last traded at £800 per 6×75, equivalent to £1,600 per case, up 23.1% on its release price.

Krug 2011, on the other hand, last traded at £2,500 per case, below its release price of £2,970, and Château Latour 2017 didn’t fare much better, trading 4.8% below its release price. These two wines are offered below their release prices, which perhaps speaks to the difficulty merchants have in shifting them.

Optimists will point out that March also brought along a brief respite for the fine wine market in the shape of a positive movement in the Liv-ex 100. Coincidence? Perhaps. While the hope is that volumes of highly-rated wines from around the world are what’s needed to reinvigorate the market, so far, the evidence suggests otherwise.

Final Thought

What’s bringing the Rest of the World 60 down?

One quarter into 2024, the Rest of the World 60 is one of the worst-performing sub-indices of the Liv-ex 1000.

The index, which tracks the price performance of the ten most recent physical vintages of six wines from Spain, Chile, the USA and Australia, is down 3.9% since January 1st, behind the Burgundy 150 (-6.0%), the Rhône 100 (-4.5%).

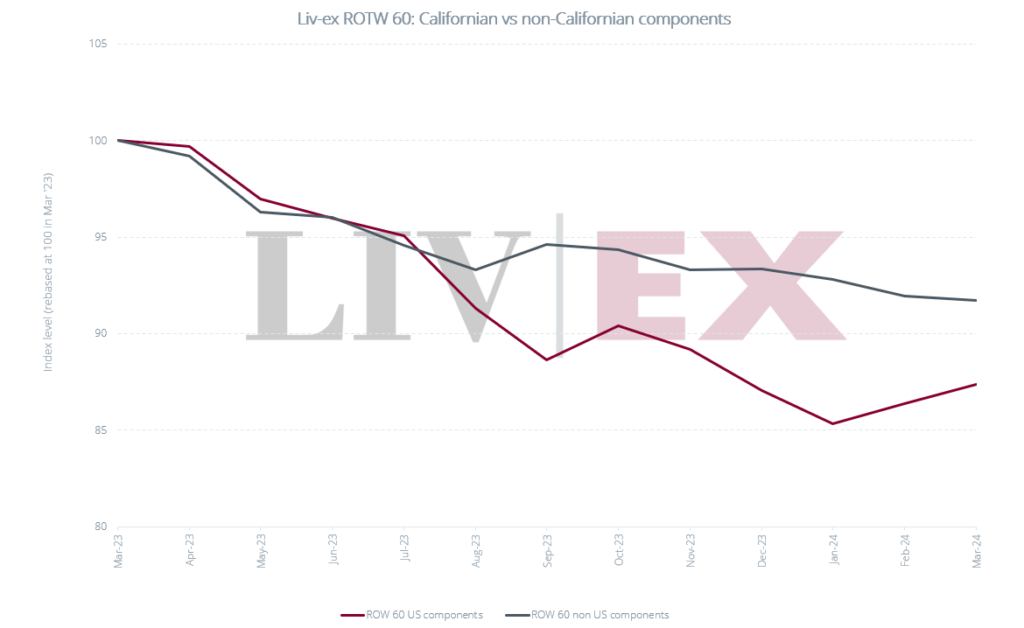

The makeup of this index is an interesting one, as it features three Californian wines (Screaming Eagle, Dominus and Opus One), Vega Sicilia’s Unico from Spain, Penfolds’ Grange from Australia and most recently, Seña from Chile. Californian wines have their own index (not a subset of the Liv-ex 1000) with the California 50, which is down 4.3% year-to-date. Are the Californian components of the Rest of the World 60 driving the index’s recent underperformance?

Looking at a one-year view, it certainly seems so. While both US and non-US components of the index fell year-on-year, the Californian wines suffered the most, about 4% lower than their counterparts.

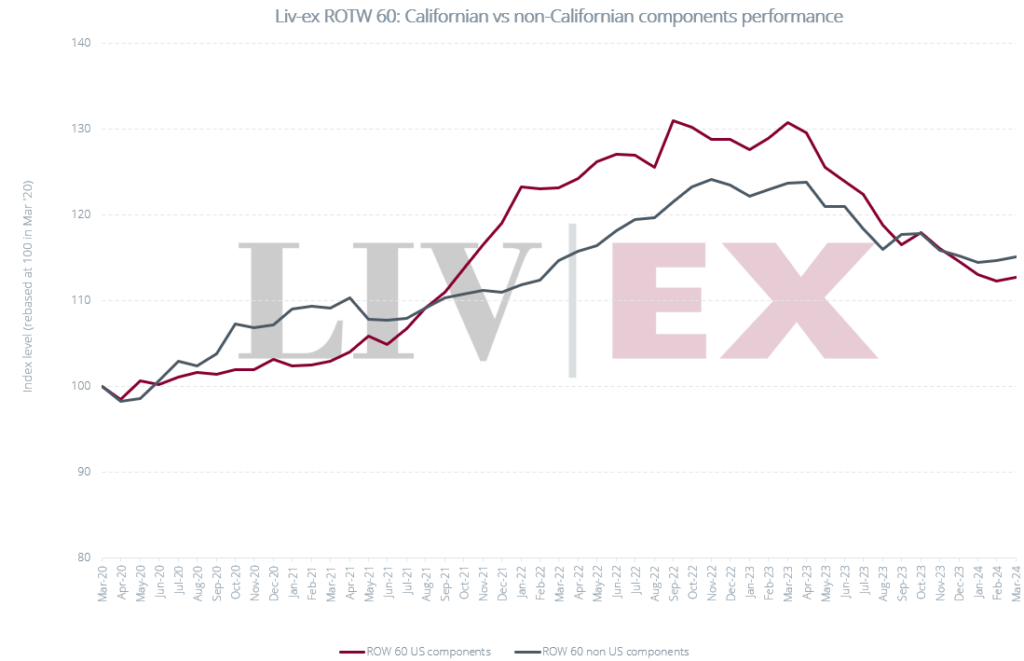

However, the chart below shows that while the Californian components of the Rest of the World 60 may be currently bringing the index down, they also clearly outperformed their non-US components during the 2021/2022 fine wine market boom.

*NB as Seña was only added to the index in January 2023, the non-US components in this graph do not include the wine.

Indeed, as fine wine prices skyrocketed in Bordeaux and Burgundy, they did so too in California. The region’s ‘cult wines’ surged in popularity during that time, and California had two new entrants in the 2022 Power 100: Scarecrow and Realm Cellars.

These wines consequently fell out of the Power 100 in 2023, as did Dominus which narrowly missed out on a place in the rankings. These relatively “new” wines which command very high prices prove harder for collectors to measure relative value, in the current market.

That can be said of most of the components of the Rest of the World 60, which are less familiar to most collectors and thus have a narrower market than the known names of Bordeaux, for example.

Producers and négociants will be hoping that the recent releases (Vega Sicilia Unico 2014, Promontory 2019, Ao Yun 2020, etc) will refocus buyers’ attention on the broader fine wine market, but that may take some time. Their “Place” in the fine wine world is in its infancy.