What’s happening in the market?

Italy has been in the spotlight since the start of December, accounting for 22.1% of total trade by value since Friday 1st.

Tuscany’s 12.3% share was secured by trades of the 2020 and 2015 vintages of Sassicaia, as well as Argiano, Brunello di Montalcino 2018 which remains among the most-traded wines by value and volume over the past month. Piedmont was slightly behind Tuscany, 8.9% of trade.

Burgundy and Bordeaux reigned strong in terms of trade by value. The top-traded wine by value since last Friday was Coche-Dury, Meursault 2021, and three vintages of Pétrus featured at the top of the rankings.

Today’s deep-dive: Who will be the next risers into the Power 100?

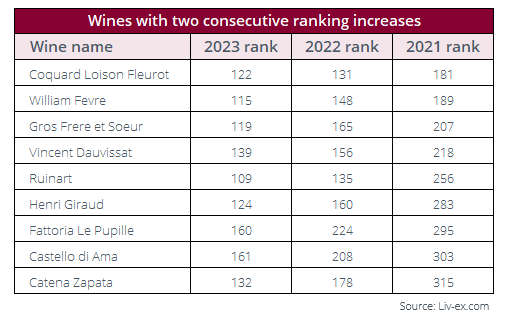

Liv-ex recently published the 2023 Power 100; while 414 brands met the requirements to be included on the list, as the name implies, only the top 100 made it into the final ranking.

In the report, we noted that the biggest price performers outside of the Power 100 are often brands on their way into a future edition of the rankings.

Based on this hypothesis, we’ve identified the wines that have gone up in the rankings two years in a row and posited which of them could potentially make it into the Power 100 next year.

Some Champagnes in the running

Champagne house Ruinart sits at the top of the list of contenders, having jumped 147 places since 2021. The biggest jump was from 2021 to 2022, when it rose 121 positions. While the brand’s trade value dropped in 2023, its trade volume rank shot up from 99th in 2022 to 32nd in 2023 which helped push it up the overall rankings.

Henri Giraud also made substantial progress, ascending 159 positions from 2021 to 2023. The brand saw a rise in terms of number of wines traded, from 269th in 2022 to 188th in 2023, accompanied by a modest rise in Market Price performance rank from 152nd in 2022 to 149th in 2023.

Tuscan contenders

From Tuscany, notable climbers since 2021 include Castello di Ama (up 142 places), Fattoria Le Pupille (up 135 places) and Ciacci Piccolomini d’Aragona (up 129 places).

In 2023, Fattoria Le Pupille held the 50th spot in terms of volume traded, a significant improvement on the last two years’ rankings. It was also ranked 108th in terms of Market Price performance in the latest edition, a rise from 2022 (250th) and 2021 (397th).

Castello di Ama follows closely, 161st overall in 2023. The brand saw an increase in both the number of its traded wines (from 177th in 2022 to 119th in 2023) and average trade rank (from 290th in 2021 to 194th in 2023). Price performance also improved significantly, from 378th in 2021 to 161st in 2023.

More white Burgundy in 2024?

William Fèvre is showing promising momentum, its trade value rank improving to propel the brand from 269th in 2021 to 177th in 2023. It has also seen growth in terms of volume traded, climbing from 197th in 2021 to 114th in 2023. While the brand has seen a drop in average trade price, its Market Price performance rank rose from 189th in 2022 to 142nd in 2023.

Fellow white Burgundy brand Vincent Dauvissat has gone up 79 places since 2021. A significantly higher number of its wines traded in 2023 than in previous years, increasing its ranking in that category from 148th in 2022 to 104th in 2023. The brand’s average trade price also increased from £1,046 in 2021 to £2,201 in 2023; where it suffered, however, was in terms of its Market Price performance. In that category, the brand dropped from 45th position in 2022 to 132nd in 2023.

Note: This analysis is speculative; market dynamics over the next year will heavily influence the performance and ultimate placement of these wines.

In case you missed it:

Here’s what we’ve been reading:

- Liv-ex: Burgundy’s rebound: Share of trade almost doubles week-on-week

- The Drinks Business: Liv-ex: flight to quality continues as Californian fine wines show buoyancy

- Financial Times: Stagnation nation: governing the UK when ‘there is no money’

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.