The 2023 Liv-ex Power 100 – Gimme Shelter

- The 2023 Liv-ex Power 100 reflects a market in the middle of a correction. Major indices have retraced more than 12% year-on-year, and trade value and volume are down on the exchange.

- Amid increasing risk aversion, Burgundy and California buyers narrowed their focus to top brands.

- The natural beneficiary of this was Bordeaux, which is the best understood and least risky market there is. The region gained five wines in the Power 100.

- Limited price performance hindered major red Burgundy producers. Brands with a high number of labels, white Burgundy producers in particular, thrived in this edition of the Power 100.

- Unlike last year, 54 brands in the Power 100 recorded a negative price performance.

Introduction

The Power 100 is a ranking of fine wine brands that reflects trade on the global marketplace over 12 months. It takes into account a range of criteria such as price performance, average price and value and volume traded on Liv-ex.

Last year’s report identified signs of an impending slowdown in the fine wine market; this year, we’re firmly in it. The Liv-ex Power 100 2023 is a reflection of a market knee-deep in a price correction.

All the major Liv-ex indices have retraced more than 12% year-on-year, and the Bordeaux 500 is approaching the double-digit mark. The Rhône 100 and the Champagne 50, the two worst-performing sub-indices of the Liv-ex Fine Wine 1000, are down 20.6% and 19.4% year-on-year. These downward movements are mirrored in the number of wines traded on Liv-ex this year, which was lower than in 2022, as were trade value and volume.

Interestingly, the 12 months to 30th of September 2023 showed more labels traded (LWIN7s) on the exchange but fewer individual wines (LWIN11s) than last year, signaling a flight to quality (a trend whereby investors tend to shift their allocations away from riskier investments and into safer ones).

*LWINs, or Liv-ex Wine Identification Numbers, are unique 7, 11, 16 or 18-digit codes. The 7-digit code (LWIN7) refers to the wine itself (I.e. the producer and brand, grape or vineyard), while LWIN11 adds vintage information.

As risk aversion took hold of the market, collectors narrowed their focus to the highest quality wines, either at brand or at vintage level. Because of this, the number of brands that qualified for inclusion in the Power 100 was down 2.1% this year; nonetheless, there were still 414 brands in the running.

The dataset considered covers the year from 1st October 2022 to 30th September 2023. The rankings are then calculated based on several weighted criteria including price performance, the number of a brand’s wines traded and the cumulative value and volume of that trade over the selected period. You can read the full methodology at the end of the report.

The 2023 Power 100 is a price performance story, but a very different one to last year’s; the running question, rather than which brands climbed the highest, is perhaps which have suffered the least. In 2022, fewer than 30 of the brands eligible for the Power 100 recorded a negative price performance over the 12 months considered – in this edition, the number climbed to 216, 54 of which are in the top 100 brands. As a result, the final list is skewed towards brands with a high number of traded labels and relatively high liquidity.

Regional breakdown of wines in the Power 100

California’s cult wines take a hit

California provides a good example of this aforementioned flight to quality; the region lost five wines in the Power 100 year-on-year, but its trade share remained relatively stable (it fell from 6.9% to 6.1% this year).

In the 2022 edition of the Power 100, California saw two new entrants, Scarecrow and Realm Cellars, possibly the result of collectors casting their nets wider in an upward-moving market. Many wines from the region surged in popularity during that time, and saw their prices rise accordingly.

These wines are not universally understood and loved in the same way that Burgundies are, for example, but they command very high prices (the average cost of a bottle from Napa exceeded $100 this year, according to Silicon Valley Bank’s direct-to-consumer wine survey). The current tougher market conditions mean that collectors are prepared to pay less for these relatively newer wines.

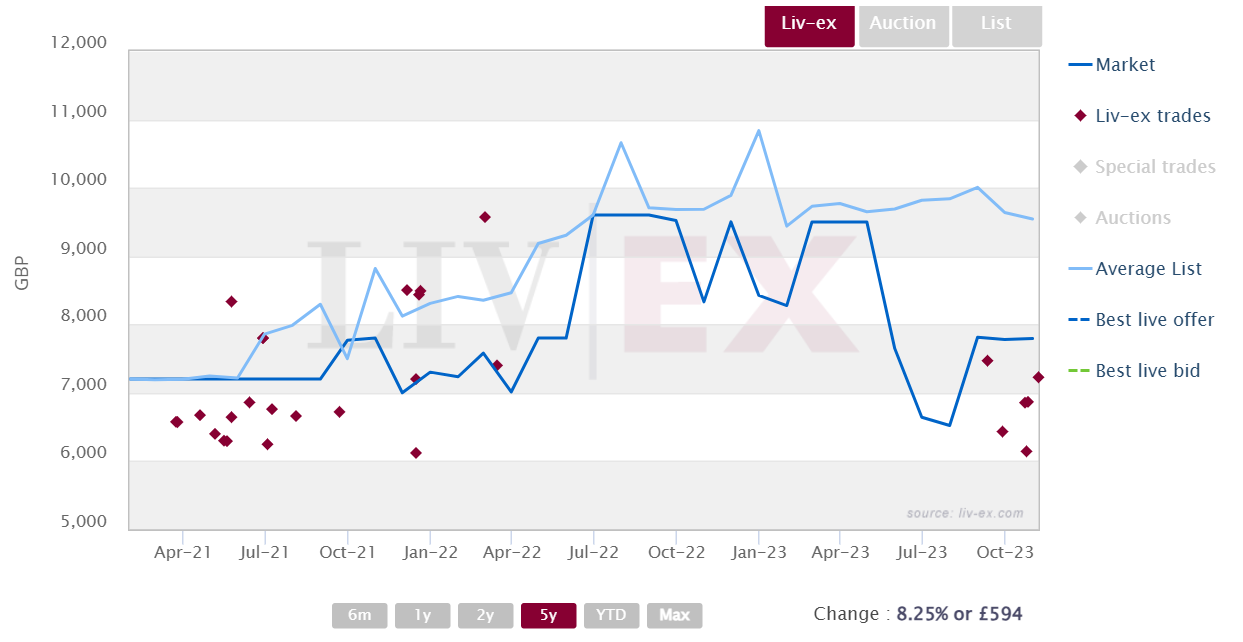

Take Scarecrow 2018, for example – the wine has a Market Price of £7,326 per case, higher than Château Lafite Rothschild 2018’s £6,600 per case. The chart below shows a widening gap between the wine’s Market Price, the level it is currently trading at, and its average price on merchants’ lists.

Scarecrow, Cabernet Sauvignon, Rutherford 2018 trades on Liv-ex

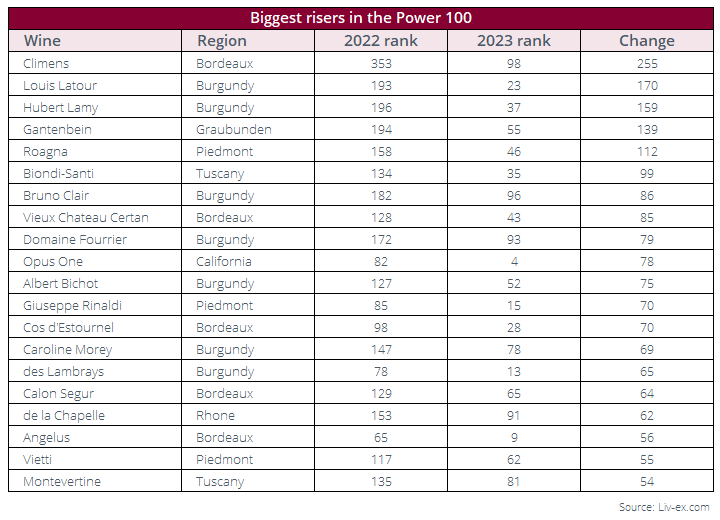

That’s not to say that the cult of California is over. Top brands from the region are still garnering a lot of interest, which is reflected in the 2023 Power 100 rankings. Opus One was among the biggest risers in this year’s edition, climbing from 82nd to 4th, and Screaming Eagle featured in the top ten brands ranked by trade price. Dominus also narrowly missed out on a place in the Power 100, coming in 102nd.

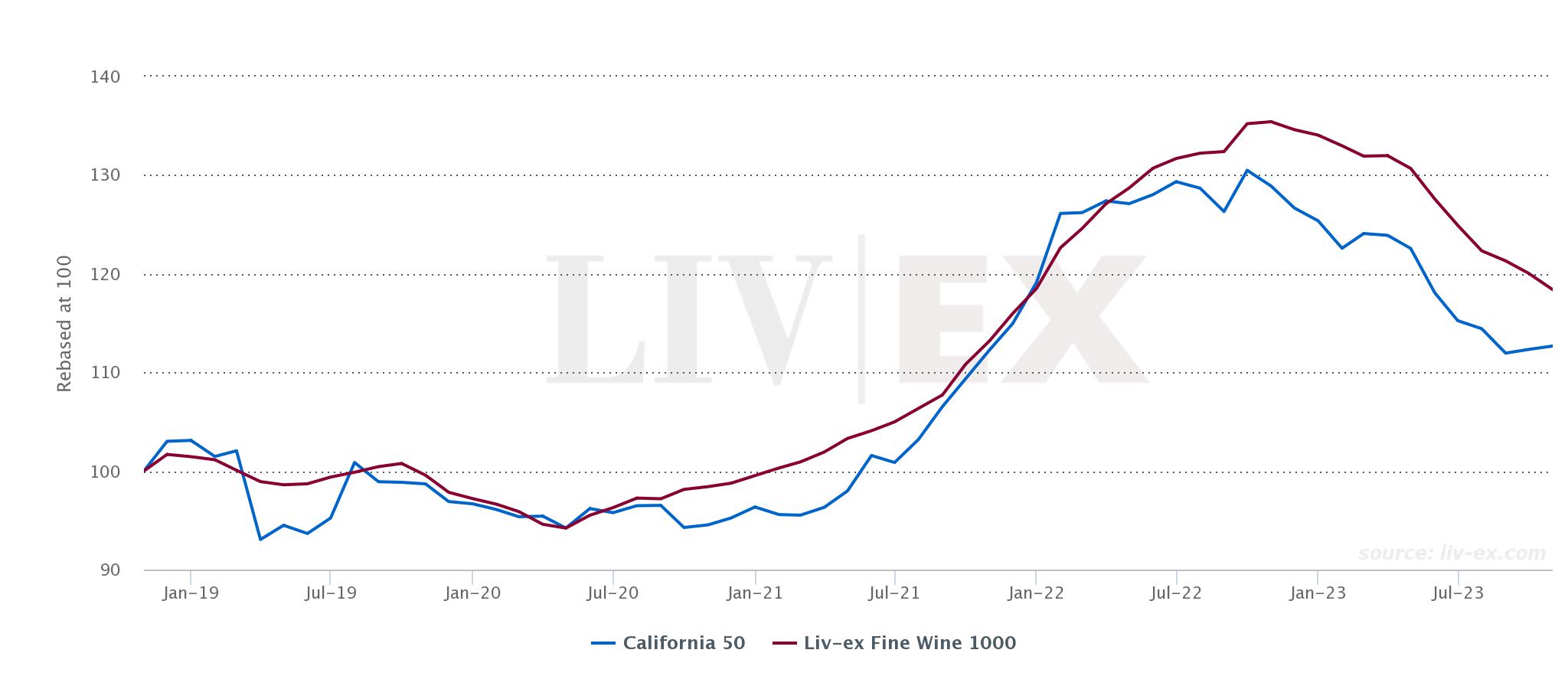

Clearly, there is an appetite for these top Californian brands, although they are also undergoing a significant price correction. The California 50, which tracks the price of the ten most recent vintages of the five most active Californian wines, has fallen 12.6% year-on-year, exactly in line with the Liv-ex Fine Wine 1000.

* Made using the Liv-ex Charting Tool.

Is the Burgundy bubble bursting?

Burgundy is in some ways similar to California, only more mainstream. From January 2021 to October 2022 when it hit its peak, the Burgundy 150 index rose 68.4% but it is now pulling back hard (-15.4% year-on-year) as prices are undergoing a correction. After gaining six wines in the Power 100 in 2022, the region has now lost two.

In the 2023 edition of the Liv-ex Classification, we highlighted the broadening Burgundian presence in the rankings, which we attributed to buyers seeking relatively affordable labels compared to the most established (and eye-wateringly expensive) ones. This phenomenon had already been noted in the 2022 Power 100, titled ‘All about Burgundy’; the surge in demand for the region, which was at the time the fastest expanding in the secondary market, was partly driven by négociant labels associated with the most powerful domaines.

As per the Power 100’s methodology, maisons and négociants are grouped in with domaines labels, which enlarges the pool of wines traded and boosts total trade value but also dilutes the brand’s average trade price. Charles Lachaux, for example, saw the price of some of its wines go up by over 1,000% in 2021-2022 as collectors sought entry-points into famed estates such as Domaine Arnoux-Lachaux. Since 2022, however, demand for Charles Lachaux labels has been declining, possibly due to these (unsustainable?) price increases.

In the 2023 Power 100, Domaine Arnoux-Lachaux was thus negatively affected by the price performance of its own wines, but also by the reduced trade value and volume of its related négociants labels. Generalised risk aversion and the significant price rises recorded across the region mean that some of the ‘newer’ Burgundy brands that had entered the Power 100 in 2022 have fallen out as collectors seek safety (and profits) in blue chip labels.

There are some exceptions to this, of course; one notable one being Kei Shiogai, which took the top spot in terms of price performance. The brand saw its Market Price increase by 185.7% year-on-year, making it 94th in the 2023 Power 100.

Bordeaux is back

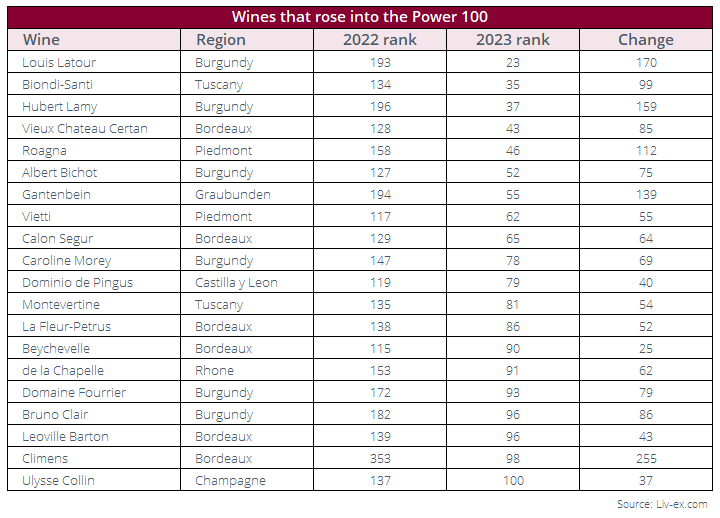

Bordeaux emerges as the natural winner here. It’s the least risky market there is, the best understood; collectors know what to expect from these wines, which is quality at a certain price, and relative liquidity. As such, Bordeaux has added five wines to the Power 100 this year, including some brands that had dropped out in 2022: Vieux Château Certan, Château Calon Ségur, Château Beychevelle and Château Léoville Barton. These strong and stable brands were pushed out when newer brands from Burgundy or California entered the rankings. Château Climens also rose from 353rd in 2022 to 98th this year, as a result of a brand repositioning under new ownership.

Italy gained one brand, Vietti, which performed particularly well on the number of wines traded (see more below). Dominio de Pingus joined Vega Sicilia as the second Spanish brand in the Power 100, buoyed by a positive price performance and the value and volume traded on the exchange, especially of its PSI and Flor de Pingus labels. One Swiss brand also entered the rankings, Gantenbein, which shone with its 10.8% price performance.

Power 100 rankings and regional trade

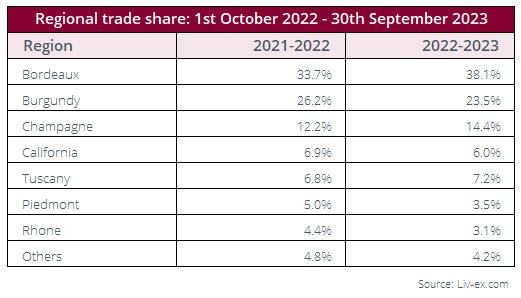

These numbers are to some extent reflected in the regional breakdown of trade by value for the 12 months ended 30th September 2023. Bordeaux has seen its share rise from 33.7% to 38.1%, while Burgundy and California dipped slightly.

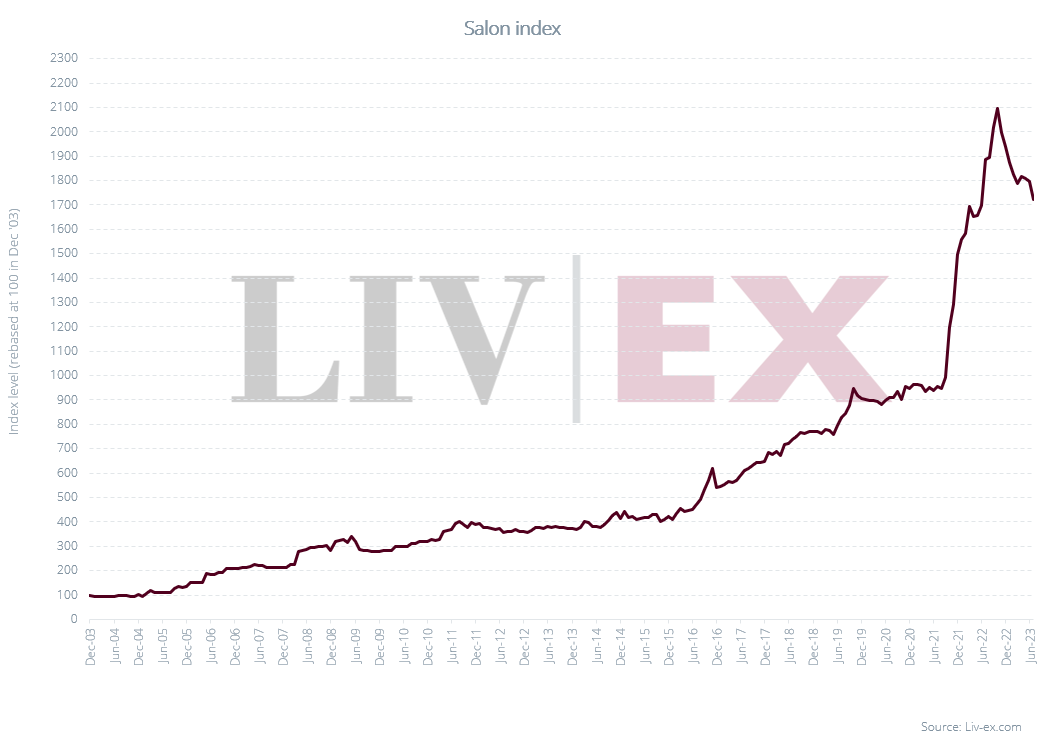

Champagne is an outlier, as it lost a brand but gained market share. The region has remained very active even as it is correcting (the Champagne 50 index is down 19.4% year-to-date), benefitting from the high volumes of wines produced and the resulting significant levels of trade. Salon, the Champagne brand which dropped out of the Power 100, lost out in part due to the comparatively limited amount of trade it saw. As the most expensive brand from the region, it also suffered from a negative price performance (-5.7%) as its prices are pulling back after they soared in 2022.

The best and worst performers in the Power 100

The brands that flew too close to the sun

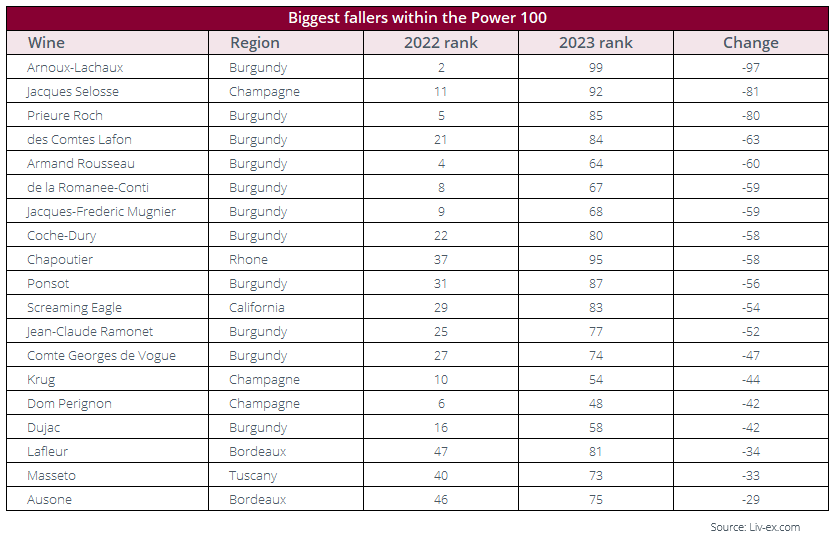

Interestingly, Burgundy had the most wines in both the list of biggest risers and fallers inside this year’s Power 100.

The theory that wines that rise the highest also tend to correct the hardest is very much supported by the biggest red Burgundy brands. The price performance engine has run out of steam; the likes of Arnoux-Lachaux, Prieuré Roch, Coche-Dury, Armand Rousseau and even Domaine de la Romanée-Conti all saw a significant drop in the Power 100.

Arnoux-Lachaux dropped 97 places and just about secured a spot in this year’s rankings, its average Market Price down 19.0% year-on-year. Likewise, Domaine de la Romanée-Conti slid from 8th to 67th place in 2023 despite maintaining its position as the most-traded brand by value on Liv-ex; the 13.9% decline in its Market Price ranked it 405th in terms of price performance. For the wines that reach such heady heights (for example Champagne’s Salon, mentioned above), the fall is often a painful one.

Strength in numbers

Luckily for Burgundy brands, price performance is not the only criteria for inclusion in the Power 100. As highlighted above, for example, Domaine de la Romanée-Conti remained buoyed by its wines’ high prices, which easily make it the most traded brand by value on Liv-ex despite a drop in price performance. The other place where the region remains competitive is in the number of labels traded per brand.

Indeed, Burgundy producers and négociants have an advantage over regions such as Bordeaux in terms of the number of labels they produce, which tend to range from Grands Crus to drinking wines. While they do produce more limited volumes of each wine than a Bordeaux estate would, in the 2023 Power 100, this criterion gave some producers a leg up in the rankings.

The continuing impact of this is particularly visible for white Burgundy: Joseph Drouhin/Drouhin-Vaudon and Louis Jadot both ranked among the top ten brands by number of wines traded. Furthermore, as these white wines are often bought to be drunk, their supply generally diminishes quickly on release, keeping prices relatively stable. Caroline Morey and Hubert Lamy, for example, both featured among the top ten brands according to price performance, recording average Market Price increases of 19.3% and 11.7% respectively.

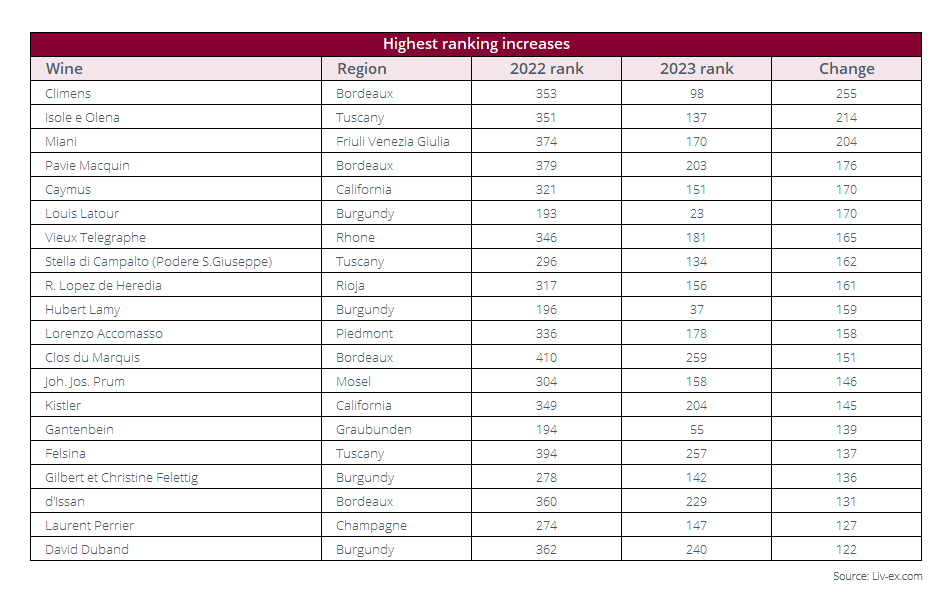

The story is much the same in Piedmont: producers such as Roagna, Rinaldi, Vietti and Gaja all comprise a high number of labels, some of which offer a good price point compared to Conterno and Bartolo, appealing to the value buyer. Vietti came in 21st in terms of number of wines traded, and Roagna 38th, increasing its overall rank from 158th in 2022 to 46 in 2023. Giuseppe Rinaldi also featured on the list of the biggest risers overall, going from 85th to 15th.

Conclusion

The downward-trending market makes this year’s results particularly interesting. Price performance being one of the parameters considered, unless brands have particularly high-value wines (e.g. Domaine de la Romanée-Conti) or a significant number of labels traded, they struggled or fell out of the Power 100 altogether.

Two seemingly contrasting trends were at play in 2023. One is the flight to quality, the search for safe bets amid tough trading conditions. While in upward moving markets, collectors tend to test their mettle slightly and explore ‘new brands’ that are less well-established globally, in a downward curve, they are reverting to what they know (read: Bordeaux).

On the other hand, the price performance of some major brands took a hit, knocking them down in the rankings (Arnoux-Lachaux, Coche-Dury, Armand Rousseau, etc.). As a result, brands with a high number of labels traded (Burgundy négociants, Piedmont producers) benefitted, especially on the more affordable end of the spectrum. White Burgundy producers in particular were on the rise as merchants and collectors focused on drinking wines rather than stock to hold.

Often, the biggest price performers outside of the Power 100 are on their way into the next edition of the rankings. Looking at those big movers now might inform next year’s list – will Dom Ruinart, now 109th (up from 135th in 2022 and 256th the year before) make its way into the Power 100 2024?

Power 100 methodology

To calculate the rankings, we took a list of all wines that traded on Liv-ex in the last year (from 1st October 2022 to 30th September 2023) and grouped these by brand. As is now standard, Burgundy labels with both maisons and Domaines were combined as one.

We then identified brands that had traded at least three wines or vintages and had a total trade value of at least £10,000.

Brands were ranked using four criteria: year-on-year price performance (based on the Market Price for a case of wine on 1st October 2022 with its Market Price on 30th September 2023); trading performance on Liv-ex (by value and volume); number of wines and vintages traded; and average price of the wines in a brand. The individual rankings were combined with a weighting of 1 for each criterion, except trading performance, which had a weighting of 1.5 (because it combined two criteria).

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £100m worth of wine and the ability to trade with more than 620+ other wine businesses worldwide. They also organise payment and delivery through their storage, transportation, and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Independent data, direct from the market.

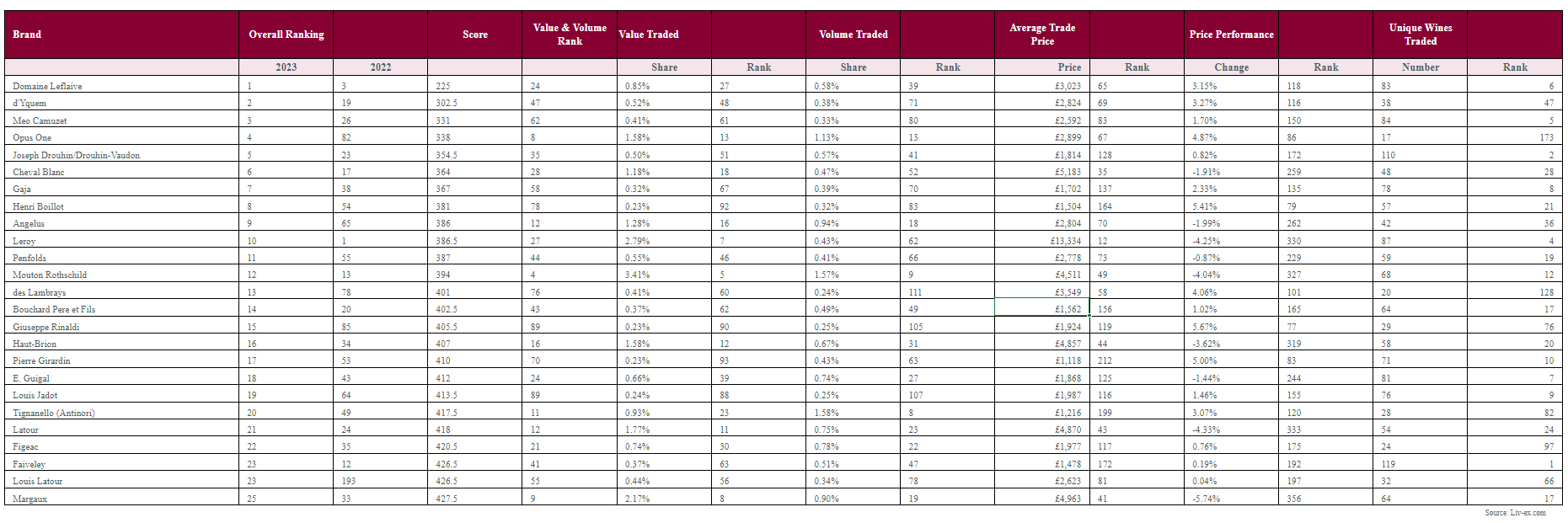

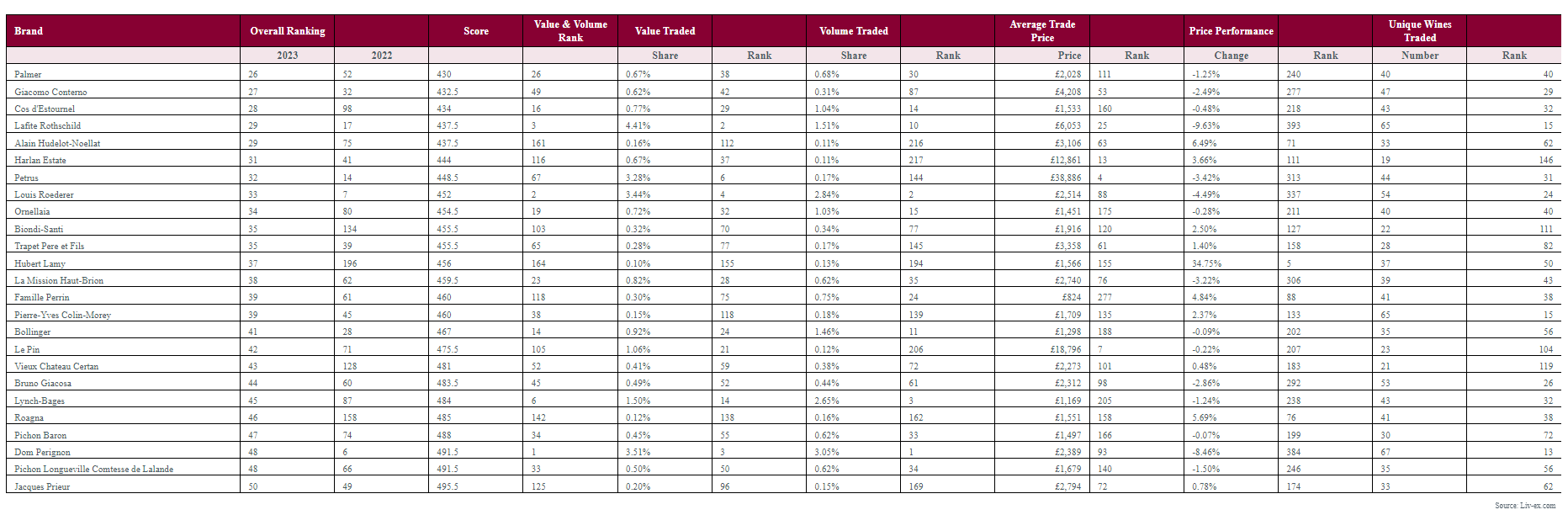

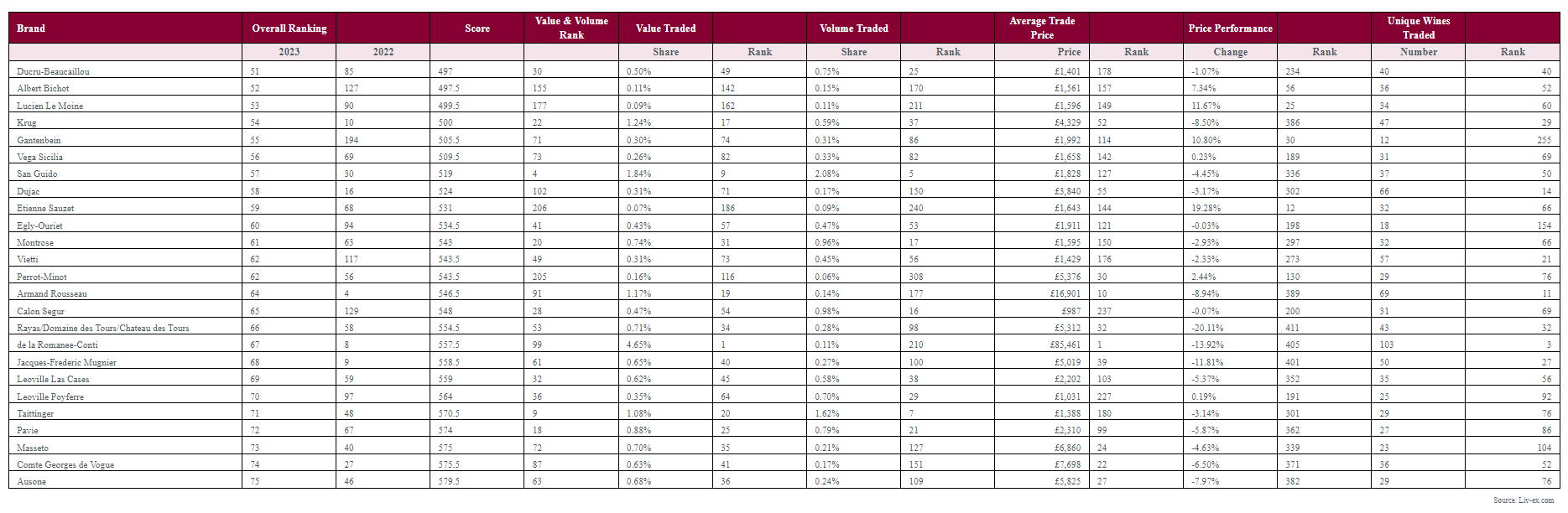

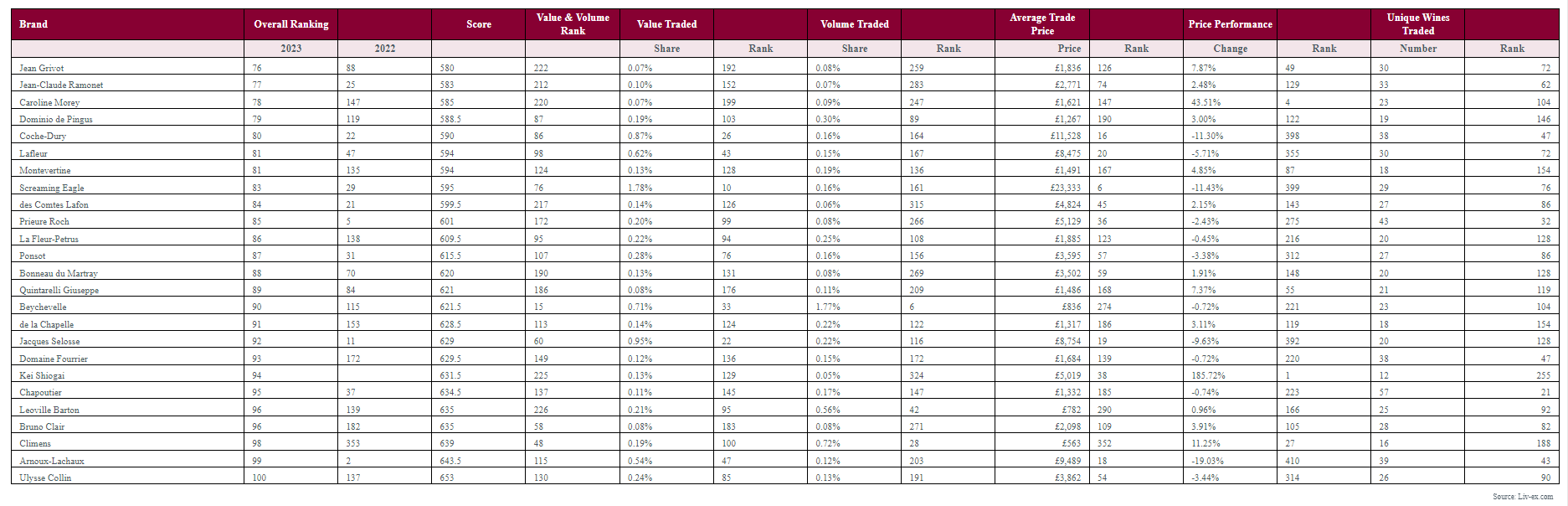

Full ranking tables

Click on each table to enlarge.