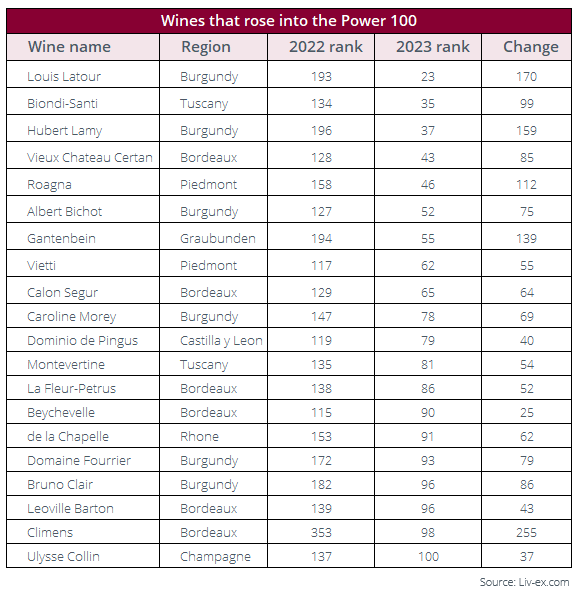

- The new entrants into the 2023 Power 100 hailed from Burgundy, Bordeaux, Tuscany, Piedmont, Champagne, the Rhône, Castilla y Leon and Graubunden.

- Among them, Burgundian brand Louis Latour ranked the highest in 23rd place.

- Burgundy continues to see a rise in the number of labels traded on the exchange.

In the 2023 Power 100, 20 newcomers entered that did not feature in the 2022 rankings.

Of these additions, six came from Burgundy, six from Bordeaux, two from Tuscany, two from Piedmont, and one each from Champagne, the Rhône, Castilla y Leon and Graubunden.

Burgundy dominates

Burgundy maintained its position as the region with the most wines in the Power 100, although the count decreased slightly from 39 last year to 37 in 2023.

Despite this reduction, Burgundy’s popularity on the exchange was made evident by 2,016 labels (LWIN7s) trading in 2023 so far, surpassing the 2022 figure of 1,972. However, the region’s current share of trade value and volume is lower than last year.

Louis Latour was the highest-ranked new entrant into the Power 100 in 23rd place, driven by a significant surge in trade value. This increase was fueled by transactions in, the brand’s top labels, for example the Romanée-Saint-Vivant Grand Cru, Les Quatre Journaux, Montrachet, Chevalier Montrachet, Corton Charlemagne, Chambertin and Echezeaux, increasingly considered to offer quality and relative value against other producers in these appellations.

Some Bordeaux are back in the top 100

Unlike Burgundy, Bordeaux saw a growth in the number of its wines in the Power 100, rising from 25 in 2022 to 30 in 2023. Despite a decrease in the number of LWIN7s traded on the exchange (373 in 2023 versus 406 in 2022), Bordeaux’s share of trade value and volume increased to 40.0% and 36.76% of the total respectively.

In our report, we attributed this phenomenon to a flight to quality whereby buyers are narrowing their focus to the top brands and the most established regions. Bordeaux brands benefited from this movement, as reflected in the increase in the number of the region’s labels in the 2023 Power 100.

Vieux Château Certan made a return to the list. The brand recorded a decrease in average trade price in 2023, however its price performance ranking improved by an impressive 140 positions, firmly securing its place in this year’s rankings.

Both Châteaux Calon Ségur and Beychevelle fell out of the rankings in 2022 and came back in in 2023. Calon Ségur saw its trade value double this year while Beychevelle, a popular brand in the Asian market, saw its price performance ranking improve by 52 positions, making room for a strong comeback in the 2023 Power 100.

Likewise, Château Léoville Barton faced a setback in 2022, possibly negatively influenced by the influx of many Burgundy wines in the previous edition of the Power 100, but is back this year in 96th position.

Italy adds new labels to the rankings

Two wines from Tuscany, Biondi-Santi and Montevertine, made their appearance in the Power 100 this year alongside two wines from Piedmont, Roagna and Vietti.

Roagna gained popularity after featuring in Vogue in 2020 which captured the attention of buyers in the US and UK markets. One of the brand’s key strengths lies in its relatively affordable price point, which makes it an attractive choice for value-conscious buyers, especially compared to fellow Piedmont producers such as Conterno and Bartolo.

Other key findings in the report:

- Amid increasing risk aversion, Burgundy and California buyers narrowed their focus to top brands inside the region.

- The natural beneficiary of this flight to quality was Bordeaux, the best understood and least risky (most liquid) market there is. The region gained five wines in the Power 100.

- Negative price performance hindered major red Burgundy producers. Brands with a high number of labels, white Burgundy producers in particular, enjoyed relative stability amid the downward market, buoyed by relative volume and earlier drinking windows.

The full report is available for all to read here: https://www.liv-ex.com/2023/11/2023-liv-ex-power-100-gimme-shelter-2/

Not a member of Liv-ex? Request a demo to see the exchange and a member of our team will be in touch with you shortly.