The 2022 Liv-ex Power 100 – All about Burgundy

- Burgundy reigns supreme in this year’s Power 100, with last year’s bullish momentum rolling into this year and reflected in a continued broadening of wines traded and price rises.

- Champagne’s star continued to rise, with quality and value being the key drivers.

- For the first time ever there are no Bordeaux labels in the top 10.

- The Italian surge abated a little, but Tignanello put in a stellar performance.

- All the brands in the top 100 have risen in price in what has been a blistering trading environment.

Introduction

We dubbed last year’s Liv-ex Power 100 a ‘rebalancing act’. The Covid-19 pandemic and the buying spree it unleashed propelled the world’s great fine wine labels back to the top of their perch, from which some had been unseated in 2020.

Both the 2020 and 2021 rankings highlighted an important trend in the secondary market; greater diversity and the ongoing move away from Bordeaux.

By contrast, this year’s Power 100 is more focused. One region in particular dominates the rankings – Burgundy.

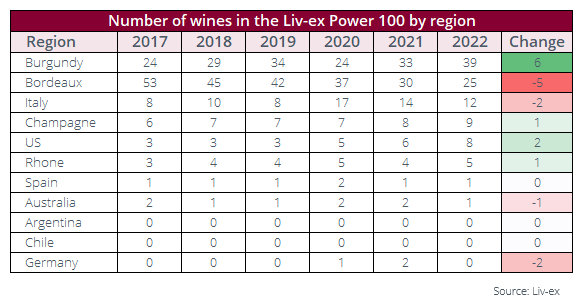

Supercharged by market confidence, ready money, and anticipation of a tiny 2021 release, Burgundy’s momentum was already building in last year’s Power 100 with big price performances and an increase in the number of wines ranked in the top 100. This year, Burgundy added six more entrants, for a total of 39; its highest-ever total and highest number since the last Burgundy surge in 2019.

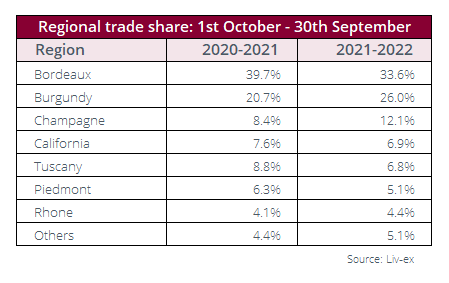

Champagne too saw its 2021 momentum spill over into 2022, as collectors sought value and portfolio diversity. Between them, Burgundy and Champagne siphoned off 9.0% of the total market share from other regions over the course of the year, largely at the expense of Bordeaux and Italy.

And with that in mind, both tables show (in part) why this year’s list looks the way it does, and why some of the previously high-flying Italian and Californian brands have slipped down the rankings – for this year at least.

This is not to say that there has not been demand across other regions. Of the 422 wines that qualified for the Power 100 this year, fewer than 30 had a negative average price performance – and none in the top 100 itself.

As always with the Power 100 there are some key factors to bear in mind. The data set analysed covers the year from 1st October 2021 to 30th September 2022.

The rankings are based on several weighted criteria of which price performance, while important, is only one. As such, it is worth looking where each wine ranks according to each criteria, as well as the overall ranking.

For example, a Burgundian estate may rank highly for the number of its wines that traded, the cumulative value of that trade, average price per case and price performance, but its trade volume may be quite small.

By contrast, a Bordeaux estate could rank highly for its trade value and volume but is likely to rank lower for the number of wines being sold and price performance.

Looking at the rankings in detail allows for a more nuanced view. The full methodology for the Power 100 can be found at the end of this report.

Top 10

- The top five wines are all Burgundies

- Domaine Arnoux-Lachaux had the biggest rise into the top 10 (60 places)

- Louis Roederer Cristal ranked first overall for volume traded

For the first time ever, no Bordeaux wines feature in the top 10. Not a single First Growth from either bank.

This year they have been totally usurped by Burgundy and Champagne. Four Burgundies and one Champagne have risen to displace Château Lafite Rothschild (2nd last year), Château Mouton Rothschild (6th), Pétrus (7th), Sassicaia (8th) and Château Margaux (10th).

The biggest risers into the top 10 were Jacques-Frédéric Mugnier (rising 38 places), Prieuré Roch (33 places) and Domaine Arnoux-Lachaux (up 60 places).

At the top for the third year in a row is Domaine Leroy. As our methodology explains, we combine maison and domain labels under one brand. For Leroy this is both a strength and a weakness.

On the plus side, it significantly enlarges the pool of wines recorded as trading at what are high volumes for Burgundy. It also provides a major boost to the brand’s total trade value.

On the other hand, the inclusion of the maison wines significantly dilutes the average trade price. Those who have ever looked at the cost of a grand cru from Domaine Leroy recently will know that they are not bought at £6,700 per dozen anymore – or even in packs that large either.

However, it demonstrates the continued power of the Leroy brand. Such is the clamour to taste these wines yet so limited is supply that eager buyers are seeking out the closest thing to it. And it keeps the prices rising. In the 2020 Power 100 Leroy’s average price performance was 8.6%. Last year it was 39.0% and this year it was a staggering 59.5%.

The other estate associated with Leroy (but treated separately) is Domaine d’Auvernay. Although not in the top 10 (it slipped down the rankings this year due to low trade figures), it saw average price increases of 127.2% and had the second-highest average trade price behind Domaine de la Romanée-Conti.

This fever around the most sought-after Burgundies continues to disenfranchise all but the wealthiest collectors who, in turn, continue to drive the expansion of the category, as we shall now examine.

Burgundy

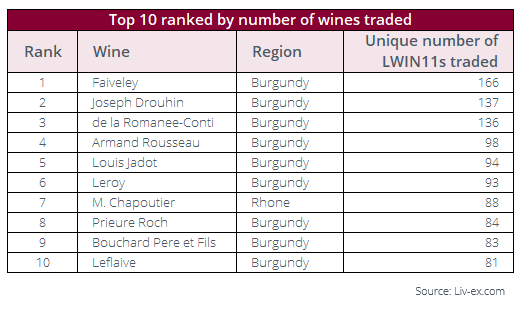

- Domaine Faiveley had the largest number of wines traded

- Domaine de la Romanée-Conti ranked first for trade value and average trade price

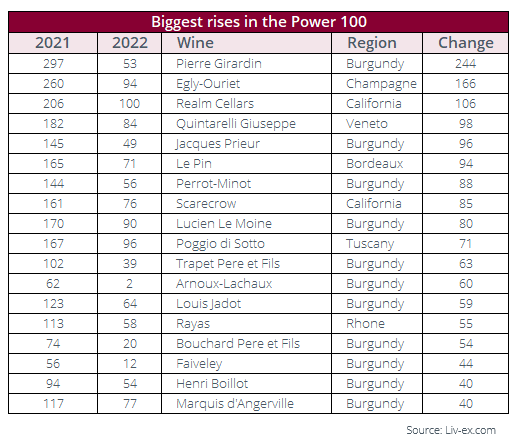

- Pierre Girardin rose 244 places into the top 100

Burgundy’s previous surge was in 2018-2019. Prices then plateaued but took flight once more over the course of the pandemic.

But they are doing so against the backdrop of a much broader market for Burgundy. It remains the fastest expanding region in the secondary market. 829 Burgundy wines traded in 2018. In 2022 there were 1,859.

One of the region’s peculiarities is the number of wines a single domain can produce and the addition of négociant labels only adds to this pool. In some cases it is these wines where recent price increases have been greatest.

This has already been discussed in relation to Domaine Leroy, but it is also true of this year’s second most powerful label, Domaine Arnoux-Lachaux.

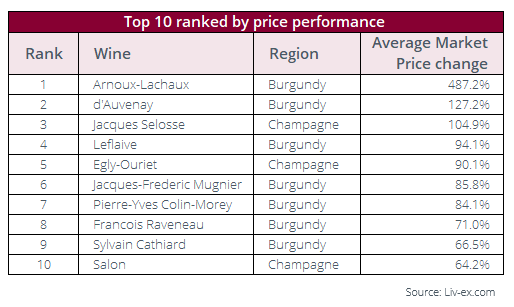

The estate has been one of the region’s rising stars for a few years now, but demand exploded in 2021-2022. Its average price performance was 487.2% but certain wines rose more than 1,000%. Some of the biggest price rises were for the négociant label Charles Lachaux, which (like Leroy) offered an accessible point of entry to a rising brand and have since hit new highs.

Conversely, trade for both Arnoux-Lachaux and Charles Lachaux has declined as 2022 has gone on, especially for the latter. It is possible that it is a brand that has already grown too hot for some to countenance buying.

This once again raises the question of Burgundy’s price sustainability. Speculation is undoubtedly an issue but ultimately, there is still not enough supply if demand continues to rise.

Furthermore, the upcoming 2021 vintage release will yield hardly any fresh stocks. This will likely keep prices high, but some prices may not rise at quite the same speed.

Champagne

- Egly-Ouriet rose furthest to make it into the top 100 (166 places)

- Jacques Selosse had the best price average performance (104.9%)

- Salon was the highest ranked Champagne for trade value and average trade price

Champagne has been a quiet presence in this year’s Power 100 with just nine brands in the ranking. However, it is a building force in the secondary market which has truly begun to breakout; amassing high levels of trade, showing strong price performances and with a growing number of brands qualifying for inclusion – even if they have not quite made it to the top just yet.

The standout brand has been Louis Roederer’s Cristal, one of three Champagnes in the top 10. It has been the top traded wine by volume and third top-traded by value over the latest Power 100 year. It first entered the top 10 in the 2019 Power 100 and has not left it since.

Dom Pérignon may have a stronger price performance and Krug may have a higher average trade price but measured by its sheer levels of trade, Cristal has become the standard bearer of Champagne’s secondary market drive.

Another cluster of brands worth keeping an eye on as the category evolves are some of the ‘grower’ labels such as Jacques Selosse.

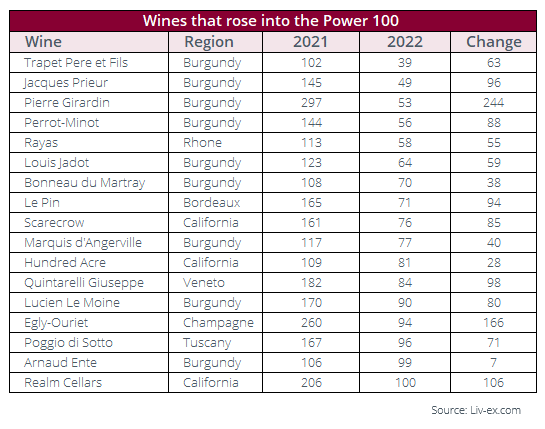

Selosse (which entered the Power 100 last year) jumped 25 places to 11th this year, because of strong price performance and a high average trade price. Egly-Ouriet is another smaller house that made it into the top 100 this year, up from 260th last year.

And finally, although they missed making the top 100, the second and third best brands for price performance, trailing only Arnoux-Lachaux, were both Champagnes, Ulysse Collin and Jérôme Prévost.

Bordeaux

- Château Figeac had the best price performance among Bordeaux brands in the top 100 (24.2%)

- Le Pin had the biggest rise back into the top 100, up 94 places.

- Château Lafite Rothschild was the second wine traded overall by value

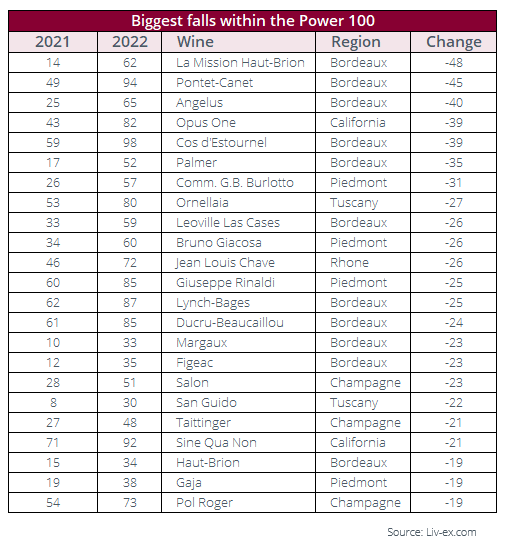

It would be easy to see the situation of Bordeaux’s brands as a negative. The region’s total trade continues to shrink, the number of brands in the top 100 has fallen to a new low, and the highest-ranked brand (Château Mouton Rothschild) is 13th.

Compared to the price performances of other regions, Bordeaux looks weaker despite its performance being above the average performances seen in pre-pandemic Power 100 rankings.

Looking more closely the bright spots begin to appear. Château Lafite Rothschild is still the second most traded brand by value and one of the top 10 by volume.

Château Cheval Blanc only dropped one place with a solid all-round performance, while Château d’Yquem rose 20 places with a sizeable number of vintages trading and high trade value.

Anticipation of Château Figeac being promoted in the Saint-Emilion classification this September (which did indeed happen) made it one of Bordeaux’s best price performers but it still dropped down the rankings. On the one hand, many other wines had much better price performance but also its trade value and volume fell as many buyers had stocked up the year before in anticipation of its promotion.

Fumbled en primeur campaigns and stock retention is now a long-standing issue for Bordeaux which continue to hold its wines back in the secondary market. Nonetheless, few regions offer the concentration of brand power, prestige, availability, longevity and, increasingly, good value that Bordeaux does. Compared to the soaring prices of topflight Burgundy or even some prestige Champagne, good claret remains a solid proposition.

Italy

- Tignanello was the only top 100 Italian brand from last year to rise in the rankings

- Quintarelli Giuseppe and Poggio di Sotto returned to the top 100 this year

- Sassicaia is the top ranked Italian wine by value and volume

It was only two years ago that Italian trade seemed to be on an unstoppable rise. That tide has receded a little, however. The high US tariffs on EU (European Union) wines from which Italy was excluded were an important factor in its secondary market success from 2019 to early 2021.

Since those tariffs were abolished, trade for Italian wines has declined, from around 15% of trade in last year’s report to 11% this year.

Many Italian wines have dropped down the list. A bit like Bordeaux, total trade by value and volume is still strong but price performance has slowed, especially compared to Burgundy and Champagne.

Sassicaia remains the highest-ranked Italian brand and the sixth most-traded by volume, though it dropped 22 places to 30th.

The Italian brand on the move though is Tignanello. It rose 16 places to 49th through a combination of high trade by volume (seventh overall) and thus a high total trade value. It also helps that it is the cheapest Italian wine in the top 100, with an average case price of £1,076.

California and the Rhône

- Realm Cellars had the highest rise into the top 100 (106 places)

- E. Guigal was the third highest-ranked brand overall by volume traded

- Between the Californian and Rhône brands in the top 100, Château Rayas had the best price performance (44.0%)

Much like Italy, with Burgundy’s dominant performance in the secondary market, there appears to have been less focus on California and the Rhône. On the other hand, both regions added brands to this year’s top 100 – two from California and one from the Rhône.

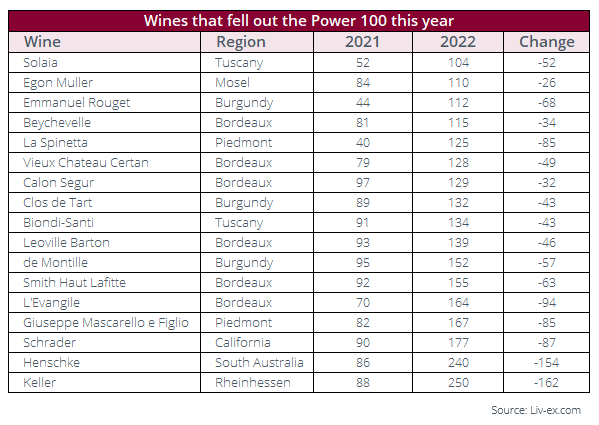

Despite the new additions, many of California’s leading labels slipped in the rankings this year, with Screaming Eagle falling nine places. The high prices of top Napa Valley wines mean they score highly when it comes to trade by value and average case price. But they have fewer wines trading, volumes are low and, again compared to other regions, their price performance is not as high.

Nonetheless, Harlan Estate climbed 26 places. Scarecrow and Hundred Acre both saw big jumps into the top 100 as well – both returning after a long hiatus.

Despite only having five wines in the top 100, the Rhône enjoyed quite a bit of success. Jean-Louis Chave dropped 26 places but the other four brands all rose.

These included Château Rayas, back into the top 100 with a jump of 55 places thanks to a strong average trade price and price performance.

The top-ranked Rhône label was Michel Chapoutier which, like Guigal, can offer a multitude of different wines thanks to its hybrid estate-négociant business model.

Conclusion

The Power 100 is a snapshot of the ever-changing landscape of the secondary market. This year’s list caught Burgundy at the very height of its latest upswing.

Yet, already, the direction of the market in 2022 suggests change is on the way. Just as we saw in 2019, Burgundy’s latest surge may be dizzying but could be swiftly stymied by a lack of supply and an increasing reluctance to pay such steep prices for handfuls of bottles. The higher it flies, the thinner the air, and the fewer buyers there are.

Furthermore, as 2022 has gone on, the monthly performance of the Burgundy 150 index has sputtered. It ran flat in June and August, rose 1.8% in September, and rose 0.7% in October – in each of those last two months it recorded its smallest monthly gains since August 2021.

The clear momentum is now with Champagne. Cristal and Dom Pérignon have been at the forefront of trade throughout the year. The Champagne 50 is the best performing Liv-ex Fine Wine 1000 index over one year and is quickly closing in on the Burgundy 150 as the best-performer year-to-date.

In truth, the market has moved in a positive direction. As mentioned previously, all the brands in the top 100 saw their prices rise.

But market headwinds are strong and further price rises may not be as easy to come by. After some record years as the market expanded, the rate of growth, measured by number of wines trading and qualifying for the Power 100, was not as great this year as it was last year.

Between 1st October 2021 and 30th September 2022 12,332 wines were traded from 1,694 producers, respective increases of 4.2% and 1.6% on the same period a year earlier. The number of wines qualifying for inclusion was 422, a rise of just 0.3%.

Overall, the market continues to bring in new wines from across the world – Kumeu River from New Zealand, Chacra in Argentina, and Spain’s Telmo Rodriguez were among the new qualifiers this year – and the market remains broader and more balanced than it was a decade ago.

Nonetheless, looking forward to next year’s Power 100, it is hard to shake the feeling that things are going to look quite different once again.

Power 100 methodology

To calculate the rankings, we took a list of all wines that traded on Liv-ex in the last year (from 1st October 2021 to 30th September 2022) and grouped these by brand. As is now standard, Burgundy labels with both maisons and domains were combined as one.

We then identified brands that had traded at least three wines or vintages and had a total trade value of at least £10,000.

Brands were ranked using four criteria: year-on-year price performance (based on the Market Price for a case of wine on 1st October 2021 with its market price on 30th September 2022); trading performance on Liv-ex (by value and volume); number of wines and vintages traded; and average price of the wines in a brand.

More than 12,332 different wines were traded on the exchange in this period. These were grouped into 1,694 brands, of which 422 qualified for the final calculation. The individual rankings were combined with a weighting of 1 for each criteria, except trading performance, which had a weighting of 1.5 (because it combined two criteria).

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £80m worth of wine and the ability to trade with more than 600 other wine businesses worldwide. They also organise payment and delivery through their storage, transportation, and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Independent data, direct from the market.

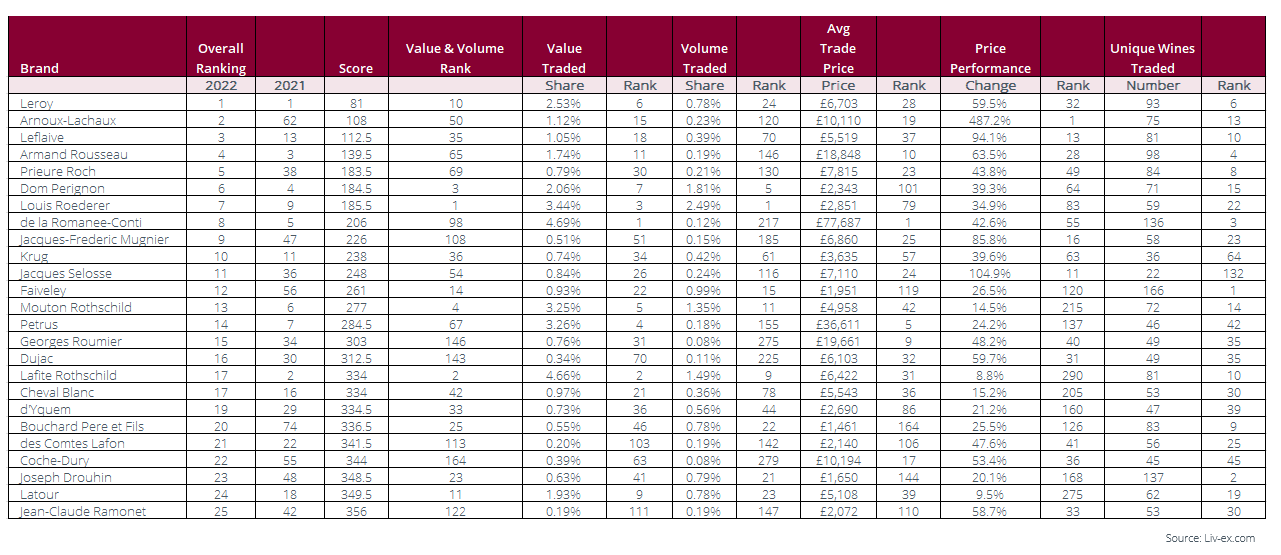

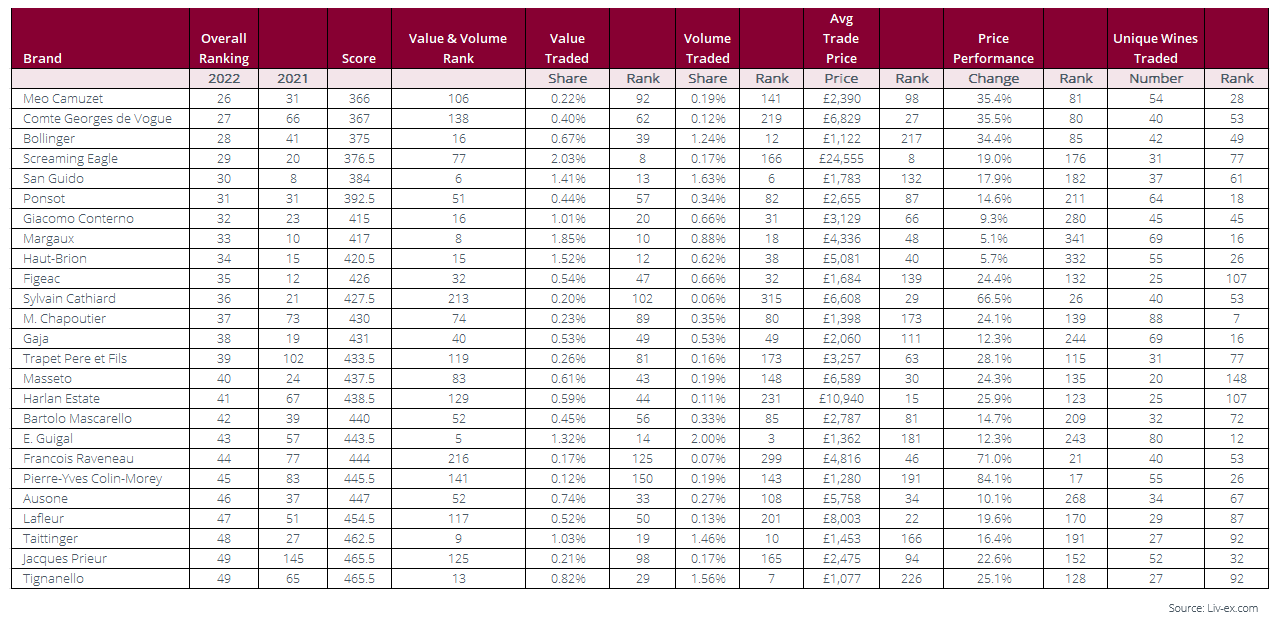

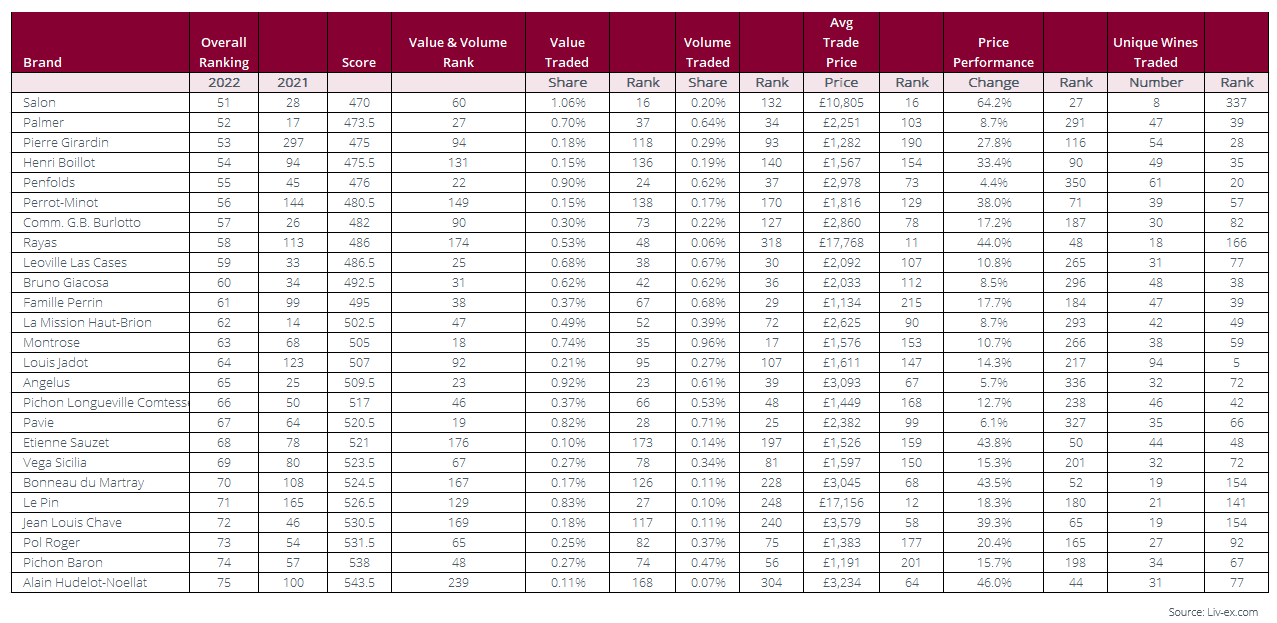

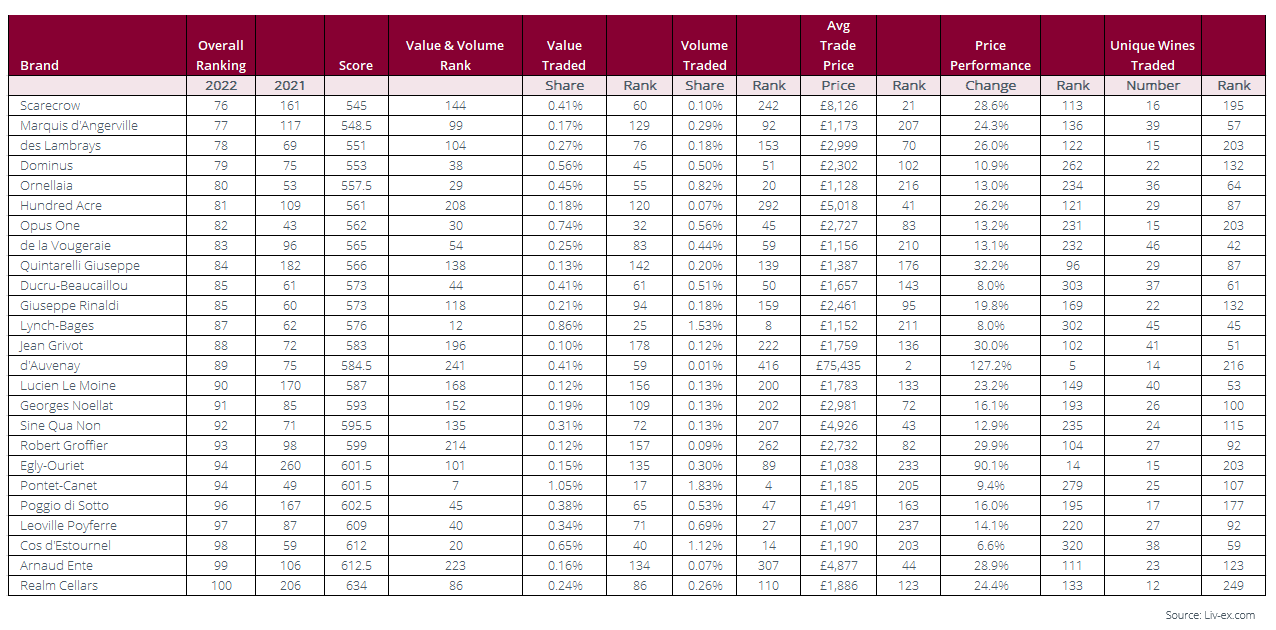

Full Ranking Table

Click on each table to enlarge.