Bordeaux En Primeur 2022 – Where is the magic?

Introduction

The 2022 vintage is one of superlatives: highest temperatures and lowest amount of rain recorded during the summer, highest scores received, and of course, the highest average release price in recent history.

As the quality of the vintage had been widely lauded by critics despite the challenging weather conditions experienced last year, price hikes were expected going into the campaign. Liv-ex members predicted a 7% year-on-year increase; the reality was much starker, as the ex-London price of wines covered by Liv-ex was up 20.8% on average from 2021.

The 2021 campaign planted the seed of scepticism in the market. The wines were largely released at the same price as the 2020s, despite being scored two points lower by Neal Martin on average. As a result, a vintage with the potential to reinvigorate the system ended with some disillusionment and with merchants and collectors alike asking what the point of this time-consuming event was.

This year, clearly, the question begs to be asked again: who is En Primeur for? The system has veered away from its origins as a means of providing working capital to the châteaux, some of which don’t need the support anymore.

It is also no longer an opportunity for collectors to acquire high-quality wine at the best price, as recent vintages attest. Nor does it consider that buyers are buying a wine without knowing how it will taste in bottle, or the opportunity cost of holding these great wines for anywhere from 10 to 30 years before they enter their peak drinking windows. At a time when inflation is rife, the cost of living is on the rise, fears of recession are growing and importantly, simply holding cash can give you a 5% annual return, it is not surprising that fewer are likely to buy an expensive asset with unknown returns.

Was it a campaign for merchants, then? It would seem not, as many are reporting offering discounts to clients to generate sales, cutting margins (and allocations) in the process. Granted, some are seeing success in spite of price increases, with customers still taking their allocations due to the quality of the vintage, or simply by habit. There will always be buyers of Bordeaux with pockets deep enough to keep buying regardless of price – but can they sustain the system, and if so, for how much longer?

We have said it before and we will say it again: the 2022 En Primeur campaign is another missed opportunity. The international trade was ready to promote and sell this great vintage, but they could not do so regardless of price. This has led to a difficult and costly campaign and sadly, despite the quality of the wine on offer, is unlikely to have encouraged a new generation of buyers.

Scores

There were initial concerns that the heat and drought of summer 2022 would lead to another 2003, and that the flash storms of June 18th may have damaged the vines in some domains. However, the advances in winemaking techniques and the vines’ surprising resilience to the heat (not to mention some long hard hours in the vineyard) resulted in what many believe to be one of Bordeaux’s greatest ever vintages – and the critics’ scores reflect this.

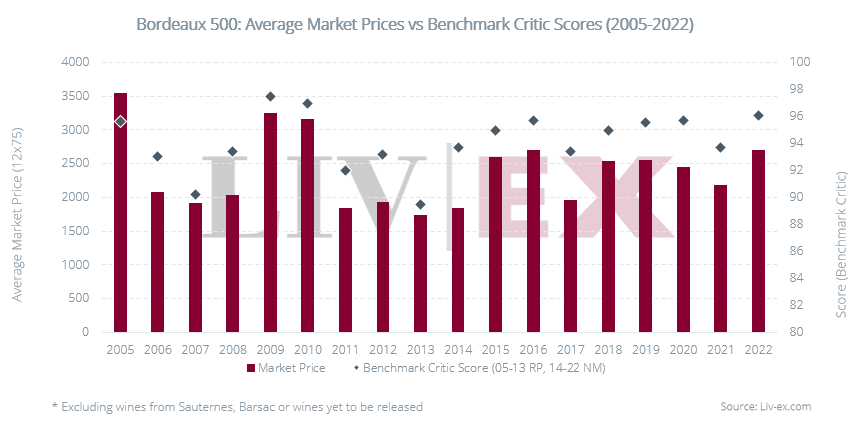

Neal Martin identified three standout wines as potential candidates for perfect scores, referring to them as the “snow-capped peaks” of the vintage: Château Léoville Las Cases, Château Cheval Blanc, and Château L’Eglise-Clinet. Looking at the average Benchmark Critic scores (Robert Parker until 2013, then Neal Martin), the chart below shows the 2022 vintage ranks higher than any other dating back to 2005.

While the 2022 vintage has the potential to rival the exceptional quality of the 2009 and 2010, its scores are more closely aligned with those of the 2020, 2019, and 2016 vintages. And despite their similar scores, the average release price for the 2022 vintage is 6% higher than the average Market Price of the 2016 vintage and equals the average price of the 2019 vintage, both of which are already physical. It’s also worth noting that Martin’s scores for the 2022 vintage are all barrel ranges, which means while they may go higher, they also have the potential to come in at the lower end of his range.

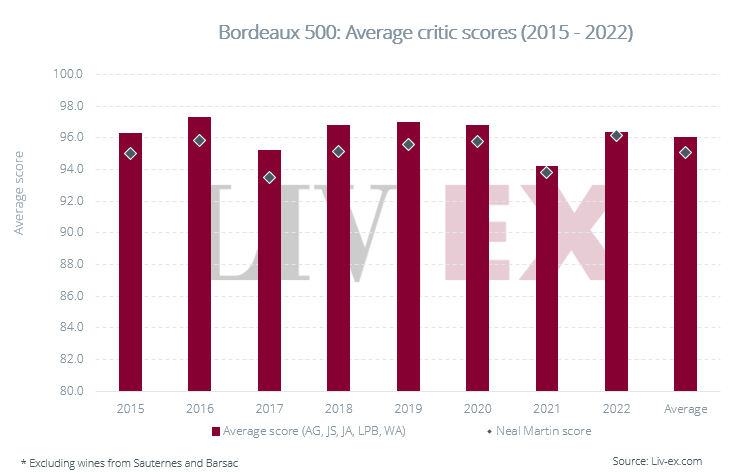

Interestingly, plotting the average scores of five other critics – Jane Anson (JA), Antonio Galloni (AG), Lisa Perotti-Brown (LPB), James Suckling (JS) and the Wine Advocate (WA) – the 2022 vintage is on par with 2015 but falls just below the 2016, 2018, 2019 and 2020 vintages.

While 2022 wines are unquestionably of high quality, its proclamation by many as ‘the vintage of the century’ should perhaps be taken with a pinch of salt (as should the influence of critics scores on price increases).

Liv-ex members can automatically populate their websites with critic scores and tasting notes

Year-on-year price changes

The average release price increase during the En Primeur campaign was 20.8% compared to 2021, markedly higher than the 7% anticipated by Liv-ex members. The vintage’s quality, as well as inflationary pressures and lower volumes released were all cited as reasons for rising prices.

That prices should be up year-on-year isn’t the issue; the 2022 wines are of far superior quality overall to the previous vintage. The main problem is that 2021 was released largely at the same price as the 2020 vintage, leading to one of the least successful campaigns in recent times. 2020 was itself priced 27% higher than 2019, despite lower scores on average, which counteracted the positive campaign of 2019 that had reawakened demand and rebuilt some faith in the system.

The bullish price hikes meant that while some wines were cleverly priced to offer relative value (more on this below) and thus sold well, others simply got it wrong and saw their sales suffer. Château Angélus, for example, was released at £4,296 per 12×75, up 37.7% year-on-year. The wine has already traded 6.8% below its release price on the secondary market. Château Troplong Mondot, was released at £1,224 per 12×75, up 43.7% on the 2021 release price. This wine was last traded at £1,050, 14.2% below its release price on the secondary market. This is of course the wholesale market, but it reflects the trade’s view of the prices of the wines released.

While some merchants reported not taking up full allocations of certain wines (or none at all) in light of the prices, it’s worth noting that some had a successful campaign, in part due to their focus on quality rather than price, but also due to collectors simply buying out of habit. This pattern naturally benefits bigger brand names, some of which sold well despite price hikes. But as Jane Anson (Inside Bordeaux) points out, ‘high prices of classified 2022 leaves merchant houses with less available budget to work with for buying petit châteaux’.

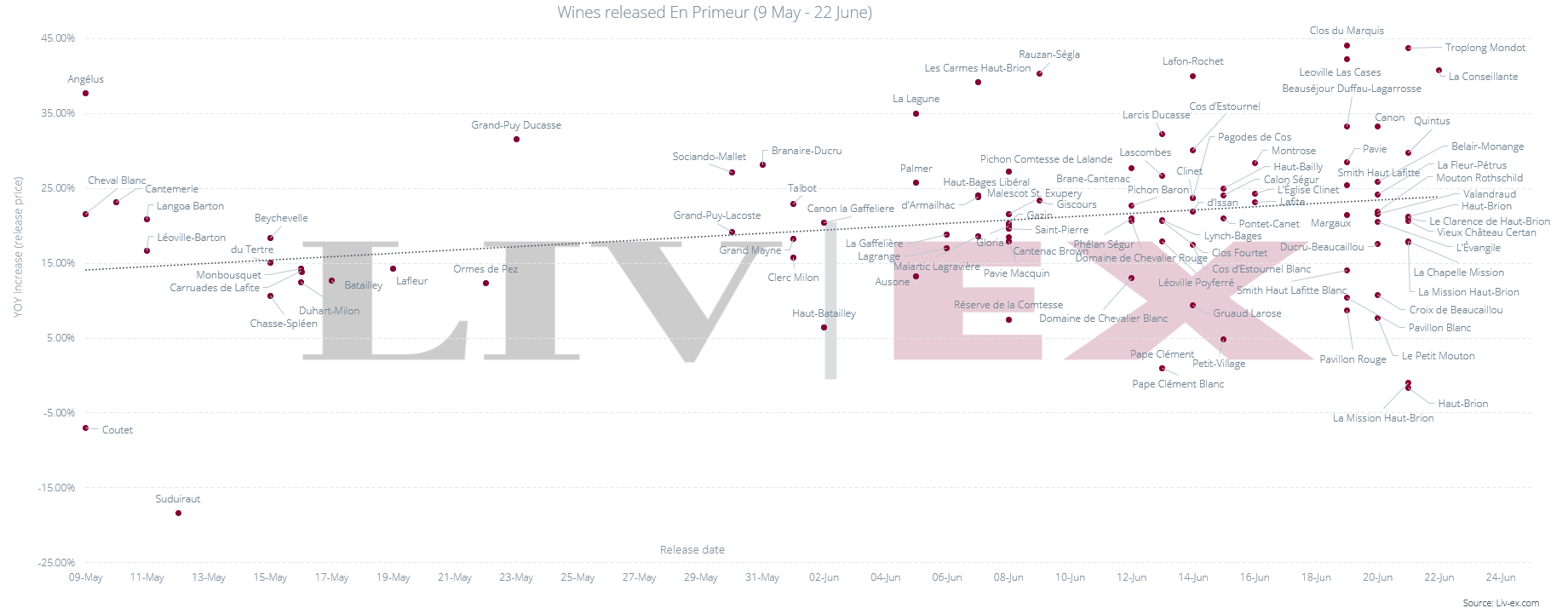

Depending on who you ask, the timing of the campaign was either a blessing or a curse. The chart below plots the 2022 releases with the percentage increase in their release price compared to 2021. The campaign was disrupted by Vinexpo, which resulted in a notable lull in the middle and two weeks of little-to-no releases. The initial slow pace of the campaign spread fatigue among merchants and collectors, with some describing the campaign as ‘tedious’ and deciding to shift their focus elsewhere quite early on.

The general impression, backed by the rising trendline in the chart above, was that châteaux were holding fire to gauge just how far price increases could be pushed. In the words of one merchant, ‘too many châteaux are keeping up with the neighbours and seemingly totally unaware of/indifferent to what back vintages of their wines in comparable vintages trade for’.

When the pace of releases eventually picked back up, the ‘lower end (sub 50 euros) struggled’, according to one merchant, who noted that the ‘timing of releases was not good when up against bigger names’. However, another said ‘The order in which the wines released was actually really good, it meant that a lot of junior/baby wines got focus at the beginning of the campaign with the biggest ticket items being reserved for the end. Everyone buys those anyways, so it meant we finished on a high’.

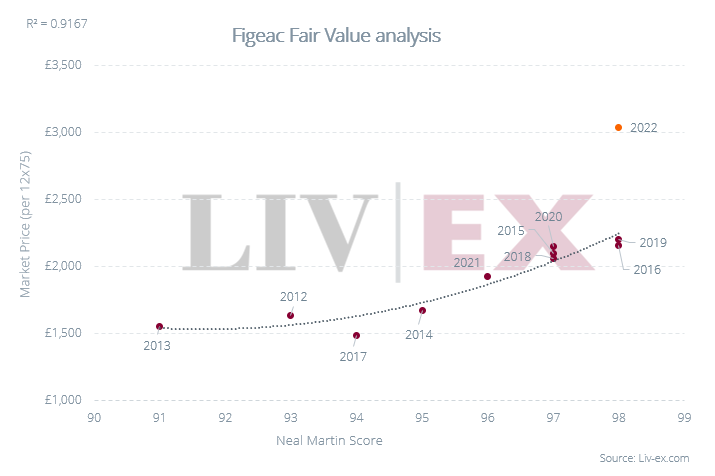

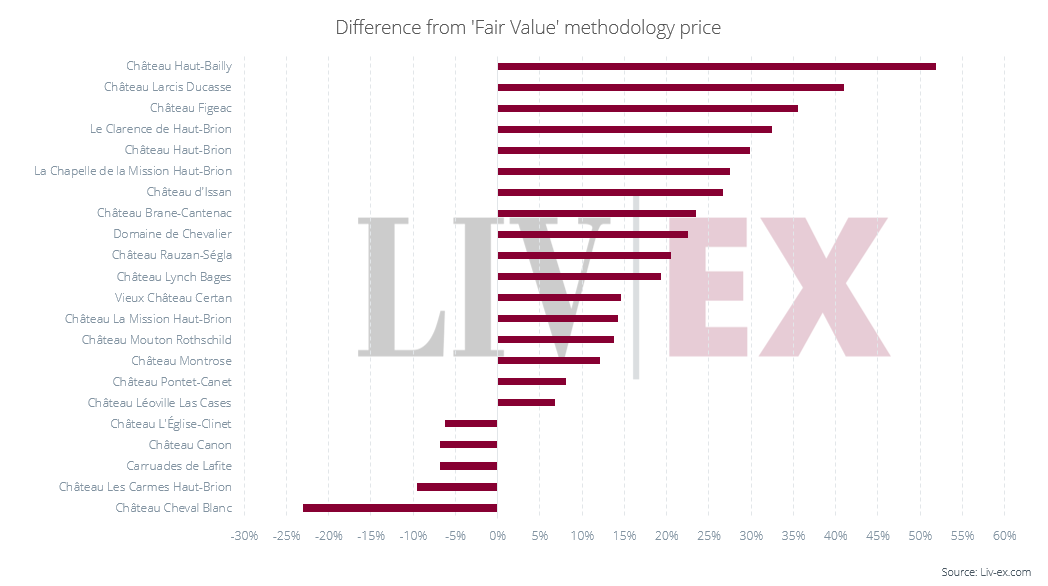

And oh, did we finish on a high. Château Figeac, one of the last wines to be released, produced the largest price increase on the 2021 release, with a significant 55.2% jump. This could perhaps be attributed to a 20% decrease in volume released compared to the previous year, but more pertinently was a result of its promotion to Premier Grand Cru Classé A in the latest revision of the Saint-Émilion Classification in September 2022.

Regardless of the reasons, the wine’s price ended up being 36% above the price implied by Liv-ex’s Fair Value methodology, as shown in the chart below. This tool is designed to measure the relationship between price and quality and establish the fair price of a wine based on its correlation with age and critic scores, taking into account the vintages already in the market.

Liv-ex ‘Fair Value’ methodology helps in determining the right price for a given wine so you can make smarter trading decisions

The best releases of the campaign

While the picture painted above is less than rosy, it isn’t black and white. Some producers reaped the rewards of good timing and clever pricing, even with a considerable price increase.

Among the wines released whose Market Prices are correlated to Neal Martin scores, the number offering good value based on Liv-ex’s ‘Fair Value’ methodology was significantly lower than those which didn’t.

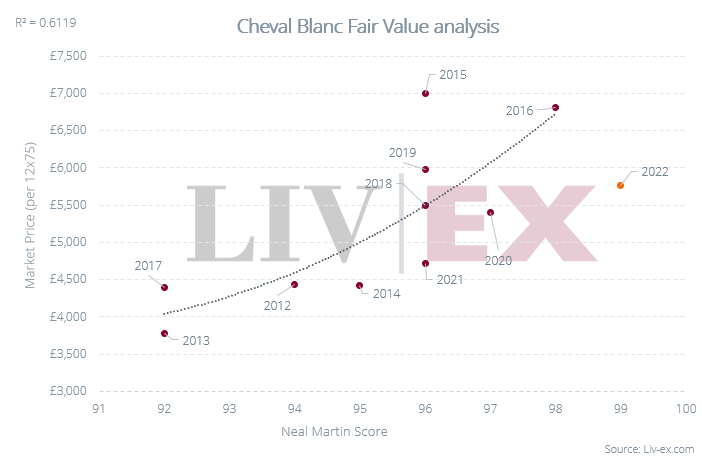

Château Cheval Blanc, despite a 21.5% increase in price year-on-year, was priced 23% below the fair value line. It also has the potential to receive a perfect score from Neal Martin, who gave it a barrel range of 98-100 points.

Merchants widely quoted this release as a success, in part due to the early release date which meant it didn’t get drowned amongst others. Releasing early also proved a good move in a tight market with limited cash to spend on all the wines throughout the campaign. The slightly-above average price increase accounts for the fact that this is potentially the highest-scoring Cheval Blanc in the past decade, while taking into account the price of physical vintages on the secondary market.

Château Les Carmes Haut-Brion also stood out, with an above-average price increase of 39.2% on the 2021 release price landing it 10% below the fair value line. Likewise, the 2022 releases of Carruades de Lafite, Château Canon and Château L’Eglise-Clinet all offered value despite increasing their prices year-on-year.

Sales by value and volume

Among merchants, 2022 was a polarising campaign, despite having all the elements to be a good one. 2019 demonstrated that with high-quality wines and clever pricing strategies, it is possible to have a successful campaign amid global economic turmoil. 2022 certainly had the former, but in most cases lacked the latter, as many châteaux failed to take the macroeconomic context and the market fundamentals into account.

For some merchants then, it was ‘the worst campaign ever’, or at least since 2010 and 2014. ‘Almost nothing was met with real enthusiasm despite the clear quality of the wines’, said one merchant. Another commented: ‘I’m not really sure what the point of EP is. We don’t recognise the revenue until the wines land, so there’s little to no benefit to us right now. It takes two months out of our financial year to run the campaign and overall it’s significantly dilutive to the average margin we work on’.

Others, however, deemed 2022 ‘very successful indeed’. ‘The majority of the (UK) wine trade forgets that there are people out there who simply want to buy wine, and they want to buy the new releases’, said one member, who saw customer numbers on the rise, including some who had never bought En Primeur through them before.

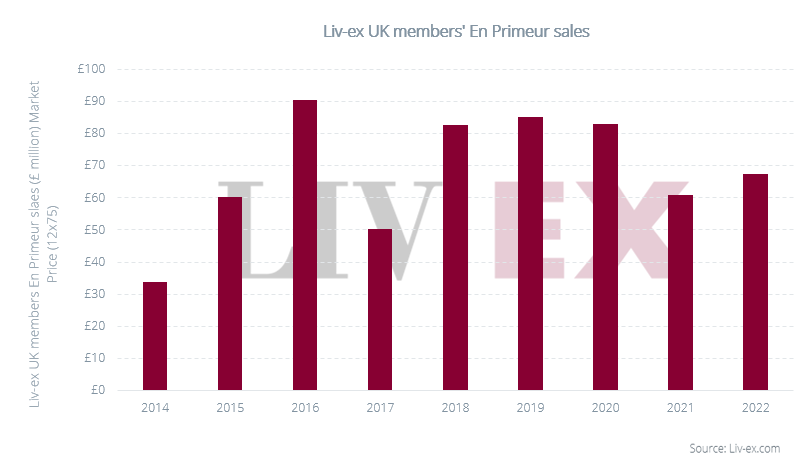

Although UK merchants reported an increase in sales value compared to last year, the number was markedly down from 2019 and 2020. The overall volume sold was down compared to 2021 and 2020. Many merchants dealt with a smaller customer base this campaign, limited to habitual buyers or those undeterred by the bullish pricing.

Several merchants were forced to reduce or cut their allocations of some wines strategically while attempting to remain in favour with négociants. There were widespread accounts of discounts given not only by merchants to collectors, but also by négociants in order to generate sales, albeit at the price of lower margins.

All in all, the 2022 campaign was considered a tale of ‘missed opportunity’ given the early promise of a candidate for the vintage of the century.

Liv-ex members can easily buy and sell En Primeur stock on our trading platform, without any added risk.

Secondary market activity

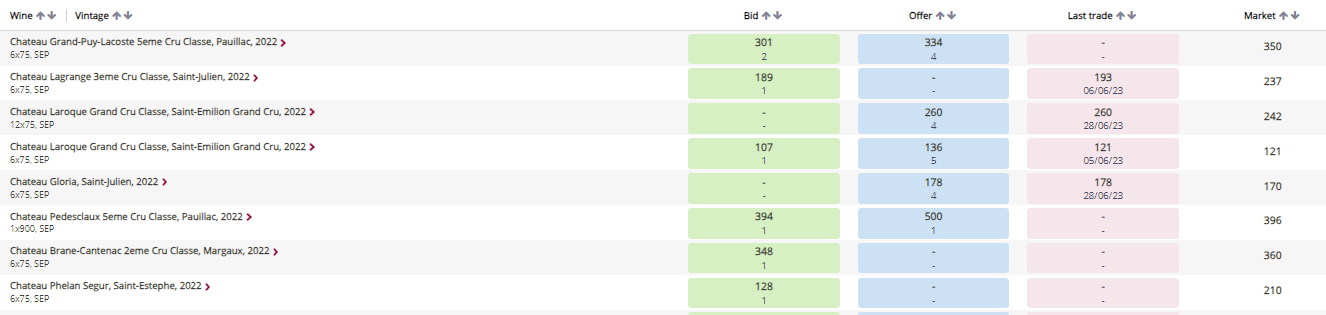

Currently, there are 114 live bids and offers for 2022 Bordeaux wines on Liv-ex, indicating an active interest in 2022 wines away from the constraints of the primary market. It is worth noting that the majority of recent trade prices on the platform have remained flat or even slid below the wines’ release prices.

Conclusion

The Bordeaux En Primeur 2022 campaign has generated mixed reactions and left many questioning its purpose and sustainability. In the words of one merchant, ‘it makes no sense’.

The pace and shape of the campaign left many frustrated. Merchants around the world commit two months of their year to the Bordeaux releases, which does not come cheap. But with lower sales than anticipated and lower margins due to discounts becoming the norm, some were forced to pull part of their sales teams off the campaign altogether. For a few, regardless of the price increases, the quality of the vintage and the desire to secure allocations, coupled with lower volumes released, resulted in a ‘better than expected’ campaign.

The big talking point of course was the price. There was little question of the quality of the vintage, but buyers do not just consider quality. They have competing demands on their capital, more so now as interest rates rise. How far can the châteaux push prices?

That question of course can ultimately only be answered by them, but what is clear from this campaign, is that in raising their prices as they did, they sacrificed volumes sold. Collectors were deterred by the prices, knowing that they could acquire comparable vintages with a few years of bottle age for less than the 2022 release. The wide availability of the 2018, 2019, and 2020 vintages contributed to this perception.

Ultimately, the buyer’s perception of value plays a vital role in maintaining the system, and this year’s pricing left many confused. Sales of the 2022 vintage fell short of 2020 by both value and volume. Where capital was committed, it was to a smaller pool of wines. The big Bordeaux châteaux have high margins, so they can afford to sell ever-decreasing volumes en primeur. But for those lower down the pecking order, the picture is far from sanguine. Already the 2023 campaign is a daunting prospect.

Liv-ex is the global marketplace for the wine trade. The fastest way to price, buy and sell wine.