The Fine Wine Market in 2022

Introduction

Last year’s review of the fine wine market was all about records; the Liv-ex indices hit record highs, there were record levels of trade (both value and volume), and a record number of wines traded.

It was a bull market powered by the low interest rate environment and a growing interest in alternative, tangible assets in the wake of the Covid-19 lockdown. As a result, the market saw robust demand from both old hands and new entrants.

The 2021 report also asked if the bullishness would survive the return of tighter fiscal and monetary conditions. Inflation expectations were rising. This year has certainly put the market to the test.

The Covid era boom in the fine wine market (among others) masked the fragility of the global supply chain which began to show its considerable cracks as the world (China excluded) emerged from lockdown. Russia’s invasion of Ukraine in late February added to the supply chain turmoil as energy prices soared.

As a result, inflation set in at higher levels than the financial markets or central banks expected. A series of aggressive rate hikes have followed leading to increased volatility in currency markets. Meanwhile China’s zero-Covid policy is driving that country, and by extension much of the rest of the world, to the brink of recession.

At a glance, the impact on the secondary market appears minimal. However, below the surface signs of the wider economic storm are apparent. There is a growing sense that the momentum carried over from last year had run out. The Liv-ex 100 fell for the first time in 18 months in July, and again in October and November. The Burgundy 150 index also saw smaller gains as the year went on, running flat in October and finally dipping in November.

In a survey of Liv-ex members, the outlook for the market was mixed, with a slight majority of respondents saying they were neutral to quite pessimistic about next year. When asked to estimate the closing level of the Liv-ex 100 in 2023, two respondents predicted it would close the year down by more than 25%.

Questions over the future of the market are more pertinent than ever. On the one hand, prices for some wines hit record highs this year, but on the other, the number of active buyers at these prices has dwindled.

The fine wine market in 2022 was a game of two halves. As we write sentiment is split. This Pushmi-Pullyu theme looks set to continue into 2023. But only one side can prevail.

The fine wine market in 2022

The good news for fine wine has been its stability in the face of increasingly severe headwinds. As a diminishing asset which encourages long-term storage, fine wine is an inherently low volatility investment. This gives it advantages over mainstream assets especially in turbulent economic times.

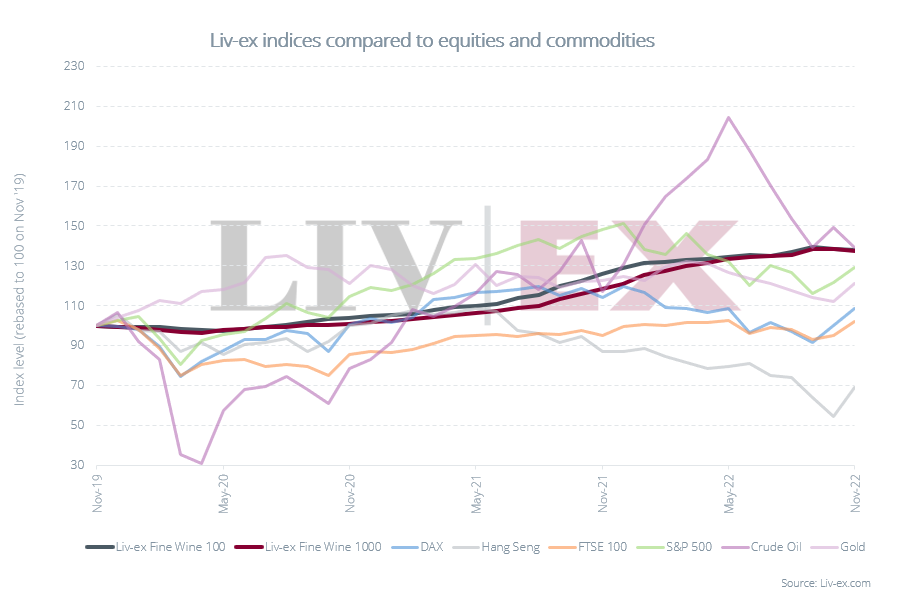

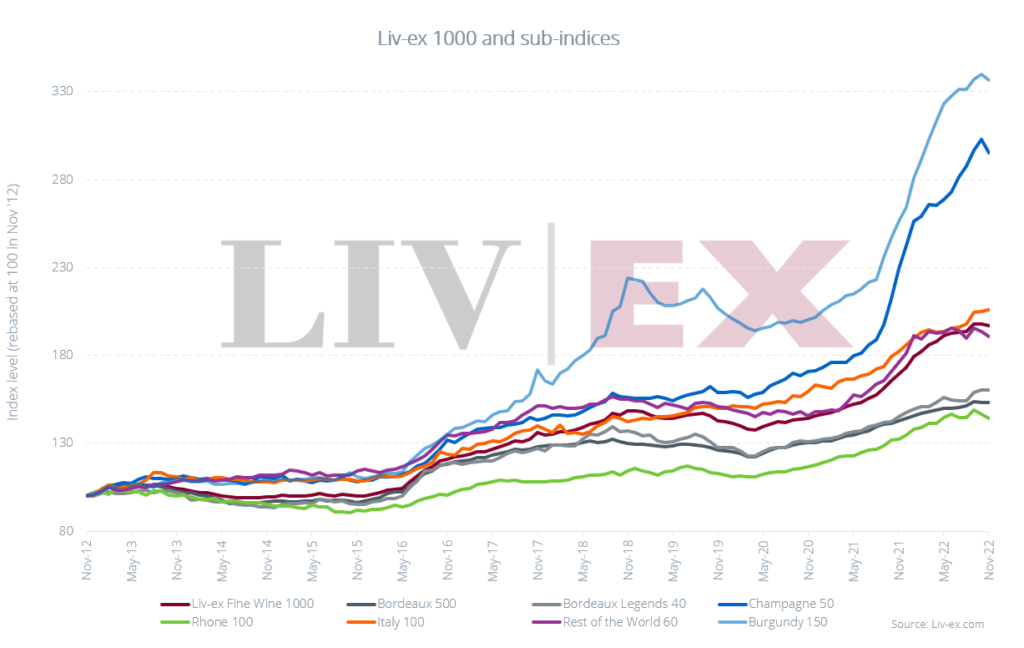

This has proved its worth this year. All the major indices have risen year-to-date. The Liv-ex Fine Wine 100 and Liv-ex Fine Wine 1000 hit new highs, the latter driven by its Burgundy 150 and Champagne 50 sub-indices.

Despite some minor setbacks of their own, the Liv-ex 100 and Liv-ex 1000 continued to outperform major equities and commodities this year, though oil remains just ahead over a three-year period.

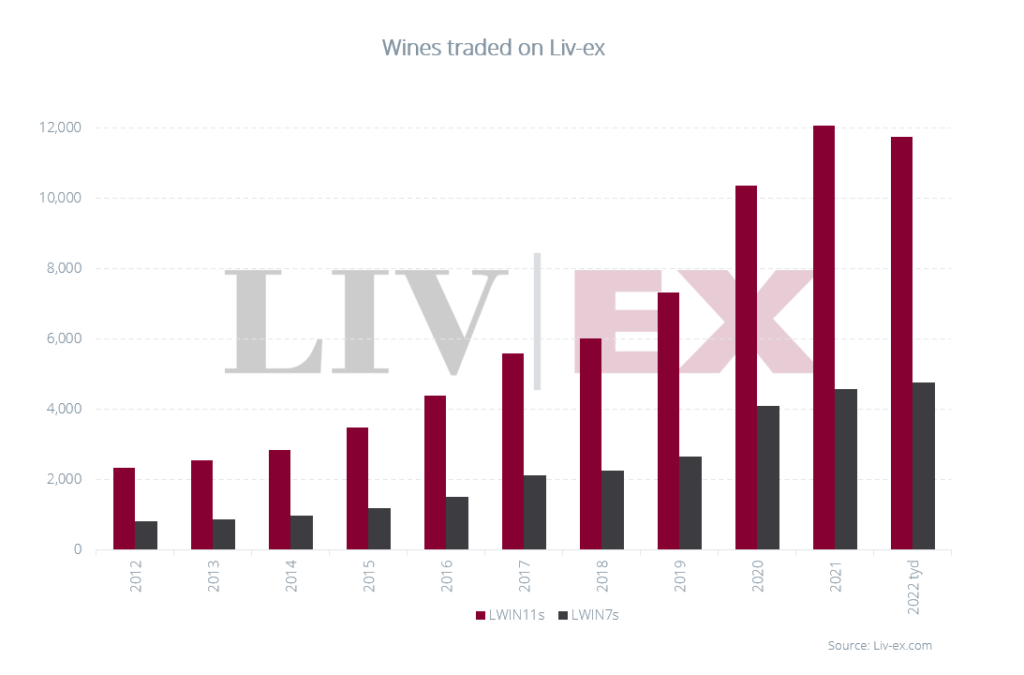

The number of wines traded (measured as LWIN7s) beat the 2021 record and fine wine continued to outperform equities and commodities; with many of the former falling into bear markets as the year progressed. Fine wine’s reputation as a mainstream alternative asset – both tangible and a hedge against inflation – was cemented. And with it came fresh investment and a period of renewed speculation.

However, signs of caution linger beneath the surface. Although the number of wines traded increased, it only rose by 2.4% when last year the rise was 10.4%. The number LWIN11s (wines identified by vintage) also failed to match that of 2021, with buyers narrowing their focus and buying with greater care.

Major regions see market shares decline

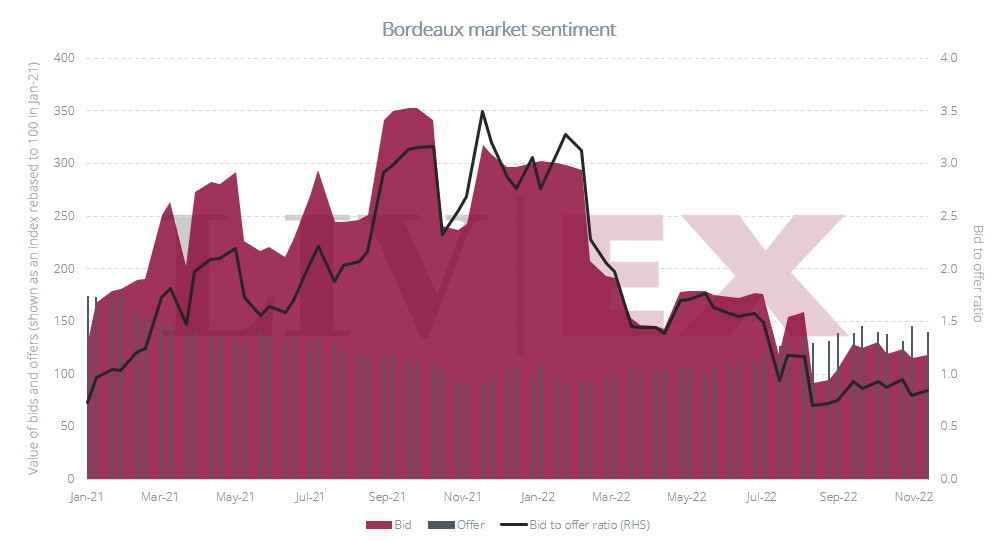

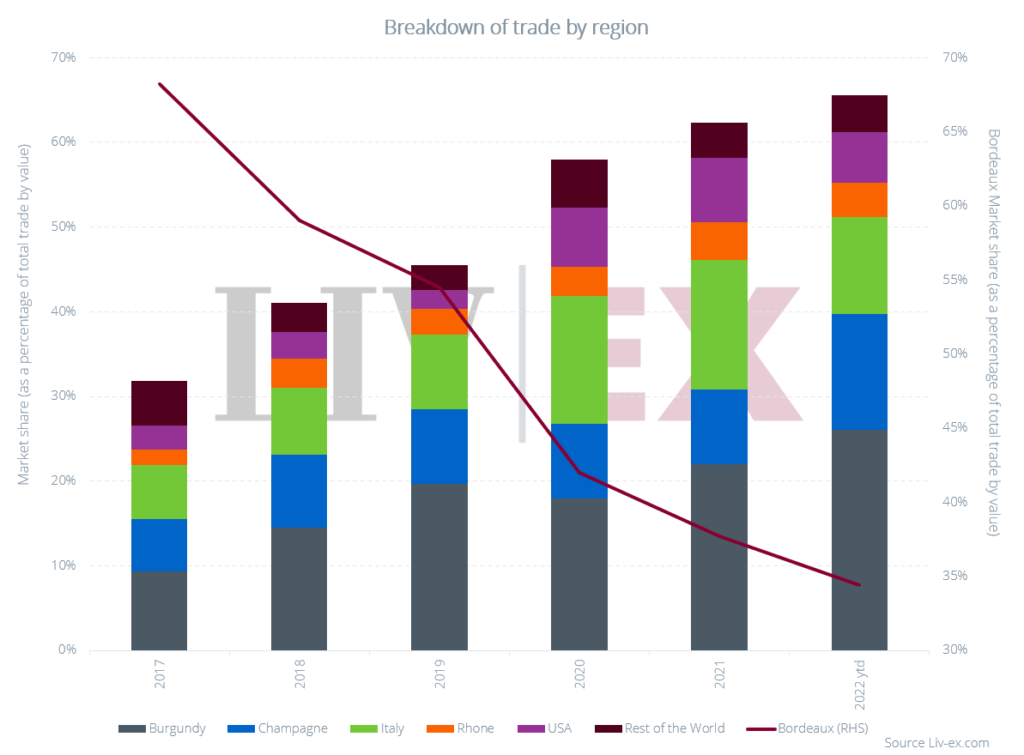

Continuing the trend of the past decade, Bordeaux’s market share fell to yet another low in 2022. The region accounted for 34.5% of total trade by value, down from 37.7% in 2021.

A poorly priced Bordeaux en primeur campaign against an indifferent vintage did little to encourage buyers and the autumn campaign then managed the same trick. Bordeaux’s bid to offer ratio fell below 0.7 for the first time in nearly two years. Although this is still in the positive territory (traditionally the threshold of positive market sentiment has been a ratio of 0.5), it is far off the high of 3.5 reached in late 2021.

In terms of trade, Bordeaux was not alone with its declining share this year. The market shares of Tuscany, Piedmont, California, and the Rhône also fell. Over the course of the year, it became apparent that the market share for California and the Italian regions was declining. This was a further consequence of collectors narrowing their focus, as highlighted by the decline in the number of LWIN11s (wine and vintage) trading.

Market share was squeezed by the market’s seemingly relentless focus on Burgundy and Champagne. Burgundy’s trade share rose from 22.0% to 26.2% and Champagne’s from 8.8% to 13.7% ̶ record highs for both and a trend that was examined in this year’s Power 100 report.

It should be noted that the market has expanded by both value and volume since 2020, so although Italy and California have lost market share to the likes of Burgundy and Champagne, the total value of trade from these regions remains above that of 2020.

As prices have soared in Burgundy and Champagne, other regions have begun to look interesting once again. Despite the poor en primeur campaigns and questionable strategy of stock retention, Bordeaux continues to offer exactly what the market needs – high quality wines, in good volumes and at (generally) accessible prices. Returns are not instant but the top Bordeaux estates have a good track record of rewarding long term investment, if not short term en primeur purchases.

Looking to other regions, the Rhône now offers the most affordable entry point into fine wine, with an extremely favourable quality to value ratio. And despite their lower market share this year, many Liv-ex members noted continued interest in Italian and US wines that they expected to continue.

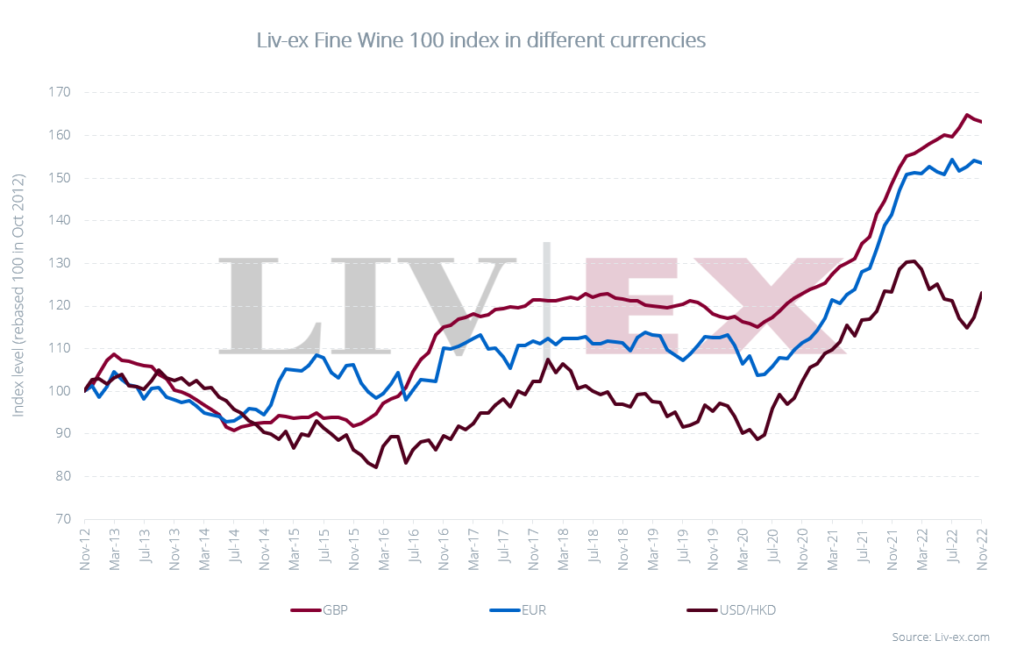

Dollar strength brings risk and reward

A major impact on the secondary market’s fortunes this year has been the strength of the US Dollar and Sterling weakness. The Dollar had chipped away at Sterling all year but the UK ‘mini budget’ on 27th September by the Liz Truss administration caused Sterling to plunge to an historic low and, ultimately, led to the government’s collapse.

In this moment there was a window in which dollar-based collectors could buy wines at a considerable discount. The impact of the volatile currency markets can be seen in the Liv-ex indices (which are measured in Sterling). In September both the Liv-ex 100 and the Liv-ex 1000 recorded their best month since January rising 1.9% and 2.1% respectively.

But currency shifts cut both ways. First and foremost, volatility and uncertainty increase risk aversion which creates negative sentiment. Second, it undermines the value of stock already held in the strengthening currency. Dollar buyers, while moving swiftly to take advantage of Sterling’s weakness at the end of September, soon became more cautious as they waited for exchange rates to settle.

Burgundy and Champagne lead market performance

As mentioned, fine wine prices continued to rise this year. All seven of the Liv-ex 1000’s sub-indices are up year-to-date, with the slowest growth coming from the Bordeaux 500 (6.1%).

The two mainstays of the Liv-ex 1000 this year have been the Burgundy 150 (27.4%) and Champagne 50 (21.6%). Although the Burgundy 150 outperformed the Champagne 50 over the course of the year, the latter index has performed better over the last one- and two-year stretches.

The broadening Burgundy market

Even though the number of wines (measured by LWIN11s) trading this year is down on last year’s total, Burgundy and Champagne were the two exceptions. The number of Champagnes traded rose 13.5% to 677, while the number of Burgundies rose 1.2% to 4,131.

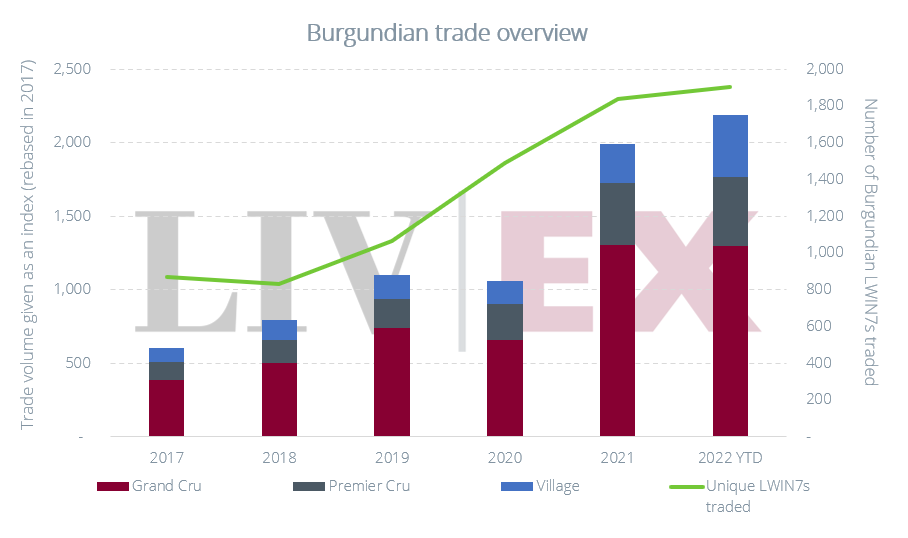

Of the two regions, Burgundy’s development has been the most dramatic. As recently as 2018, the number of individual Burgundian wines (measured as LWIN7s) trading was 829. A decade ago it was just 166. Even in 2020 it was 1,488. This year it has been 1,924. It is a seismic change.

And the types of wines changing hands is also striking. The chart below shows that while grand crus dominate Burgundy trade, there has been a considerable rise in the number of premier cru and even village wines trading. This has the result of buyers seeking value but also stock, as rising global demand has coincided with a series of short harvests in the region.

Another key evolution has been the renewed demand for white Burgundy. Once stigmatised due to fears of premature oxidation, white Burgundy has seen its trade value and volume rise steadily in recent years; and trade by value hit an all-time high in 2022.

Furthermore, white Burgundy prices are cheaper on average than their reds counterparts (with a few exceptions), but the price performance of the whites is stronger. Over the last three years the white Burgundy index has outperformed both the Burgundy 150 and the red Burgundy indices.

Questions around Champagne and Burgundy grow

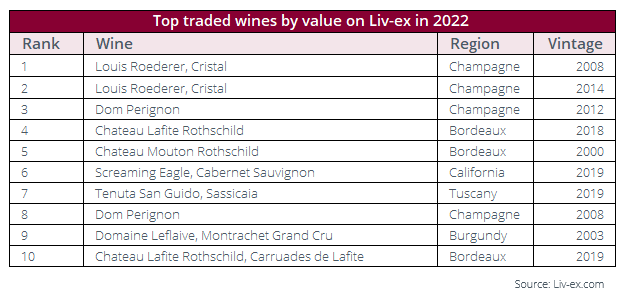

Of the two indices, Champagne had greater momentum as the year went on. For five consecutive months (June-October) the Champagne 50 was the best-performing sub-index of the Liv-ex 1000. The three top traded wines by value in 2022 have all been Champagnes (Louis Roederer Cristal 2008 and 2014 and Dom Pérignon 2012).

When looking at the 10 top traded wines by volume, the three mentioned above make the list, along with Taittinger Comtes de Champagne 2011 and Dom Pérignon 2008.

Burgundy’s performance was built on a strong first half. Price gains in late 2021 and early 2022 were impressive and as the Power 100 showed, some brands saw average price rises of several hundred percent.

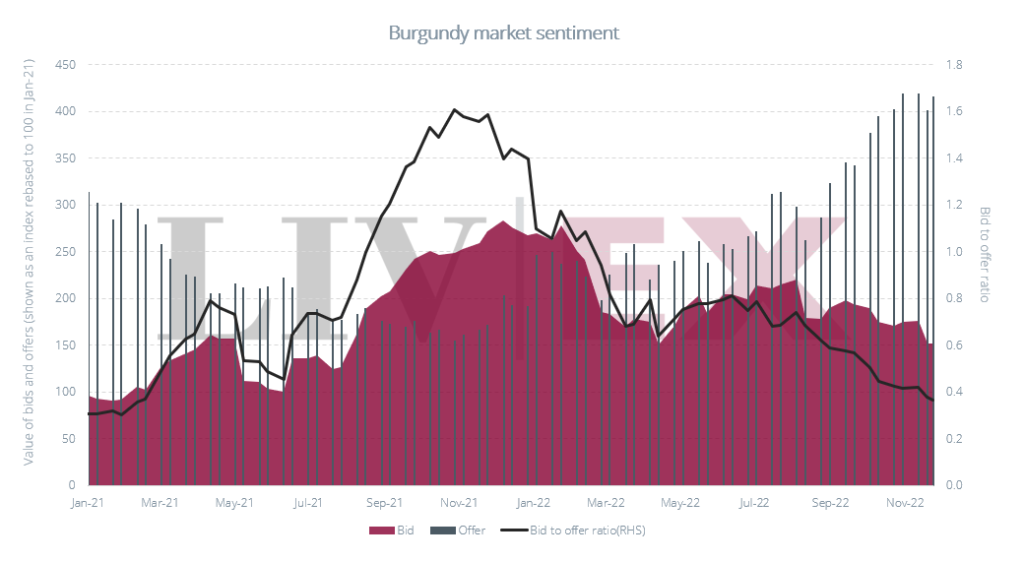

Yet, as Burgundy prices have soared, buoyed by a demand-supply imbalance, the air at the top has got thinner. Fewer collectors can either afford to, or dare to, commit new money. Sentiment for Burgundy is wavering (see the chart below) as more stock comes to the market and takes longer to sell.

Over the summer, the Burgundy 150 started to look increasingly sluggish, rising just 0.7% in October and declining 0.9% in November.

Its bid:offer ratio has also fallen to 0.3. By comparison, Bordeaux’s ratio is currently 0.7 and the market’s as a whole is 0.4.

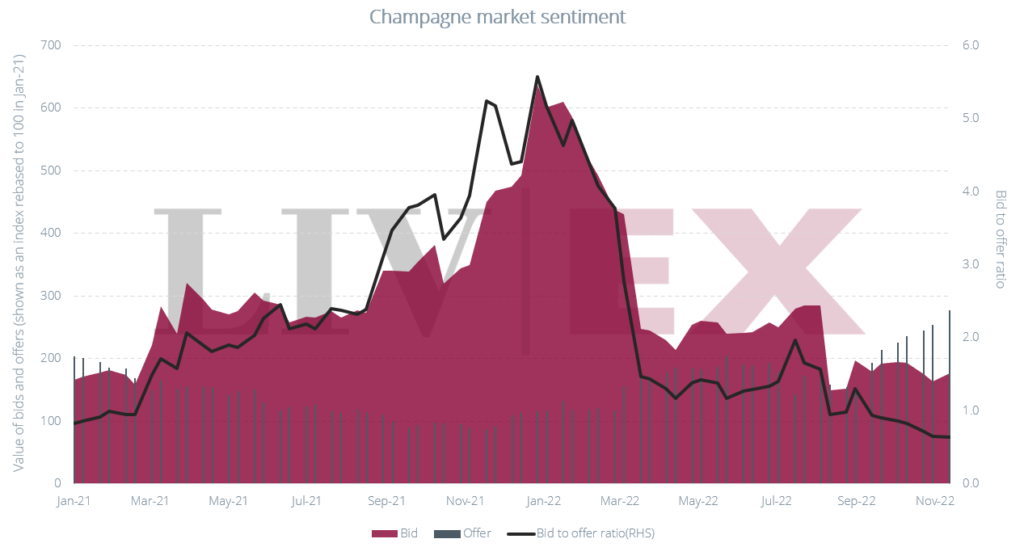

The Champagne 50 also saw a pullback in November when it fell 2.5% – its biggest decline this year erasing two months of gains.

Our recent report cautioned that the rapid gain in Champagne prices could soon lead to a cooling off period. Champagne’s bid:offer ratio was holding at 0.5 but dipped to 0.4 at the start of December. And while there are good vintages yet to be released by major houses – such as 2013s and 2014s – there have been warnings of stock shortages. The war in Ukraine has also caused severe disruption to glass supplies, especially for preferred formats such as magnums.

The changing collector

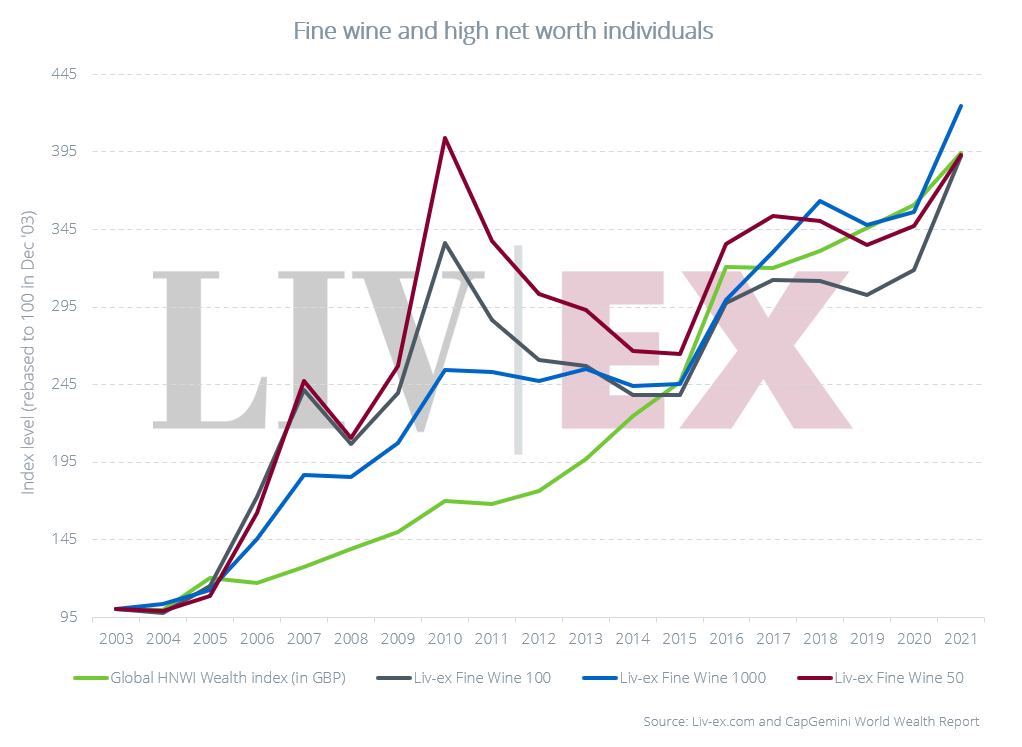

Demographically, the fine wine market is also changing. Younger drinkers and more women are increasingly exploring the category especially as the definition of what constitutes a ‘fine wine’ broadens, enabling more drinkers to be swept into its embrace. The rise of trading apps has also opened the door to a much wider base of investors, who are looking for alternative assets. The performance of the market in late 2020 and throughout 2021 bought a fresh influx of players– on a level not seen since the China-driven bull-run of 2010. The pandemic also saw enormous wealth creation and a significant increase in the number of high-net-worth individuals (HNWIs) who spent some of their new wealth on fine wine both as a genuine passion and as a viable investment.

Both Deloitte and CapGemini pointed to the rise of HNWIs during the pandemic as an important driver of growth for alternative assets such as art and fine wine. The rise in the number of HNWIs correlates neatly with the rise of the leading fine wine indices.

A long period of substantial wealth creation has led to a boom for alternative investments, fuelled by a widening array of new and exciting technologies that bring an assortment of tantalising promises and opportunities.

The market has seen fine wine linked to the world of non-fungible tokens (NFTs) and crypto currencies. In the US, Singapore and South Korea there has been a rise in wealth management services that offer tokenised fine wine portfolios or NFT wine clubs.

Producers such as Penfolds and Dom Pérignon have also offered special edition bottles as NFTs which can be paid for with cryptocurrency like Ethereum. Domaine Liger-Belair and Jacques Selosse are among several estates that joined the NFT platform Wokenwine earlier this year.

Market sentiment begins to fall

However, the cross-over between fine wine and new technologies should be approached with caution. The further crypto has risen, the more it has come under scrutiny and suspicion, exemplified most recently by the spectacular collapse of the crypto exchange FTX.

Recent articles by the Financial Times and The Economist, were unsparing in their appraisal of the crypto world. ‘A vehicle for pure speculation’ according to the FT’s interviewee, while FTX’s downfall moved The Economist to write that ‘never before has crypto looked so criminal, wasteful and useless’.

Wealth destruction replaces wealth creation

Much of the crypto world has thrived through lack of regulation and transparency. Looking at the crypto implosion, a reasonable concern might be that a similar fate could befall fine wine prices, especially at the very top end where the pricing metrics and buying pool remains highly opaque.

A passage in the Deloitte report on the art world serves just as well for the rising prices of certain Burgundies: ‘There are fears that the market speculation for younger artists could threaten its future sustainability… Some art market experts view the speculation among younger artists as unhealthy and unsustainable – with the fear of missing out (FOMO) among collectors and investors looking for the next big thing pushing prices far beyond justified limits, given the stage of these artists’ careers.’

Looking ahead, are there enough buyers and money to sustain current fine wine prices? As much as there was wealth creation in 2021, this year was marked by a great deal of wealth destruction, with billions wiped off equities and bonds. In a recent survey, Liv-ex members noted continued fears of global recession, rising logistics costs, foreign exchange volatility, loss of consumer confidence, price corrections and volumes of in-demand stock as the prime challenges for the trade in 2023. None of this is an atmosphere conducive to sustaining overstretched prices.

A note of caution in the Liv-ex indices

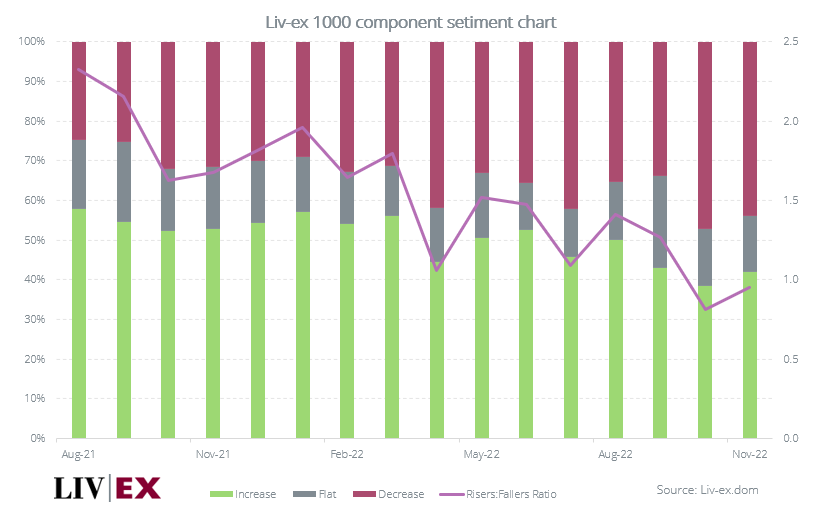

A closer look at the Liv-ex indices also provides a cautionary tale. Although the Liv-ex 1000 index has risen over the past year, the number of wines increasing in price on a monthly basis has steadily declined since August 2021.

In November 2022, 44.9% of its components fell in price, while just 42.8% increased. The remaining 12.3% ran flat.

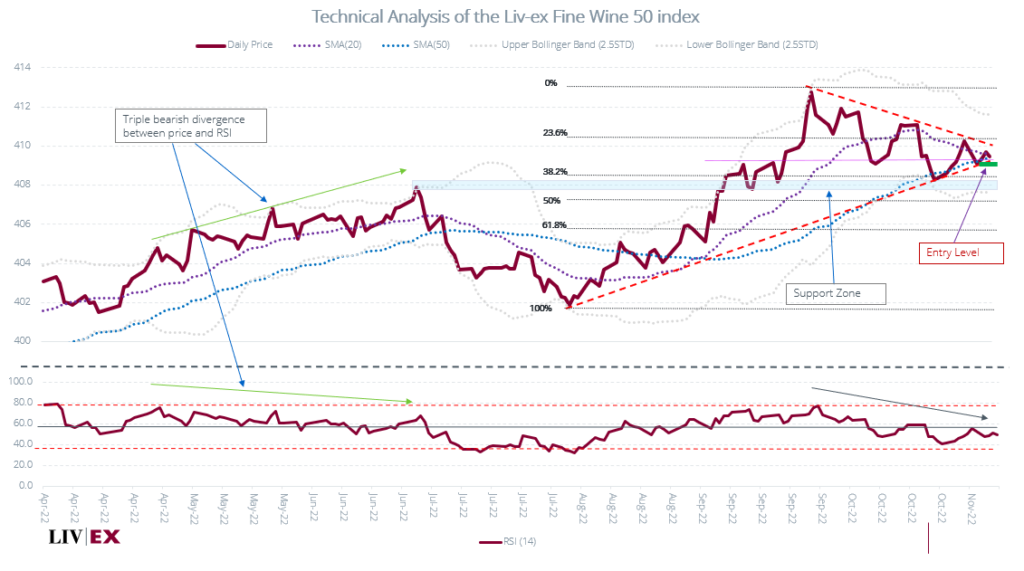

Technical Analysis of the daily Liv-ex Fine Wine 50 index raises a possible red flag. While the trend remains bullish, supported by the 50-day simple moving average, since 29th September a symmetrical triangle has formed signalling a battle between buyers and sellers and suggesting greater uncertainty now pervades the market. With the price action in the apex of the triangle, a break either up or down is imminent. If the market breaks lower, the first support will be at 407.

Conclusion

The outlook for 2023 is not the brightest. Despite a recent rally in equity and bond markets, they remain gripped by volatility. A debate rages among financial commentators and economists as to how far interest rates will need to rise to quell inflation. No-one knows. And so, volatility can be expected to remain with us.

But there remain many positives for the fine wine market. Fine wine continues to offer relative stability and acts as an inflationary hedge. Rising inflation, and with it, rising interest rates will reduce the appetite for risk but this is likely to affect a minority of labels (those most speculated in) rather than the market at large. Prices across all regions continued to rise in 2022 and, in most instances, these were steady gains. Boring perhaps but reliable.

This said, the headwinds faced by the market are severe. No market rises forever, and recent action suggests that some regions may have peaked for the time being. Buying has become more focused, and Liv-ex members spoke of customers ‘buying less but better’ and being more ‘measured’.

Upon closer look, there are also warning signs within the Liv-ex indices. Within the Liv-ex 1000, more wines fell in price than those that rose this month. Technical analysis of the Liv-ex 50 also suggests a break lower is possible.

The devil-may-care spending attitude seems to have passed. With demand starting to dry up, the small pool of buyers for the very rarest wines either have the wines they always wanted or expensive bottles they can no longer sell.

The red flags have been hoisted. But given fine wine’s track record during periods of inflation and uncertainty, long-term enthusiasts will find it easy to look on the bright side. Will they continue to throw caution to the wind? In the short term, all indications are for a period of drift. Happily, the fine wine market has never been about the short term.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.