The fine wine market in Q3 2022

Introduction

There was much to distract the market from the persistent narrative of economic gloom in the third quarter. But behind the solemnity of the state funeral of the late Queen Elizabeth II, Europe’s scorching summer heatwaves and Bordeaux’s autumn releases the dreaded drum of recession and downturn has continued to beat a steady rhythm.

The fine wine market experienced a hiccup in the 3Q. The Liv-ex Fine Wine 100 dipped in July – its first negative movement since June 2020 – but began to rise again in August and September as a result of the weak Pound.

The Liv-ex Fine Wine 1000 saw its progress slow to a crawl, effectively running flat in July and August before rebounding in September.

An unnerving three months but ones that reflected the increasingly severe headwinds that have been worrying the market since the latter half of Q1.

The bid to offer ratio – an indicator of market sentiment – fell further during the quarter. It started the year at 1.0, had declined to 0.8 at the end of Q2 but by the end of September was 0.56.

Historically, anything above 0.5 has been seen as a positive sign but it is clear that caution has well and truly replaced the exuberance and devil-may-care spending spree of 2021.

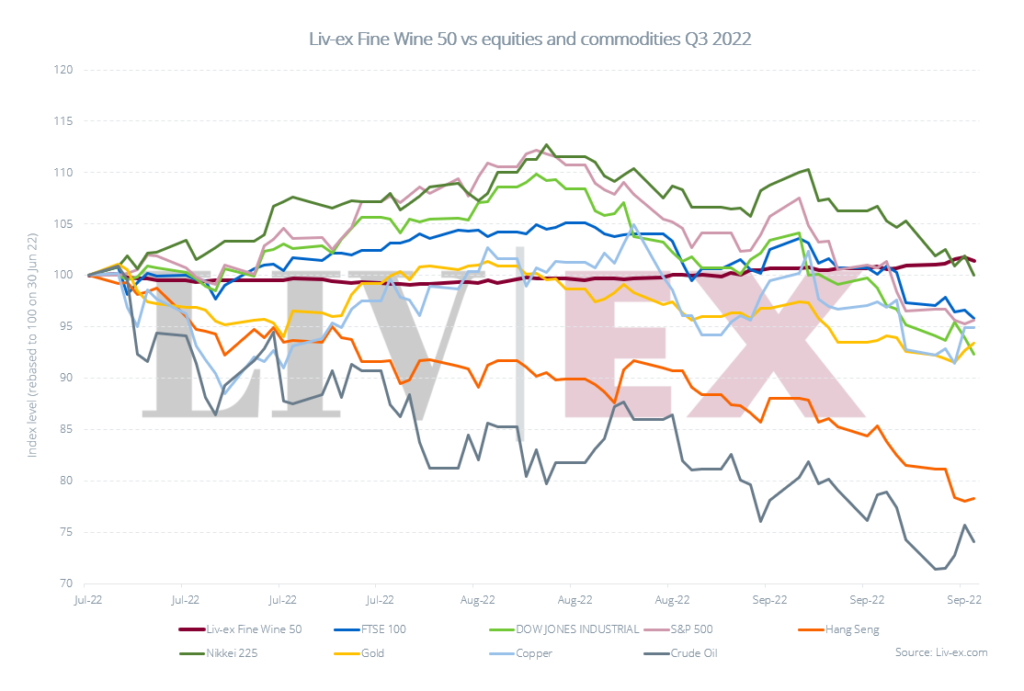

Fine wine stays the course as equities flounder

Global equities rallied in July and August but ended September firmly in bear market territory, with rising energy prices, further interest rate hikes from central banks and geopolitical uncertainty playing on market fears.

The Hang Seng in particular struggled. First as a result of China’s zero Covid policy hampering economic activity. Then the descent toward recession, hastened by the collapse of the domestic housing market. The Yuan too struggled against the surging US Dollar.

Quarter-on-quarter the Liv-ex Fine Wine 50 only rose 1.3% but even this modest performance was enough to see it out-perform global equities and commodities.

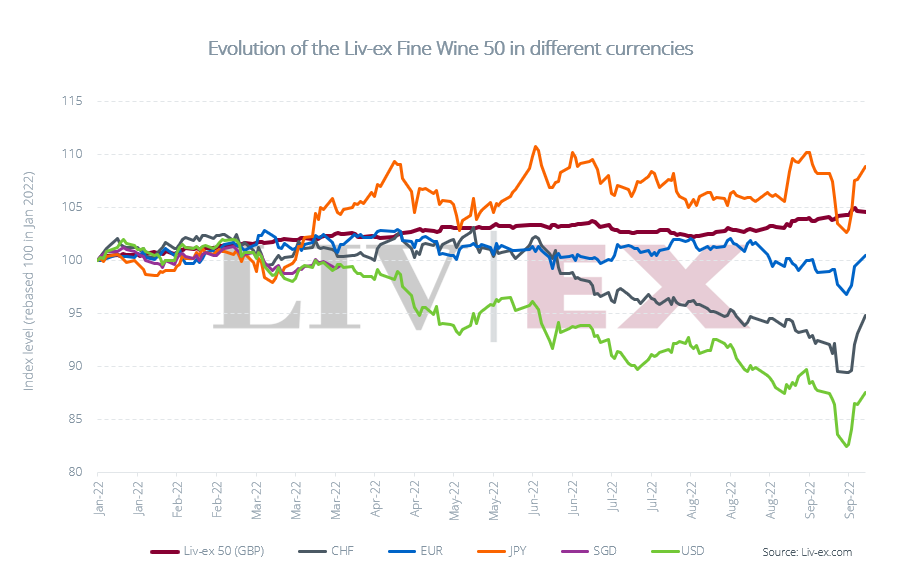

September exacerbates Sterling’s woes

The dominant theme of the last quarter was the collapse of Sterling. While down only 1.8% against the Euro at the end of the quarter, a week earlier it had fallen 7%. Against the Dollar it closed the quarter 8% weaker. Over the course of the year, the Dollar has chipped away at Sterling. But the announcement of the UK ‘mini budget’ on 27th September saw Sterling swoon.

The effect of Sterling’s decline is clearly visible in the chart below. Although Sterling has since recovered its composure, there was a brief window when collectors in most major currencies were able to purchase fine wines at a considerable discount to their local market.

Sterling weakness benefits the secondary market as it boosts the buying power of the Dollar (and Dollar-linked currencies), Swiss Franc, Euro and Yen buyers – if their timing is right.

The flipside is that a weak or volatile Sterling can be bad news for stockholders whose stocks are valued in those other currencies. In short, currency shifts and precise timing can yield rewards but there is risk. Ultimately, buyers and sellers prefer stability and without it, risk aversion rises.

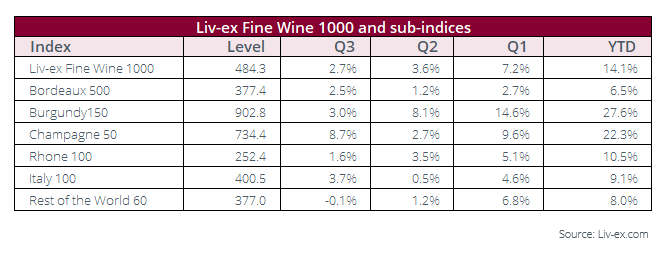

Liv-ex 1000 sub-indices rise and fall

The Liv-ex 1000 saw smaller gains in Q3, but the underlying picture was mixed. The Burgundy 150 continued to slow, rising just 3% this quarter. The Champagne 50 and Italy 100 however, were more robust. The former rose 8.7% between July and September, while the latter overcame a poor Q2 with a sturdier 3.7% gain.

Bordeaux was a little stronger this quarter than in the previous, its performance driven by steady demand for high quality vintages and the security offered in older, ‘classic’ vintages.

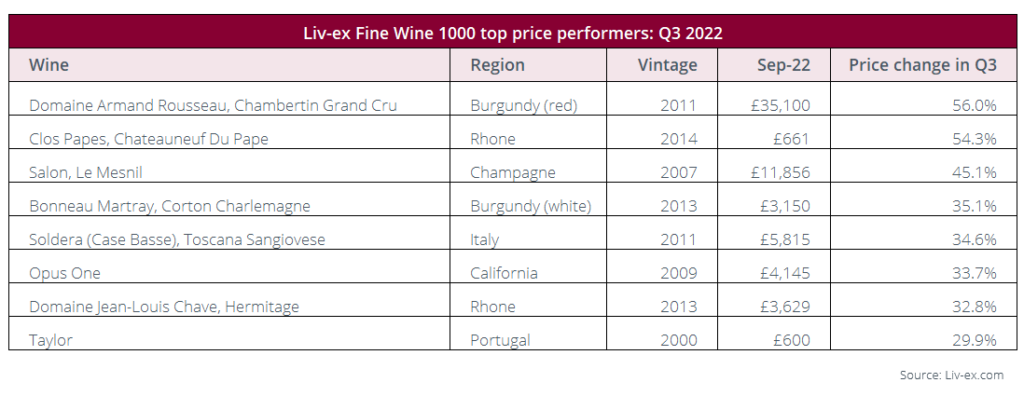

Top price performers

Just as in Q2, the best performers from July to September were diverse with increasingly fewer Burgundies.

Domaine Armand Rousseau’s Chambertin 2011 topped the group, its 2014 and 2010 vintages saw strong gains last quarter.

The same is true of Port such as Taylor’s 2000 vintage. Taylor’s is a strong brand, the wine has 98-points from influential critics such as Neal Martin and Robert Parker and it is a wine style that is famously long-lived. A small investment relative to the price of other great wines of the world.

Trading overview in Q3

Bordeaux managed to increase its share of overall trade from 32.8% in Q2 to 35.9% in Q3. The region has been enjoying steady demand for its best vintages over these last few months.

Otherwise, trade levels remained steady quarter to quarter, with just Piedmont and the Rhône changing places once, though on the thinnest of margins; neither region commanding more than 3% of overall trade between July to September.

California remained down in fifth place, its share of trade has been declining on a monthly basis throughout the year, as indeed has Italy’s where demand has been narrowing on a few established brands such as Sassicaia and Tignanello.

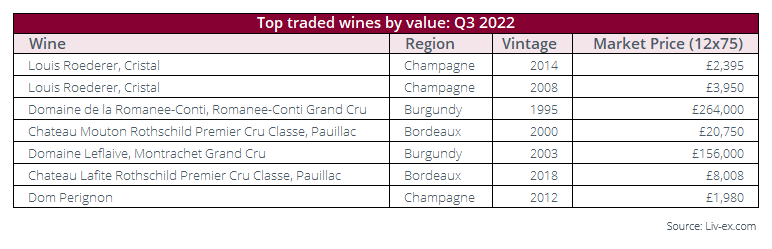

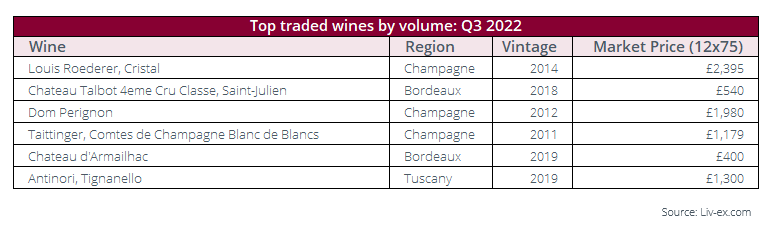

Top traded wines in Q3

Given the Champagne 50’s strong performance this quarter, it is unsurprising that several should be among the top-traded. Louis Roederer’s Cristal, especially the 2008 and 2014 vintages continue to blaze a path through the secondary market. Both wines have been in these tables every quarter this year, as has Dom Pérignon 2012.

The focus of on-going market demand is clear as several of the wines below have repeatedly featured throughout the year. In Bordeaux, the repeated demand for top vintages is highlighted by demand for wines from 2019, 2018 or even 2000. Meanwhile, activity for Tignanello 2019 is a nod to the increased focus of Italian trade.

The prices shown in the table above are Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. It is always presented for a 12×75 case unless otherwise stated. To calculate the Market Price, we look at list prices from a large group of trusted international merchants. Preference is given to prices from stockholders over brokers, to cases over single bottles, and to recent prices over older prices. The algorithm behind it runs every day, evaluating a pool of over 1 billion data points to determine the most accurate Market Prices for 240,000+ wines.

Conclusion

Winter and recession are coming. Headwinds are increasing to gale force. After a summer respite, stock markets are once again on a downward trend. Wealth destruction this year has been immense. The Economist recently reported that an estimated US$12 trillion has been wiped off US stocks alone, with a further $7trn wiped off bonds. For the fine wine market, the pattern seems to be consolidation. Italian trade is weaker this year than it was in 2020 or 2021 in both absolute value and in market share; while Californian market share is also lower than it was in those years. The Burgundy 150’s rise has slowed considerably.

Bordeaux and Champagne, however, have remained robust – the reason being perhaps, that they are the two regions that offer what the market wants right now: brand security, a track record, relative value and, crucially, liquidity.

The question now is what the fine wine market can continue to offer buyers (new and old) not just in the 4Q but next year as well. What will drive the market on? Exciting vintages on the horizon might be one answer.

For Champagne there are very few 2012s yet to be released and the 2013s and 2014s are highly regarded. The 2021 vintage in Burgundy being released next year is tiny but will doubtless, be in demand, while in Napa Valley there will be gaps in the 2020 vintage releases due to smoke taint. As for Bordeaux, the market will be looking to the 2022 vintage for hope.

The fine wine market has, by and large, remained a beacon of stability in these stormy times. It is a relatively small ‘alternative’ investment for most and a passion for many. But it is also a luxury that can be done without. The question may not be what will drive the market higher, but what might knock it lower? Rising costs for growers, négociants, merchants, retailers and collectors will undoubtedly be felt. The effects of the global downturn suggest leaner times ahead.

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 600 of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable. Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.