Champagne: The growing secondary market for luxury

Introduction

Ten years ago, Champagne accounted for 2% of the total secondary market trade. Prices rose steadily almost every year, and, as explored in our first report on the region in 2018, ‘A market without bubbles’, Champagne occupied its own niche in the fine wine market without the level of attention that saw Burgundy prices spike.

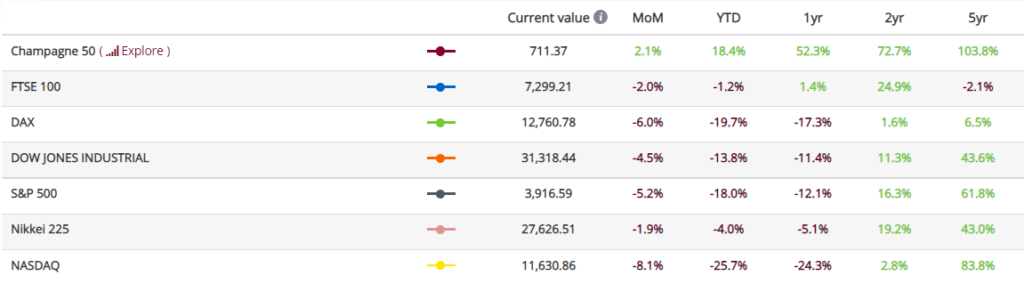

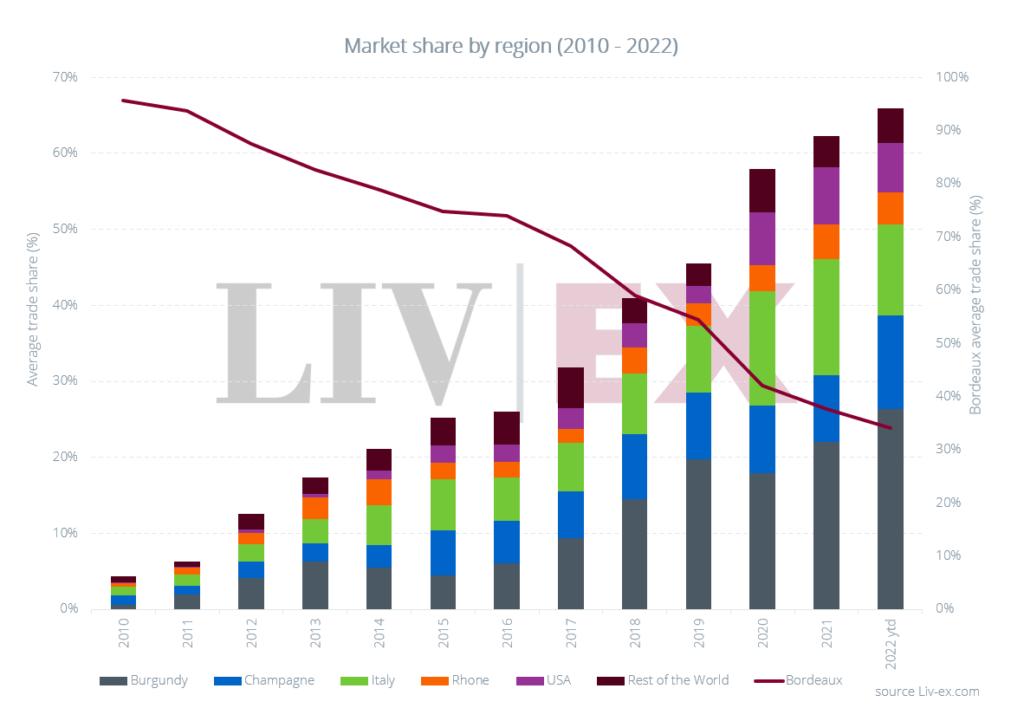

Since then, the market has changed. Champagne’s trade share has climbed to new highs – 12.4% so far in 2022 – making it the third most traded fine wine region after Bordeaux and Burgundy. Once a relatively modest price performer, Champagne has become the best performer over the past one (52.3%) and two years (72.7%). In that time, it has outperformed other assets such as Gold, and major equities such as the FTSE 100 (24.9%) and the S&P 500 (16.3%). Prices for some Champagnes have risen over 140%, such as the 2006 and 2007 vintages of Salon Le Mesnil-sur-Oger Grand Cru.

All of this has happened during a period of great uncertainty, from the Covid-19 pandemic, through war in Ukraine, rising inflation and now, looming recession. In fact, ‘luxury goods’ performed particularly well during this time, as the sector was able to raise prices without killing demand. For example, luxury group Louis Vuitton Moët Hennessy (LVMH), which owns Champagne houses Moët & Chandon, Dom Pérignon, Veuve Clicquot, Krug, Ruinart and Mercier, reported a 28% growth in revenue in the first half of the year.

During this time market confidence in Champagne has only grown. The average trade price of a 9-litre case rose 76.7%, from £1,885 in 2019 to £3,331 in 2022.

Back in July, Champagne also had the highest bid:offer ratio of all regions, standing at 1.6 – a sign of strong demand. Vintage quality, an enviable global distribution network and international brand recognition have all played a part.

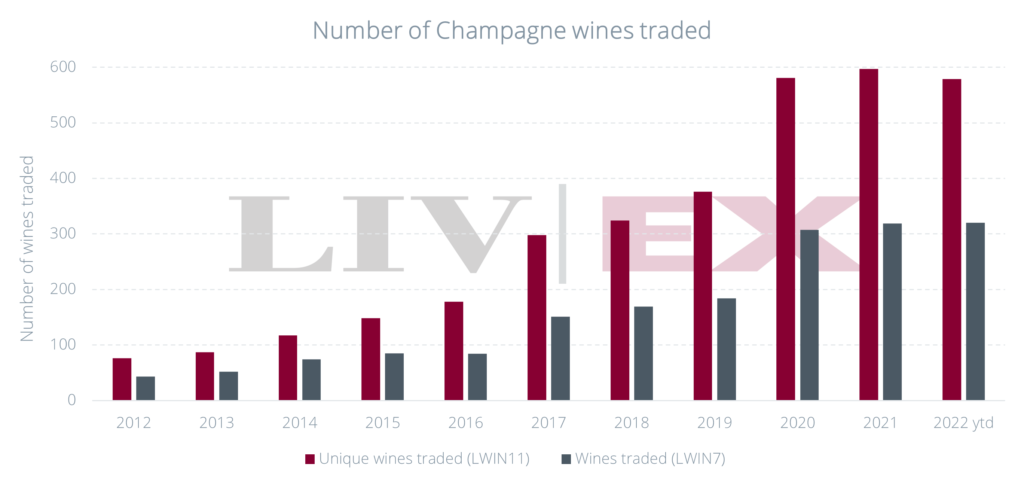

Buyers have also become more adventurous. Year-to-date, 579 different Champagnes have traded on the market, a sevenfold increase in the past decade. Furthermore, a growing category has been large format Champagne, which has been a source of even greater fascination for luxury buyers, due to its inherent rarity and exclusivity. Secondary market trade of big bottles has risen from a pre-pandemic level of 5.9% of total Champagne trade to 18.0% year-to-date.

Yet the relentless tally of Champagne’s secondary market progression also hides the more fundamental change taking place. Five years ago, when we last looked at Champagne, a steady but successful future seemed assured. However, world events have intervened and, driven by the bull market of the pandemic years, Champagne has found itself fast-tracked into the big leagues of investment-worthy wines.

Speculators are active. As prices have risen, warehouses have filled, and the value Champagne offers relative to other fine wines has narrowed. The old rules around Champagne’s market dynamics no longer apply – or certainly not as rigidly as they once did. Although the secondary market for Champagne remains robust, a whiff of caution is in the air as new records are broken.

“A series of strong vintages and market leading returns has put Champagne in sharp focus in recent years, drawing interest from an ever-growing audience of buyers – both drinkers and investors. But as prices rise and the core dynamics driving the market continue to evolve there are signs that returns may soon begin to slow.”

Justin Gibbs, Liv-ex Deputy Chairman and Exchange Director

The price performance of luxury Champagne

Champagne outperforms mainstream equities

The Champagne 50 index tracks the price performance of the most recent physical vintages of the 12 most actively traded champagnes: Krug, Philipponnat Clos des Goisses, Perrier Jouët Belle Epoque, Louis Roederer Cristal (blanc and rosé), Bollinger La Grande Année, Salon, Pol Roger Cuvée Sir Winston Churchill, Taittinger Comtes de Champagne (blanc and rosé) and Dom Pérignon (blanc and rosé).

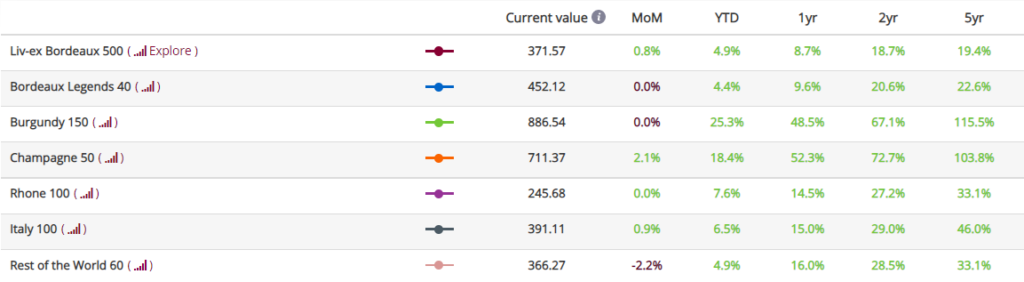

Its run over the last two years has been impressive, rising 72.7%, and outperforming major equities and the leading fine wine indices.

The Champagne 50 has risen twice as much as the industry benchmark, the Liv-ex Fine Wine 100 (36.1%), and its parent index, the Liv-ex Fine Wine 1000 (36.2%) – the broadest measure of the market.

It has also considerably outperformed the Bordeaux First Growths, as represented by the Liv-ex 50, which have risen 20.7% over the past two years.

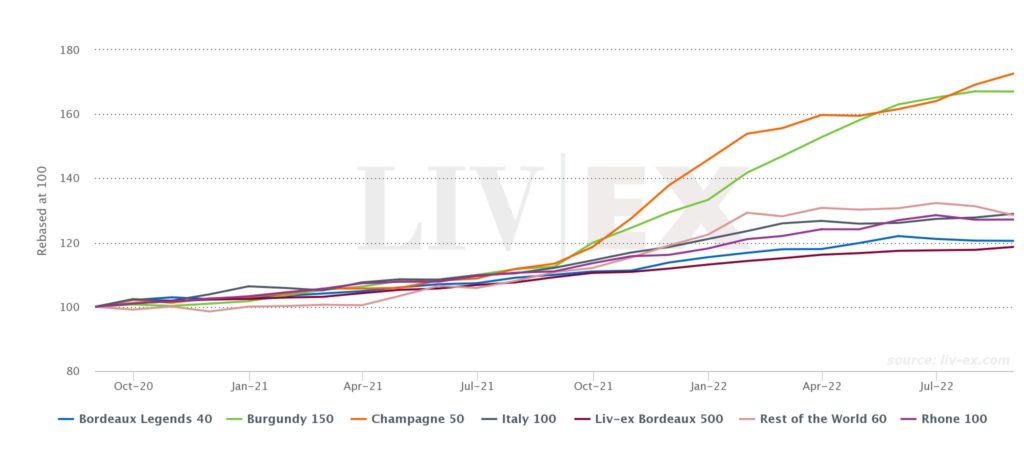

Champagne 50 vs major Liv-ex indices

Made with the Liv-ex Charting tool.

Champagne is also the top performing fine wine region over the past one and two years, even outperforming Burgundy which leads the market over the long-term (5+ years).

Champagne 50 vs other regional indices

The best performing Champagne labels

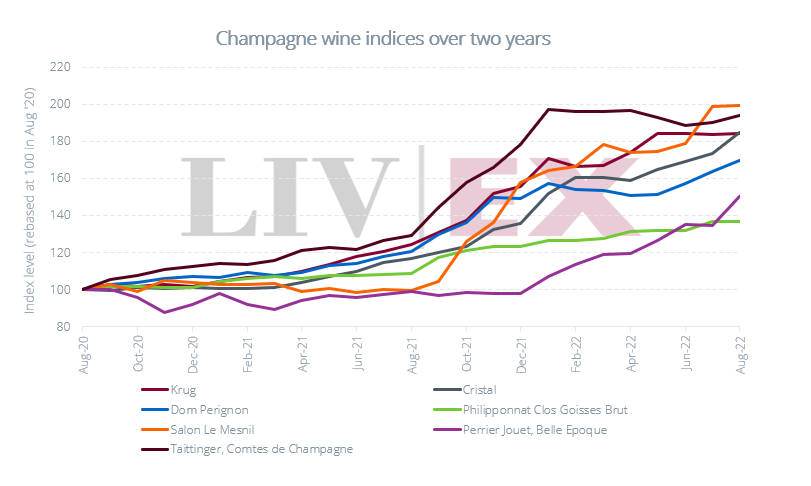

The Champagne at the forefront of the market’s two-year bull-run has been Salon Le Mesnil, which has risen 99.5% on average during this time. Founded by Eugène Aimé Salon in the early 20th century and part of the Laurent-Perrier group since 1989, Salon is defined by its singularity: coming from a single terroir – the Côte des Blancs; a single cru – Le Mesnil-sur-Oger; and a single grape variety – Chardonnay. Salon has been the third most traded Champagne by value in the last year.

The second-best performer has been Taittinger Comtes de Champagne, up 94.3%. The third spot has been taken by Louis Roederer Cristal, up 84.6%, which has also been the top traded Champagne label this year. Meanwhile, Krug has risen 84.1%, Dom Pérignon 69.7%, Perrier Jouët Belle Epoque 50.6%, and Philipponnat Clos des Goisses 36.7%. The latter is the first Champagne to have been offered via La Place de Bordeaux.

The biggest risers from the Champagne 50 index

The top-performing Champagnes on individual wine and vintage level (LWIN11) over the past two years can be seen in the table below.

The 2006 and 2007 vintages of Salon Le Mesnil-sur-Oger Grand Cru have risen 142.0% and 140.5% respectively, while the 2004 is up 113.7%.

Notably, only one rosé Champagne features among the top 10 – Louis Roederer Cristal Rosé 2008, which is up 88.8% over the past two years. However, the wine has 100-points from The Wine Advocate’s William Kelley, who said that ‘impeccably balanced and harmonious, this superb wine represents one of the qualitative peaks of this great vintage’. It commands a current Market Price of £8,400 per 12×75 case.

*Liv-ex members can see more on the Indices Explorer tool. Data correct as of September 2022.

Join Liv-ex for access to exclusive, member only insights and analysis

Join 600+ trusted merchant members and see over £80m of live opportunities across 20,000 markets. Get everything you need to do better business

Market demand

Champagne becomes the third most traded region in 2022

Heightened demand for Champagne has seen it become the third most traded fine wine region so far in 2022. Its annual trade share currently stands at 12.4%, surpassed only by Bordeaux (34.1%) and Burgundy (26.3%) but ahead of Italy (11.9%), which placed third in 2020 and 2021.

Year-to-date, the main markets for Champagne have been the UK (40.3%) and Europe (30.0%). US demand, which accounted for 39.1% of the total trade in 2021, has fallen back to 22.1% year-to-date. The US has long been an important driver of Champagne trade, but its high trade share in 2021 can also be explained by the fact that the region was exempt from the high import tariffs on European wines introduced by President Donald Trump in 2020. When those tariffs were removed by the Biden administration in mid-2021, US buyers were able to turn their attention to other regions like Bordeaux and Burgundy.

Last there is the Asian market, taking 7.4% of the total trade. China’s zero Covid policy continues to impact both it and Hong Kong. That said, aside from Japan, Asia has not traditionally been a big market for Champagne, showing a marked preference for red wines instead. Last year, 81.1% of trades by Asian merchants were for red wines and just 7.3% for Champagne.

Broadening choice

Buyers have benefitted from an ever-widening pool of Champagnes on the secondary market. Among them is a greater selection of ‘grower’ Champagnes; small estates where the brand identity is centered around the vigneron themselves. Leading this group are the likes of Jacques Selosse, Egly-Ouriet and Ulysse Collin.

Year-to-date, 579 different wines (LWIN11s) have traded on Liv-ex, compared to 597 for the whole of 2021. It looks as though the number will surpass the previous record by the end of Q3. The number of wine labels trading (LWIN7s) has already surpassed 2021, with 320 trading so far this year compared to 319 last year. However, the number of new wines being traded is not growing as rapidly as it once did, which suggests that – at least for now – the Champagne market’s broadening is approaching a peak.

The most traded Champagnes this year

The price brackets of Champagnes traded have been relatively wide, with the lowest costing just £174 per 12×75 (J. de Telmont Grand Reserve Brut NV) and the highest at £48,600 per 12×75 (Dom Pérignon P3 1990).

The most traded Champagnes this year have come from the top houses Louis Roederer, Dom Pérignon, Salon and Taittinger.

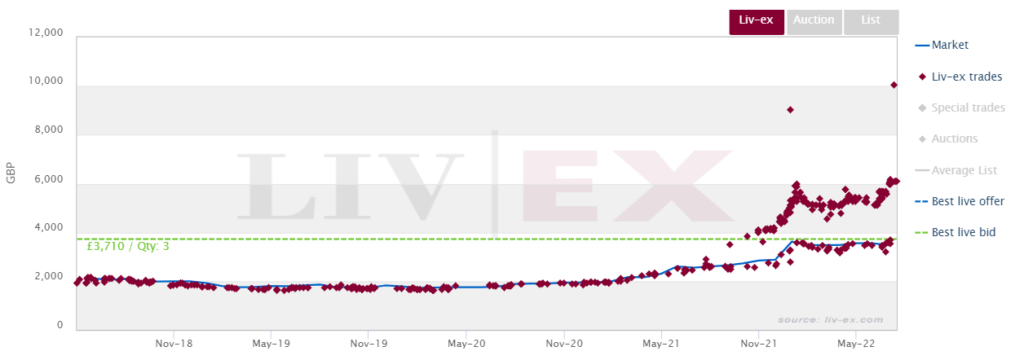

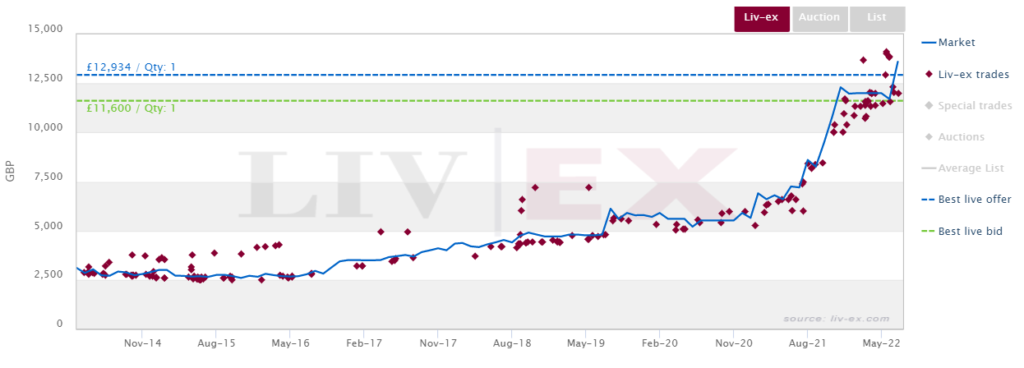

The most traded Champagne, indeed the most traded fine wine this year, has been Louis Roederer Cristal 2008. As the chart below shows, the wine has seen consistent demand for both larger bottles (which trade at a premium) and standard bottles. The wine has a 100-point score from James Suckling and 99-points from Antonio Galloni (Vinous).

Louis Roederer Cristal 2008 trades on Liv-ex

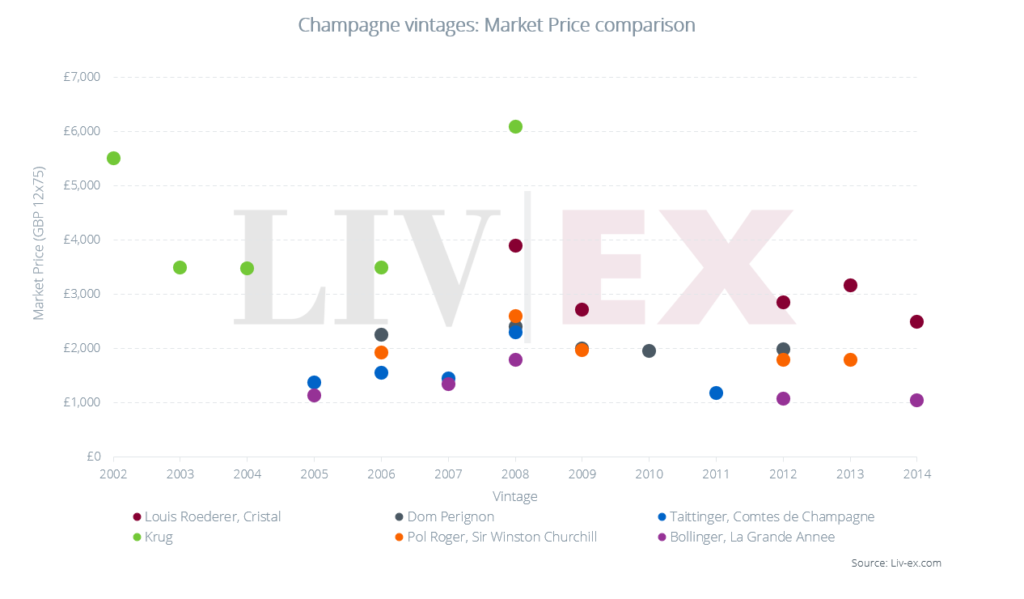

The 2008 premium and increasing vintage output

The 2008 Champagnes stand out for the premium they command versus other vintages.

The chart above shows the five most recently released vintages from six leading brands. In all cases the 2008 is the most expensive vintage available, with premiums ranging from 6.5% (Dom Pérignon) to 47.4% (Comtes de Champagne) above the next most expensive wine.

Interestingly, the 2008 vintage is the only vintage (so far) that has been produced and released by all six labels. The 2012 would appear to be the next vintage in line, with Comtes due to release its 2012 later this year and Krug at a later date.

It is also worth touching on another element of Champagne’s shifting market dynamics, which is the concept of ‘on’ and ‘off’ vintages.

Although Champagne houses historically do not make vintages in poor years, which should somewhat negate the concept of an ‘on’ or ‘off’ vintage, as more buyers and investors have come to the Champagne market they have bee-lined for what they consider the ‘best’.

This naturally concentrates attention on widely declared, critically acclaimed vintages, leading to greater demand and rising prices. It can also leave other vintages produced with less fanfare struggling to make gains.

Amid the wider narrative of rising prices, one positive element highlighted in this chart is the value still offered by newer vintages, which in turn continues to create opportunities for savvy buyers. And it is not an impediment to trade. Historically, some of the top-performing First Growths are ‘off’ vintages because they offer an affordable point of entry into the brand.

On the other hand, with some vintages rising in value faster than others, this may also create a situation where not every release looks compelling compared to back vintages. This can lead to a faltering start for new vintages hitting the market, which in turn impacts their price performance. And, as we’ve seen with Bordeaux, if returns on Champagne falter then investors may turn their attention elsewhere.

Salon 2002 leads return on investment

However, for now, that does not seem to be the case. From the top 10 traded Champagnes (shown in the table above), Salon Le Mesnil-sur-Oger Grand Cru 2002 has been the wine with the highest returns on investment since release. With an increase of 392.9% over the past seven years, it now commands a Market Price of £13,061 per 12×75 case, making it the most expensive of the top traded Champagnes this year. Only 5,000 cases were released, and the wine has garnered much praise from critics, including a score of 19.5/20 from Jancis Robinson.

Salon Le Mesnil-sur-Oger Grand Cru 2002 trades on Liv-ex

Join Liv-ex

Buy and sell with speed and confidence from and to the largest pool of trusted merchants worldwide.

The market for large format bottles

Large size Champagne bottles have enjoyed heightened demand in recent months. Produced in smaller quantities and often bought for the grandest occasions, large format Champagne is the ultimate example of a ‘luxury good’ in the fine wine market.

As mentioned in the introduction of this report, luxury goods have been one sector that has performed particularly well this year and big bottles have been part of this trend.

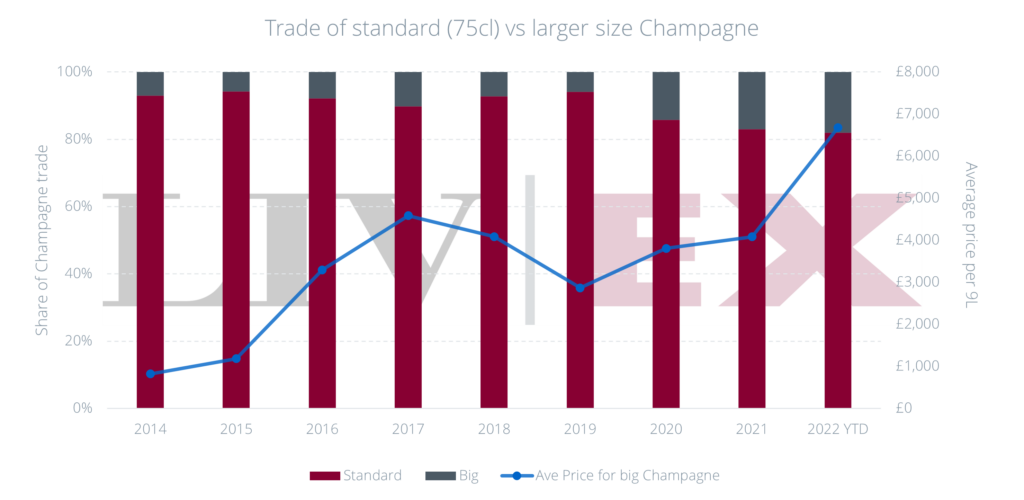

The average price of a large format Champagne has risen 63.6% year-to-date (by comparison the Champagne 50 index is up 18.4% over this period). Their share of Champagne trade has also risen, from a pre-pandemic level of 5.9% in 2019 to 18% so far this year.

After standard bottles, magnums are the second-most traded Champagne format accounting for 13.5% of the total trade. Methuselahs come third at 3.7% of the market, followed by jeroboams at 0.8%.

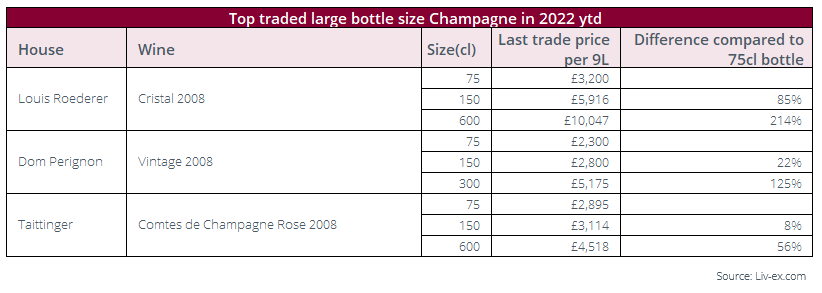

The largest bottles also carry the biggest premium. The average price of a 12-bottle case is £2,982 for standard bottles and £9,963 for a methuselah, a premium of 234.1%.

The top traded large format Champagnes this year have been, magnums and methuselahs of Louis Roederer Cristal 2008 and Taittinger Comtes de Champagne Blanc de Blancs 2006, and magnums and jeroboams of Dom Pérignon 2008.

The future of the Champagne market

Faced with Champagne’s current success, it is easy to forget that the region is still in a relatively early stage of its secondary market development.

Market demand generally congregates around established names that have global reach and resonance and then, as the market matures so it expands outwards to incorporate lesser-known names and other styles. This is precisely what has been occurring with Champagne.

On the other hand, there is a clear shift in the market dynamics of Champagne at present. In our last Champagne report, we noted that everything about Champagne worked in its favour.

Stock was plentiful, distribution was strong, the wines were drunk, keeping supply and demand in balance and they consistently offered relative value to other fine wines. As this report has shown, there has been a radical change in Champagne’s secondary market, which is positive on the surface but, on further analysis, raises questions about its future direction.

There can be little doubt that speculators have cashed in on Champagne’s many strengths; boosted by a run of excellent vintages over the last decade that has driven demand.

This has led to a change in the rules that used to apply to the Champagne market. Speculators rarely drink their stock, meaning that the volumes released with each new vintage no longer diminish at their usual rate. This raises questions about the sustainability of rising prices in the face of a potential stock overhang.

Relative value compared to other regions

Simultaneously, the rising value of Champagne means it no longer has the relative price advantage it used to hold against its fine wine counterparts.

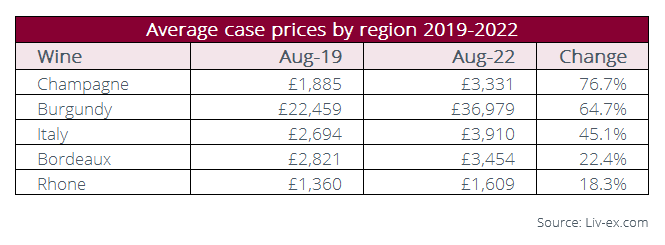

As the table below shows, Champagne has seen the greatest price rise of all the leading European fine wine regions since 2019.

Where once it offered one of the most affordable routes into fine wine, it now costs almost as much as Bordeaux on average.

The calling card of grande marque Champagne used to be that you could have a fine wine with all the pedigree of a Bordeaux First Growth but for a fraction of the price. That is no longer the case.

*The prices here are based on the average 12×75 case of wine from each region’s respective sub-index in the Liv-ex Fine Wine 1000.

The role of producers

Not only is the value of Champagne rising on the secondary market, there appears to be an ambition to increase prices coming from the producers too. There is a growing group of brands that have chosen representation through La Place de Bordeaux. Philipponnat’s Clos des Goisses is the most prominent example, but it has been joined by Lanson’s Le Clos Lanson, Leclerc-Briant, Champagne Thiénot, Champagne Boizel and Barons de Rothschild.

Although a method of enhancing distribution, producers that use La Place are also clearly demonstrating a desire to push their brand – which also means raising prices.

Finally, in February this year François Pinault’s Artemis Group took a majority stake in Champagne Jacquesson. An established luxury group buying into Champagne is a clear sign of the health and potential of this sector, but nor is Artemis Group interested in offering collectors wines at entry level prices.

With both the houses and secondary market pushing prices, margins and gains will eventually come under pressure.

Conclusion

Champagne is clearly a region feeling the white heat of secondary market attention. Trade may be concentrated among a few leading names, but it is precisely these brands that have helped Champagne resonate with collectors and drinkers worldwide. More accessible and widely known, these brands have propelled Champagne to its record 12.4% share of the secondary market.

It is shaped by an aura of luxury and the most ostentatious bottles tend to carry the biggest premiums – be it large formats, special editions or celebrity Champagne.

Big bottles may also be something of a secret weapon for Champagne. It is the only region where big houses reliably produce sizeable quantities of magnums, jeroboams and upwards. Bordeaux does a bit but Burgundy, hardly at all as supply there suffers due to small vintages. And as the trade figures show, Champagne’s larger formats are incredibly popular regardless of the premium they command.

Heading into stormy economic waters once more, Champagne should be buoyed by its many strengths, namely brand power, prestige, distribution, relative value (although much reduced) and the much-heralded recent returns on investment. Nonetheless, any region on the boil will eventually get too hot for some. No market rises forever and the experience of other regions – such as Bordeaux in 2011– shows that periods of rapid growth can be followed by periods of pause, or retreat.

Champagne’s core strength lies in brand power and an enviable global distribution network. The question is whether these two elements alone will be enough to sustain the current run, as the old rules of engagement evolve, and the world loses its enthusiasm for celebration.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines. Independent data, direct from the market.