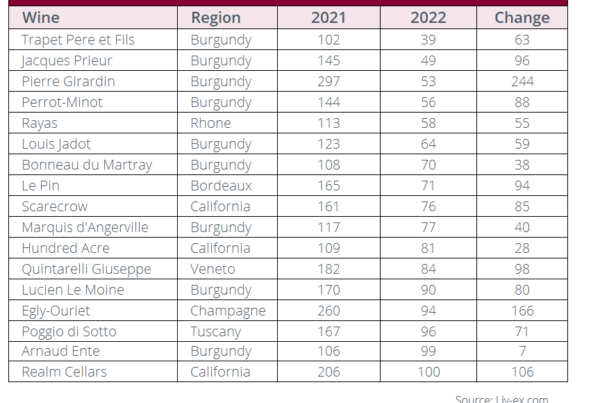

A league table ranking the most important wines of the world by their average trade prices

London UK: The top tier of the classification will reveal few obvious surprises but the real winners this year have undoubtedly been Italy and the U.S.

This is according to the results of Liv-ex’s latest report which analyses the most important wines of the world by ranking them based on their average trade prices.

Liv-ex is the London-based global marketplace for the wine trade, where 550 fine wine businesses from around the world buy and sell wine. What happens on the exchange is a reliable indicator of the health of the secondary wine market.

First published in 2009, the Liv-ex Classification has been updated every two years to reflect the changing conditions of the market.

The classification uses price to determine a hierarchy of the leading labels in the secondary market. Its inspiration is the 1855 Classification in Bordeaux which ordered the wines from top estates from fifth to first growths using their market price.

Italy and the U.S. lead the charge

The top tier of the classification will reveal few obvious surprises. The top wines of the world – the leading crus classés of Bordeaux, great grands crus of Burgundy, most exclusive Champagnes, Australia’s top Shiraz and cult Californians – all continue to command the leading prices in the fine wine market.

However, the real winners of this year’s classification have undoubtedly been Italy and the U.S.

With 83 wines included overall, the number of Italian labels increased 112% from the 2019 rankings. While the U.S. (entirely represented by California) rose 120% from 10 to 22 wines.

Four Italian wines that were in the 2nd tier in 2019 have risen into the 1st tier – all of them from Piedmont. The 1st tier is the only level of the classification where wines from Piedmont outnumber their Tuscan counterparts – eight wines to three.

Of the eight Piedmontese wines at the top, only one was a 1st tier wine in 2019 (Bruno Giacosa’s Barolo Falletto Vigna Le Rocche Riserva). The rest either rose up from the 2nd tier or are new entrants, such as another wine from Bruno Giacosa and one the Monfortino Riserva from Giacomo Conterno.

There may be more Tuscan labels in the classification as a whole, but these northern Italian wines are starting to deliver on their nickname of the “Burgundy of Italy”.

California has gone from having six to 10 labels in the 1st tier, equal to Bordeaux’s number of qualifiers.

As discussed in Liv-ex’s recent California report, Californian estates have some of the highest average prices in the market. With more activity surrounding Californian wines, more of its labels have qualified for the classification.

New Californian entries in the 1st tier include a second wine for Colgin, with the “Cariad” joining the “IX Estate”, Eisele, Hundred Acre’s Kayli Morgan Vineyard, Promontory, Screaming Eagle’s second label “The Flight” and one of Sine Qua Non’s wines also placed in the top tier.

France sees competition from other regions

As more wines from more diverse regions trade on the exchange, established regions like Bordeaux and Burgundy are experiencing growing competition.

This trend is reflected in the rankings as many wines that previously ranked in the top tiers have fallen due to their average trade prices struggling to keep up with other wines from up-and-coming regions.

For example, in 2019, Bordeaux labels constituted just over 37% over the classification list, this year it is just 28.6%.

Interestingly, the number of Burgundian wines on the list also declined by 30%. In 2019 there were 102 Burgundy labels, representing 29% of the total. In 2021 there are just 71, 20% of the whole.

However, interest in these regions has not disappeared. Instead it filtered out and down to other grands and premiers crus offering more immediate value. The scale of the broadening Burgundy market was examined back in April, and showed an increasing number of wines trading over the past three years.

In total there were 120 new entrants to the classification this year – 34% of the total. But 70% of these were not from Bordeaux or Burgundy.

Conclusion

This Liv-ex Classification cements many ongoing trends in the secondary market and these trends can be seen across almost every tier.

These trends have included Bordeaux’s declining share of trade, the diversification of the market (with Italy, Champagne, California and the Rhône seeing increased activity) and the broadening of the market even within leading categories such as Burgundy and Bordeaux as buyers seek value.

There was also more depth to all regions in the Classification. For example, in 2019, U.S. wines only appeared in the top two tiers, this year they were spread across four.

Bordeaux, Tuscany, Piedmont and the Rhône also had wines across all five tiers. Burgundy was found across four tiers, Portugal and Australia across three.

As the classification shows, buyers are casting their net wider in general and deeper within categories in the search for greater value. And, whether from £300 to £3,000+ per case, they are finding it.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £80m worth of wine and the ability to trade with 550 other wine businesses worldwide. They also organise payment and delivery through their storage, transportation and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Further information

This press release provides a shortened summary of Liv-ex’s latest report. The full report covers:

- A full list of the wines included in each tier

- Which wines went up and down

- Analysis on new entrants

- The methodology behind the ranking

To download the full report, please fill in the form on this page: https://www.liv-ex.com/2021/08/liv-ex-classification-2021/