Print and read offline instead.

Introduction

La Place de Bordeaux is one the world’s oldest established wine marketplaces. Originally a hub for distributing Bordeaux’s finest wines, La Place is a three-tier system where producers sell their wine to a network of over 300 négociants (via a middleman, known as a courtier), who then sell to merchants in more than 170 countries around the world.

Producers benefit from the négociants’ extensive global reach and expertise in promoting and allocating often limited volumes of highly sought-after wines to different markets. This distribution process guarantees the wines’ provenance and is an efficient way to reduce risk and manage supply and demand.

Today, the two most prominent La Place events are Bordeaux En Primeur in the spring/early summer, along with the release of (mostly) non-Bordeaux wines in the autumn. This latter offering has expanded considerably in recent years.

Unlike the En Primeur campaign, which is fluid, reactive and driven by châteaux decisions on pricing and release times, the autumn La Place campaign is more structured, which makes it easier for the supply chain to plan around. It has flourished in recent years, as the fine wine market has diversified and broadened beyond Bordeaux.

What started with the Chilean brand Almaviva in 1998 (a project of Baroness Philippine de Rothschild of Château Mouton-Rothschild) is now a fully-fledged campaign in its own right. Over 100 different wines from Argentina, Australia, the USA, New Zealand, Austria, Chile, China, Italy, Spain, South Africa, Uruguay and even French wines from Champagne and the Rhône have joined the marketplace.

Overall, close to 108 wines from 32 regions across 11 countries are expected to be released via La Place this autumn alone.

Part of the allure is the prestige of the system. Producers join to build or strengthen a globally recognised fine wine brand and, by doing so, hope to raise prices. Strategic brand development and gradual price increases over the longer term are key to their success, which becomes evident when the wines enter the secondary market.

Another reason for joining La Place is the négociants’ knowledge of niche markets. They have years of prior experience selling Bordeaux wines and understand the complexities of penetrating foreign markets.

The benefit is mutual. By selling wines from multiple sources, négociants get another revenue stream and reduce their dependency on the Bordeaux châteaux.

This is especially pertinent in a climate when the Bordeaux trade has been facing declining margins, as examined in our last En Primeur report.

Many Bordeaux châteaux have been releasing less stock at higher prices, which has meant that négociants have had less wine to allocate, which has (perhaps unintentionally) driven collectors to look further afield. Being able to offer more internationally renowned brands, as fine wine buying trends change, has naturally led to the expansion of the La Place portfolio.

Last year, Colin Hay wrote for the drinks business that ‘a small revolution has been quietly taking place in Bordeaux. La Place de Bordeaux, it seems, is becoming “the place to be”, not just for the grands crus of the Médoc, St Emilion, Graves and Pomerol, but also and increasingly for the leading fine wine regions of the world hors Bordeaux’.

But there might yet be a downside. Speaking with Liv-ex, Bordeaux wine expert Jane Anson warned that if too many wines are offered through La Place, the prestige of the system might suffer. However, for now, she continued, ‘the expansion of La Place de Bordeaux is a definite recognition that fine wine is no longer defined by a specific region or country but rather it is its own group’.

The changing secondary market

According to Liv-ex’s co-Founder and Director Justin Gibbs, ‘fine wine defines itself by having an active secondary market’. Fine wine has a resale value, brand recognition due to heritage, critical acclaim or both, and improves over time.

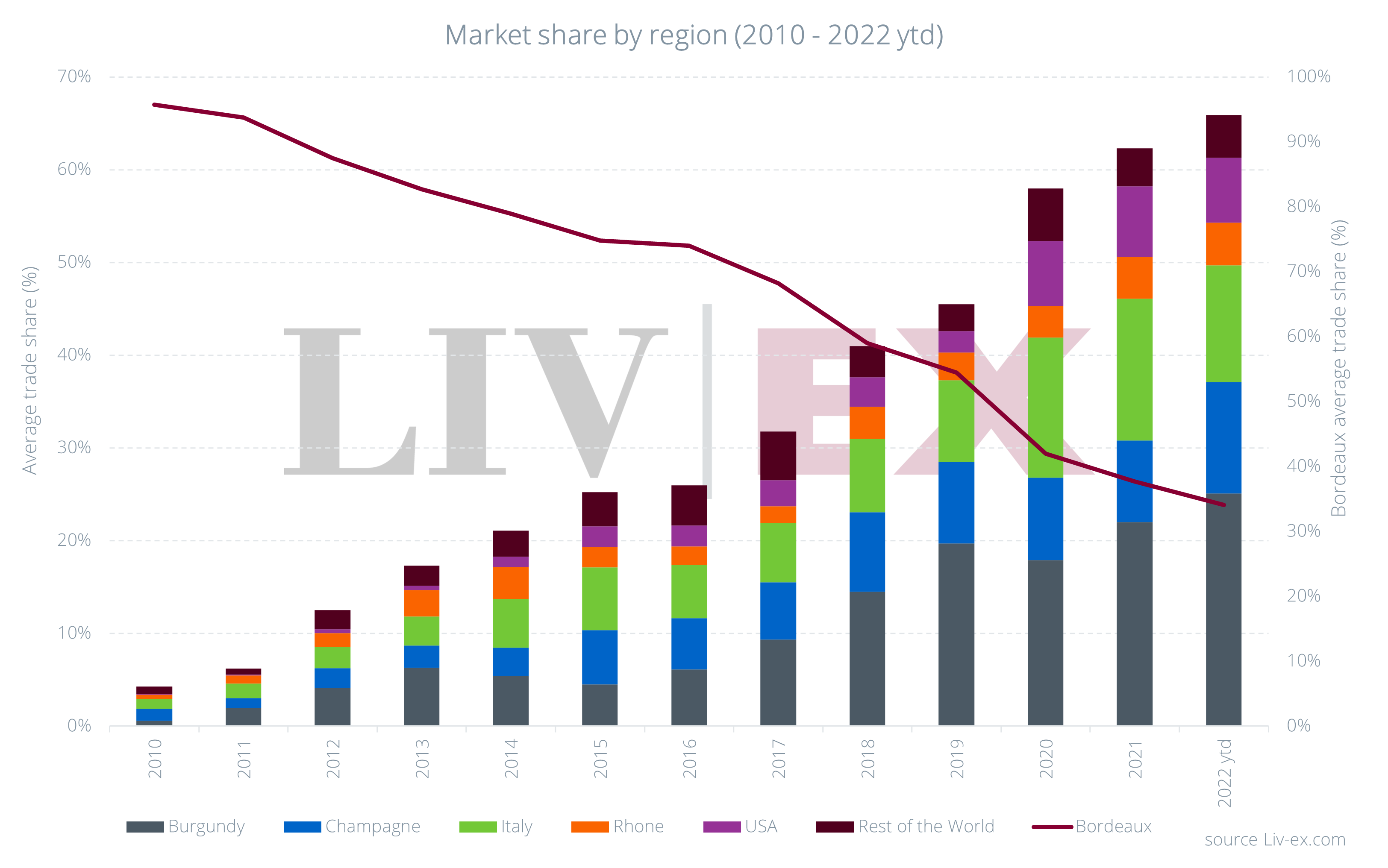

From a secondary market perspective, fine wine buying trends are changing. The market is no longer reliant on a single region. Bordeaux’s trade share has been faltering since 2010, when it accounted for 95.7% of total trade by value. Year-to-date, it sits at a record low of 34.1%. Bordeaux is also no longer the most traded fine wine region in some key markets such as Asia.

The transformation of La Place de Bordeaux reflects this shift in the buying patterns in the secondary market.

The number of wines trading on the secondary market has risen sevenfold in this same period. Year-to-date, over 9,100 different wines (measured as LWIN11s) have traded on the market. Last year marked a record high of 12,055. A big portion of these wines came from the Rest of the World (RoW) category.

Rest of the World gains momentum

The Rest of the World category tracks the trading activity for wines outside of the six key regions that have traditionally dominated the secondary market: Bordeaux, Burgundy, Champagne, the Rhône, Italy and the USA. Its growth in the last 12 years has been notable.

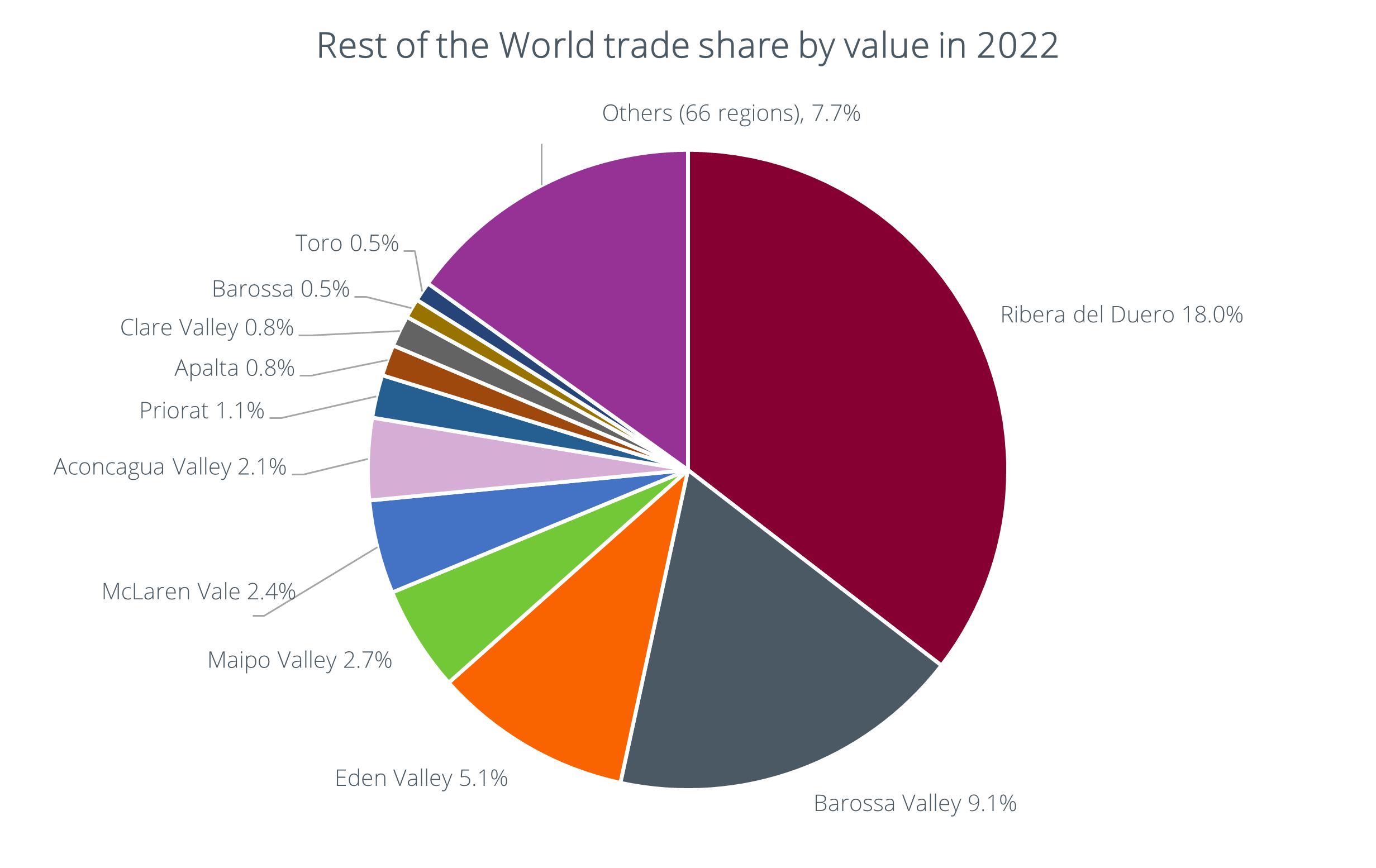

In 2010, its market share stood at just 0.8%, year-to-date it accounts for 4.6% of the total market.

So far in 2022, the category includes wines from 77 different regions, up from 60 in 2021. The chart below shows the regions that have taken the largest share of trade by value in 2022. Australian and Spanish regions are the leading players.

Wines such as Telmo Rodriquez Yjar (Rioja), VivaltuS (Ribera del Duero), Will Berliner’s Cloudburst (Margaret River) and Jim Barry’s The Armagh Shiraz (Clare Valley) are among those now released via La Place. According to a Wine Spectator article, Sam Barry, commercial manager of Jim Barry wines, said that ‘Australian wine is still underrepresented on the global fine wine stage, so being on La Place is not only a breakthrough for The Armagh, it is a breakthrough for fine Australian wine’.

This year will see the launch of the first brand from New Zealand as well, Craggy Range with its Le Sol Syrah and Aroha Pinot Noir.

Main La Place stars

While wines from South Africa, Uruguay and China appear on the global stage via La Place, the majority of autumn releases come from Italy, the USA and France itself.

Italy

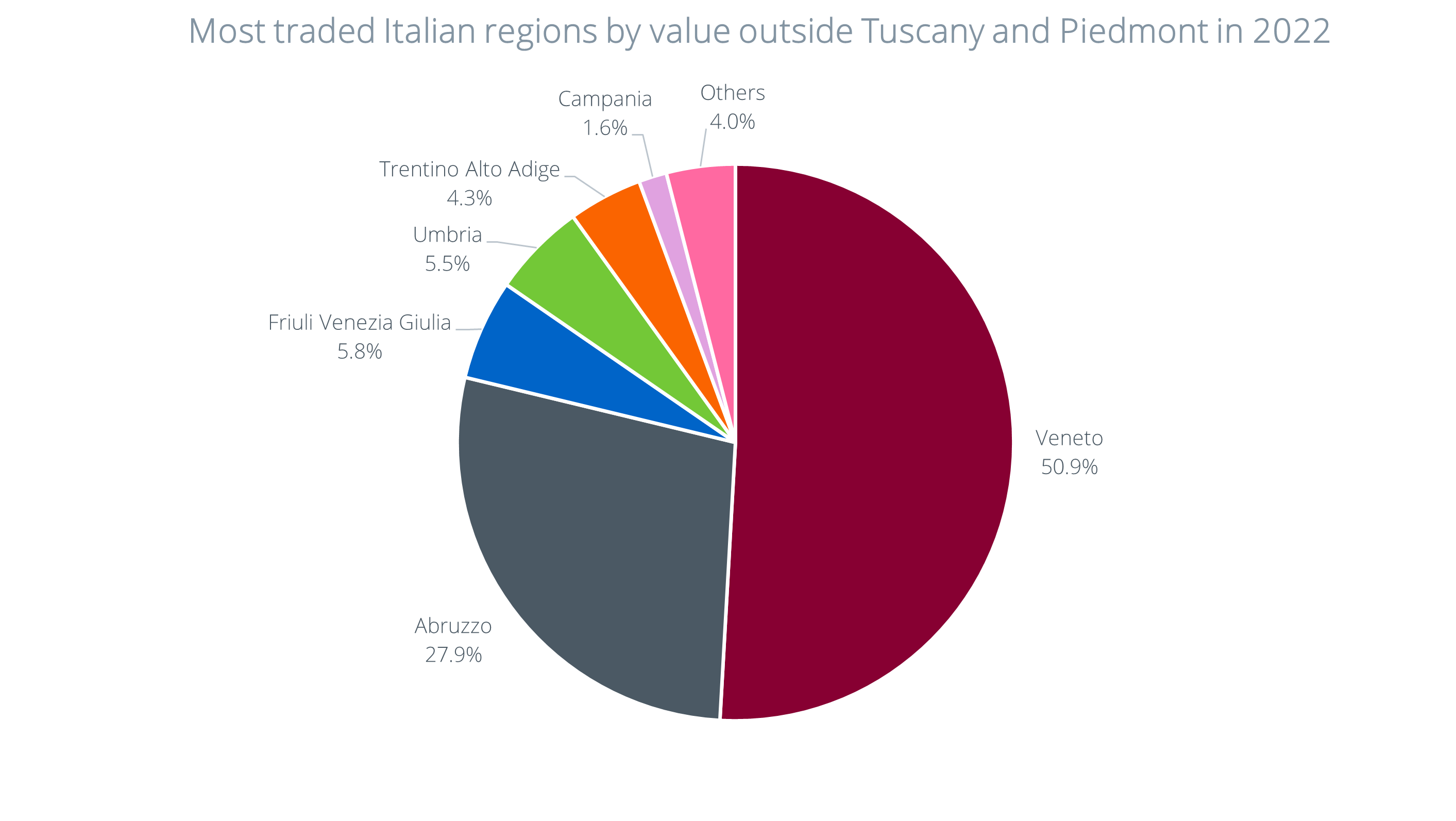

Italy – whose market has considerably diversified beyond its main pillars, Tuscany and Piedmont – makes up over a third of the autumn releases and is thus the most heavily represented country.

Masseto was the first wine ‘with no specific Bordeaux ties’ to join La Place in 2009 with its 2006 vintage. The brand kick-started an influx of Italian fine wines, that now includes Antinori’s Solaia, Bibi Graetz’s Testamatta and Colore, alongside Caiarossa and Galatrona.

While the Super Tuscans Ornellaia, Masseto, Solaia and Bibi Graetz are now among the most established La Place names – and have developed active secondary markets – many other Italian wine regions are represented.

These range from Podere Giodo (Brunello di Montalcino) and Castello di Fonterutoli (Chinati Classico), to the Barolo producers Parusso and Michele Chiarlo, Allegrini from Veneto and Giovanni Rosso from Sicily. Of these, Parusso, Chiarlo and Allegrini joined the network this year, the first domains from Piedmont and Veneto.

As examined in our 2021 report Italy’s underdogs, the secondary market for Italian wine has also expanded recently, following a sustained rise in the number of wines in demand. Critical attention and the search for value have led to the increased presence of ‘other’ Italian regions in the secondary market, such as Veneto and Abruzzo.

*Others includes Sicily, Marche, Puglia, Calabria, Lombardia, Emilia Romagna, Lazio, Basilicata, Lugana and Sardinia.

The USA

The USA is the second most represented country in the autumn La Place campaign. The first American estate to join (in 2004) was Opus One, which like Almaviva has a link with the Rothschild family.

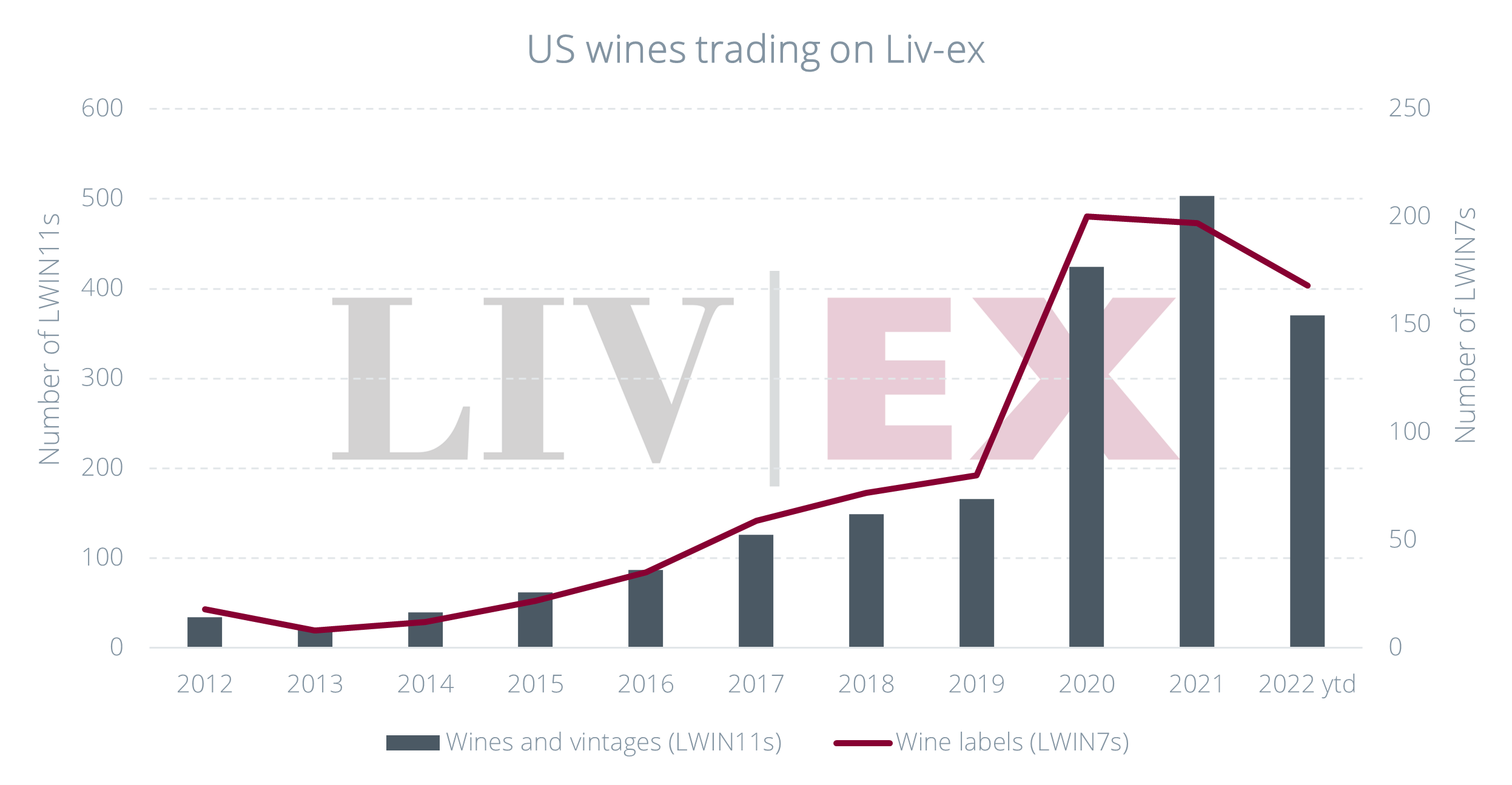

As with Italy, the USA has emerged as a strong secondary market force, and particularly so, over the past three years. Between 2019 and 2021, its share of trade has risen from 2.3% to 7.6%, while the number of wines trading has tripled. We explored its development and future potential in our report, California: A Golden Era for the Golden State. During this time, more US wine producers have started using La Place.

Considered by many to be the USA’s premier wine region, it is no surprise that a growing number of Napa Valley estates have since followed in Opus One’s steps. Estates such as Inglenook, Joseph Phelps and Promontory.

They are far from alone, though. US wines available via the Bordeaux négociants also include Sonoma’s Vérité and Trinité Estate, Oregon’s Beaux Frères, and L’Aventure and Daou Family Estates from Paso Robles.

Sustained demand for Opus One

As mentioned at the beginning, part of the aim of selling through La Place is to build a brand by giving it a global reach. The consequent rise in demand for a limited product, it is hoped, means the price for that wine can be increased, adding to its luxury status and image.

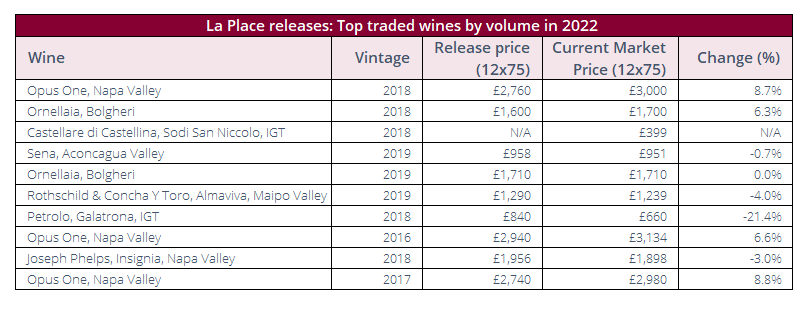

For some labels this has been the case. Opus One for example. Opus One 2018, released in September last year, is the top-traded wine from last autumn’s clutch of releases. The wine’s Market Price has risen 8.7% in value since release.

Furthermore, despite being released several years ago, its 2017 and 2016 vintages continue to see high levels of secondary market activity.

Post release price performance

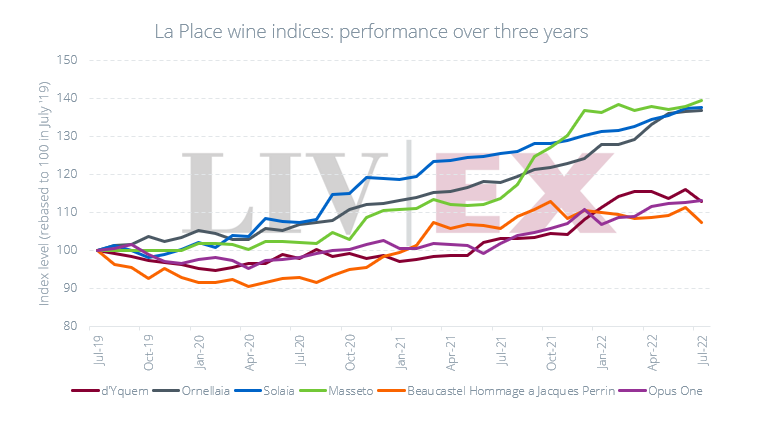

The chart below shows the price performance of some of the more established brands released via La Place today.

While all of the wine indices have risen in value, Beaucastel Hommage à Jacques Perrin (11.3%), Opus One (12.6%) and d’Yquem (15.9%) have lagged behind the Super Tuscans. Masseto (40.5%), Ornellaia (38.2%) and Solaia (37.2%) have led the way over the past three years.

Founded in 1981, Masseto built and enhanced its brand image over time, while prices gradually appreciated based on scores, age and vintage quality. New releases such as last year’s 2018 offering tend to offer relative value compared to older vintages from the same producer. The brand has also outperformed the broader Italy 100 index over the last three years.

During this time, Masseto has been the second-most traded Italian wine on Liv-ex after Sassicaia. Prior to joining La Place (2005-2007), it was the ninth most traded Italian wine brand (out of a much smaller pool of wines trading). Upon joining the distribution network, Giovanni Geddes, CEO of Tenuta dell’Ornellaia, told Decanter that the estate had ‘decided to do this to help raise the global profile of Masseto’. And it would seem it has succeeded.

However, not all aspirational producers achieve the same success. Those that push prices before their brand is fully established are unlikely to see the desired benefits. Nor for that matter is La Place.

Mixed fortunes for newly released brands

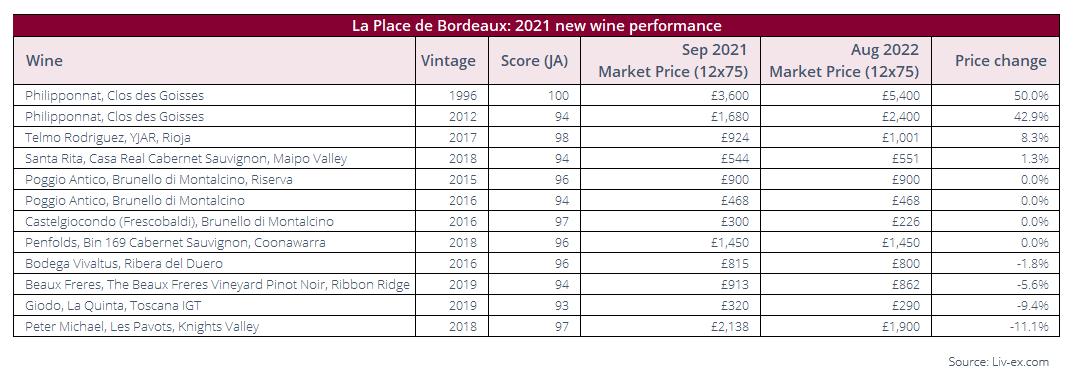

The table below shows the price performance of brands offered via La Place for the first time last year. The top-performer has been Philipponnat Clos des Goisses, which released its 2012 vintage and re-released its 1996 via four select négociants. Since last September, the Market Price of the 1996 has risen 50%, while the 2012 is up 42.9%. But, while new to La Place, Philipponnat was already a known and well-respected brand and the market for Champagne is thriving.

More interesting to note is Telmo Rodriguez’s Yjar 2017. Jane Anson described it as ‘a cult wine in the making’, and it has risen 8.3%. The Chilean Santa Rita Casa Real Cabernet Sauvignon 2018 is also up 1.3% since release.

However, the rest of the new arrivals have run flat or declined in value. Clearly, releasing via La Place does not guarantee immediate price appreciation. Like Bordeaux En Primeur, it all comes down to price and relative value.

According to Liv-ex’s Americas Territory Manager, Robbie Stevens: ‘A successful release can see a wine selling out in a matter of hours; the wrong price can leave stock languishing in négociant and merchant cellars for years. Whether the wine is from Bordeaux or elsewhere, it needs to be priced correctly relative to the ever-broadening market’.

*click to enlarge

Concluding thoughts

As the market continues to broaden, producers are facing competition from all corners of the world. Releasing via the premier distribution network for fine wine, La Place de Bordeaux, helps create global reach and make their name known. However, building a brand does not happen overnight. It requires careful planning and pricing in line with the market, as buyers are increasingly aware of value.

The current economic climate, characterised by rising inflation, is providing the ultimate test to emerging brands and the fine wine market as a whole. Diversity looks to be the reason behind the market’s resilience despite external pressures. Indeed, only the broadest measure, the Liv-ex 1000 index, managed to keep its head above water in July. The rise of ‘other’ regions trading actively, unlike five years ago, also attests to the opportunities for diversification within the fine wine market.

La Place de Bordeaux seems to be riding the wave of expansion. At present, all players can benefit from it. Producers get more exposure, négociants can exploit more sources of revenue and fine wine merchants enjoy a wider choice of wines to offer their customers who amass a more diversified portfolio; which lessens the risk of losses during a potential market downturn.

It remains to be seen to what extent La Place, and indeed the fine wine market, will continue to expand. The more crowded it becomes, the more new arrivals might struggle to find an audience. There may yet be a saturation point where the benefits of being released through La Place are lost in an enormous jumble of releases.

Above all, it needs to be remembered that releasing through La Place is not a portal to instant success. It is a useful component in brand development but not an automatic green light to push prices beyond the limit the market is ready to pay.

Meanwhile, the upcoming campaign, bigger than ever before, will showcase new brands and new vintages from established favourites. The market will decide where to bestow its favour.

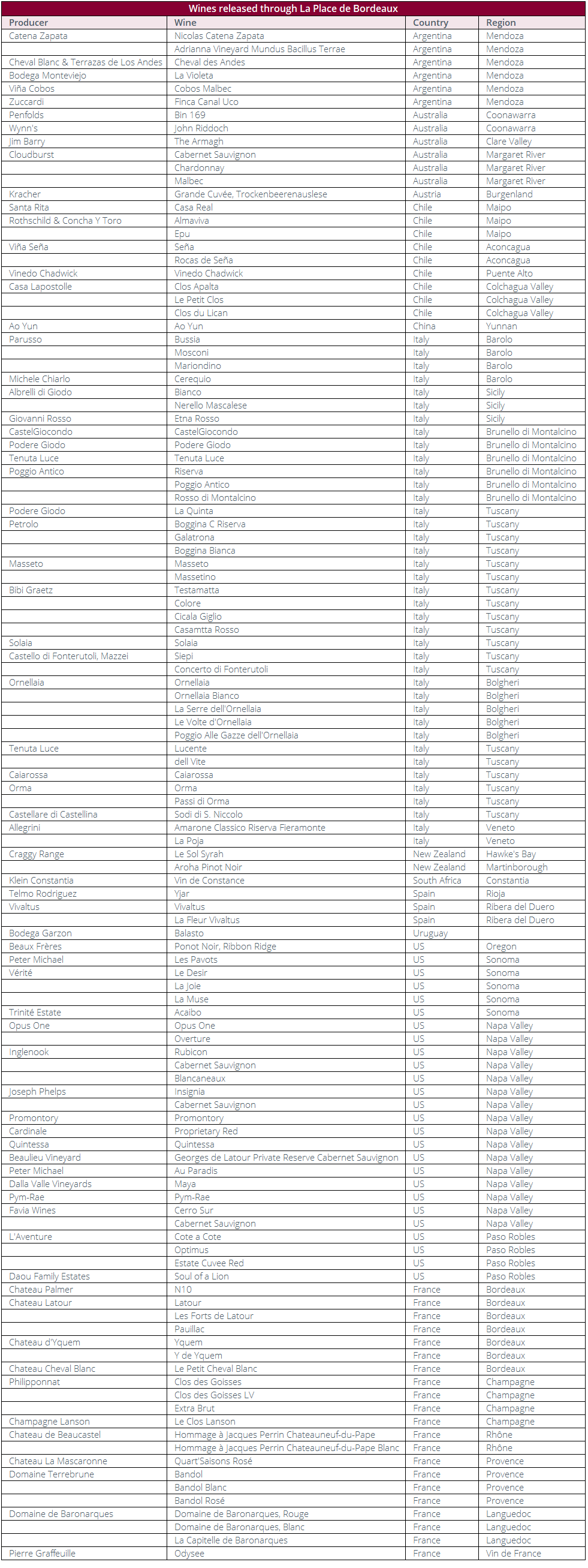

Appendix of upcoming releases

*Click to enlarge

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines. Independent data, direct from the market.

Read the full article or jump to the relevant section…