“It’s only so long until word gets out. Frankly, these are two of the most exciting winemaking regions in Italy today.” – Eric Guido on Umbria and Lazio for Vinous, August 2021

Italy cultivates over 2,000 grape varieties, has 20 administrative wine regions, and was a vital springboard in the development of western wine civilisation.

It is also increasingly playing an important role in the development of the secondary market for fine wine; a topic first explored in our 2019 report, The fine wines of Italy: past, present and future. Its market is more buoyant than ever, the Italy 100 index reached an all-time high last month (August 2021), and the country’s share of total trade by value stands at a record 16% year-to-date.

The diversity the country has to offer combined with the quality of its wines has attracted more active market participants from the US, UK, Asia and Europe. As a result, more Italian fine wines have begun trading. The number of Italian wines that made it into in the 2021 Liv-ex Classification, which ranks the wines of the world by price, rose 112% from 2019.

In the main, it is the leading estates of Tuscany and Piedmont that dominate trade so far – the “Super Tuscans” and great domains of Barolo. But there has been movement from smaller producers and previously underrepresented Italian regions outside these main strongholds too. This increasing diversity is the topic of the following report.

Broader market overview

Fine wine prices have been rising across all regions, and Italy is now the third-best performer of the past year in the Liv-ex 1000, up 12.2%.

Its long-term price performance has been characterised by low volatility and steady returns. The Italy 100 has appreciated 240% since its creation, having enjoyed a particularly good half-decade.

The index tracks the prices of five Super Tuscans and five other leading Italian producers, but it can be used as an indicator of broader pricing trends in the Italian market.

Regional trade share

Italy is taking an increased share of secondary market trade – a record high of 16% so far this year. Italy is now the third most traded region after Bordeaux (40.5%) and Burgundy (20.4%).

How many Italian wines trade on the secondary market?

Italy is also one of the few regions where the number of distinct wines trading (ie the number of wines with a vintage, as measured by LWIN11) in the first nine months of the year has already surpassed the levels achieved for the whole of 2020, by 5.3%.

The increase in the number of wines trading has been sustained, pointing to a significant market expansion and heightened demand for Italian fine wine. More Italian brands (LWIN7s) have entered the secondary market, pushing trade across a wider array of vintages too. Between 2010 and 2021, the increase in Italian LWIN11s traded has been an impressive 2,566%.

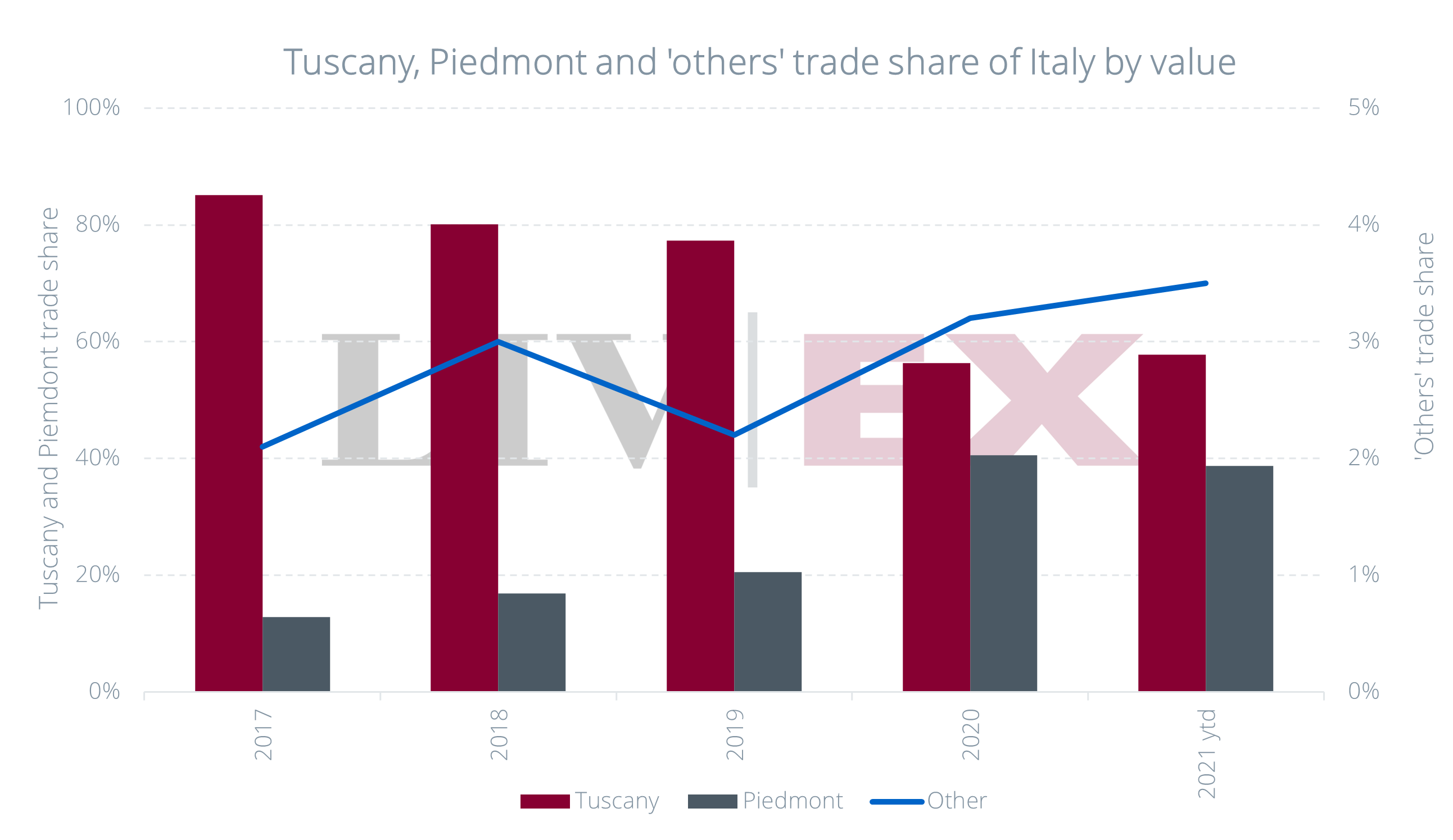

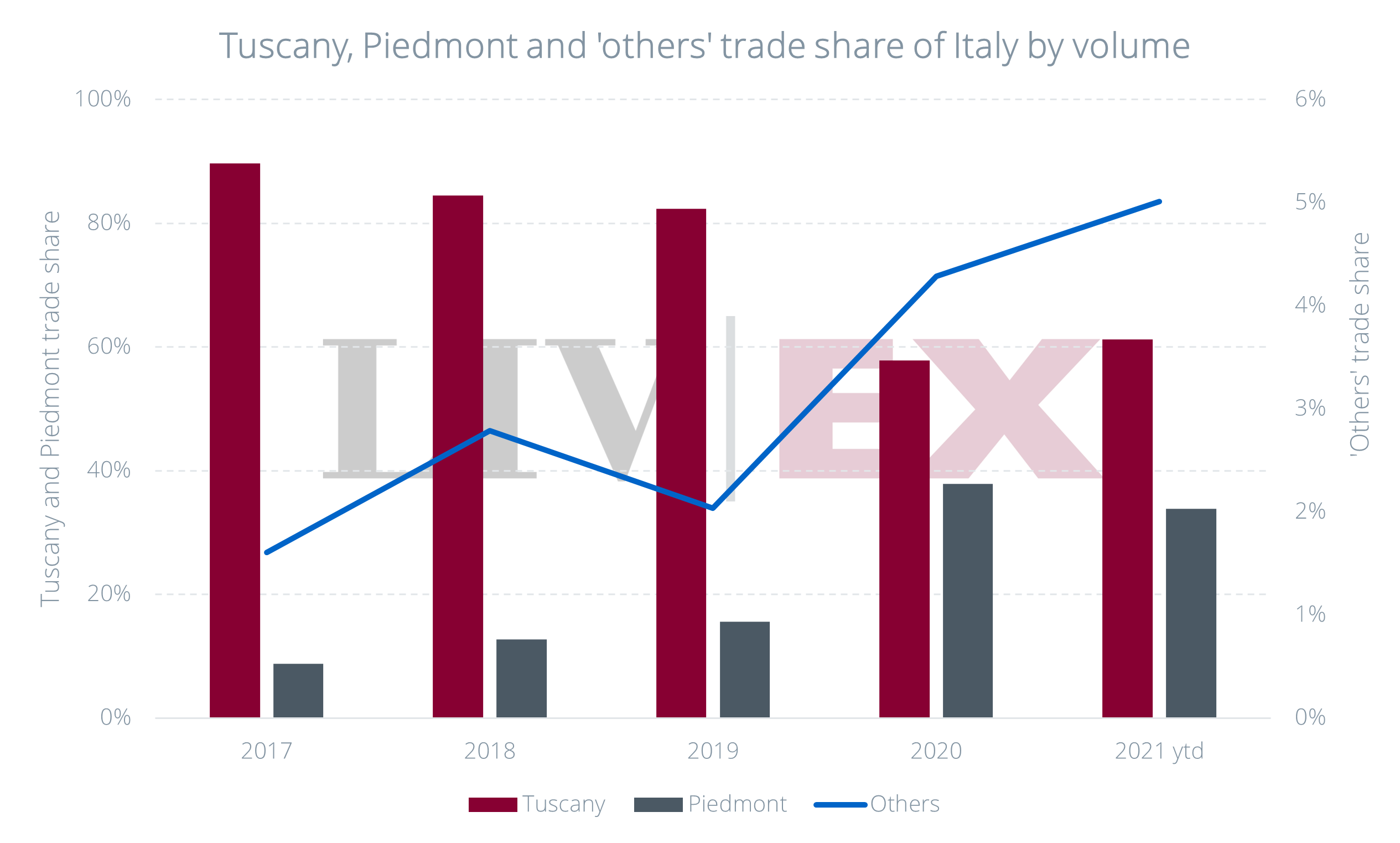

Tuscany, Piedmont and the “others”

In our last report on Italy, we pointed towards the divide between Tuscany and Piedmont. Historically, Tuscany has led in terms of trade share thanks to the greater liquidity of its wines, while Piedmont has given rise to some of the best price performers.

While Tuscany and Piedmont remain the pillars of Italy, combined taking over 95% of total trade value and volume, there is evidence that the Italian market is broadening.

The “other” Italians, which failed to accumulate significant trade share up until five years ago, now make up over 5% of the Italian market by volume. Due to their generally lower prices, their value share has also been lower – but it’s still on the rise.

The reasons for this have been manifold.

Buyers are searching for exciting new discoveries within Italy, and many of the smaller regions offer great value for money. There are wines for drinking, but also for investment. As the fine wine market broadens and expands, more major wine critics are reporting on the excellent quality offered by many of these wines.

In his recent report for Vinous, for instance, Eric Guido argued that Umbria and Lazzio “are the two Italian regions that receive significantly less credit than they deserve” and that “when it comes to value, both regions offer that in spades”. In July, Guido looked at the “treasures of Italy’s Southern Adriatic and Ionian Coasts”, reviewing wines from Umbria, Basilicata and Calabria.

The Wine Advocate’s Monica Larner also published her annual report on Alto Adige this September, noting that the “northern Italian wine region moves closer to icon status” each year. She added that “a string of excellent vintages is hitting the market now”, including white wines from the 2020 and 2019 growing seasons and red wines from 2018 and the warmer 2017 vintage.

In his latest weekly tasting report, James Suckling wrote about another Italian region – Campania: “I first visited the area for wine in 1985 and have been astonished by the history and pure beauty of the region ever since. Its unique wines, from such varieties as Aglianico and Fiano, highlight the incredible diversity and raw beauty of the appellations it holds”.

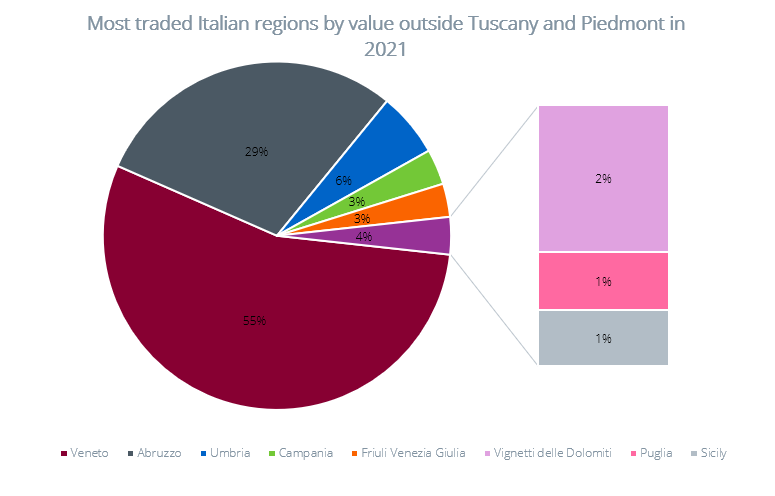

The chart below shows the most traded Italian regions by value on Liv-ex year-to-date.

Veneto

Veneto, in the northeast corner of Italy delivers fairly large-scale wine production. The region has gained recognition for its highly diverse array of wines, which include Valpolicella, Amarone, Soave and Prosecco.

On the secondary market, Veneto accounts for more than half the total market for “other” Italians – 55%. The first trade for a wine from the region on the global marketplace happened in 2003 for Dal Forno Romano’s Amarone.

The most traded wines (LWIN11s) from Veneto so far this year, along with their current Market Price, can be seen in the table below.

Abruzzo

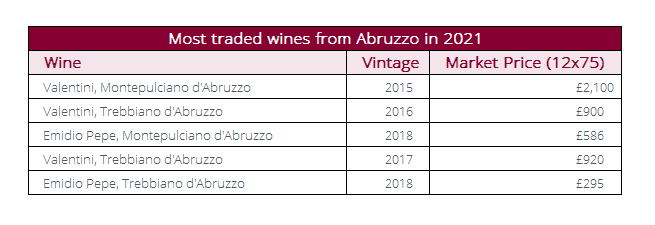

Abruzzo, located on Italy’s Adriatic coast, is most famous for Montepulciano and Trebbiano, which were historically used for bulk wine production. Other native wines produced in the area include Sangiovese, Passerina, Pecorino and Cococciola.

Abruzzo has accounted for 29% of the total market for “other Italians” by value so far in 2021. It’s the region’s first trade was for the increasingly sought-after Emidio Pepe in 2018. Year-to-date, the highly sought after Valentini Montepulciano d’Abruzzo has been the most traded wine by value.

Umbria

Umbria, bordering Tuscany and situated above Rome, is home to crisp Grechetto and the bold Sagrantino. Guido commented that in 2021, “there’s a newfound energy here, higher-quality winemaking, and a focus on terroir that I’ve never witnessed before in Umbria”.

The region has taken 6% of trade by value, with the first trade for its Lamborghini Campoleone happening in 2009. Now, Antinori’s Cervato della Sala leads the trade category – a rare example of a white wine topping Italian trade.

The rest

Regions like Puglia, Sicily and Campania are yet to generate more significant trading activity, but more eyes are beginning to wander in their direction.

So far this year, 16 distinct wines from Campania have changed hands, as well as 11 from Sicily, and four each from Puglia, Trentino Alto Adige and Sardinia.

Below are the top traded by value from each region.

As their exposure grows, and more producers seek routes to the international market, it is certain that the future of Italian wine – beyond Tuscany and Piedmont – is looking bright.

Final thoughts

The increased diversity of Italian wines trading on the secondary market would have hardly been possible without Italy’s strengthened image as a competitive fine wine force on the international stage.

The wines of Tuscany and Piedmont have lured in buyers, who are now exploring other Italian regions. The rare wines made from Nebbiolo in the north have contributed to the country’s impressive price performance and sparked investment interest, while the critically acclaimed Super Tuscans (combined with their brand strength and larger quantities) have generated the majority of trade and offered steady returns and low volatility.

Italy’s exemption from the 25% US tariffs on European wine (imposed in October 2019; suspended in March 2021) contributed to heightened demand for the country’s offerings from American buyers. In 2020, US merchants focused mostly on Italian wines, which took up 27.4% of total trade, compared to 26.5% from Bordeaux and 11% from Burgundy.

As recently explored, another traditionally Bordeaux-dominated market, Asia, has also turned its eyes towards Italy. Wines from Barbaresco feature among the most active wines traded by volume in Asia in 2021, highlighting the on-going strength of Italy on the secondary market.

This demand has led to greater exposure from more Italian regions, including many of Italy’s “underdogs” which entered the market in the last two years.

As for the future, the quality and value offered by Italian wines would seem to be attracting more active players globally and Italy’s full potential is yet to be truly unveiled.