Key findings:

- The timing of this year’s En Primeur no longer looks as stifling as it once did, and most critics’ tastings and reports should be concluded by early May.

- These assessments will be vital to the success of the campaign, with release prices predicted to rise, but should not obscure the delicate position of Bordeaux in the wider market.

- Initial indications suggest potential for high quality-wines, but 2020 appears to be a heterogenous vintage.

- High temperatures in the growing season affected volumes, making the 2020 crop smaller than 10-year average.

- With on-going stock retention practices and the possibility of bad frost damage in the region, the number of cases released this year could shrink further.

- The trade should expect a small, fast-paced campaign, likely to happen in late May-June.

Print and read offline instead.

Background to the 2020 campaign

Hopes for an improved global situation and the chance to host in-person tastings this year have foundered, dashed on the twin rocks of government ‘roadmaps’ out of lockdown and rising Covid cases in mainland Europe. Once again, much of the fine wine trade will be faced with assessing the latest Bordeaux vintage ‘remotely’ and while demand for fine wine is in far ruder health than it appeared a year ago, there are a unique set of challenges facing the 2020 vintage as it comes to market.

The main question, as it is each year, is how the new vintage will be positioned. Over the past decade, Bordeaux has priced itself based on an inherent perception of vintage quality, as determined by critic scores, rather than the commercial reality of the day-to-day market. Last year’s campaign marked a step away from this logic. Despite major critic scores placing the 2019 as one of the best vintages of the decade, prices were cut by 21% on average versus the 2018s with some labels seeing reductions as high as 31%.

This was a welcome nod to the financial stress the market was experiencing as the pandemic, combined with US tariffs, ongoing Brexit uncertainty and conflicts in Hong Kong, impacted demand. Attractive pricing lured many in the trade and their customers back to En Primeur, and for the first time in years, a healthy secondary market developed, the sign of a successful campaign. Will we see the same this year?

Price increases?

Recent reports seem to suggest an expectation of price increases to come. As one merchant recently quoted in the drinks business said: “Bordeaux seem to be of the opinion that customers got too good a deal in 2019.” Although a (supply) limited campaign in hindsight, the 2019 release proved to be a success for all involved – château, négociant, merchant and collector – precisely because it was a good deal. And when viewed in this way it shows that a taste for Bordeaux futures still very much exists. But push too hard on prices and this enthusiasm can prove fleeting. Buyers scare easily if the pricing pendulum swings too abruptly.

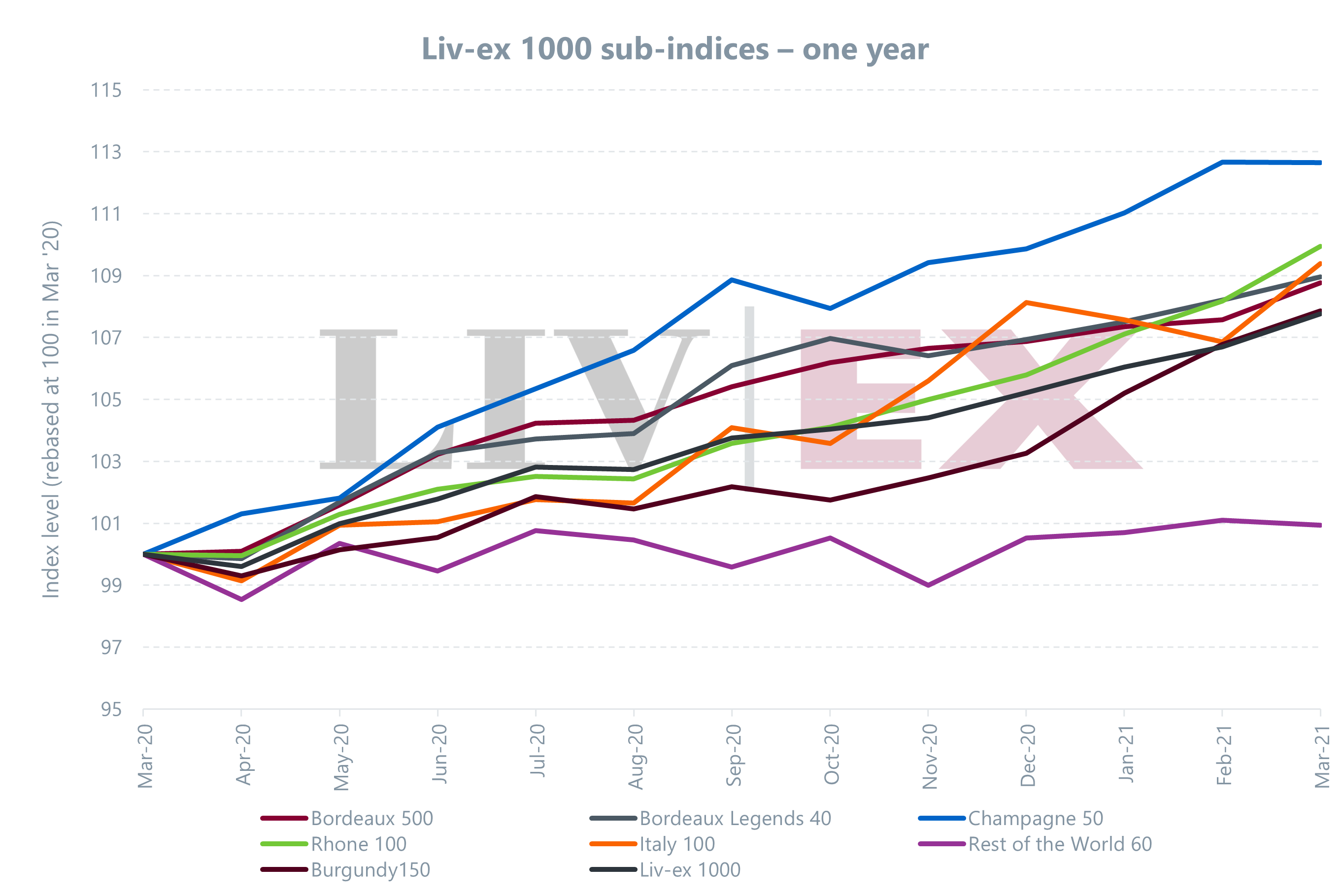

After a year of the pandemic, the outlook is not as uncertain as it once was. US tariffs are currently suspended, the situation in Hong Kong is more settled, and while Brexit has brought added complications for importers, it has not stymied trade entirely. The market for fine wine has in fact gathered steady momentum since last summer. The benchmark indices, the Liv-ex 100 and Liv-ex 1000, have seen gains over ten and seven consecutive months respectively, driving the Liv-ex 1000 to its highest-ever level. March, meanwhile, proved to be the broadest month of trade yet recorded, with over 1,400 distinct wines in play.

Amid all of this, the market for Bordeaux itself is delicately poised. The welcoming of the Year of the Ox in Asia, the suspension of US tariffs and the release of in-bottle reviews for the 2018 vintage, have all provided succour to Bordeaux’s steady performance of late. And yet, Bordeaux’s monthly share trade by value has continued to drift to hit a low of 37.2% at the end of March, and it has sunk further since. The Bordeaux 500 index has also been a slow mover over one year, having risen 8.7%, slightly outperforming the Burgundy 100 (7.8%), but underperforming Champagne, Italy and the Rhône. The region faltered in the 2020 Power 100 rankings too, with five labels falling out.

As this report will make clear, it is likely that this will be another short, sharp and limited campaign. Last year’s was a smaller than average vintage and with (at the time of writing) frost alerts across France, concerns about the 2021 crop could affect the release and pricing strategy for this campaign as the 2017 frosts did on the cusp of the release of the 2016s. If so, this will add to continuing concerns surrounding stock retention in Bordeaux, and the sustainability of the châteaux strategy of withholding wines to release at a later date.

The market for Bordeaux is open and robust and will no doubt welcome a well-judged campaign, but not at any price. The 2019s were able to catch the attention of the market, the Bordelais should ensure that their 2020 wines are able to hold it.

2020 harvest overview

The great variable in any discussion of each year’s En Primeur campaign is the quality of the vintage at the heart of it.

An enormous amount of the world’s time, attention and energy last year was taken up by the unfolding Covid-19 situation. The logistical gymnastics of a ‘remote’ En Primeur campaign and the challenges of managing estates and harvesting while complying with national lockdowns and social distancing requirements became hot topics; the usual subject of the weather took a back seat for once.

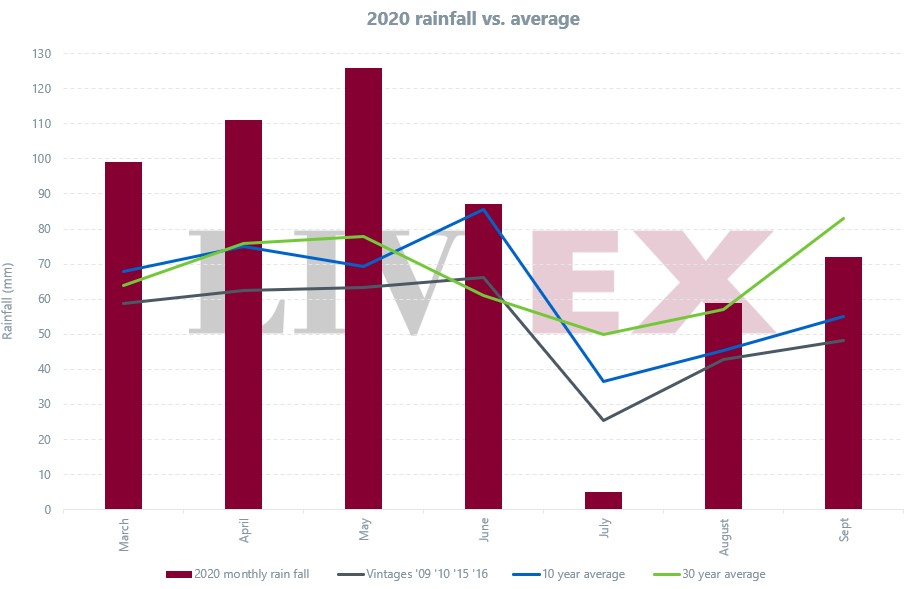

It is true that there was no cataclysm in the form of frost or hail – a small mercy perhaps given the current situation – but it was not an entirely uneventful growing season. The overall pattern was a wet spring with quite high mildew pressure, followed by a long, hot summer and a harvest-time heatwave.

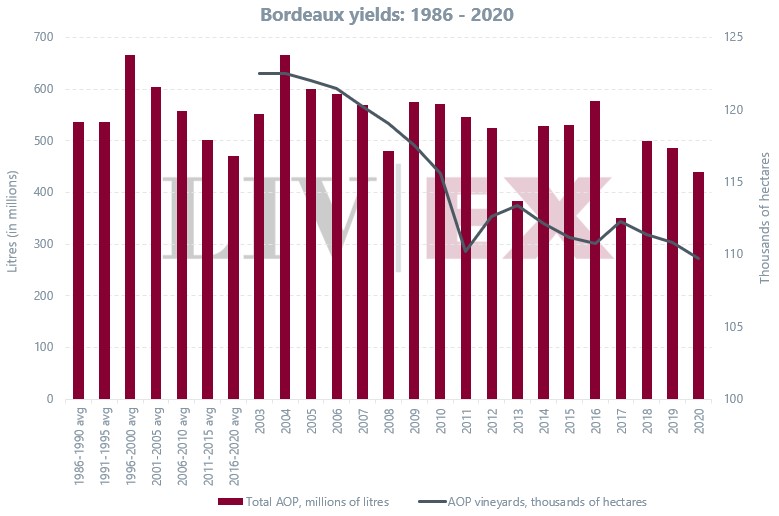

Similarities have been drawn to the 2016, 2018 and 2019 growing seasons, but while 2016 delivered a sizeable crop and both 2018 and 2019 hit the 10-year average (486 million litres), 2020’s final yield of 440m litres is about 10% lower than the two years that preceded it.

The chief cause of this was the heat. As Gavin Quinney laid out in his annual harvest overview, there were 54 days of drought between 18th June and 11th August and a heatwave with temperatures in the mid-30s in September led to a loss of juice at this crucial stage as well.

“You could almost feel the juice evaporating,” he commented.

Chart 1

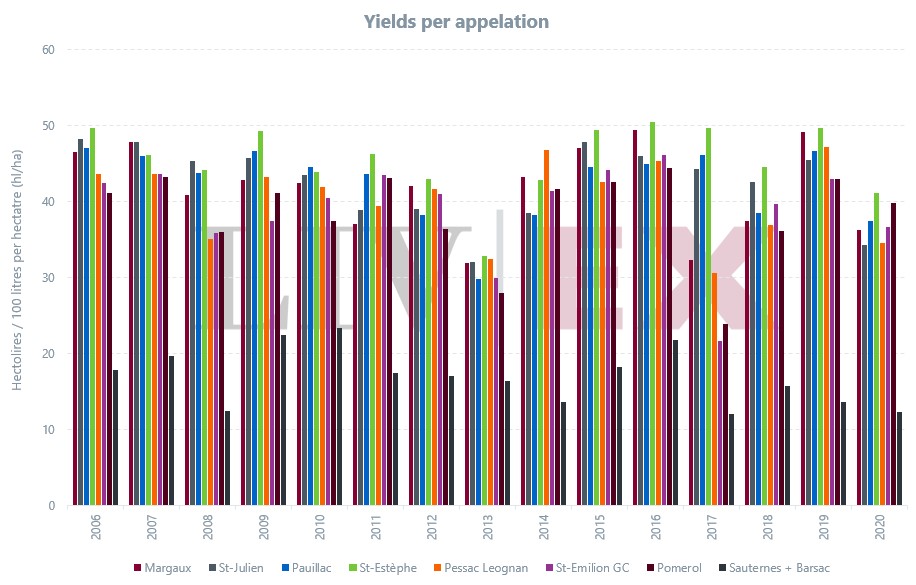

Yields then were small but not miniscule; this is still a bigger harvest than the frost-struck 2017s and the rot-ridden 2013s. In AOCs with classed growths the only noticeably smaller crops were in St Julien and Sauternes & Barsac.

And it is worth pointing out that in Pomerol, yields were slightly higher than they were in 2018 (40hl/ha in 2020, 36hl/ha in 2018), as the earlier-ripening Merlot had largely been harvested by September and so escaped the shrivelling effect of the late heatwave. Dry white production was also less affected for the same reason.

Chart 2

Saturnalia’s initial harvest assessment also noted that 2020, while a warm vintage, lacked the “excesses of 2018 and 2015”. And drought aside, it was a wet season overall. Was there enough rain in the early part of the year to temper the worst of the summer drought?

Following its own analysis, Saturnalia picked out Pessac-Léognan, St Emilion and Pomerol as its top-performing appellations, with half of the top-rated 10 wines (in their estimation) likely to be from Pomerol.

Chart 3

Ripeness, concentration and alcohol levels will be deeply scrutinised across many AOCs, therefore. Many early commentators have remarked on the potential for excellent wines but also on what is likely to be a high degree of heterogeneity from appellation to appellation, château to château.

The Bordelais, along with other French winemakers, are becoming more adept at dealing with hotter vintages. Certainly, there is now the know-how and technology to handle ripeness and alcohol better than in the past. Nonetheless, Antonio Galloni at Vinous in his recent in-bottle report for the 2018s was moved to say that: “It does seem we are approaching a limit of how rich these wines can be.”

2020 En Primeur Campaign Overview

2019: The surprise success

Last year’s campaign ended up being a surprise success, though a limited one. With all the headwinds against the financial and fine wine markets at the time, as well as the challenges presented by the spreading Covid-19 pandemic, postponing the show seemed a real possibility.

The Union des Grands Crus de Bordeaux persevered, sending out hundreds of samples to the trade and critics, but the disjointed nature of samples arriving, being tasted, written up and so forth meant that wines were being released before a full picture had emerged. Nonetheless, in what was a short, sharp campaign, with good scores rolling in and prices being cut by as much as a third on the 2018s, the vintage found a ready market.

Perspective, however, is important. Expectations were so low for the campaign that almost any level of sustained interest would have counted as a win. Demand proved to be narrow and focused on about thirty key names in total. As explained in the post-campaign report, many wines remain unsold, in Bordeaux.

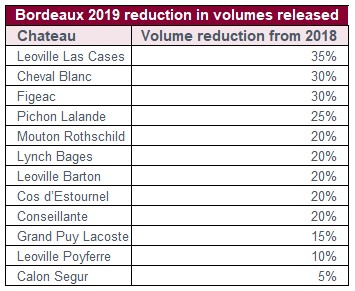

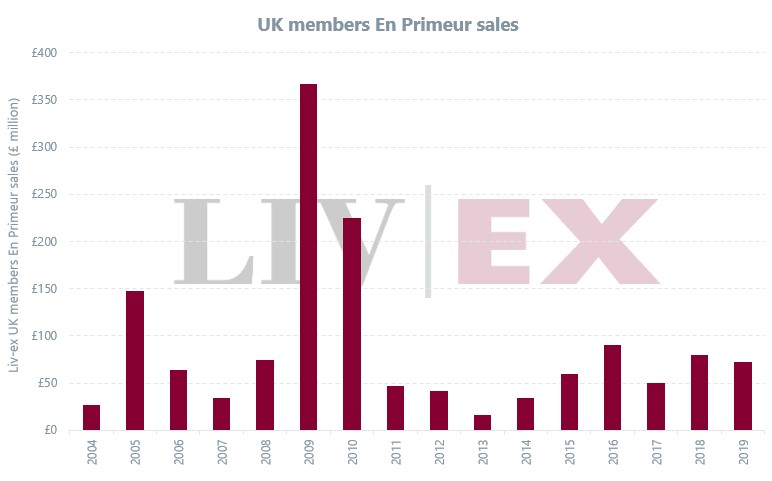

Prices came down but so did the volume of stock released. This has been a long-running trend over recent campaigns and a source of some frustration; both because it entails a lack of transparency in the process and it restricts the opportunity for trade. It was especially frustrating last year as price cuts meant there were eager buyers but not enough wine to satisfy demand.

This had the odd effect of meaning that although more wine was sold overall than the year before (up 15%), UK merchants’ sales values were less on average (down 10% overall and by as much as 30% in some individual cases). This was because stock was being spread more thinly between sellers, in addition to price cuts and continuing stock retention. Furthermore, the limited scale of the campaign did not lend itself to bringing in a new generation of customers. For many merchants, it was regarded as a missed opportunity.

Chart 4

There was one clear and positive message that the campaign reinforced: attractively priced wines will find a market. The 2019s were actively traded post their release. A total of 63 distinct wines from the 2019 vintage were eventually traded on the market in 2020 following their release, while a mere 11 labels from the 2018 vintage were traded following theirs.

Chart 5

Nonetheless, the lingering question after the campaign was whether this signalled a new approach to En Primeur or was something of a one-off given the circumstances.

2020 campaign: Back on course?

The UGCB tried to strike a positive tone earlier this year by organising tastings in 10 cities in Europe, Asia and the US for late April. However, as it became clear that holding the UK and US legs would not be possible, they were cancelled. Europe’s vaccination programme has proved slow and trade shows such as Vinexposium and Vinitaly have now cancelled their planned June events. Nonetheless, the UGCB has confirmed (at the time of going to press) that its tastings in Bordeaux, Frankfurt, Brussels and Zurich are going ahead in late April.

The timely arrival of samples is vital to the assessment and pacing of this campaign. Initially, there were concerns that new laws surrounding imports might hamper samples arriving in the UK. However, some major critics have been posting pictures on their social media accounts of samples getting to them, and the UGCB likewise confirmed, on 12th April, the safe UK arrival of its sample kits destined for leading merchants and critics. It is certainly a more organised state of affairs than last year.

Nonetheless, although there are now indications the campaign will unfurl in its usual time slot, those hoping for a leisurely pace to releases may still be disappointed.

Campaign pacing: Rapid fire

Given the speed of recent past campaigns, the likelihood of the small 2020 vintage being sold into July is remote. Another rapid-fire campaign brings both positives and negatives. If there are some encouraging looking scores and opinions before the bulk of releases begin, allied with what look like attractive prices, then the speed and momentum can carry the 2020s home.

But fast campaigns also mean the focus will fall on a small group of releases that stand out most immediately from the pack. In the rough and tumble triage of a day’s releases, some labels will inevitably be left behind. Over the last few campaigns, merchants have already shown themselves to be much pickier, committing only to headline releases and the bankable workhorse labels.

What will prove frustrating, is if scores and prices are attractive, but the châteaux continue to withhold stock. Volumes will be tight as it is, and so the market is already looking at another bijou campaign with limited potential to do business and, importantly, develop the next generation of Bordeaux collectors.

Pricing variables

The potential impact of serious frost damage on the nascent 2021 crop is also an emerging factor here. At the time of writing the extent of the damage is unclear. It may be recalled, however, that bad frosts in 2017 on the eve of the 2016 campaign acted as a spur to estates to reduce stocks and increase their prices. And this was despite many of the classed growths suffering negligible frost damage.

Price increases are always a matter for debate. There has been some limited talk of 5% to even 20% increases on the 2019s. Sterling is somewhat stronger than it was versus the Euro in spring last year, which will soften the impact.

After the excitement of price cuts last year, the Bordelais will need positive views to justify price rises this year. But even positive scores should not be seen as a green light to race back to 2018 pricing levels. Especially when considering how finely balanced market sentiment towards Bordeaux currently is.

Relative vintage value

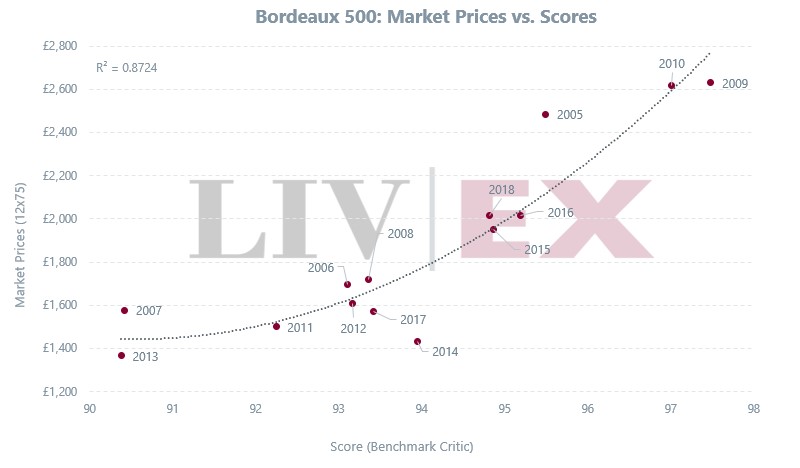

Critic scores help shape the Bordeaux market. Chart 6 looks at the average value over the past 12 physical vintages, comparing the average Market Price of the wines in the Bordeaux 500 index to their average Neal Martin score. Following Robert Parker’s retirement – the critic with the greatest influence on Bordeaux pricing (and style) – other Bordeaux critics such as Neal Martin, Lisa Perrotti-Brown MW, James Suckling, Jeb Dunnuck and Antonio Galloni have demonstrated their ability to move the market. Yet, according to a Liv-ex survey among its global merchant members, Neal Martin is the most trusted critic when it comes to Bordeaux En Primeur. The Liv-ex ‘Benchmark Critic’ uses Robert Parker’s scores for 2005-2012 and Martin’s score for vintages post 2013 from the Wine Advocate and, more recently, Vinous.

Chart 6

The supply chain

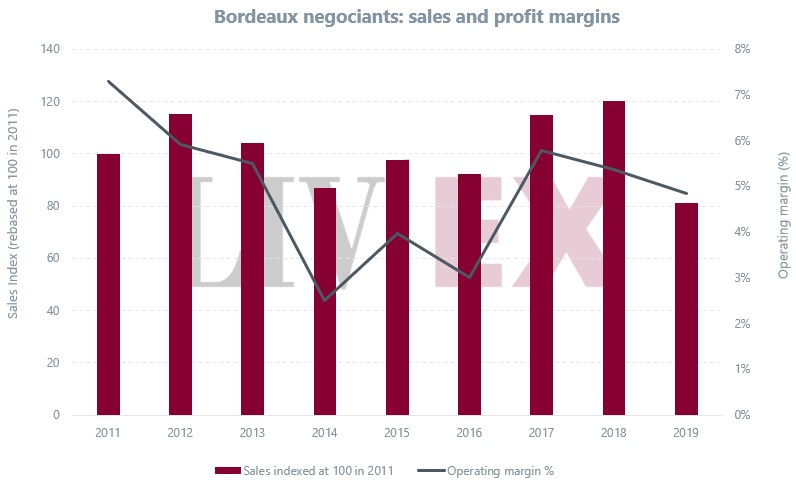

Charts 7 – 10 show the aggregated profit and loss and balance sheet data for the UK and Bordeaux trade.

In Bordeaux, after two strong years in 2017 and 2018, built on the back of high value sales of the 2015 and 2016 vintages, the poor performance of the 2017 vintage campaign will have been a disappointment. Improved sales of the 2018 and 2019 wines will likely prove a timely corrective although it is unlikely that the expensive 2018s will have done much to improve operating margins.

Chart 7

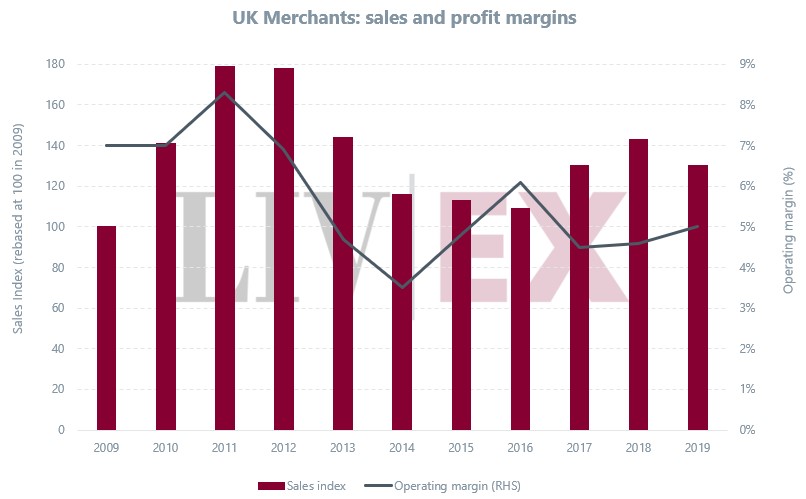

It is a very similar story for the UK as can be seen in Chart 8. The point made in last year’s report, however, about Bordeaux’s falling share of that total is even truer today. As Chart 11 will show, Bordeaux’s trade share continues to decline to new lows and En Primeur, while still important, is no longer the pivotal sales opportunity it once was.

Chart 8

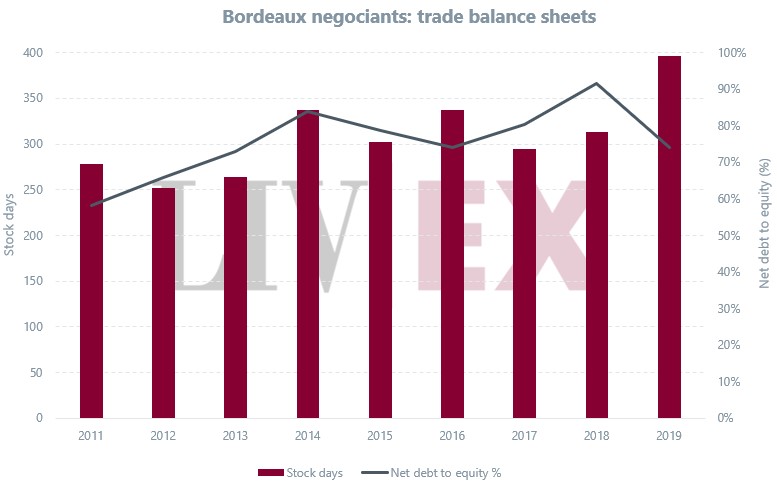

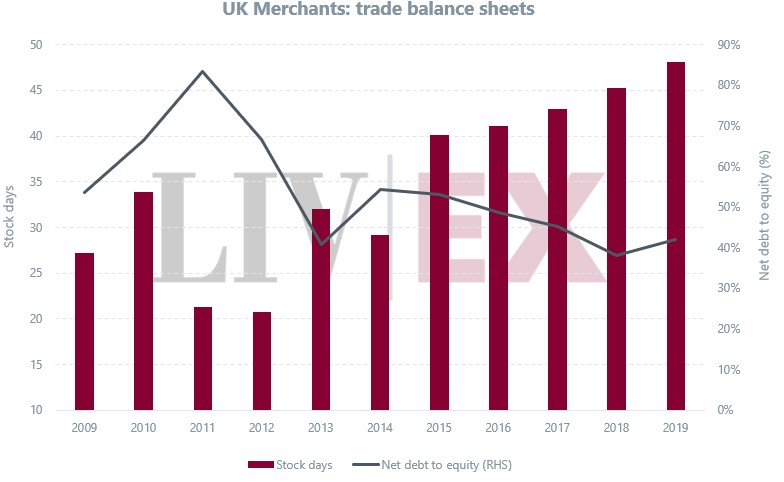

With a slight slowdown in sales in 2019, there has been a corresponding rise in stock days in both Bordeaux and the UK. This is unsurprising given the increasingly stressful market conditions that began to form in 2019 and it will be interesting to see how this changed in 2020 when the market sprang back into life in early summer.

The most striking statistic is that stock days in Bordeaux are now in excess of a year. UK merchants’ might have seen their stock days rise steadily since 2015 but their stock turnover is still six to eight times greater than their Bordelais counterparts. The fall in net debt, by contrast, would seem out of place in this scenario but may be an anomaly of timing. Unsold wines of the 2017 vintage becoming physical may be playing into the rising stock levels seen in 2019, while sales of the 2018s brought in a welcome cash windfall. Nonetheless, as unsold 2018s and the trickle of funds from the 2019s perhaps work to counteract one another in the 2020 figures, balance sheets in Bordeaux remain stretched.

Chart 9

With regards to rising stock days among UK merchants, it is rather harder to discern any one reason behind it. It is possible that while the figures show Bordeaux’s share of trade in the secondary market declining, some merchants may not have diversified their offering sufficiently, leaving them with rising stocks of slower selling claret. Others may have been unwilling to reduce margins in an increasingly competitive market, meaning stock lingers a little longer on their books.

Chart 10

The current state of the Bordeaux market

Market share

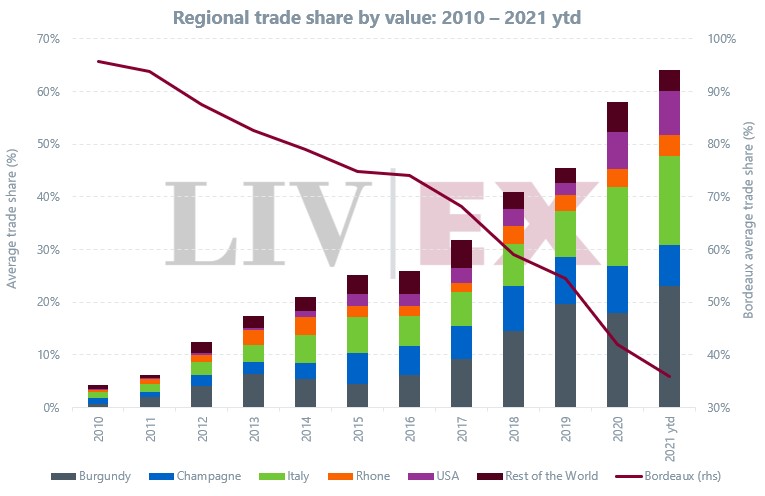

While still dominant, Bordeaux now accounts for a smaller part of the fine wine market than ever before. Its trade share by value has slipped from its height of 95.7% in 2010 to 36.8% year-to-date, in part due to the market’s continued broadening, as can be seen in Chart 11.

Back in 2010, 1,644 unique wines (LWIN11) traded on the exchange. Of that, 1,126 were Bordeaux (and predominantly First Growths). By 2020, the number of wines had increased 530% to 10,361. Of that, 2,827 wines came from Bordeaux, marking a 151% regional jump.

Bordeaux has also faced numerous headwinds. While Italy (16.8%) and Champagne (7.8%) benefited from being excluded from the 25% US tariffs throughout 2020, demand for most Bordeaux (wines below 14% ABV) fell, impacting the region’s market share.

Chart 11

The impact of the US tariffs and their suspension

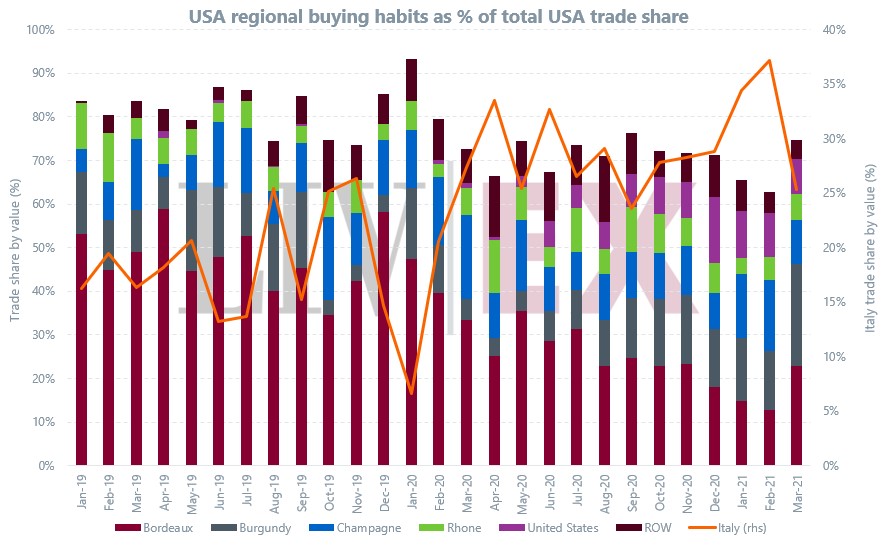

The 25% US tariffs, which came into effect on 18th October 2019, had an impact on demand, prices and regional market share. Before the tariffs were introduced, Bordeaux accounted for 48% of monthly trade by value on average (Jan 2019 – Oct 2019). Since October last year, Bordeaux’s average share of US buying has fallen to 30%. In February, before the tariffs were suspended, it hit a monthly low of 13% to then increase to 23% in March.

Where previously US buyers had focused on the tariff-free regions of Italy and Champagne, after the announcement, their eyes (and dollars) increasingly turned back to Bordeaux. This was also reflected in the value of live bids for Bordeaux, which went from 4% pre-announcement to 55% post-announcement.

With the renewed interest in Bordeaux, the region’s share of trade by value – driven by the First Growths – increased from 37.5% in February to 41.3% in early March – a step closer to pre-tariff levels. Although, as we have seen, this share of trade did not last.

Chart 12

Bordeaux buying appetite

While Bordeaux is showing signs of movement Stateside, how are things looking for other key markets?

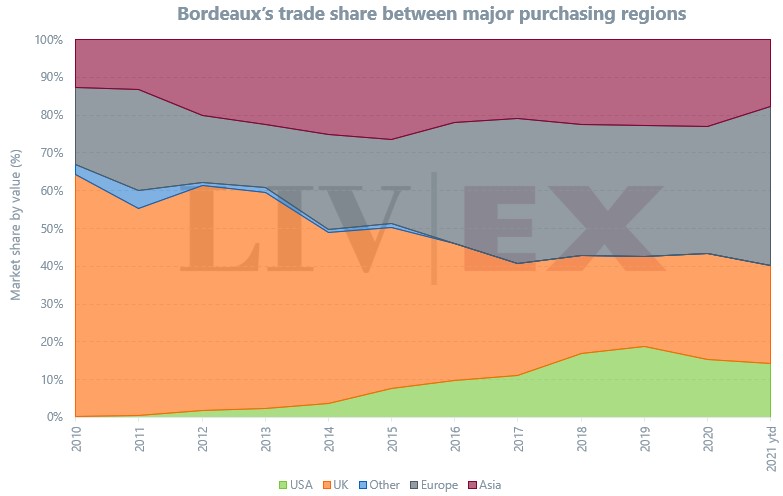

The UK – the oldest international market for Bordeaux and the biggest buyer of En Primeur wine – has been less active, with its share of trade by value falling from 64% in 2010 to 28% in 2020. In recent years, well stocked (Bordeaux) cellars and an increased interest in other regions that offer relative value for money, has led to falling demand. It remains to be seen how the UK market will react if post-Brexit burdens on European wine are imposed from 2022, but the postponement on introducing VI-1 forms this year has given some hope they can be done away with entirely.

Similarly, Asia – a long-time buyer of Bordeaux’s top brands – has regressed. In 2020, it took 23% of Bordeaux’s market share. European buying has taken up the slack (34% in 2020).

Chart 13

Inside Bordeaux’s trade share

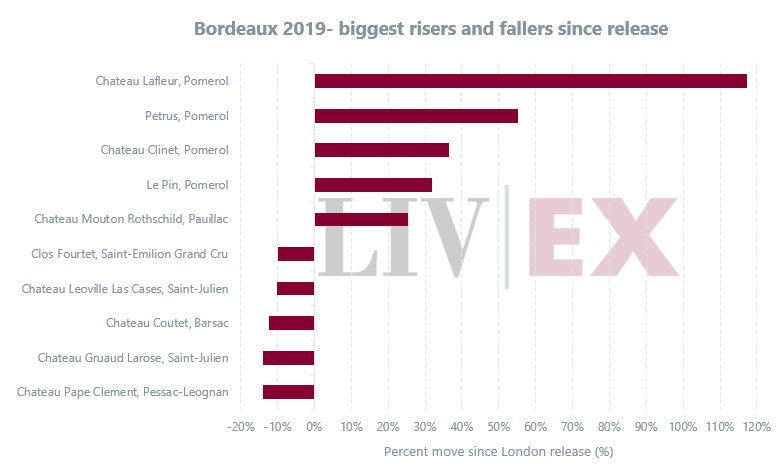

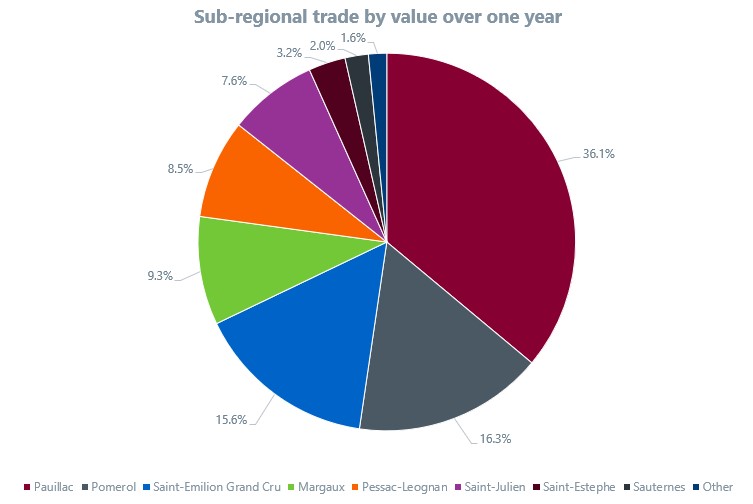

In the past year, the leading appellation by value trade has been Pauillac (36.1%), home to the First Growths Latour, Lafite Rothschild and Mouton Rothschild, and other highly active wines on the secondary market such as Pontet-Canet, Lynch-Bages and Duhart-Milon.

It has been followed by Pomerol (16.3%), the leading appellation on the Right Bank, where Petrus, Le Pin and Lafleur are produced. Saint Emilion Grand Cru (15.6%) and Margaux (9.3%) follow.

The ‘other’ category (1.6%) includes appellations less dominant on the secondary market such as Haut-Médoc, Médoc, Barsac, Fronsac, Graves and Bordeaux Supérieur.

Chart 14

Looking at vintage level trade, 2016 leads the way over the past 15 months. The critically acclaimed vintage has accounted for 11% of the Bordeaux market in this period, followed by the 2010 and 2009 at 10.4% each.

Lafite Rothschild continues to be the most active wine by value, with its 2016 at the very top of the rankings. But while the high-value First Growths dominate trade by value, the likes of Quinalt L’Enclos 2006 and Fonbel 2015 have seen high volume trade.

Bordeaux prices: calm waters

Bordeaux is the most important constituent of the Liv-ex benchmark indices, the Liv-ex Fine Wine 100 and the Liv-ex Fine Wine 1000, which are 53.9% and 42.3% weighted towards the region respectively.

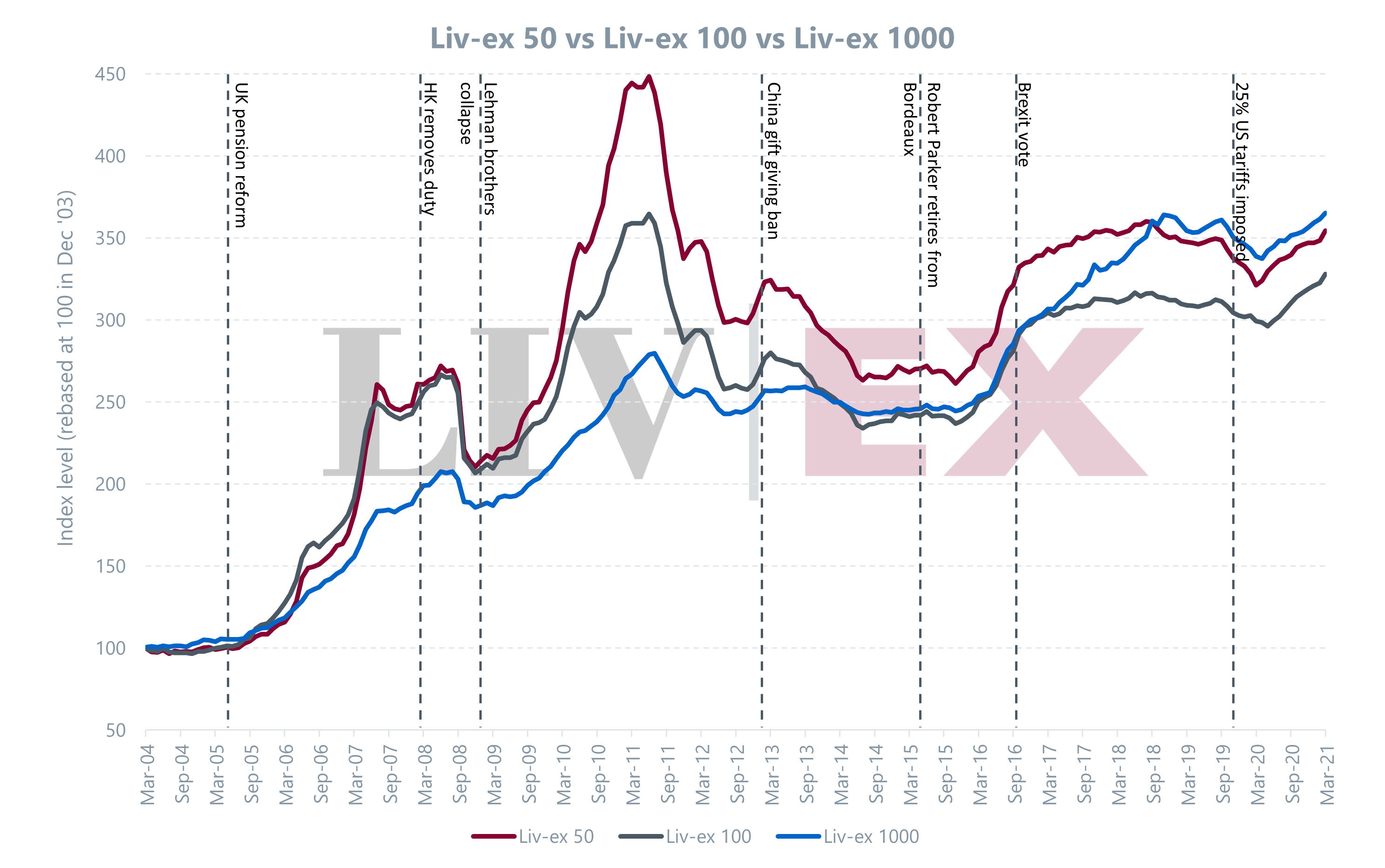

Chart 15 compares the performance of the Liv-ex 50, which tracks the daily movement of the Bordeaux First Growths, to the benchmark Liv-ex 100 and the broadest measure of the market, the Liv-ex 1000. It reveals Bordeaux’s general tendency to affect sentiment in the broader market.

Since its inception, the Liv-ex 50 has risen 254.4%, outperforming the Liv-ex 100, up 227.9% over the same period, but trailing the Liv-ex 1000 (265.1%), which had a strong run in 2018/2019 thanks to Burgundy’s rocketing prices. It is worth noting however, that the Liv-ex 50 remains well below the highs reached exactly ten years ago.

As the fine wine market’s dominant force, Bordeaux is the most sensitive to global events such as the collapse of the Lehman Brothers in 2008, which hit prices hard, and the Brexit vote in 2016, when Sterling weakness benefitted foreign buyers. (Liv-ex indices are denominated in Sterling).

Chart 15

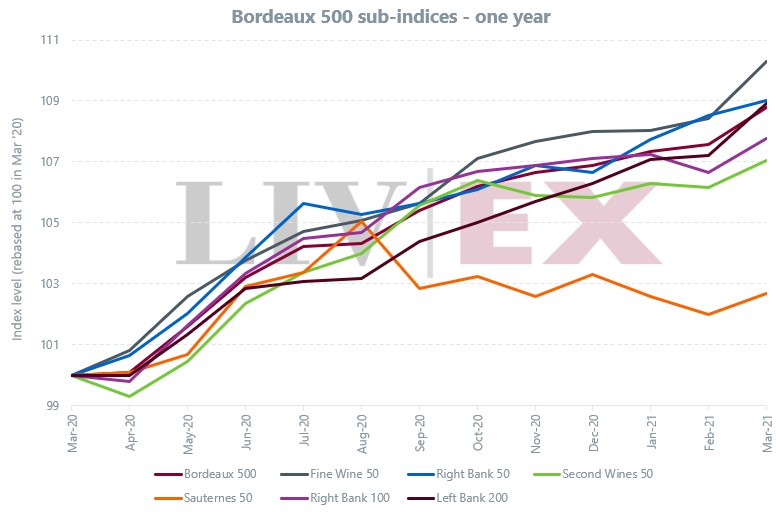

In the past year, the Bordeaux 500 index, which tracks the prices of the last 10 physical vintages of 50 leading producers, has risen 8.8%. It has been led by increases for ‘off’ vintages such as 2008, 2013 and 2012. As investment interest in Bordeaux has started to revive, prices for top vintages have also started to move – 2010 being a prime example.

Still, the Bordeaux 500 has been the third worst performing index over the past year, surpassing just the Burgundy 150 (7.8%) and the Rest of the World 60 (0.9%). The Champagne 50 (12.7%) and the Rhone 100 (9.9%) have been the biggest risers.

Chart 16

Chart 17

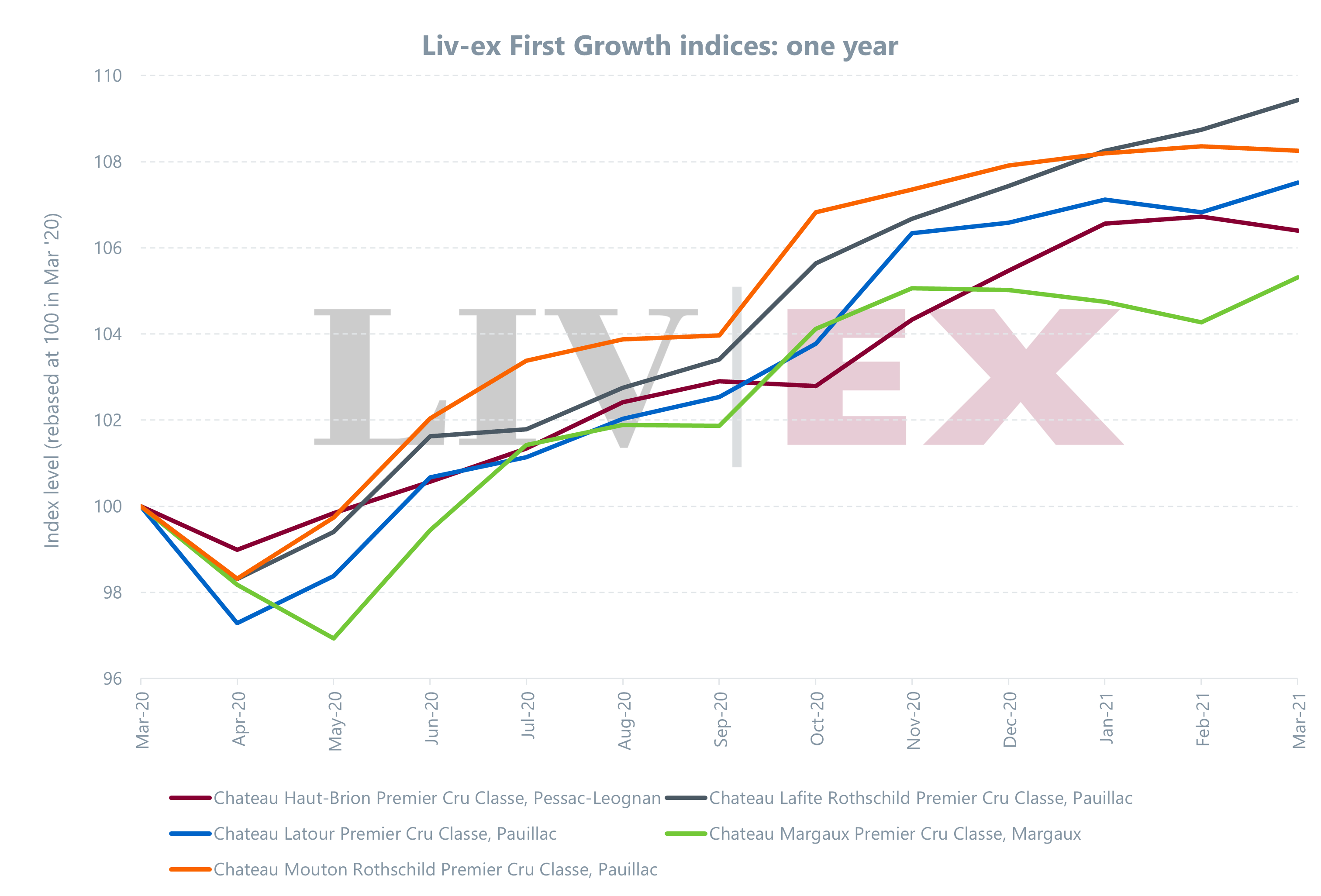

The First Growths have led from the front in the past year, with the Liv-ex 50 index up 10.3%. First Growth prices stumbled at the beginning of the pandemic in March 2020, to later recover following the successful 2019 En Primeur launch.

As can be seen in Chart 18, the First Growths have been led by Lafite Rothschild (9.4%), with Mouton Rothschild following suit (8.3%). Latour, which famously exited the En Primeur system after the 2011 vintage and recently released its 2013 vintage, is up 7.5%. Haut Brion has risen 6.4%, with Margaux being the slowest mover of late, up 5.3%.

Year-to-date, the First Growths have made up 30.9% of Bordeaux value trade on the secondary market.

Chart 18

Conclusion

As with all En Primeur campaigns, there are a lot of moving parts. In their favour, the Bordelais have an audience looking for distraction (though less so in the UK as lockdown eases and pubs open!), who are currently in the mood for buying fine wine. Last year’s campaign proved that the flame for buying Bordeaux futures is still flickering, while remote tastings and campaigns have become somewhat second nature to the trade and their clients.

Yet since last year’s campaign the market has broadened noticeably, and Bordeaux’s weekly and monthly share of trade has continued to decline. There is also a distinct lack of novelty to the current situation. The 2019 campaign, unfurling at a gallop, ended up pulling off a Buster Keaton-esque escape in challenging circumstances. A year ago, there was a galvanising energy to proceedings as businesses adapted in the face of an evolving situation. It’s doubtful the same feeling is still there, and old cynicisms will be back in play.

Last year in the concluding section of our En Primeur report, it was noted that it would be a “bold move indeed” if châteaux were to release their wines without critical backing, and it would require “eye-catching prices” if they were to do so. In the event, this did happen, with some releases in late May and early June, well ahead of many major critics’ reports which didn’t emerge until mid to late June. But many worked because their price cuts were suitably tempting.

It is hard to imagine the 2020 wines being able to pull off the same trick as the 2019s if they are going to be more expensive. First, opinion on the 2020 vintage at this early stage is unclear and few seem to know what to expect. Second, over-reaching price rises will likely kill off any lingering hopes that last year’s campaign signalled a ‘new direction’ for En Primeur. Fortunately, with key critics indicating at this stage that their reports will be ready for May, the first issue should be neatly resolved, giving all parts of the chain time to consider how to approach the crucial second part.

In order to keep buyers engaged this campaign, the Bordelais cannot afford to put a foot wrong. While market sentiment towards Bordeaux is showing signs of a recovery, it is tentative. There are still a great many wines from vintages that are known quantities – from good to outstanding – available at discounts to their initial release prices. While Sterling’s recent strength gives some room for manoeuvre, the Dollar’s weakness does the opposite. Wines will have to be cleverly and thoughtfully positioned. Even when a better understanding of the vintage’s qualities has been formed, keeping prices within orbit of the much-admired 2019s would seem to be the logical step.

The danger for estates in recent campaigns has been getting lost in the crowd of releases. To ensure the 2020 vintage not lost in an increasingly crowded fine wine market the Bordelais must make it stand out.

Liv-ex will be analysing and publishing Bordeaux analyses in the run up to and throughout the upcoming 2020 En Primeur campaign. For instant email alerts, subscribe below.