Print and read offline instead.

- The 2021 vintage was the coolest and second wettest Bordeaux vintage of the last decade.

- Market conditions have been very favourable over the past two years, but storm clouds are gathering.

- The French and UK trade are seeing slower stock turn.

- Competition from other regions continues to impact Bordeaux’s share of secondary market trade.

- Producers are making conscious efforts to reverse the trend, but pricing will be the key determinant to the success of the forthcoming campaign.

Introduction

It is striking that for a fine wine region so endlessly picked over and dissected as Bordeaux, there is always something new to discuss.

Each year of course brings a new vintage. A fresh set of weather patterns brings speculation over which appellations or estates have performed better than their peers. What will the wines be like? How will they be priced?

The first part of this report will consider the 2021 growing season. Using weather data provided by Saturnalia, the first impression is of a cool and relatively wet vintage after the warm 2018-2020 run, which suggests wines more akin to the 2014 or 2017 vintage.

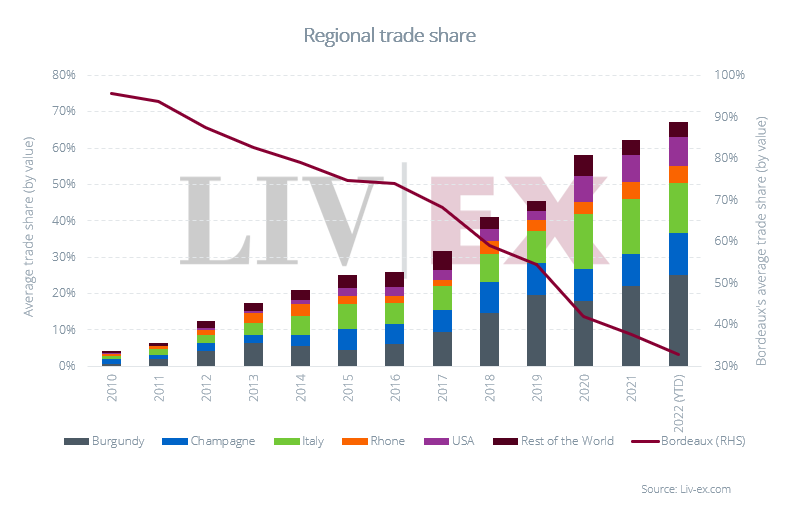

In the second part of the report we turn to the current market for Bordeaux. With every passing year the secondary market broadens, challenging Bordeaux’s dominance. Year to date, the region’s market share is holding just above 30%, an historically low level.

Burgundy and Champagne are on the rise but offer something stylistically different to Bordeaux. The real challenge comes from the growing market for Tuscan and Californian wines. Both regions are beginning to offer more attractive returns than their Bordeaux counterparts, which in turn creates greater interest.

We examine how Bordeaux is evolving its offering in the face of this competition. Stock is lingering longer in the supply chain, narrowing margins for merchants in Bordeaux and beyond. While inflationary pressures are adding to the cost base of growers, sentiment toward this year’s En Primeur campaign is seemingly luke-warm, suggesting that this is not a vintage that will in any way benefit from an ambitious pricing strategy.

Weather overview in 2021

Over the last decade, Bordeaux has been lucky with its run of vintages. Although the region has experienced its share of frosts, hailstorms, droughts and drenchings, only the 2013 and 2017 vintages stand out as having delivered, comparatively speaking, indifferent wines.

Overall, the general pattern has been a run of three good to extremely good vintages punctuated by a true ‘off’ vintage. The 2013 was followed by 2014-2016 for example, which gave way to a low in 2017 and then a renewed run from 2018-2020 and now perhaps 2021.

Before the wines have been properly assessed (UGC tastings begin next week) it would be folly to make any definitive assessment of the vintage. But the reports from Bordeaux at the end of last year and so far in 2022, as well as an examination of the growing season, do not give the impression that 2021 will match its immediate predecessors in quality.

A cool wet vintage

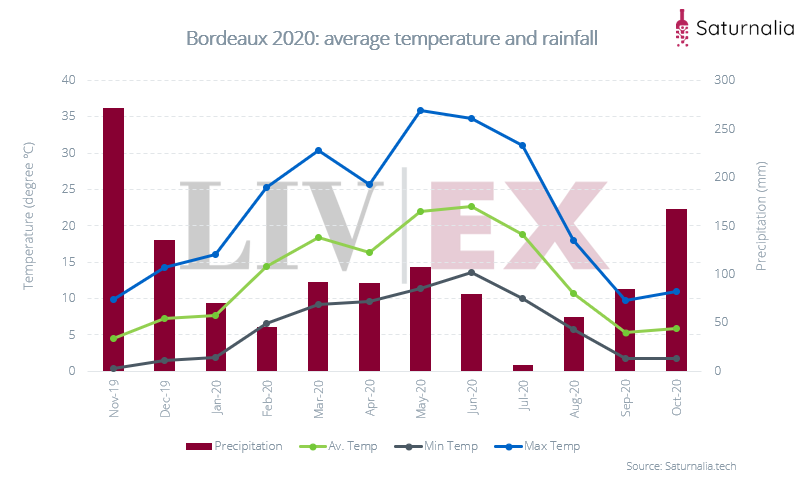

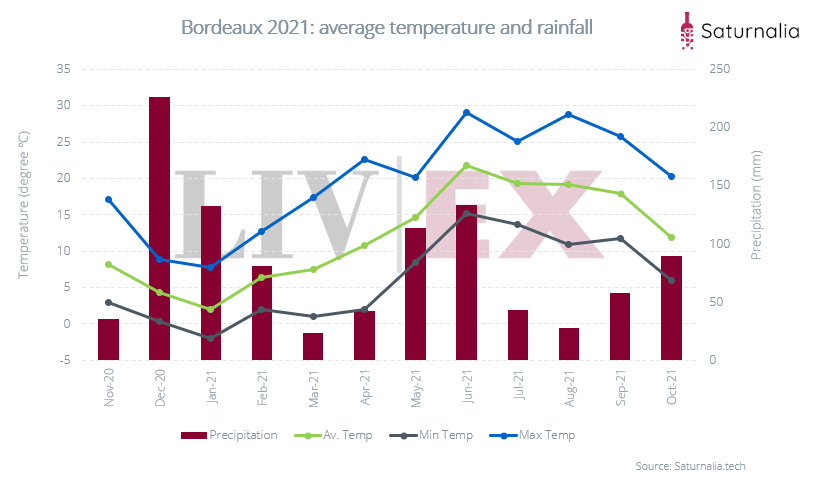

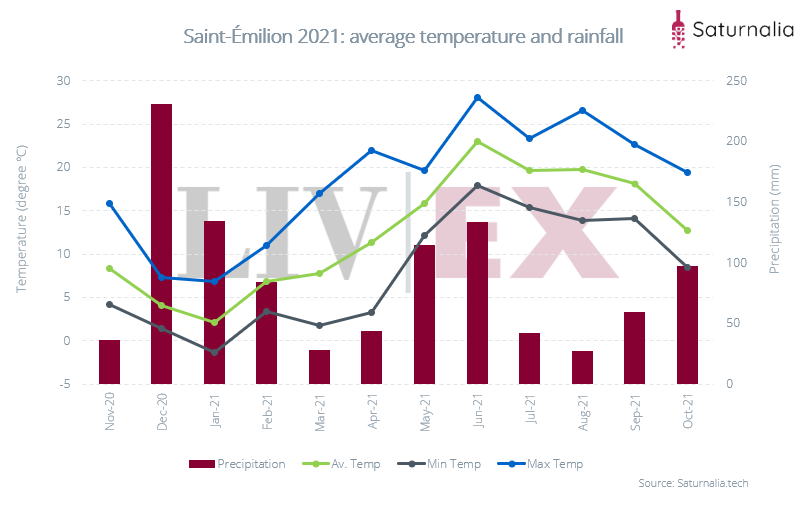

Weather data from Saturnalia shows that 2021 was a cool and wet vintage overall. In total 1,182mm of rain fell on Bordeaux last year between November 2020 to October 2021 (the growing season), an average of 83.9mm a month.

This is slightly less than the total rainfall in 2020 (1,244mm in total) but as Saturnalia explained in its own vintage report, the problem is not the volume of rain per se, but its concentration.

During the 2020 growing season (see chart below), there was only one month during the flowering and ripening period where rainfall exceeded 100mm – that was in May.

Compare this with 2021 in the chart below. Bordeaux was largely spared the crushing frosts that struck other French regions in April 2021 but its fortune did not last long. Here we can clearly see how wet it was in that crucial May-June period, when both months recorded well over 100mm of rain.

This heavy rainfall also coincided with the year’s warmest spell. The Saturnalia data has June as the warmest month overall at 21.8˚C on average (though this is cooler than the normal average for June) as well as the wettest, with 133mm of precipitation. The majority of the June rain also fell in the last two weeks of the month, just as it did in 2017.

Early reports of severe mildew and botrytis make sense in light of this, given the ideal conditions for rot that wet and warm weather create.

Rainfall dropped off sharply for July and August, but temperatures also dipped slightly on average. There is certainly no indication that there was a summer drought in 2021 with temperatures regularly exceeding 30˚C as there was in 2020. A cool and wet year, therefore, bringing to mind conditions in 2014 and 2017.

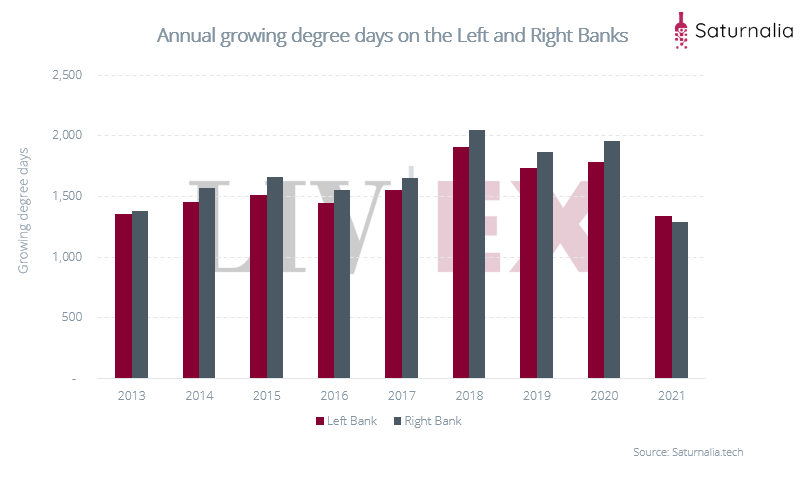

Saturnalia also tracks ‘Growing Degree Days’ (GDD), which is the amount of heat the vines receive during the season to support growth and development.

As can be seen in the chart below, 2021 had the lowest GDD of any vintage on either the Left or Right Bank since 2013.

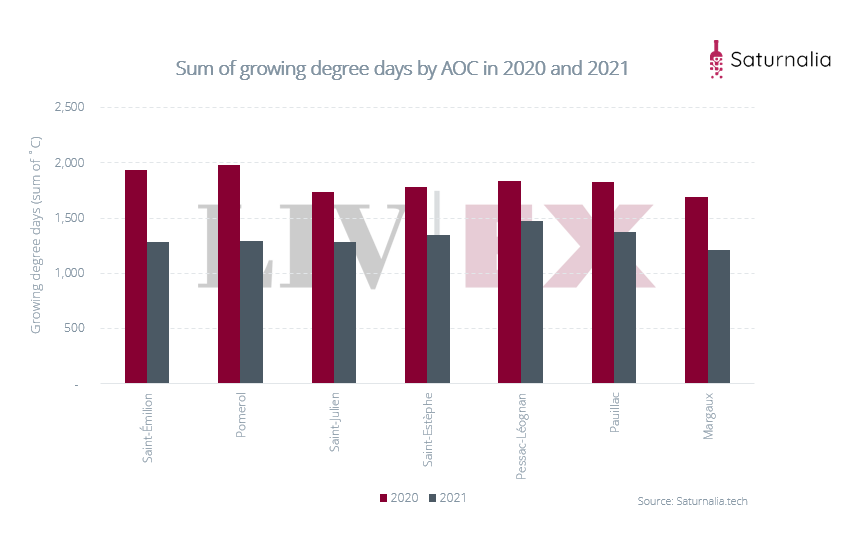

The sum of GDD in ˚C across the key appellations was also less in 2021 than in 2020, adding to the evidence of how much cooler this vintage was, which will in turn have had an effect on ripeness and maturation levels.

The Left Bank

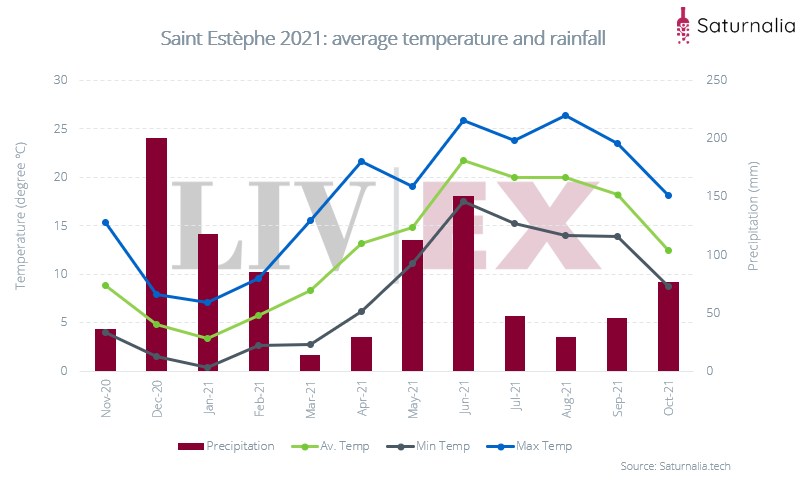

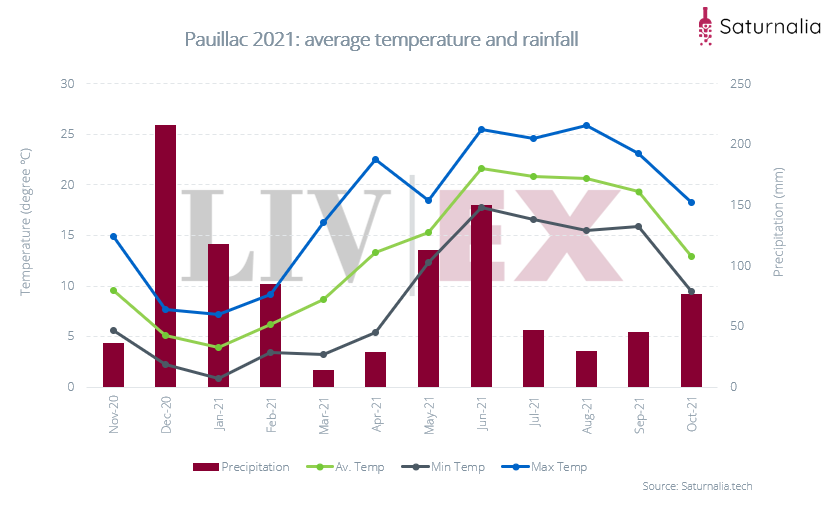

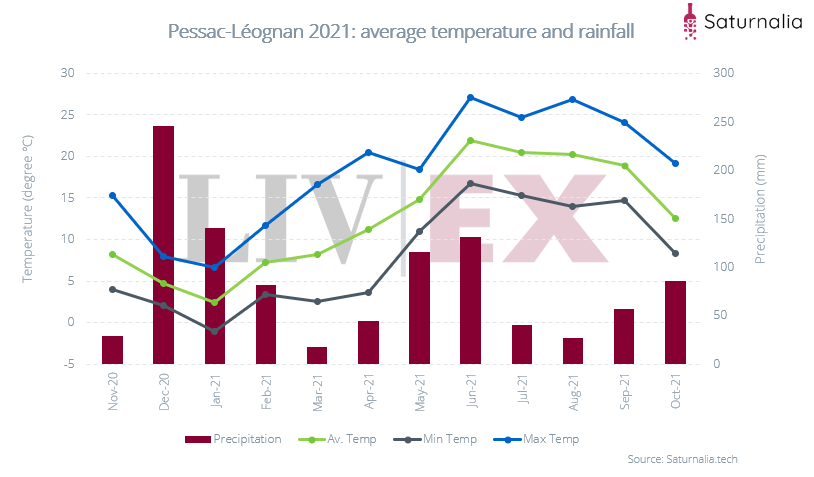

It is important to look at each appellation in detail. It is well known that, given the size of Bordeaux, there can be subtle or stark contrasts between weather conditions in neighbouring as well as far-flung communes every year. On the Left Bank, some of the vagaries of the 2021 vintage’s weather are clear.

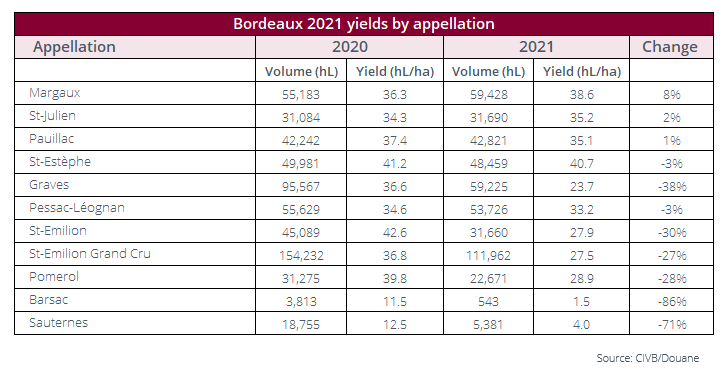

For example, both Saint-Estèphe and Pauillac suffered the wettest June, with 150mm of rain falling in both appellations. However, overall, they were among the least-wet AOCs with Saint-Estèphe receiving 946mm overall and Pauillac 960mm.

Meanwhile, further south, Pessac-Léognan was the wettest of the Left Bank appellations, with 1,015mm of rain falling in total. Yet it also experienced the least rainfall in June – 131mm.

And although it had higher rainfall, Pessac also had warmer temperatures and more cumulative growing degree days than Saint-Estèphe or Pauillac. Warmer and wetter is of course a recipe for rot but the final yields show that it did not fare much worse than in 2020, with a 3% decline in yields, which was the same as Saint-Estèphe.

Ultimately, no appellation really ‘escaped’ the poor weather and the difference in average temperature and rainfall across the Left Bank appellations was not great in general. Small mercies such as low precipitation in June were often countered by higher rainfall elsewhere. Similarly, a greater number of GDD did not mean higher temperatures.

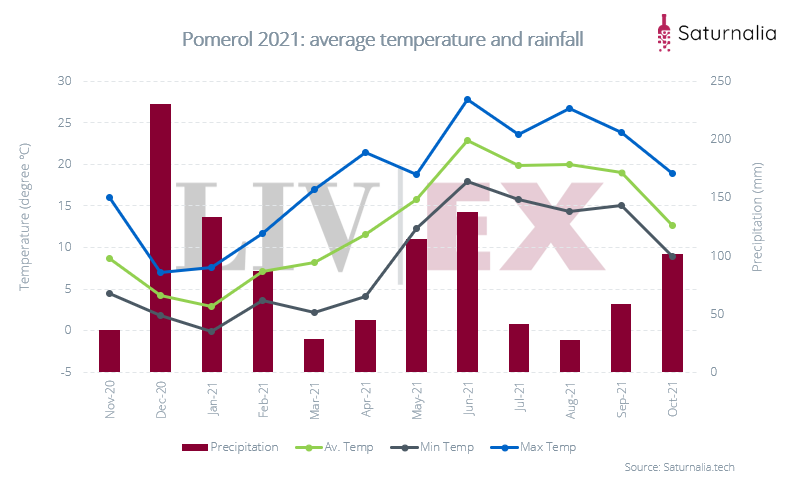

The Right Bank

As the charts showing GDD illustrate, over on the Right Bank it was a different story yet again. For the first time in almost 10 years, it was actually the Left Bank that enjoyed the greater number of growing degree days.

Both Saint-Emilion and Pomerol were wetter overall than any on the Left Bank, but temperatures were broadly the same on average. Pomerol suffered the highest rainfall, 1,042mm in total – 137mm in June.

Saint-Emilion was not especially drier, 1,031mm in total, 133mm in June.

As is always the case in tricky vintages, site and position will be an extremely important factor for wine quality. Estates on higher ground, with better-drained soils may have fared drastically differently to their near-neighbours. How the Right Bank estates on the high plateau fared versus others will no doubt be a key talking point.

Crop size

As mentioned, the warmer temperatures and high rainfall in May and June led to high disease pressure and this has contributed to some severe losses in overall yields.

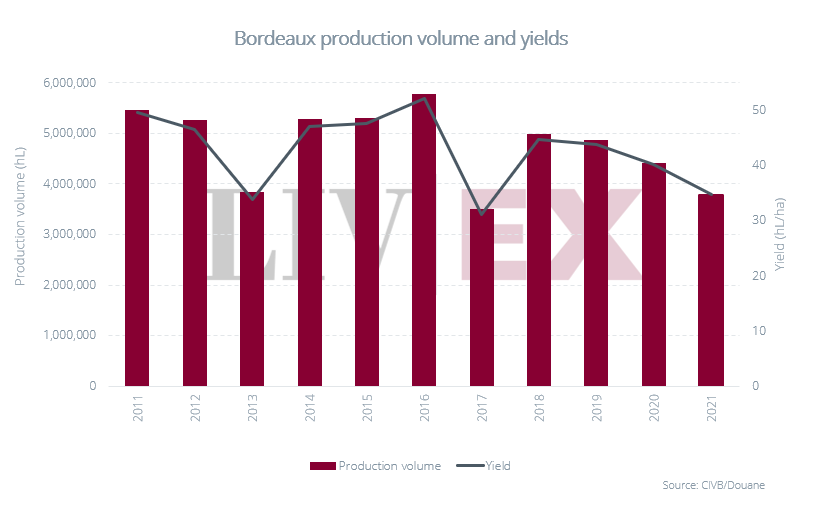

As the chart below shows, the 2021 vintage is the latest in a declining series of vintages since 2018. It is in fact very slightly smaller than the 2013 vintage; 3.7 million hectolitres to 2013’s 3.8m hl, though it is still larger than 2017.

The 2021 total yield was also 14% lower than 2020’s crop of 4.4m hectolitres. But, this is not to say yields were down universally on 2020 – it is important to remember that problems with mildew and drought in 2020 led to some low yields across the appellations.

Saint-Julien and Margaux for example both experienced lower than average yields in 2020. Despite the difficulties of the 2021 growing season, both appellations enjoyed increased yields again, with Margaux up 8% (see table below).

Nonetheless, most appellations in 2021 did experience losses and yields are down across the key AOCs on both banks. The sweet wine AOCs of Sauternes and Barsac have suffered particularly heavily.

The figures from the CIVB show that the white wine crop for both dry and sweet wines was significantly down on 2020; by 15% for dry whites (Graves showing the biggest drop, down 53%) and by 57% for sweet wines.

Vintage summary

The picture that emerges is of a small, heterogenous vintage, with what are likely to be substantial peaks and troughs in quality from appellation to appellation and estate to estate.

A difficult and heterogenous vintage does not automatically equate to universally poor wines. This is especially true of a region such as Bordeaux, where investment in winemaking equipment and extremely sophisticated levels of viticultural knowledge and expertise has greatly softened the bumps that come with awkward growing seasons.

Looked at through a glass half full and on the basis of available data, one might say that the best wines will offer 2014 and the better-end-of-2017 levels of quality, with coolness and leafy freshness, that are good for early drinking.

A less generous outlook suggests there will also be wines reflecting the worst traits of vintages such as 2011, 2013 or 2017, which is to say lacking body and ripeness with hard tannins.

Bordeaux’s reaction to the changing secondary market

Bordeaux’s secondary market is changing

Bordeaux remains the fine wine market’s most prominent player. Precisely because of its exposure, it is often the first to bear the impact of economic and political headwinds which have not been lacking lately.

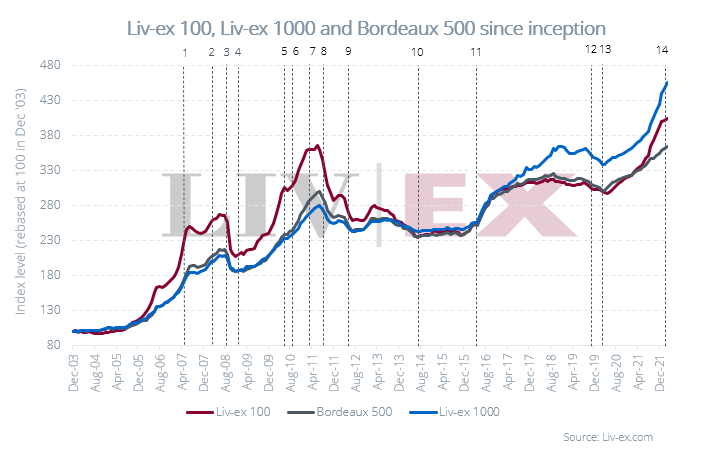

Bordeaux has been through many cycles in its secondary market history: decline following the 2008 financial crisis, peak and subsequent fall during the China-led bull run in 2010/2011, slow signs of recovery after the 2016 Brexit referendum when US and Asian buyers took advantage of sterling’s weakness. At the start of the Covid-19 pandemic, the Bordeaux 500 index dipped 1.6%, but quickly made up for its losses. This past quarter, upon Russia’s invasion of Ukraine, the region has been rising but by considerably less than the broader market.

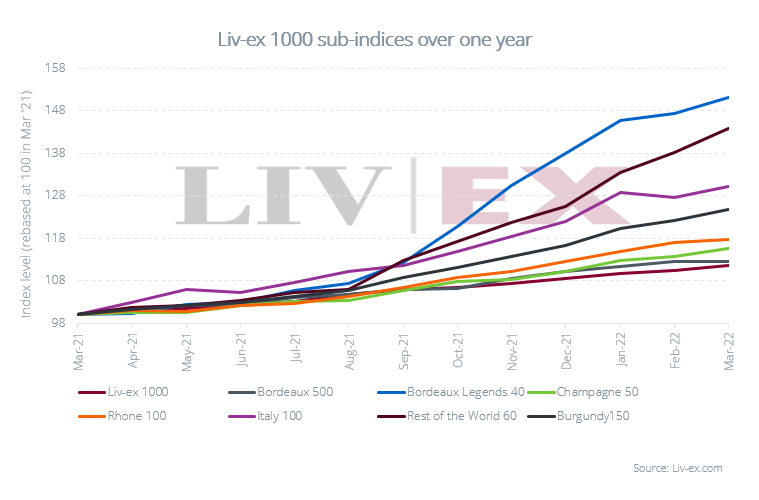

The Liv-ex 1000 index, which represents the price performance of a broader pool of wines, has delivered the best returns since its inception. The broadest measure of the market, which is less reliant on Bordeaux, is up 355.2%, compared with 304.0% for the Liv-ex 100 and 263.9% for the Bordeaux 500.

Timeline of key events:

- July 2007: Hong Kong cuts duty from 80% to 40%.

- March 2008: Hong Kong cuts duty to 0%.

- September 2008: Lehman Brothers files for bankruptcy, signalling the start of the financial crisis.

- November 2008: China announces economic stimulus programmes: 4 trillion yuan of investments in areas such as infrastructure, transport, industry, tax cuts and finance. Chinese interest in fine wine, a popular gift among officials, steadily increases.

- June 2010: The Bordeaux 2009 vintage is released En Primeur at all-time high prices.

- October 2010: China’s economic stimulus package was a success and purchases of luxury goods in the country were booming.

- May 2011: The Bordeaux 2010 vintage is offered for sale at new record prices, testing the strength of the market.

- August 2011: The fine wine market peaks before experiencing a downturn in prices.

- July 2012: China announces a crack-down on gift-giving of luxury goods among government officials.

- July 2014: The market hits its lowest point since before the China-led boom.

- June 2016: Sterling weakens following the UK’s ‘Brexit’ vote. This provides a boost to the market as stock held in the UK is effectively discounted to overseas buyers.

- October 2019: Following disputes over the World Trade Organisation’s ruling on the Airbus/Boeing dispute, the US introduces 25% tariffs on European goods, including wine. Regions exempt from the tariffs saw the biggest price appreciation in 2020.

- March 2020: Donald Trump declares Covid-19 a national emergency. Europe goes into lockdown.

- February 2022: After months of military build-up by Russia and diplomatic efforts by Western leaders, Russia invades Ukraine.

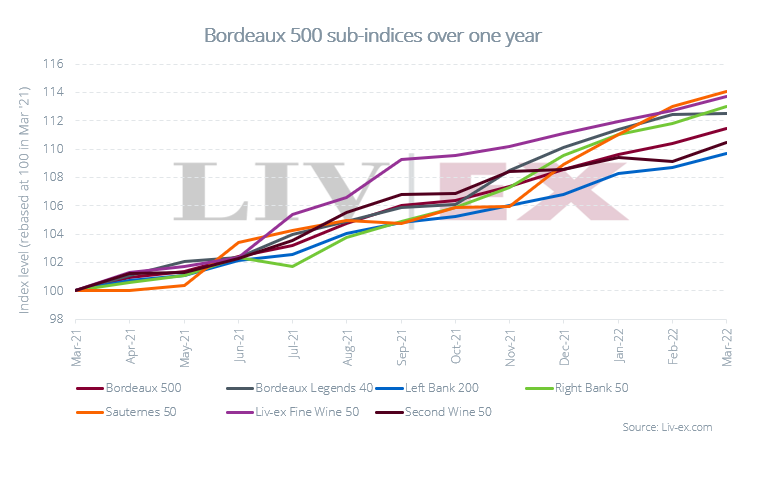

Within Bordeaux, Sauternes (14.1%) and the First Growths (13.7%) have enjoyed the biggest increases over the past year. The Left Bank 200 sub-index has risen the least, up 9.7%.

Growing competition in the secondary market

Bordeaux is facing growing competition from other regions.

The most serious contestant is Burgundy, which has surpassed Bordeaux both in terms of its price performance and the number of different wines traded. In recent weeks, the region has also been taking a similar share of the market to Bordeaux – even surpassing it on some occasions.

Over the past year, Bordeaux has risen less than other Liv-ex 1000 sub-indices; just 11.5% versus a staggering 51.2% for Champagne and 43.8% for Burgundy.

Tuscany and California named biggest competitors by merchants

While Burgundy and Champagne top the price performance charts, they produce stylistically different wines to Bordeaux so direct comparison is somewhat unfair. When polled by Liv-ex, most merchants named Tuscany and California, which produce Bordeaux-style blends, as Bordeaux’s strongest competitors.

On the secondary market, the Super Tuscans attract consistent levels of demand and are among the most liquid group of wines together with the Bordeaux First Growths.

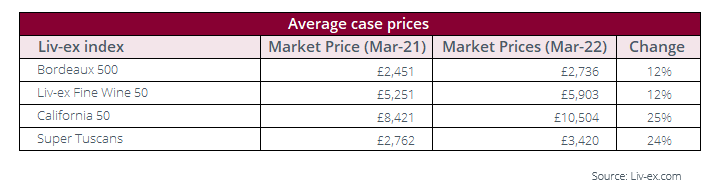

When it comes to California, the region has enjoyed a rapid rise in recent years, both in terms of price performance and market share. The California 50 index has risen 34.0% over the past year, compared to 13.5% for the Fine Wine 50 index, which tracks the performance of the First Growths, and 11.5% for the Bordeaux 500.

As the table below shows, the average Market Price for a case of Super Tuscans and the top Californian wines has increased more than the top wines of Bordeaux.

The Super Tuscans continue to offer a lower point of entry into the fine wine market versus the First Growths, perhaps explaining their greater return on investment in recent years.

The prices shown in the table above are Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. It is always presented for a 12×75 case unless otherwise stated. To calculate the Market Price, we look at list prices from a large group of trusted international merchants. Preference is given to prices from stock holders over brokers, to cases over single bottles, and to recent prices over older prices. The algorithm behind it runs every day, evaluating a pool of over 1 billion data points to determine the most accurate Market Prices for 240,000+ wines.

Bordeaux’s secondary market expansion stalls

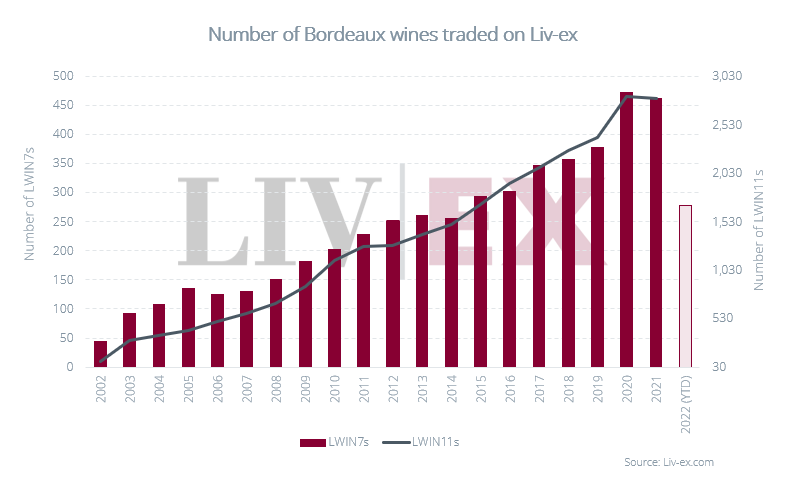

While Tuscany and California have seen steady increase in the number of wines trading each year, Bordeaux’s broadening has paused.

The number of unique Bordeaux wines traded (LWIN11s) declined 0.8% in 2021 compared to 2020. 10 fewer estates (LWIN7s) traded than in 2020, as well.

The number of Bordeaux wines traded on Liv-ex is calculated by counting the number of LWINs trading (both LWIN7s and LWIN11s). LWIN (The Liv-ex Wine Identification Number) is the universal identifier for wine and spirits. It assigns unique codes to over 110,000 different wines and spirits. It’s a lot like ISBN for books. Each wine or spirit has a unique number and display name which can be shared automatically. By counting numbers rather than names, errors are reduced and reporting is simplified.

Bordeaux’s place in a broadening market

The halt in Bordeaux’s expansion has made it even more difficult for the region to compete in a broadening market.

As the market’s overall trade value climbs, Bordeaux has been struggling to retain its share. Furthermore, its decline has also been in terms of absolute trade value, which remains well below the 2010 peak.

In 2021, Bordeaux’s trade share fell under 40% for the first time – 37.7%, and at the time of writing, it stands at just 32.0%.

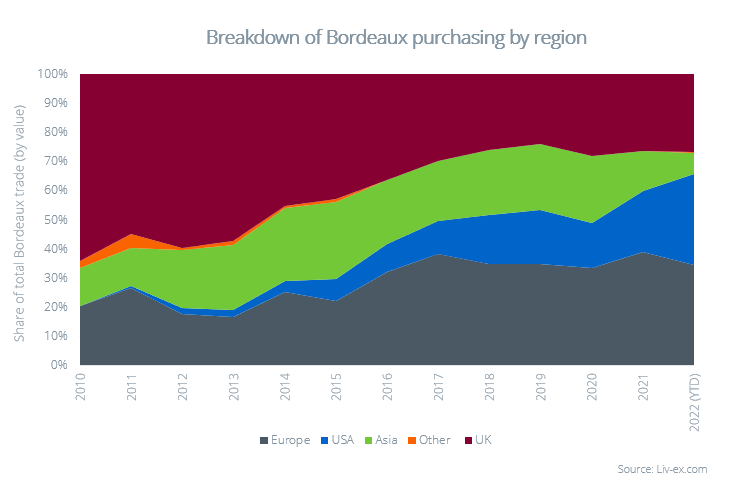

Bordeaux’s main markets

There has been a shift in Bordeaux’s main purchasing markets. Demand used to be UK-led but today it is more evenly split between other players. So far this year, Europe (35%) leads, followed by the USA (31%), which is an increasingly important player since the removal of the 25% tariffs on French wines last year. The UK accounted for 27%, while Asia slipped to just 7%.

Changing sentiment around En Primeur

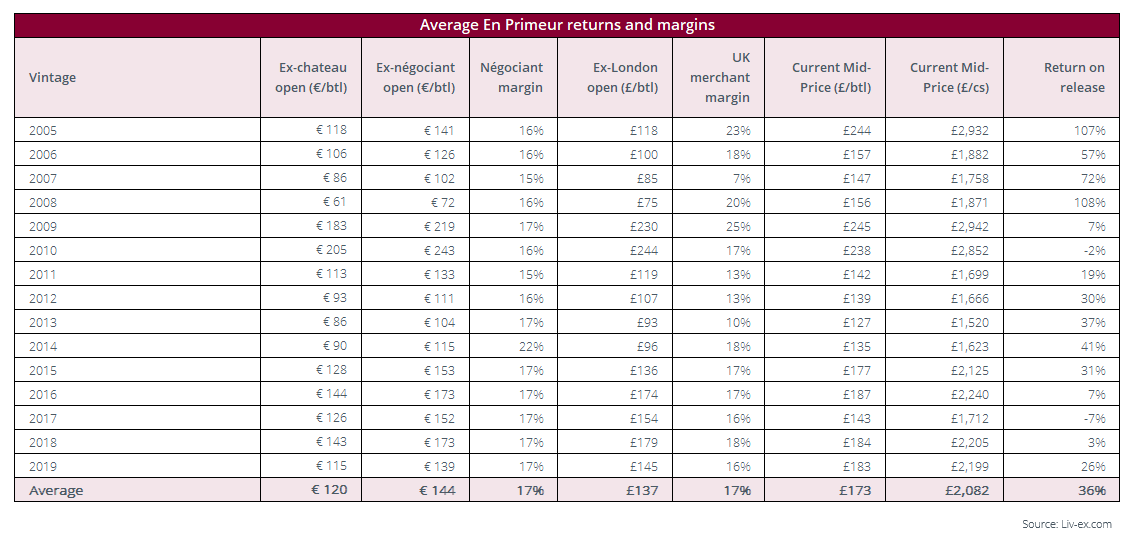

The appeal of buying Bordeaux En Primeur has been challenged by the returns on investment in recent years.

For instance, the average price of the 2010 vintage, offered at record levels during the China-led bull run in 2011, had declined 11% by the time the vintage became physically available two years later. Just over a decade later, the wines from this storied vintage remain, on average, 2% below their En Primeur release.

Another example is the 2017, considered an ‘off’ vintage and released at a high price after the expensive 2016s. The wines are still 7% cheaper on average than they were on release.

There have also been vintages that have largely run flat. ‘On’ vintages like 2009 and 2016 have risen just 7%, with many wines still available around their release prices. The 2018 vintage is up just 3% since release. When storage and other logistics costs are factored in, these small returns turn negative.

To calculate the average margins, Liv-ex first calculated the average ex-château, ex-négociant, ex-London and current Mid-Prices of the wines in the Bordeaux 500 index and split them by vintage. Allocation-only wines Lafleur, La Fleur-Pétrus, Petrus and Le Pin were excluded from the calculation. The margin was estimated based on the difference between the price at each point of delivery. The Mid-Price is the mid-point between the highest live bid and lowest live offer on the market. These are the firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 600 of the world’s leading fine wine merchants. Because Liv-ex doesn’t itself trade, this data is truly independent and reliable. Prices given are for 12x75cl trades, or 6x75cl converted to a 12x75cl price.

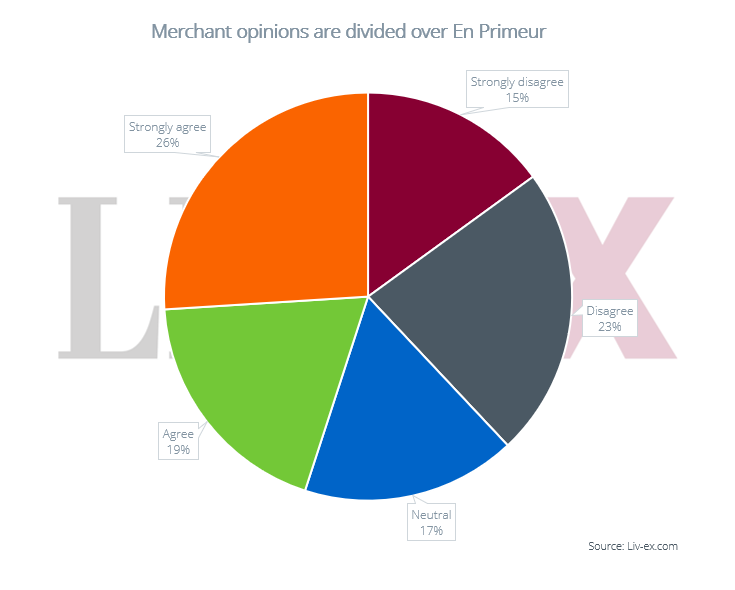

According to a 2020 Liv-ex survey, merchant opinion was divided over the significance of En Primeur. Of the respondents, 38% disagreed that it is the most important buying event of the year; another 17% were neutral.

In a survey, Liv-ex members were asked to what extent did they agree with the following statement? ‘Bordeaux En Primeur remains the most important buying event of the year’.

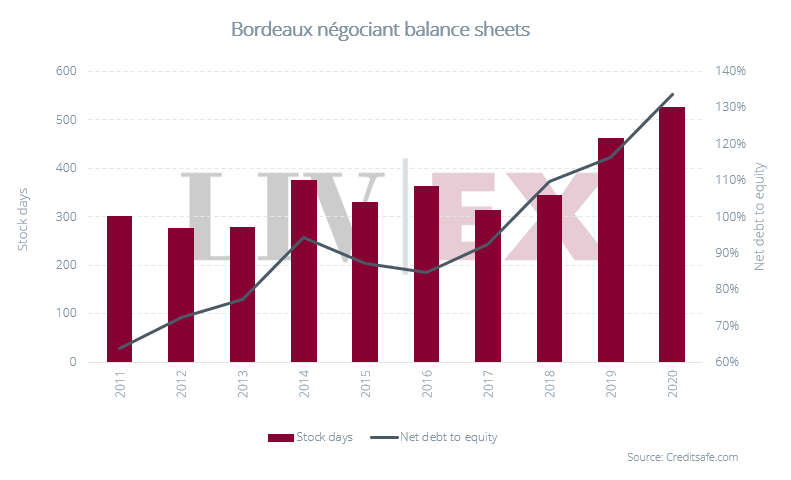

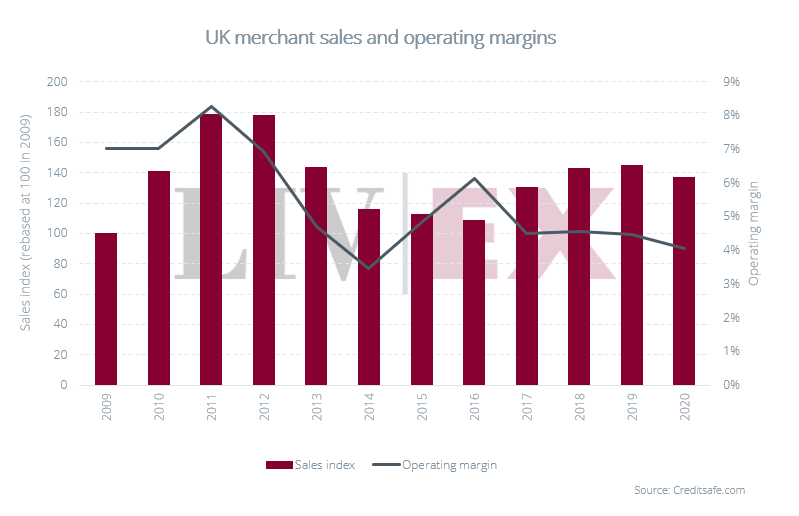

Underlying pressures on balance sheets

As last year’s report pointed out, wine has been slower to sell, with rising stock days among Bordeaux’s leading négociants. The chart below shows, balance sheets in Bordeaux were stretched further in 2020 (latest figures available).

Stock days in Bordeaux were well in excess of a year. Net debt to equity ratios have also been rising, indicating that a higher percentage of stock is being financed through debt.

As the costs associated with storing wine continue to rise, négociants are likely to face further margin pressures going forward.

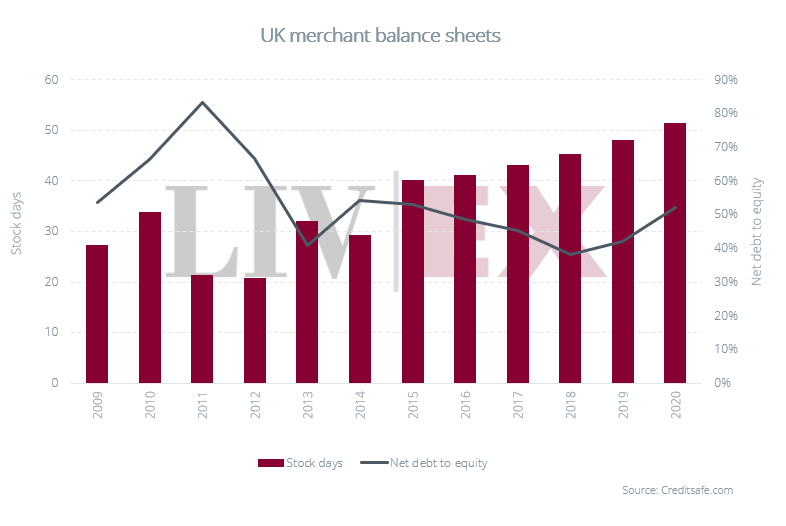

By comparison, the picture is brighter in the UK (again data for year 2020), with headline numbers pointing to far quicker stock turn and minimal debt financing.

Balance sheets look healthy for now, but stock days are creeping up and operating margins are trending gradually downwards. With the world facing a period of sustained inflation, and central banks indicating several rate rises to come, UK merchants are likely to be increasingly cautious.

*Net debt to equity figures in this graph for UK Merchants are negative ratios. i.e. Cash is increasing / debt is decreasing.

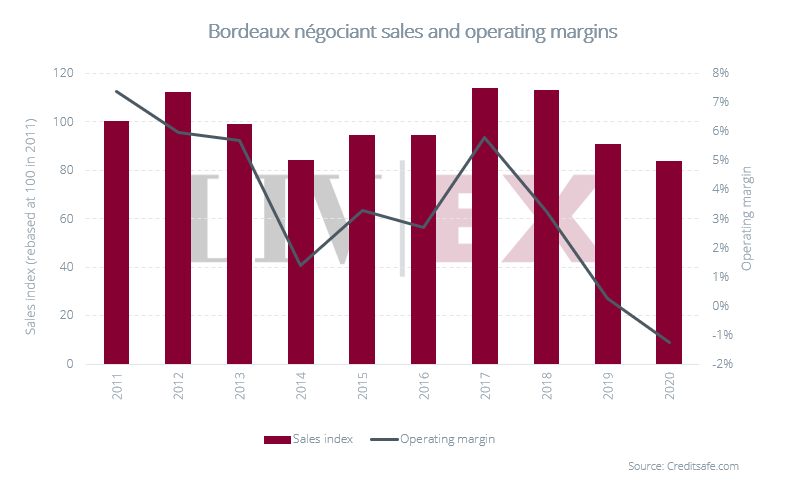

Supply chains face declining profits

As was shown in last year’s closing report, despite some very successful campaigns, there has not been a true ‘blockbuster’ offering since the 2010s were offered over a decade ago.

After a successful 2019 campaign, sales declined again with the 2020 vintage.

More worrying is the fact that the Bordeaux trade faced negative operating margins in 2020, as the chart below shows. To increase their operating margins, the negociants need to increase their income by selling more stock, and faster or lower their expenses.

In a period of rising inflation, however, decreasing overhead costs will be a significant challenge.

Faster stock turn will be critical to avoid any further deterioration of balance sheets. Bordeaux En Primeur needs to be an attractive proposition for all those involved in the supply chain, not just the négociants – perhaps more so than ever before.

Efforts from producers

Bordeaux producers are recognising these challenges, and some are making conscious efforts to reverse the trend and protect their share of the market.

Heavy investments have been made in marketing and PR, market studies and major tasting events. One of the biggest shifts in recent years has been towards sustainability, organic and biodynamic viticulture, which has been the focus of innovative research and communication from some of the region’s top names, such as Château Smith Haut Lafitte, Château Palmer and Château d’Yquem.

As well as being an effort to continually improve their winemaking and a genuine attempt to lessen their environmental impact, there is also no doubt that sustainability carries additional social and marketing cachet. For estates that are increasingly viewed and view themselves as brands, this environmental responsibility is an important part of their consumer facing image.

New initiatives

Producers have been looking for new ways to present their wines to the market, fusing art and craftsmanship into their winemaking projects.

In March this year, Château Les Carmes Haut-Brion launched an ‘Elements’ collection, showcasing a limited number of ex-château bottles, magnums and double magnums in handcrafted wooden boxes. The project is said to have been four years in the making, in order to share ‘the DNA and philosophy of the estate’, and to ‘transmit the essence of attention to detail in which the Carmes wines are made’ (Decanter).

Château d’Yquem also announced a new initiative in September last year, postponing the release of the 2019 vintage to March 2022 in order to launch LMVH’s ‘Lighthouse’ project. The ‘Lighthouse’ programme includes by-the-glass promotion of Yquem in 35 leading restaurants around the world, with the aim to make Sauternes more accessible and persuade people to drink it younger.

Mathieu Jullien, marketing and sales director for LVMH Vins d’Exception, said that, ‘the point is that it’s never going to be a cheap glass of wine, but it should be possible for someone to try a glass of Yquem at least once in their life’.

There has also been a steady rhythm in the number of ex-cellar auctions, with the private collection of Prince Robert of Luxembourg and wines from Château Lynch-Bages being some of the latest stock to go under the hammer.

Pricing strategy

The success of single producer marketing initiatives when it comes to Bordeaux’s overall place in the secondary market is unclear. However, a proven way to stimulate demand is attractive pricing on release.

Over the past decade, Bordeaux has largely priced itself based on an inherent perception of vintage quality (as determined by critic scores), rather than the commercial reality of the day-to-day market. The 2019 En Primeur campaign, launched virtually at the start of the Covid-19 pandemic, was a notable exception. The châteaux price positioning left room for profit for the supply chain and stimulated demand for Bordeaux. In March this year, 2019 was the most traded Bordeaux vintage by value and the second-most by volume.

Last year, one of the successful releases was Cheval Blanc, which presented good value for money. The château revealed in an interview that it used ‘the Liv-ex Fair Value tool* to position the release price against our other vintages in the market’. It recognised that a ‘successful’ campaign should ‘combine commercial success with communication success […] generate demand across geographies and lay the foundations for long-term price appreciation’.

It is precisely this combination of bringing value back to every point of the supply chain that will guarantee that Bordeaux remains a key force in the secondary market for fine wine.

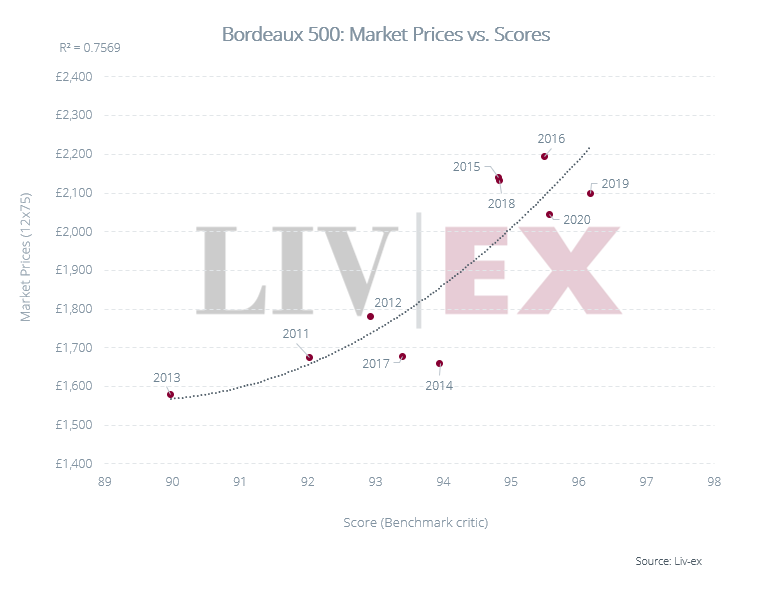

*Liv-ex’s ‘Fair Value’ methodology is a scientific approach to pricing wines. It uses regression analysis to measure the relationship between price and quality or age and establish the fair price of a wine based on its critic score and vintages already available in the market. Where there is a correlation (R-squared) between the scores/age and prices of over 50%, the trend line suggests a wine’s ‘Fair Value’.

Fair Value’ is a more rigorous way of assessing the price of a wine rather than the antiquated focus on year-on-year price change. For instance, a wine can go up in price from the previous year and still be undervalued if its quality is markedly better. We hypothesise that, over time, wines will tend toward their ‘Fair Value’ price. Typically, though not always, the most ‘undervalued’ wines provide the best returns as the price moves up to ‘Fair Value’ in the secondary market, whereas ‘overvalued’ wines provide the worst return.

Conclusion

Bordeaux remains, at least for the moment, the single largest component of the secondary market. Its top chateaux, especially the First Growths, continue to see high volumes of trade.

But this dominance is being eroded. Interest in Bordeaux (as measured by the number of wines traded in the secondary market) has begun to narrow, or put another way, become more focused. A broader, more diverse wine market has introduced greater competition, especially from regions that Bordeaux itself was the inspiration for – Napa Valley and Bolgheri’s Super Tuscan labels in particular.

As has been detailed in past reports, the current trend for releasing less stock at higher prices has two effects. First there is less stock to allocate, so buyers are driven elsewhere and second, the resultant stock overhang has a long-term detrimental effect on secondary market performance. No matter how innovative an estate is, nothing creates market demand like a well-priced release with decent volumes that offers margin to the supply chain and importantly, the collector.

Jeb Dunnuck and William Kelley have both just completed their in-bottle reviews of the 2019 vintage and have called it ‘unquestionably terrific’ and ‘vibrant, concentrated and structurally seamless’. Is the praise for 2021 likely to be so effusive? If this vintage is merely fine as the growing conditions suggest it might be, then it needs to be sold at a price that reflects this. The secondary market in physical comparable vintages provides the chateaux with plenty of guidance here. If it is not a truly ‘great’ vintage then it does not deserve to be hoarded for years in Bordeaux and eked out incrementally at prices collectors are unwilling to pay.

The 2019 vintage proved that a well-priced set of wines can find a market, even in difficult times. The uncertainty of a pandemic may be (largely) behind us but the current headwinds of rising inflation, rising taxes and rising interest rates are rattling the mainstream financial markets and no doubt the wallets of collectors.

Here then is another chance to energise the market and inject much needed capital into the distribution network. These wines should be priced to get this vintage out of Bordeaux and into cellars to be enjoyed as the truly great vintages come of age.

About

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 600 of the world’s leading fine wine merchants. Because Liv-ex doesn’t itself trade, this data is truly independent and reliable.

Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.

About Saturnalia

Saturnalia leverages data to deliver state-of-the-art intelligence and marketing for the fine wines industry. All you need to know about fine wines in one platform.

Saturnalia is a digital platform capable of providing a 360-degree immersive experience of the fine wines vineyards. Thanks to the combination of satellite-derived data and AI-driven algorithms, Saturnalia is able to showcase in one platform 3D wine maps, grape quality data and label/vintage price trend analyses for top players of Bordeaux.

With 400 hundred fine wine labels in the database and 10+ million sq km of vineyards mapped worldwide, Saturnalia is the perfect tool for fine wine collectors and professionals looking for objective and trustworthy information about wine regions, vintages and price trends.

To learn more and take advantage of a free trial visit saturnalia.tech.

- Introduction

- Weather overview in 2021

- Bordeaux’s reaction to the changing secondary market

- Bordeaux’s secondary market is changing

- Growing competition in the secondary market

- Tuscany and California named biggest competitors by merchants

- Bordeaux’s secondary market expansion stalls

- Bordeaux’s place in a broadening market

- Bordeaux’s main markets

- Changing sentiment around En Primeur

- Underlying pressures on balance sheets

- Supply chains face declining profits

- Efforts from producers

- New initiatives

- Pricing strategy

- Conclusion

- About