What’s happening in the market?

Bordeaux recorded a strong performance to start 2024. The region accounted for 41.8% of total trade since last Friday, with Château Lafite Rothschild 2009 leading in terms of trade by value.

Champagne overtook Burgundy to take second place, buoyed by trades of the 2012 vintage of Louis Roederer Cristal and Cristal Rosé. Several cases of Bollinger R.D. 2008 also changed hands.

Tuscany also started the year strongly, accounting for 18.5% of trade since last Friday. The 2016 and 2019 vintages of Sassicaia were particularly active, as was Rampolla, Sammarco 2018.

Today’s deep-dive: How well did the wine trade predict 2023?

In early 2023, we polled Liv-ex members to get their thoughts and predictions about the year ahead. Respondents included a range of professionals from our 620+ members, from established wine merchants to start-ups, spanning 44 countries.

Now, with all the data in hand, we can look back at these survey results and assess how well they did.

Want to give us your 2024 predictions? Fill in our survey here.

Outlook

At the start of the year, most members polled (38%) described their outlook for the fine wine trade in 2023 as quite optimistic – surprising, perhaps, but hindsight is a beautiful thing! 5% of respondents said they were very optimistic, 34% were neutral and 21% replied they were quite pessimistic.

The outcome of the year will of course have varied widely between members of the fine wine trade depending on many factors including location, size, operating model and more.

However, the numbers below are a powerful illustration of the correction the fine wine market is currently undergoing:

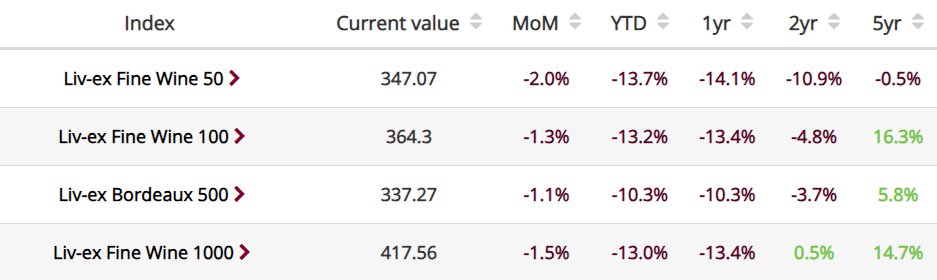

*Data taken in December 2023. See more on the Indices Explorer.

Major Liv-ex indices (which turn 20 this month!) retraced most of the growth they recorded in the previous two years. The Liv-ex Fine Wine 100, the industry benchmark, was down 13.4% from January until the end of November 2023, and both the Fine Wine 50 (which tracks the movements of First Growths) and Fine Wine 1000 (the broadest measure of the market) are down 13.0% over the same period.

Market Challenges

There was more consensus when it came to identifying major market challenges in early 2023.

Over half of survey respondents mentioned the global economy, and of those, 30% noted the global economic downturn and regional recessions. Currency volatility, inflation, declining risk appetite and market uncertainty were also cited, all of which have materialised or continued to be an issue in 2023.

16% of survey respondents expected logistics and supply chain issues to pose serious challenges in 2023, which has been the case as energy costs soared in response to geopolitical conflicts. Warehousing, transporting, logistics services and production all cost more than they did a year ago, significantly impacting the fine wine trade.

Interestingly, 12% of respondents quoted China as a likely challenge for the wine trade in 2023, specifically diminishing demand from the region (in particular from Hong Kong). However, the survey was conducted before China abandoned parts of its zero-Covid strategy, which was cited by many as a reason behind diminished trade. Some survey respondents expressed optimism at the prospect of China returning to the market.

On the whole, trade value and volume from Asia and Hong Kong remained relatively flat year-on-year. The dip in demand from the region has not (yet?) fully materialised as many merchants reported a strong first quarter of 2023 which buoyed numbers for the rest of the year. In fact, Hong Kong actually recorded an uptick in trade value year-on-year, although the number of cases traded fell in 2023.

Stock shortages were cited by 12% of respondents as a potential challenge in 2023, which was true in Burgundy as the 2021 vintage was not large enough to satisfy demand. White wines in particular saw their prices remain remarkably stable due to their limited supply but sustained demand, while most red labels recorded price declines. Overall, however, this was not a catalyst to market demand.

This stock shortage was not an issue in Bordeaux, as many young wines from the region are still readily available to purchase on the primary and secondary markets. Rising prices in the region contributed to this phenomenon, as the average release price increase was 20.8% during the 2022 En Primeur campaign. 10% of respondents to our survey identified rising prices as a challenge in 2023, a prediction which materialised as some customers rejected high ex-domaine and ex-château release prices.

Want to have your say on the trends and themes that will shape 2024? Fill in our survey here.

In case you missed it

Here’s what we’ve been reading:

- Liv-ex: The best and worst performing wines of 2023

- Decanter: Wine investment: Reality check for fine wine in 2023

- Financial Times: UK economy will enter ‘grey gloom’ until polling day, economists say

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.