January Market Report

- All of the major Liv-ex indices fell once again in December.

- One of the sub-indices of the Liv-ex 1000 recorded a positive movement: the Italy 100 rose by 0.4% month-on-month.

- Amid a month of milder declines, we highlight some of the Right Bank 50’s top performers.

- Technical analysis of the Burgundy 150 shows that the index is set to continue its downward trend.

- Even as Champagne sales fell in 2023, rare vintage Champagne remained the darling of the secondary market.

- Neil Martin’s account of Burgfest reiterates the importance of blind tasting, especially in regions like Burgundy.

- As a conclusion, we take a look at the current bid:offer ratio on the secondary market.

Introduction

Where do we go from here?

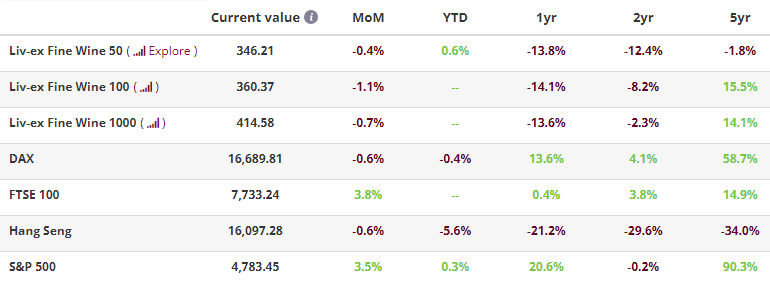

*data taken on the 11th of January 2024. The FTSE 100 was last updated on the 31st of December. The Liv-ex Fine Wine 50 is updated daily.

All major Liv-ex indices fell once again in December, concluding the year on a challenging note, with no market bottom in sight. The Liv-ex Fine Wine 100, the industry benchmark, dropped 1.1% month-on-month to close at 360.37, albeit an improvement on the previous month’s 1.3% drop and the 1.9% decline in October. The Liv-ex Fine Wine 50, which tracks the daily price movements of First Growths, fell by 1.3% in December (note: the index is updated daily).

Looking at the broader market, the Liv-ex Fine Wine 1000 also fell by 0.7% in December compared to 1.5% the month before. In contrast, major financial markets put in strong performances. The DAX rose by 0.8% month-on-month, the S&P 500 by 3.0%, the FTSE 100 by 1.8% and the Hang Seng remained flat.

The festive period, coupled with merchants taking leave, resulted in a decline for trading activity on the market in terms of both value and volume traded. However, exposure (the value of bids and offers on the exchange) nearly matched that of November, suggesting a willingness to engage. Market breadth experienced a slight decline, with 1,876 individual labels (LWIN11s) traded on Liv-ex throughout the month.

Despite challenging conditions, might releases from Burgundy and California be enough to invigorate the market?

Major Market Movers

A month of milder declines

In December, the Liv-ex 1000 sub-indices recorded declines across the board except for the Italy 100, which rose 0.4% month-on-month.

While all of the Liv-ex 1000’s sub-indices fell month-on-month, the rate of decline was slightly slower than the previous month. The Burgundy 150 saw a 0.5% drop, an improvement on the 1.9% decline in November. Likewise, the Champagne 50 and Rhône 100 recorded declines of 1.4% and 0.2%, respectively, a slowdown in comparison to the steeper drops of 2.2% and 1.6% observed in November.

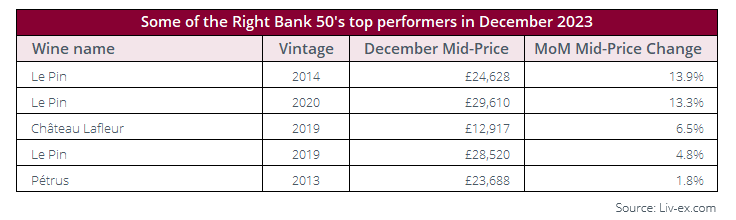

Even inside declining indices, there are some positive movements to be found. The Right Bank 50 (a sub-index of the Bordeaux 500), which was down 0.6% month-on-month, saw 21 of its components decline, 12 run flat, and just 17 record positive movements in their Mid-Prices.

Notably, among those wines that recorded positive movements were several vintages of Le Pin, Lafleur and Pétrus, lower-volume, high-price wines which tend to trade little and often but have a significant influence on the market.

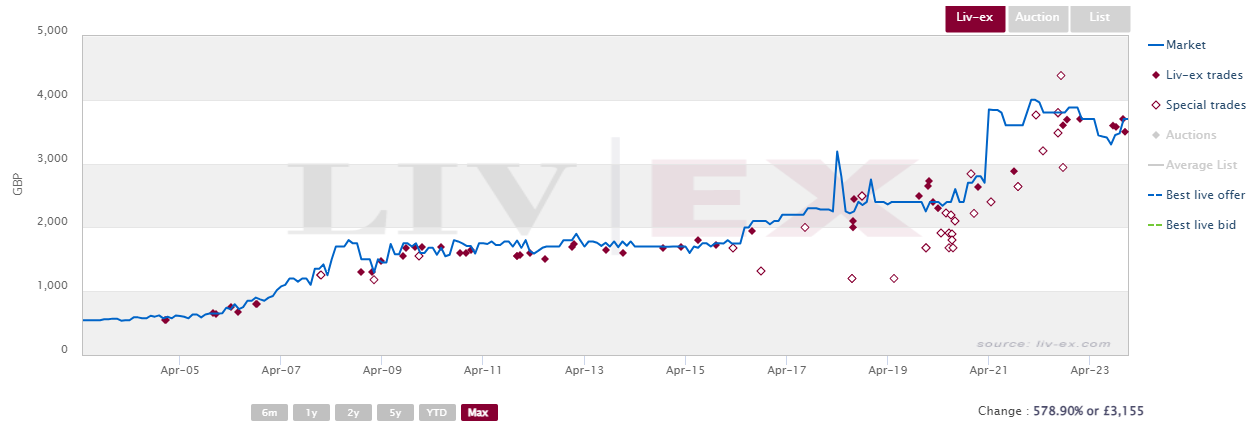

Château Lafleur 2019 was released at £5,800 per case back in 2020 and has since seen its Market Price rise by 114.7% to £14,000 per case. The wine is a triple 100-pointer (William Kelley, James Suckling and Jeb Dunnuck all gave it top marks), with 99-point scores from Neal Martin and Lisa-Perrotti Brown and 98 from Antonio Galloni and Jane Anson.

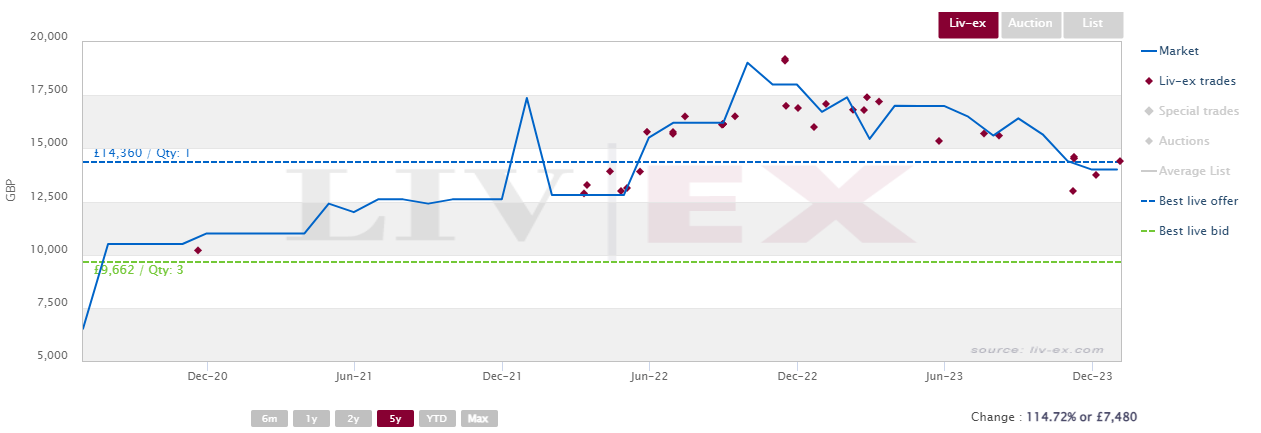

Although the spread on this wine is currently quite wide, the last trades have all occurred at or around Market Price, a level similar to the best live offer, as seen below.

Château Lafleur 2019 trades on Liv-ex

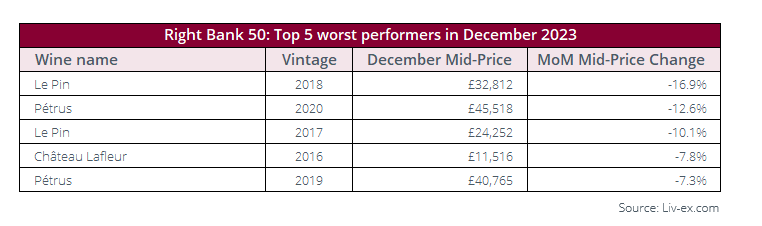

It’s worth noting that at the other end of the scale, the worst performers in the Right Bank 50 were also Le Pin, Pétrus and Lafleur, highlighting the market’s current volatility.

Chart of the Month

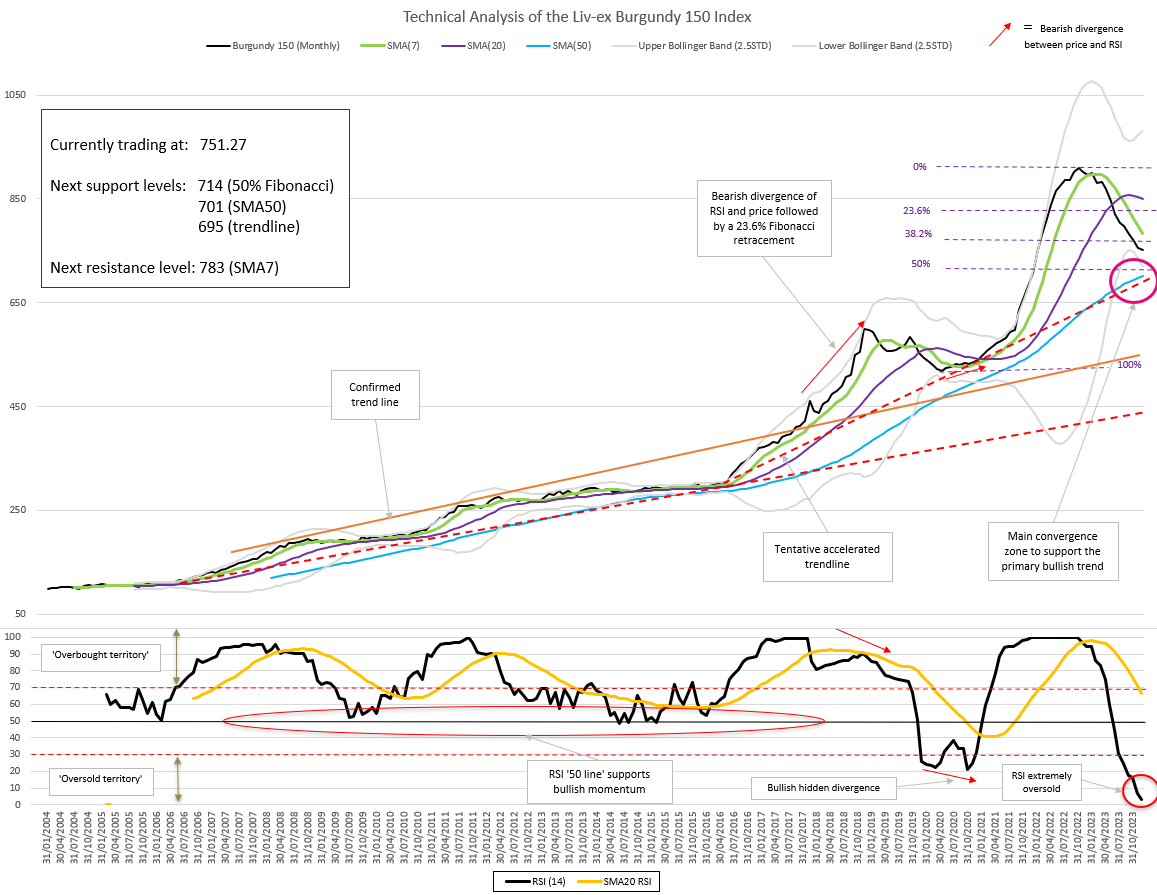

The Burgundy 150 needs a lifeline

In our March 2023 report, we highlighted that the Burgundy 150’s bullish run looked stretched. Since then, the index has declined for nine consecutive months, and is down 17% from its peak in September 2022.

In our September 2023 update, we noted that the long-term bullish trend was becoming more vulnerable but had yet to be invalidated. We further noted that a break below the Simple Moving Average 50-Months (SMA50) would be a more serious threat to the long-term trend, especially if accompanied by a break below the rising tentative accelerated trend line (the ‘main convergence zone’ circled on the chart).

At the time of writing, this statement still applies.

The index price has been riding its SMA7 downwards and looks set to continue to do so in light of the opening Bollinger Bands (BB), which signal a potential decrease in volatility. The ‘main convergence zone’ between 695 and 714 is the main objective for the price to find support in the short-term.

The Relative Strength Index (RSI), which is used to measure the speed and magnitude of an index’s movements, continues to decline into extremely oversold territory. We will monitor how it behaves if/when the price reaches the ‘main convergence support zone’.

The invalidation of the current downward move would, at the minimum, require a break of the SMA7 by the price. In view of the facts at hand, this is not expected for now.

Liv-ex members on Gold packages and above will soon have access to a tool to conduct their own technical analysis on Liv-ex data. Find out more about how technical analysis can be applied to fine wine here.

News Insight

Champagne trade on the secondary market

Champagne has dominated many a headline in 2023, ours included.

At the end of December, it was the focus of yet another story, The Drinks Business reporting that falling Champagne prices presented opportunities for buyers, especially at lower price points.

The article cites figures from the Comité Interprofessionnel du Vin de Champagne (CIVC), according to which Champagne sales declined by 9.6% year-on-year at the end of October 2023, though they remain higher than pre-Covid levels.

French auction house iDealWine also reported declines in hammer prices in 2023, but nonetheless expected to report an increase in Champagne sales in 2023, despite the average price per bottle decreasing slightly. Top labels, the auction house said, are holding out fine, although there were notably fewer ‘bidding wars’.

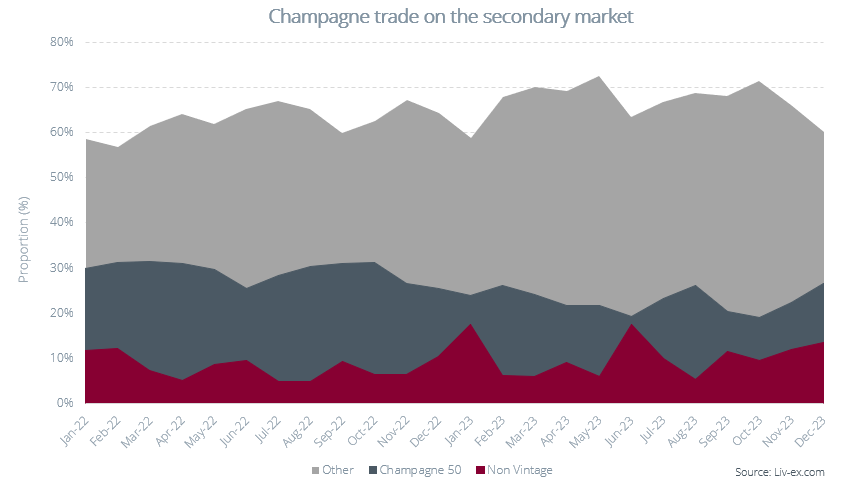

What of the secondary market? In 2023, Champagne sales were down in terms of value compared to 2021 and 2022 but remained much higher than 2019 and 2020.

The makeup of Champagne sales on the market over the past two years is interesting. The chart below shows the proportion of Champagne trade value occupied by wines within the Champagne 50 (top vintage Champagnes), Non-Vintage wines and ‘Others’.

Our piece on Non-Vintage Champagnes in last month’s Market Report outlines their increasing relevance in the secondary market, but it is interesting to note the peaks and troughs around the festive period in December/January and during summer 2023. Overall, they account for more of the Champagne market than they did back in 2022.

The Champagne 50 doesn’t seem to follow the same patterns as Non-Vintage wines, their proportion of total Champagne trade very gradually declining over 2022 and 2023. That said, they have also seen an uptick in the last three months and accounted for almost 30% of Champagne trade in December.

In The Drinks Business article, iDealWine also highlighted that old vintage Champagne and rare cuvées are continuing to set records at auction. This is also true on the secondary market, recent examples including Dom Pérignon 1996 which is experiencing a negligible pullback compared to more recent vintages of the wine.

Dom Pérignon 1996 trades on Liv-ex

Critical Corner

Neal Martin tastes 2019 Burgundies blind

In his recent report titled ‘Pump Up The Volume: 2019 Burgundy – Blind,’ Neal Martin feeds back on the Burgfest tasting, during which he tasted 438 Burgundy 2019 wines blind. The report raises questions about the importance of labels in Burgundy wines and their influence on perceived value, but also about the importance of blind tasting.

Importantly, Martin acknowledged that the tasting was not entirely blind, as ‘flights are pre-ordered per appellation’, prompting consideration that the exercise would be more compelling ‘if bottles were completely jumbled’. He also mentioned that the wines tasted were ‘poured and decanted, ensuring they [were] served at the correct temperature at every moment. Even so, some of the more stoic and backward wines [were] denied perhaps the two or three hours in a carafe that would see their true personalities revealed’. Additionally, Martin emphasised he is ‘always more critical in [his] scoring, so marks tend to be lower’.

We analysed some of the wines that Martin scored and highlighted any significant score changes.

Of the wines within the Burgundy 150 index, Martin downgraded two by five points since they were first scored in-barrel. However, both come with a caveat in their tasting notes.

Perhaps the headline figure is Domaine des Lambrays, Clos des Lambrays Grand Cru 2019’s downgrade. The wine was awarded a barrel range of 95-97 points in 2020, which Neal Martin then rectified to 96 points in 2021. In this latest blind tasting, Martin downgraded the wine to 91 points; that said, in his tasting note, he expressed doubts about the quality of the bottle he tasted.

Likewise, Domaine Georges Roumier, Bonnes Mares Grand Cru 2019 was awarded a barrel range of 96-98 points in 2020. However, in his latest blind tasting, Martin downgraded the wine to 92+ points, caveating the score by saying that ‘having been misadvised that this was in fact a flight of Premier Crus, given its propensity for aging, [he] would have been more generous in [his] score’.

Two fellow Burgundy 150 wines, Clos de Tart, Clos de Tart Grand Cru 2019 and Domaine Armand Rousseau, Chambertin Grand Cru 2019 received scores on the lower end of their in-barrel ranges when tasted blind. Clos de Tart, Clos de Tart Grand Cru 2019 received a barrel range of 96-98 points in 2020 with the blind tasting awarding the wine 96+ points. Likewise, Domaine Armand Rousseau, Chambertin Grand Cru 2019 received a barrel range of 95 to 97 points in 2020 and was scored 95 points in the blind tasting with Martin noting ‘jury is out on this for now’.

Looking more broadly, two wines from Domaine Confuron Cotetidot saw their scores reduced by 7 points each: the Echezeaux Grand Cru 2019 went from a barrel range of 91-93 points in 2020 to 85 points when tasted blind and the Gevrey-Chambertin Premier Cru Lavaut Saint-Jacques 2019 went from a barrel range of 92-94 points in 2020 points to 86 points.

On the other hand, Domaine Rossignol-Trapet, Latricieres-Chambertin Grand Cru 2019 was upgraded from a barrel range of 90-92 points in 2020 to 98 points when tasted blind. In his tasting note Martin remarks that ‘this was so shut down in barrel, but re-reading my note, I speculated that, if it could muster more substance, it would become something special – I just didn’t anticipate to this extent’.

Four further wines shifted upwards by five points: Domaine Louis Jadot, Gevrey-Chambertin Premier Cru Clos Saint-Jacques 2019 from 92-94 points to 98 points, Bachelet-Monnot, Puligny-Montrachet Premier Cru Les Referts 2019 from 89-91 points to 95 points, Bouchard Père et Fils, Chevalier-Montrachet Grand Cru 2019 from 91-93 points to 97 points and Domaine de Montille, Puligny-Montrachet Premier Cru Le Cailleret 2019 from 90-92 to 96 points.

Blind tastings such as this one, as Martin points out, highlight the influence of ‘history, reputation, and arguably the most important of all: market value’ in regular tastings. The former are important to make sure the ‘playing field is leveled’, but in their current form, their methodology is far from perfect.

Should blind tastings be more frequent occurrences in the fine wine calendar? Perhaps. In the meantime, if you trust Martin’s palate blindly, you might want to revise your 2019 Burgundy purchasing list.

There are currently 1,245 LIVE bids and offers for Burgundy 2019 wines on the exchange. Log in to view them and trade.

Final Thought

What does the bid to offer ratio tell us about the market?

The bid to offer ratio, which compares the total value of bids to the total value of offers on the Liv-ex exchange, is a measure of sentiment and confidence, which itself is a reflection of the risks involved in market making.

A ratio above 1 points to higher demand; for example, back in 2021, the bid to offer ratio on the exchange exceeded 2:1. Right now, the picture is less rosy; the bid to offer ratio on the exchange is closer to 1:5, signalling increased risk aversion and uncertainty.

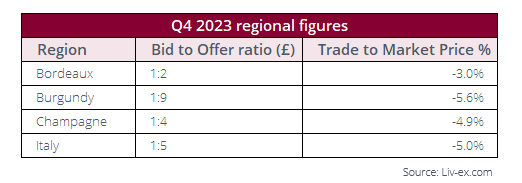

However, looking at different regions’ bid to offer ratios can shed light on potential opportunities. An interesting pattern emerges when comparing four of the most prominent regions on the exchange.

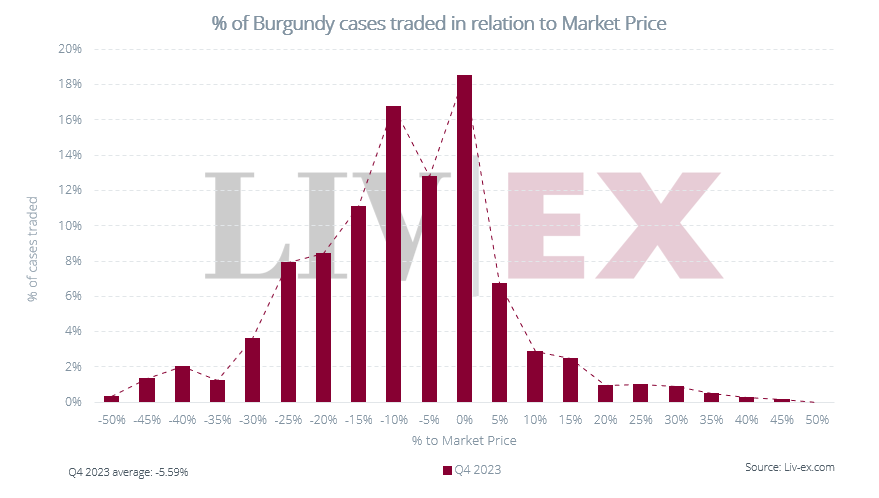

Burgundy has the lowest bid to offer ratio of these regions, which reflects the relative illiquidity of the market and the increased risk this brings. This risk aversion rises at higher price points, as illustrated by the fact that the bid to offer ratio worsens when you consider wines with a price over £15,000 a case.

This relation appears to translate into the gap between wines’ trade price and their Market Price. On average, Burgundy cases in Q4 2023 traded 5.6% below their Market Price; for cases with a Market Price over £5,000, the gap widened to 8.2% below Market on average, and trades occurred on average 14.3% below market for cases with a Market Price over £10,000. Indeed, 28% of Burgundy cases traded 10-15% below their Market Price in Q4 2023.

It’s worth noting that while the region is currently one of the biggest fallers, the Burgundy 150 is also the clear winner among the Liv-ex 1000 sub-indices in terms of its 2-year performance, up by 6.2%. The index comes in third behind the Champagne 50 and the Italy 100 in terms of its 5-year performance (+25.8%).

With the upcoming 2022 Burgundy releases and further (small) price increases, now could be the time to look at older vintages.

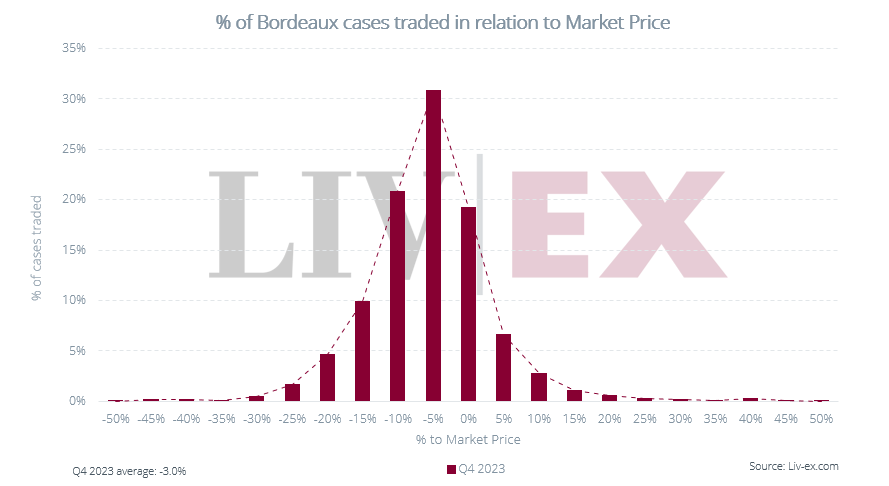

At the other end of the spectrum, the region with the narrowest bid to offer ratio is Bordeaux, a result of its relative liquidity and buyers returning to this safe bet during the current downturn.

In Q4 2023, Bordeaux cases traded much closer to their Market Price than Burgundy wines, on average just 3.0% below. However, it’s worth noting that as in Burgundy, cases with a Market Price of over £5,000 traded 4.9% below Market Price on average, and 6.2% below for cases with a Market Price above £10,000.

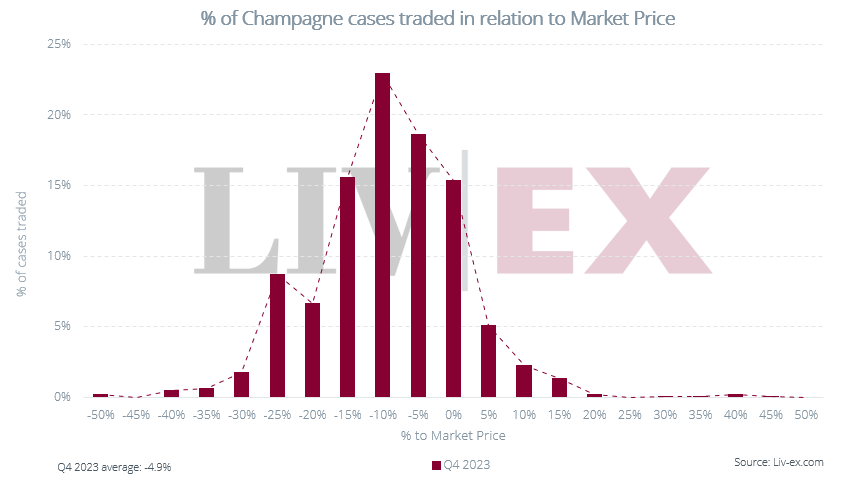

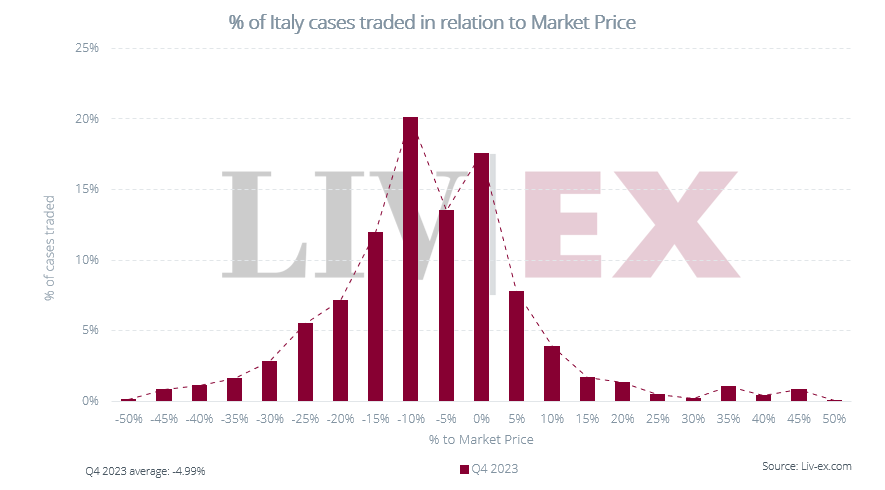

Italy and Champagne both have wider bid to offer ratios than Bordeaux, but narrower than Burgundy. Their trade to Market Price percentages also followed the pattern above, with Italy trades on average 5.0% below Market Prices and Champagne 4.9% below in Q4 2023.

The bid to offer ratio is a reflection of market conditions, with a low ratio indicating high risk aversion. However, currently, the regions with the lowest bid to offer ratios are also the ones where buyers are on average securing the largest discount on cases traded compared to their Market Price, proving that now more than ever, fortune favours the bold.