What’s happening in the market?

Looking at trading activity from last Friday through to this Tuesday, Bordeaux’s market share by value stood at 47.0%, up from the 40.8% it recorded during the week ended Friday 6th October. This uptick was primarily driven by trading activity around wines from Château Mouton Rothschild and Pétrus.

Piedmont also saw an uptick in trading activity, accounting for 5.1% of regional trade from last Friday through to Tuesday, up from the 3.3% it held at the end of last week. Wines from Giacomo Conterno and Comm. G.B. Burlotto experienced increased trading activity.

Today’s deep-dive: What’s driving stability in the Italy 100?

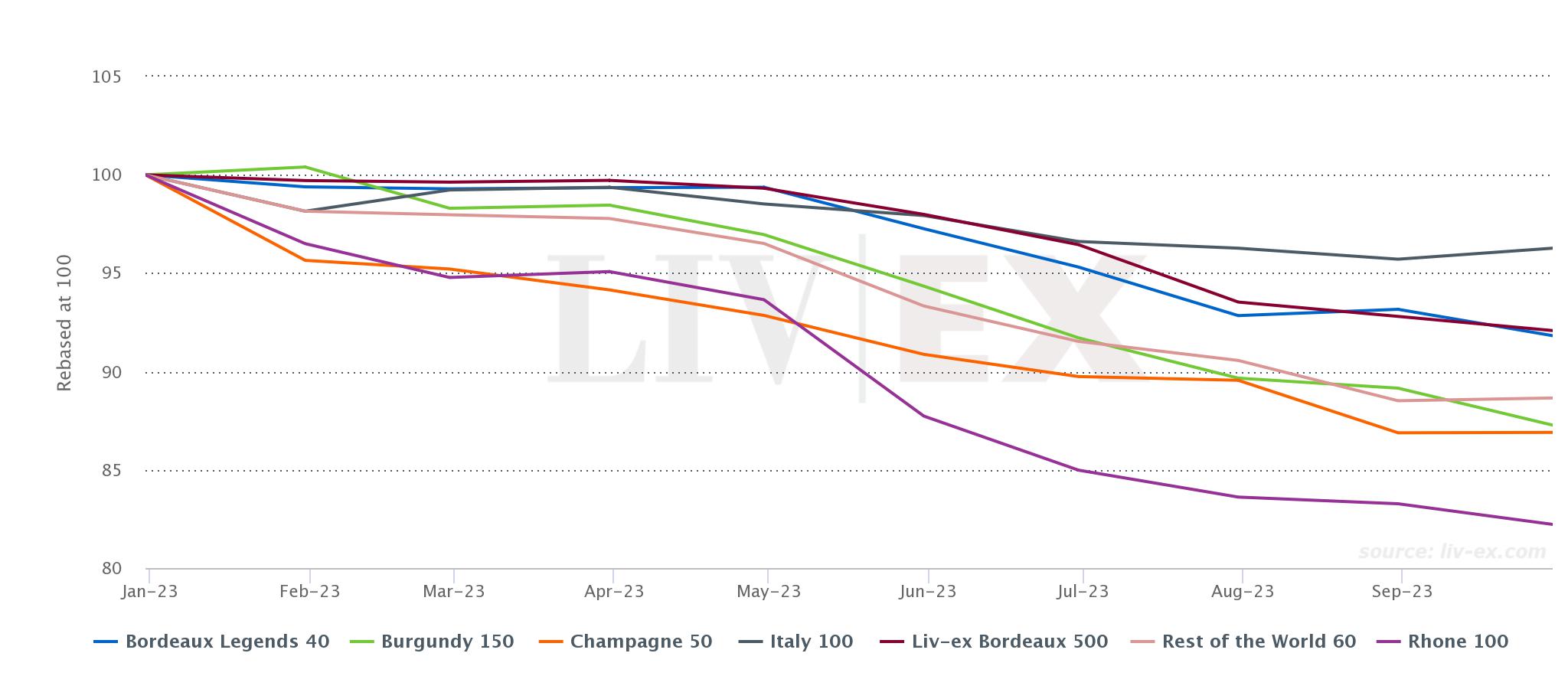

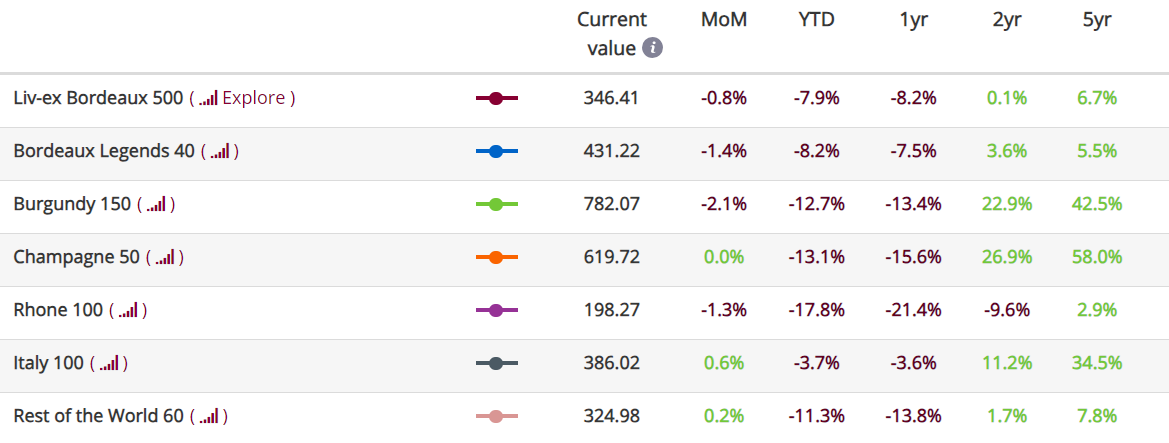

The Italy 100 index has displayed stability throughout this year, setting it apart from all the other Liv-ex Fine Wine 1000 sub-indices. Year-to-date, it has recorded a marginal 3.7% decline, in contrast with the steeper falls experienced by other sub-indices such as the Champagne 50 (-13.1%), the Burgundy 150 (-12.7%), the Rhône 100 (-17.8%) and the Bordeaux 500 (-7.9%). Even the Bordeaux Legends 40 has dropped 8.2% since the start of the year.

*made using the Liv-ex Charting Tool. Data taken on 11.10.2023

A strong showing in September

In September, the Italy 100 outshone its peers, with a 0.6% month-on-month increase, once again surpassing all other sub-indices of the Liv-ex Fine Wine 1000.

Looking at the components of the Italy 100:

- 26 wines maintained their value month-on-month.

- 49 wines rose in value.

- 25 wines recorded a decline in value month-on-month.

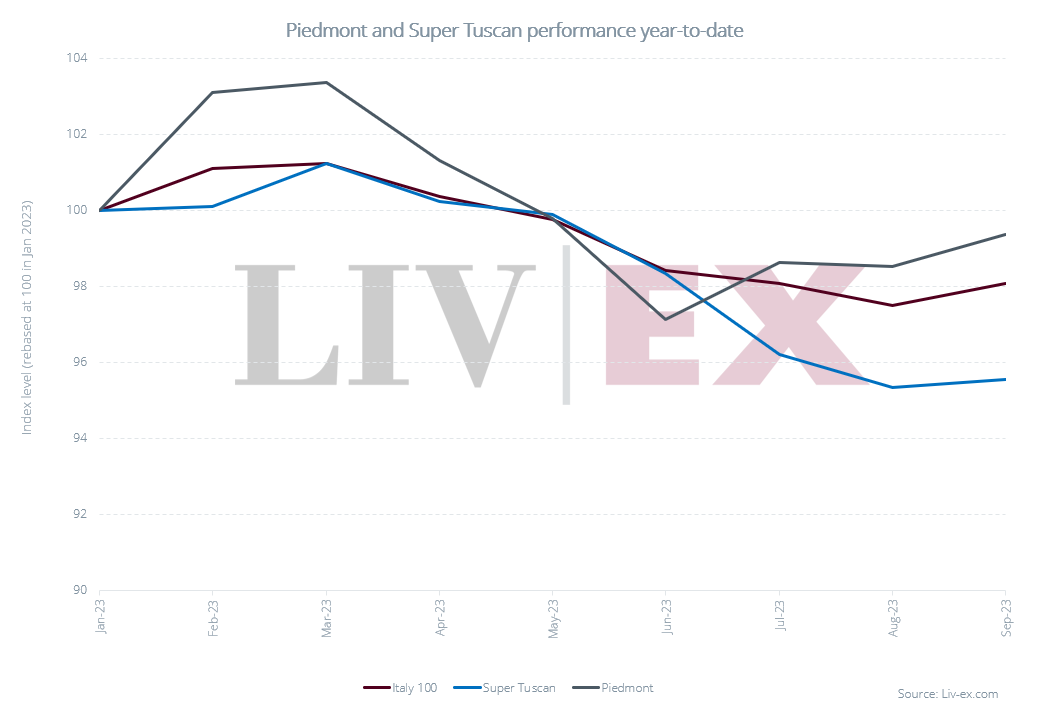

Piedmont outperforms Tuscany in 2023

Looking deeper into the regional trends within the Italy 100, Piedmont emerges as a driver of the index’s stability. In September, 35 Piedmont wines either held their value or appreciated, while only five recorded a decrease. By contrast, Tuscany had 40 wines maintain or increase their value but a larger proportion (20 wines) fall.

Looking at year-to-date performance, the story is much the same: 68% of Piedmont wines declined in value while 32% recorded a positive movement, whereas 80% of Tuscan wines fell and only 20% remained stable or increased in value.

Which are the best-performing wines in the Italy 100?

Looking at the top performers in the Italy 100 year-to-date, only two of the top ten wines come from Tuscany. One of them, Fontodi, Flaccianello delle Pieve, Colli della Toscana Centrale 2011, is the best performer in the index year-to-date. The wine has a Wine Advocate score of 94 points and a current Market Price of £1,220 per case.

The 2017 vintage of Fontodi, Flaccianello delle Pieve, Colli della Toscana Centrale takes the tenth spot with a year-to-date increase in its Mid-Price of 7.6%. In September, the wine’s Mid-Price increased by 21.0%, making it the index’s top performer last month. The wine has a Wine Advocate score of 96 points and a Market Price of £946 per case, well below the average Tuscan wine’s Market Price (within the Italy 100 index at least) of £2,902 per case.

Looking at Piedmont wines within the index, both the 2015 and 2011 vintages of Gaja, Barbaresco, feature in the top ten performers with increases of 18.1% and 13.1% since the start of the year respectively. Both wines have Wine Advocate scores of 93 points, and their Market Prices of £1,700 and £1,800 per case respectively position them well below the average Market Price of Piedmont wines within the Italy 100 index, which stands at £5,886 per case.

Giacomo Conterno, Barolo, Monfortino Riserva 2004, with a perfect 100-point score from both The Wine Advocate and Antonio Galloni, has recorded an 8.7% year-to-date increase. This wine has a current Market Price of £14,400 per 12×75.

The Italy 100’s year-to-date decline has been primarily influenced by Tuscan wines, which have recorded an average 4.5% decline so far this year compared to Piedmont’s 3.3% fall. In September, Piedmont wines buoyed the index towards a positive movement, with an average increase of 1.1%, surpassing Tuscan wines, which saw a more modest average increase 0.5% in September.

Interestingly, this time last year, the tables were turned as Tuscan wines were outperforming Piedmont wines, as buyers fell back on established and comparatively more liquid Tuscan brands.

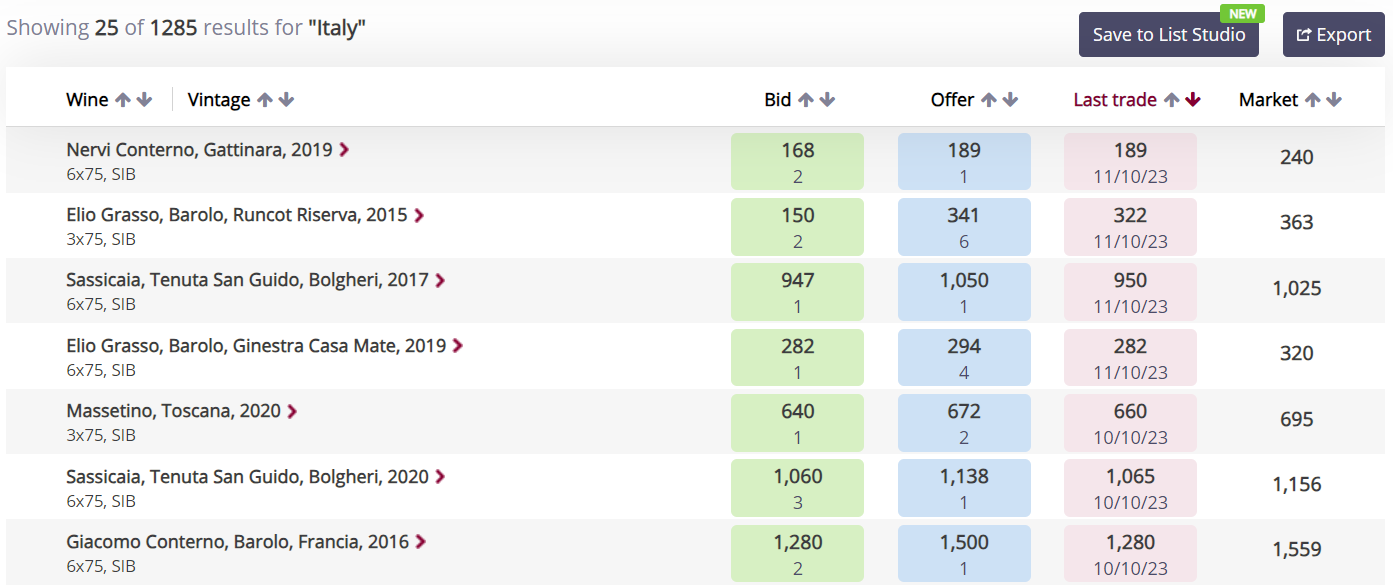

There are currently 1,285 LIVE bids for Italian wines on Liv-ex. Log in to the exchange to view them and trade. Additionally, you can use the new ‘Save to List Studio’ function to add these wines to a list you and add further data points to it, or come back and review it when it suits you.

In case you missed it:

Here’s what we’ve been reading:

- Liv-ex: The fine wine market in Q3 2023

- The drinks business: How can Argentina rival the world’s finest wines?

- Financial Times: Further UK rate rise possible due to ‘persistent’ inflation, IMF predicts

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines.