Print and read offline instead.

In this report:

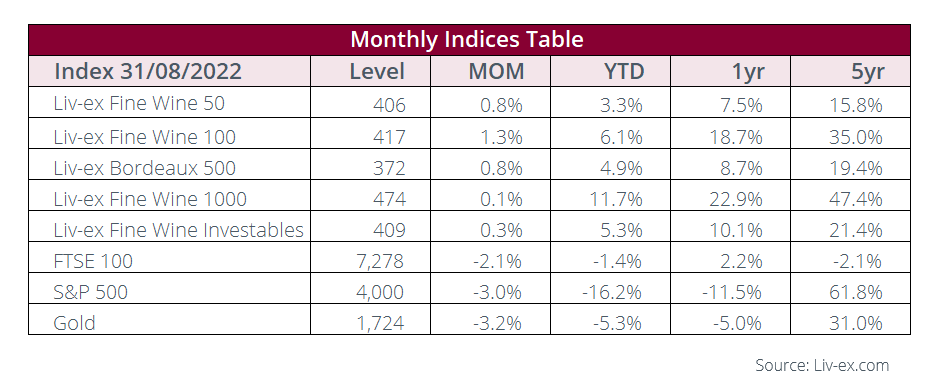

- The leading fine wine indices outperformed equities in August.

- For the first time ever, Burgundy overtook Bordeaux as the most traded fine wine region this month.

- Super Tuscans from the 2016 and 2017 vintages were among the best performing wines in the Liv-ex 100 index in August.

- German wine remains a niche player in the secondary market but its presence is increasing.

- Lisa Perrott-Brown MW offered a retrospective on the ‘trick-or-treat’ Bordeaux 2012 vintage.

- Amid the talk of each new global addition to La Place de Bordeaux, autumn and spring are becoming equally important for Bordeaux releases as well.

Weaker Sterling gives a boon to the fine wine market in August

Weaker Sterling gives a boon to the fine wine market in August

The Liv-ex Fine Wine 50 and 100 indices, which declined in July, rose again last month by 0.8% and 1.3% respectively. Sterling dropped to its lowest level since March 2020, which proved a boon for the fine wine indices. As the Liv-ex indices are measured in Sterling, the weakened state of the currency means the buying power of the Euro and, most of all, the US Dollar have risen as a result. The broadest measure of the market, the Liv-ex 1000 index largely ran flat, with a 0.1% rise which marked its smallest increase this year.

While reflecting the troubled economic outlook, fine wine managed to keep ahead of other markets. UK stocks extended their losses, with the benchmark FTSE 100 dropping 2%. US equities also weakened as the S&P 500 tried to balance interest rates and Fed expectations. Even safe havens like gold came under pressure.

For a third month in a row, the best performing region was Champagne. The Champagne 50 sub-index rose 2.1% in August, contributing to its stellar year of gains. It has recorded a rise of 52.3% so far this year. At the other end was the Rest of the World 60 index, which dipped 2.2% in August. All major fine wine indices, however, remain in the positive territory so far in 2022.

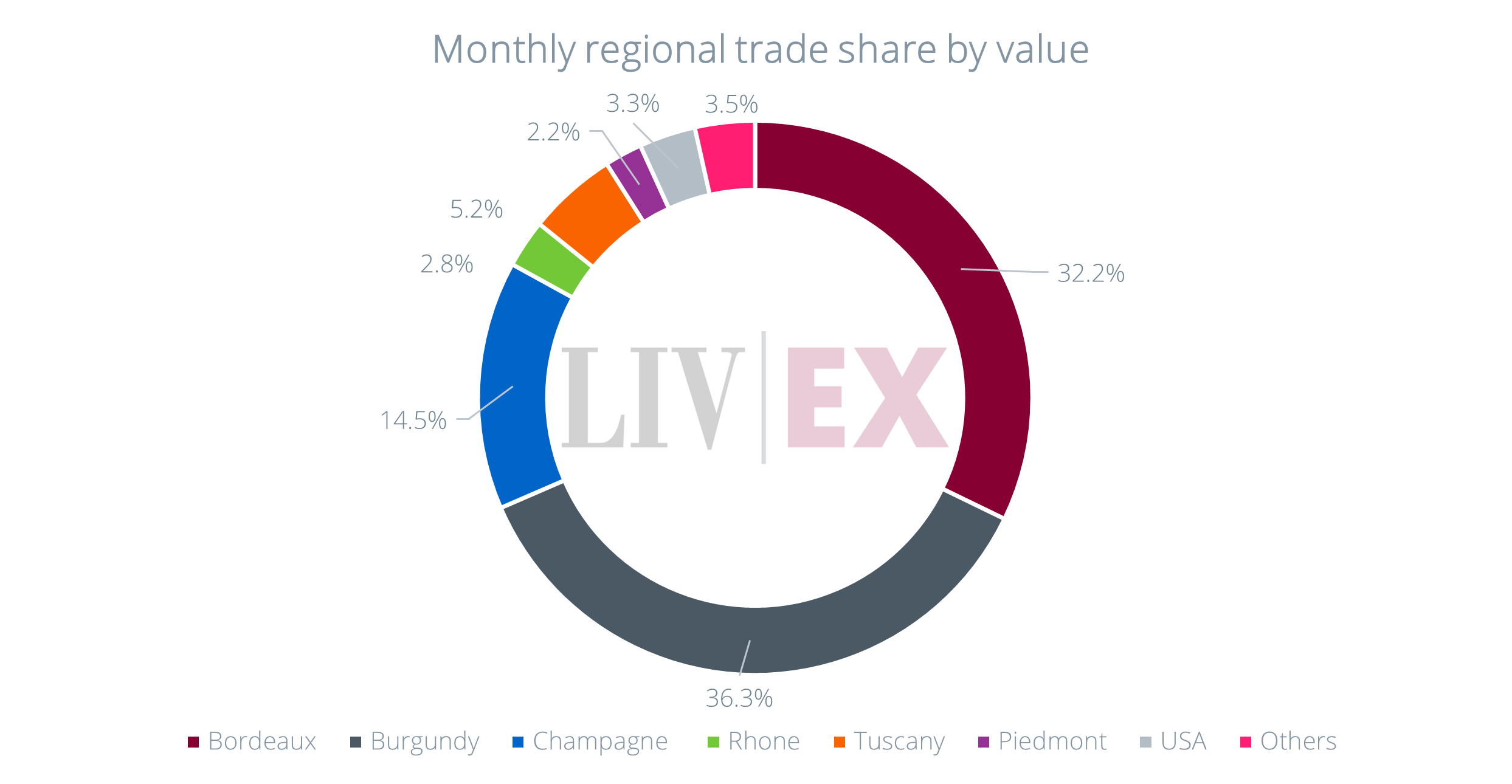

Chart of the month – Burgundy overtakes Bordeaux as the most traded region

Burgundy was the most traded fine wine region in August, taking 36.3% of the total market. This marked a record monthly high for the region. In the third week of the month, the region’s market share surpassed 50% for the first time ever. Trade of high value wines from Domaine de la Romanée-Conti and Armand Rousseau contributed to this result.

Bordeaux accounted for just 32.2% of total trade, with interest centered around ‘on’ vintages, such as the 2019 and 2000.

Champagne, which hit a record high in July of 16.7%, dipped to 14.5% in August. The 2008 and 2012 vintages led demand.

Italy, the USA and the ‘others’ were also in decline. The latter saw the biggest drop, from 6.9% in July to 3.5% in August. Australia (0.6%), Germany (0.5%) and Spain (0.4%) enjoyed the most trade from within the category.

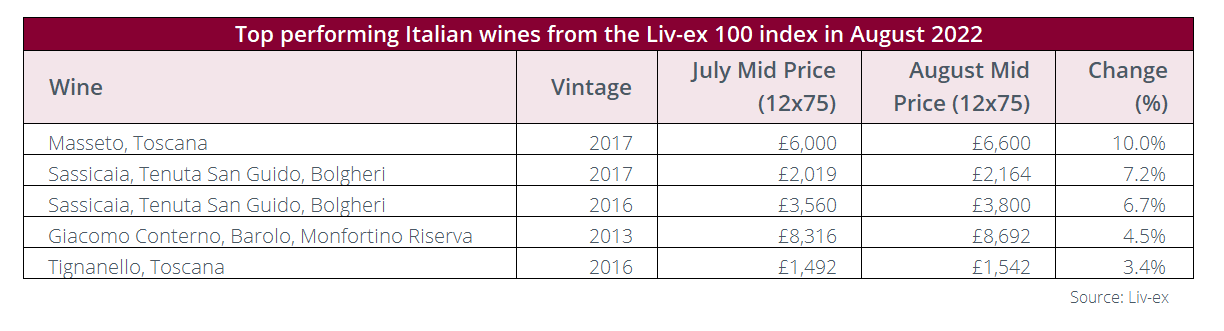

Major Market Movers – Italy makes gains in August

Compared to its impressive run between 2019-2021, Italy has seen more modest activity on the secondary market this year. Year-to-date, the country is the fourth most-traded fine wine region, and the Italy 100 is the fourth-best performing Liv-ex 1000 sub-index (+6.5%).

However, last month, the Italy 100 was the second-best performer. It rose 0.8%, just behind the Champagne 50. Italian wines in Liv-ex 100 index were also on the move, appearing among this months’ biggest risers.

Ahead of the release of the 2019 vintage via La Place de Bordeaux, Masseto 2017 rose 10.0% on the back of increased trading activity. The 2017 and 2016 (WA 100) Sassicaia vintages also went up 7.2% and 6.7% respectively. Tignanello 2016 rose 3.4% and set a new trading record at £1,542 per 12×75.

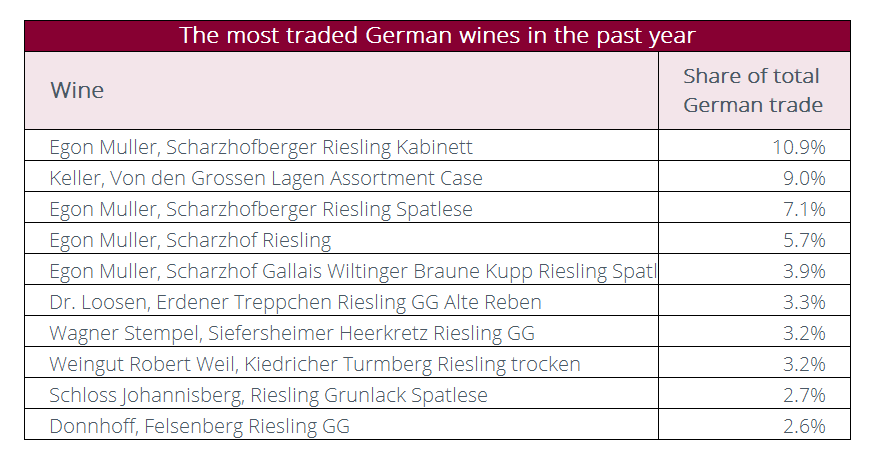

News Insight – The German fine wine market in the past year

It has been over a year since the flooding of the Ahr Valley that inflicted ‘billions of euros of damage,’ according to a recent article by the drinks business. Various initiatives have been undertaken to help rebuild Germany’s smallest wine region, such as the SolidAHRität movement and fundraising events. Some wineries lost their entire 2021 vintage, while others were able to make up some losses, with the ‘help of wineries from other regions’.

In light of Germany’s recent coverage in the press, today we look at the country’s performance in the fine wine market.

German wines are starting to see some benefit from the on-going broadening of the market. Germany’s trade share has gone from a high of 0.9% of the total market in 2020, to 0.5% in 2021 and it currently sits at 0.6% so far in 2022.

There has also been an increase in the number of wines trading, rising from 182 in 2020 to 201 in 2021. Year-to-date, the number stands at 156. Red wine is increasingly present in trading activity, accounting for 3% of all German wine trade so far in 2022, up from 0.5% in 2021.

In the past year, the split in trade between the different regions has been the following: Mosel (50.9%), Rheinhessen (40.9%), Nahe (3.6%), Rheingau (2.5%), Franken (1.2%), Pfalz (0.5%) and Baden (0.4%). A wine from the Ahr last traded in April 2021 – Jean Stodden Spätburgunder 2019.

The 10 most-traded wines in the past year have all been dry and sweet styles of Riesling split between seven different producers. The rankings, along with their share of the total German trade by volume, can be seen in the table below.

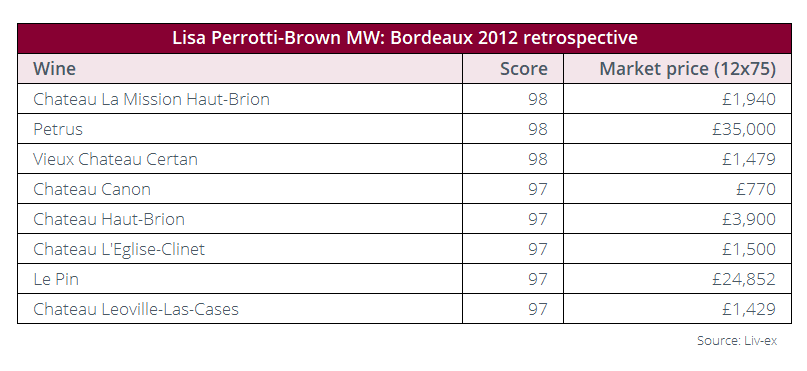

Critical Corner – Perrotti-Brown Bordeaux 2012 retrospective

Lisa Perrotti-Brown MW recently reviewed the 2012 Bordeaux vintage for The Wine Independent as it reaches the 10-year milestone.

She said that 2012 is a ‘trick-or-treat vintage’ because ‘there are lots of treats, but also a few scary tricks’.

The vintage is heterogenous. She said that some wines were ‘starting to fade’ and, ‘many of the top wines are mature now and won’t last much more than another 10 to 15 years.’

However, there was a small clutch of wines – mainly from Pessac-Léognan, Pomerol and Saint-Emilion – that were ‘spectacular successes’ with another ’20 to 30 years of cellaring potential’.

Final Thought – Bordeaux’s ex-cellar campaigns

With every passing year, more brands from Italy, the US, New Zealand, Australia, Spain and even Hungary announce they will be represented by négociant houses in Bordeaux.

As examined in our recent report on the broadening scope of La Place de Bordeaux, the number of wines now being offered each autumn and spring is well over 100 – up from 70 as recently as last year.

Yet alongside the Super Tuscans, Andean Icons and Cult Napa Cabs, is the growing number of Bordeaux wineries using these autumn and spring release periods to offer new and library stock of their own.

Château Latour led the way a decade ago, quitting the traditional En Primeur system to offer bottle-aged wines instead. Its routine is now to offer new vintages each spring and a library release in the autumn. The 2010 vintage is being offered on 13th September.

In September 2020, Château Palmer also launched a late-release programme called ‘N-10’. The estate had been holding back half of its production since 2010 to have sufficient stocks to supply the initiative. The 2012 vintage is out on 22nd September.

These are two of the most obvious examples but others such as Château Ausone and Valandraud also use the autumn to release collection cases and ex-cellar stock of mature vintages.

New sales period for Bordeaux whites

Alongside the release of new and old red wines is the emerging use of autumn and spring as a new sales period for the region’s dry and sweet white wines.

The Sauternes 50 is traditionally the weakest sub-index of the Bordeaux 500. Since 2004 it has risen just 23.2% - whereas all the other indices have risen by triple figures.

However, its performance more recently has been better. It rose 1.1% in August, the only sub-index besides the Right Bank 50 (2.0%) to show positive gains. It is also the third best-performing sub-index of the Bordeaux 500 index year-to-date, up 3.9%.

In a collecting and secondary market already strongly geared towards dry, red wines, the added problems of sweet wines falling out of fashion and some difficult vintages has seen Sauternes and Barsac put under serious pressure.

As a result, estates seem to be migrating their releases away from the summer’s En Primeur campaign where they risk passing largely unnoticed amid the attention around the reds.

In February of this year, Château d’Yquem said that it would move its 2020 releases to the spring of 2023 and its dry wine (Y de Yquem) in following September. Library stock of Yquem 2016 (half-bottle) will be released this month.

Domaine Barons de Rothschild has also moved the release date of its own Sauternes estate (Château Rieussec) to the autumn as well. The 2020 vintage of Rieussec and R de Rieussec 2021 were released on 31st August.

Another Sauternes estate, Château Suduiraut, is debuting a dry white this autumn as well. Extremely limited quantities of the Vieilles Vignes 2020 are being released on 15th September.

Finally, Château Cheval Blanc’s white wine, Le Petit Cheval Blanc, is also offered each autumn. The 2020 vintage is due out on 19th September.

While attention largely focuses on the growing number of ‘Global Icons’ that are joining La Place, its increasing role as a continued vehicle for distributing Bordeaux wines outside of En Primeur should not be overlooked.

Brands are turning to La Place as a means to reposition their offering in a changing and increasingly global market for fine wine. This change is having as much of an effect on the wines of Bordeaux as it is elsewhere.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines. Independent data, direct from the market.