Print and read offline instead.

Bordeaux, then what?

-

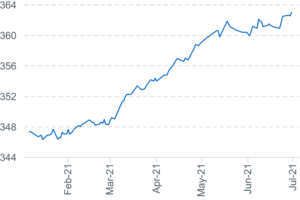

- Liv-ex 50 index

-

- Liv-ex 100 index

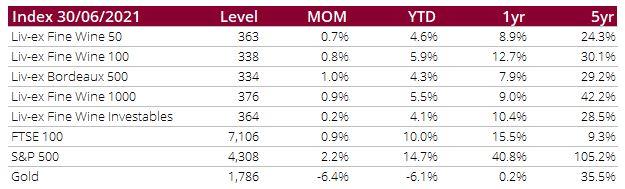

The 2020 Bordeaux En Primeur campaign is officially behind us. And while its inconsistent pricing and pacing held the trade’s attention, trade outside Bordeaux remained steady.

Italy and Burgundy took equal parts of the market in June (16.8%) and capped off their best ever first half to a year. The Rhône had a strong month too, with trade by value climbing from 4.2% in May to 4.7% in June, as its secondary market continued its expansion. There was increased activity around English and German wines. German whites from the Mosel (89%), Rheinhessen (9%), Nahe (0.8%) and Rheingau (0.4%) found willing buyers last month.

Fine wine prices rose, with the Liv-ex 100 up 0.76%, pushed by strong performances from Burgundy’s 2015 vintage and Bordeaux’s finest – 2005, 2009 and 2010.

The broadest measure of the market, the Liv-ex 1000 index, also rose 0.9% in June. Its best performing sub-index was the Rhone 100 (1.6%), followed by the Burgundy 150 and the Italy 100, up 1.3% each. The Rest of the World 60 was the only sub-index to decline (-0.7%), partly due to dips across Opus One and Dominus – though Screaming Eagle was the best-performing label overall.

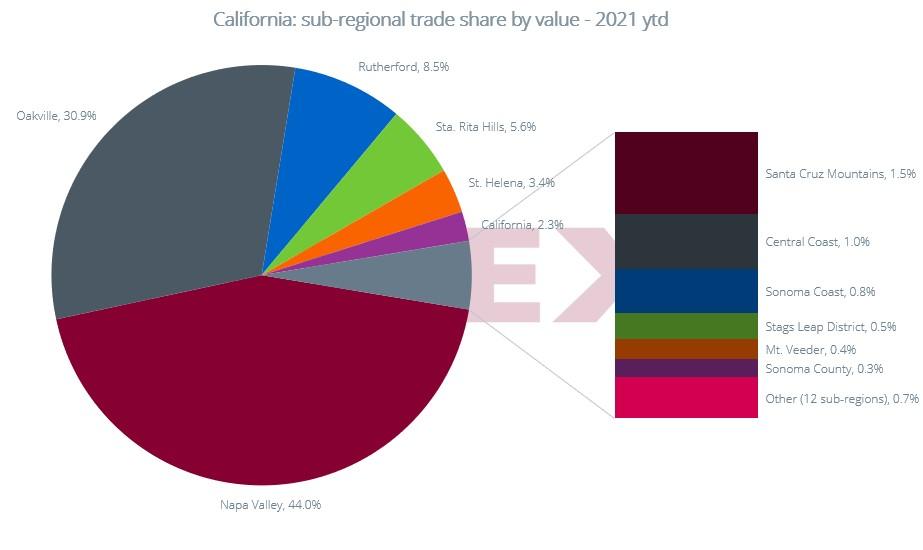

Chart of the month – Californian wines

As recently reported, the US market is growing and so is demand for Californian wine. California still makes up the lion’s share of US wine traded on the secondary market (99.6%), but there are signs.

The impact of the broadening market has not bypassed California. So far in 2021, Napa has accounted for less than 90% of California’s trade share by value, down from 93% in 2010, as other Californian regions and varieties find new buyers.

Even within Napa, increasing demand for a wider array of wines has seen a growth in sub-regional trade for AVAs such as Oakville, Rutherford and Stag’s Leap. Wines from Howell Mountain (Abreu and Dana Estates) have also been traded for the first time.

The Central Coast (1%) is largely represented by the boutique Sine Qua Non, whose Rhône blends traded initially in 2018 and are back in play this year.

And while reds dominate the secondary market, Sauvignon Blanc and Chardonnay are also finding buyers. Oakville, Napa, and Sonoma Coast might just be the AVAs to watch for quality whites in the near future.

In the news

LVMH has reportedly suspended exports to Russia after the Russian government announced that the term “Champagne” will only be used for locally made sparkling wine, while the world-famous wine from France’s Champagne region should be called “sparkling wine”.

The Wine Institute and CEEV have issued a statement supporting the removal of all tariffs on wine traded between EU and US. A total of 86 US and EU lawmakers endorsed the statement which acknowledged the detrimental impact of retaliatory tariffs and called for a “zero for zero” tariff-free wine trade environment.

Château Pichon Longueville Comtesse de Lalande announced on Twitter that it has officially began conversion to organic farming. This is the “logical consequence of a virtuous global approach started ten years ago,” it said. The first fully organic vintage will be 2024.

Unfortunate news for Loire growers as a tornado hit Saint-Nicolas-de-Bourgueil on Saturday, 19th June. It has left crops ravaged throughout the area, with the material damage yet to be determined.

And, finally, Liv-ex ABV published its findings into the rise in alcohol levels in wine over the past 30 years. Red wines from Bordeaux, Tuscany, Piedmont and California all had higher alcohol levels on average in the decade between 2010 and 2019 than they did in the 1990s. Find out more here.

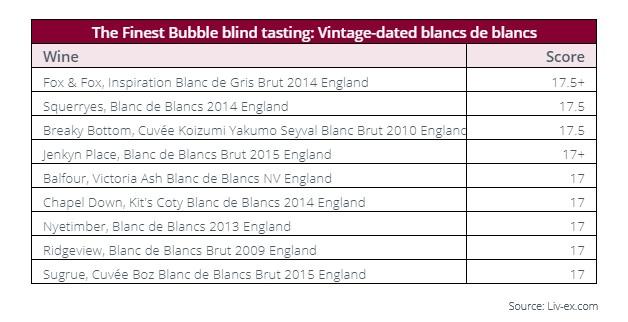

Critical Corner – English fizz

Just in time for English wine week (19th-27th June), Jancis Robinson MW and Tamlyn Currin released critical assessments of 64 English sparkling wines.

In their report, Currin wrote that, “the last few years have seen more and more ‘icon’ and limited-edition releases […] Gaining confidence in their vineyards and winemaking experience, winemakers are starting to play, to experiment beyond the ‘house style’”.

Below is a selection of vintage and non-vintage fizz awarded 17 points or more. The “very vital and confident” Fox & Fox, Inspiration Blanc de Gris Brut 2014 received the highest score of 17.5+.

On the secondary market for English wine, white sparkling has dominated trade. The blanc de blancs wines of Gusbourne, Wiston and Nyetimber have cornered much of the trade share by volume and value.

Increased critical praise for English wine, however, will help it find its feet in domestic and export markets, and its secondary market will undoubtedly rise as well.

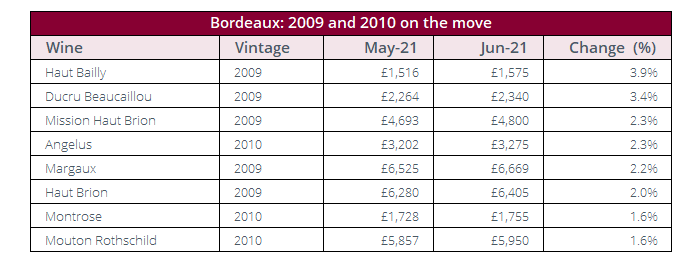

Major Market Movers – Bordeaux’s greatest

En Primeur is not just a look into the future. The campaign highlights value in previous Bordeaux vintages too. Indeed, some the best price performers this month came from the French region’s two most expensive vintages, 2009 and 2010.

Both 2009 and 2010 were released at record prices, when the Bordeaux market was nearing its peak.

The 2009 En Primeur campaign launched amid a rising tide of demand from Asia and a global financial system awash with ready money. The market was at its peak when the 2010s were offered at a 5%-20% premium on average to the previous year.

In mid-2011, the secondary fine wine market took a turn, leading both vintages to fall in value for much of the next five years.

Having struggled to reposition themselves in the following years, some of these more mature wines have begun to represent fair value in the context of fresh releases – and have thus begun to recover.

Final thought – Back to the drawing board

So ends the 2020 Bordeaux En Primeur campaign. Where last year’s lasted a blistering four weeks, this year’s took a more leisurely six (and a bit). The talk of last year’s campaign was price cuts, this year it was of prices escalating once more.

‘The Magic is Back’ was the title of last year’s closing report, it is unlikely the next will be headlined quite so optimistically.

This year’s campaign with its strong but inconsistent array of wines was a golden opportunity to cement the success of the 2019s.

It began well enough with the surprisingly early launch of Cheval Blanc. Released on 11th May, its initial offer of £4,656 per case was 3.5% up on the 2019 release but 2.7% down on that wine’s Market Price.

Many expected price increases for the 2020s. With this well considered release, however, it was hoped that Cheval Blanc was setting the tone for the campaign to come.

Although some subsequent releases went much further (Angélus increased its price by 13% ex-négociant for example), in the first four weeks of the campaign the average price increase was just 5.3%.

This was comfortably within the biggest pre-campaign predictions and lead to steady demand from collectors. The pace of releases lagged in late May, however.

Unlike last year, when wines were flying out before the verdict of major critics had been delivered, most estates this time seemed to prefer to wait for critical reports from Vinous and the Wine Advocate which were released in late May.

Following the late Spring Bank Holiday releases picked up again but the pace remained stately, with three to four releases a day.

It was only really from the 14th June that the tempo of the campaign really began to pick up. Unfortunately, so did the pricing.

As June continued the ex-négociant price began to rise – first by 10%, then 15%, then 25% and by the final week prices were consistently up over 30% and even on occasion by as much as 40%. We were back at 2018 levels.

The biggest increase seen in the campaign was for Pomerol estate Petit Village. Recently acquired by the Moulin family which owns Groupe Galeries Lafayette, its ex-négociant price per bottle was 97% higher than the 2019.

Even with price increases, there were still wines that looked Fair Value and wines that sold through. Though to what extent wines sold out (stocks released were reduced once again) is still unclear.

The up-coming En Primeur Closing Report will have the full breakdown of the campaign to show where its strengths lay and where it fell short.

In the immediate aftermath, however, it would seem as though an opportunity may have been missed in terms of the amount of wine sold, new customers retained and good will nurtured.