Print and read offline instead.

Key findings

- California’s trade share has risen from 0.1% to 7.1% in the past decade

- California is the most important region from the Rest of the World category, based on prices and trading activity

- California is the second most expensive fine wine region based on the average price of its leading estates

- The California 50 index hit an all-time high in August 2021

- While Napa “cult” wines command the highest prices and attract the most trade by value, Ridge Monte Bello from Santa Cruz is the best performing Californian wine index

- A string of good vintages in the past decade, high critic scores and a global distribution network have pushed prices and led to increased trade

- The UK remains the biggest foreign market for Californian wine

- Diversification has allowed for more trade of white wine, and AVAs beyond Napa Valley

Introduction

The 24th May 1976 is the date considered by many as the turning point for Californian wine.

The notorious Paris Wine Tasting (“The Judgement of Paris”) which took place that day, organised by the late Steven Spurrier and Patricia Gallagher, was a blind tasting competition in two parts: top Californian Bordeaux blends against Bordeaux classed growths, and Californian Chardonnays against their white Burgundian counterparts.

Until this point, it had barely been considered that another region could rival the dominant fine wine market force. When the scores were tallied, however, Californian wines led both categories. That day not only opened the doors for Californian wines to the global stage; it helped set in motion the future broadening of the market we are witnessing now.

Oz Clarke wrote in his New Encyclopaedia of Wine:

“California was the catalyst and then the locomotive for change that finally pried open the ancient European wine land’s rigid grip on the hierarchy of quality wine and led the way in proving that there are hundreds if not thousands of places around the world where good to great wine can be made […] until the exploits of California’s modern pioneers of the 1960s and ’70’s, no-one had ever before challenged the right of Europe’s, and in particular, France’s vineyards, to be regarded as the only source of great wine in the world.”

But how important exactly is California in today’s fine wine market? And what has changed since 1976?

Chiefly, California has emerged as one of the few non-European wine investment players. With the emergence of key brands, cult wines attracting collector interest, and Hollywood celebrities flocking to the Golden State aiming to fulfil their winemaking dream, California has challenged the old-fashioned image of wine; breaking stereotypes with its modern and approachable nature, and innovative marketing.

A string of good vintages in the past decade, particularly 2010, 2013, 2016 and 2018, increased critical coverage and high scores have strengthened California’s international image. Year-to-date, California is the highest-scored fine wine region by international critics, with a large number of 100-point wines.

So far in 2021, California has taken a 7% value share of the fine wine market, against an ever-diminishing share of Bordeaux. Its top wines command the second highest prices in fine wine; after red Burgundy. Demand keeps on rising, from the UK, US and Europe, as do prices – the California 50 index reached its highest ever level in July 2021, having appreciated 38% in the past half decade.

Californian fine wine has certainly cemented its place on the global market. The following report explores its development, identifies opportunities, and discusses the sustainability of its secondary market success.

Cult wines – the formula for success

Although winemaking in California was begun in the 18th century by Franciscan missionaries, it wasn’t until the late 20th century that the real revolution began.

The 1990s would prove instrumental for the development of the Californian fine wine market. The biggest Californian success after the Judgement of Paris, was the emergence of cult wines – a decidedly American phenomenon – that helped push California on the global collectible stage.

Producers such as Inglenook, Stag’s Leap and Robert Mondavi laid the foundation for the emergence of cult brands, but it was Screaming Eagle, that proved the pioneering cult label, establishing the formula for success that many followed. Tiny volumes (often under 600 cases), word-of-mouth hype resulting in high demand, and soaring prices. Scores of 99-100 points from leading critics, like Robert Parker, pushed prices to incredible highs.

Screaming Eagle’s first vintage, the 1992 released in 1995, received 99-points from Parker, and became one of the most celebrated and expensive wines in Napa Valley. Other wineries also joined the “cult” revolution, including Harlan Estate, Opus One, Dominus, Scarecrow, Colgin, Joseph Phelps, and Sine Qua Non.

Indeed, these are the brands that would shape the Californian fine wine market – and would enable other producers to leave their mark.

Secondary market overview

Trading background

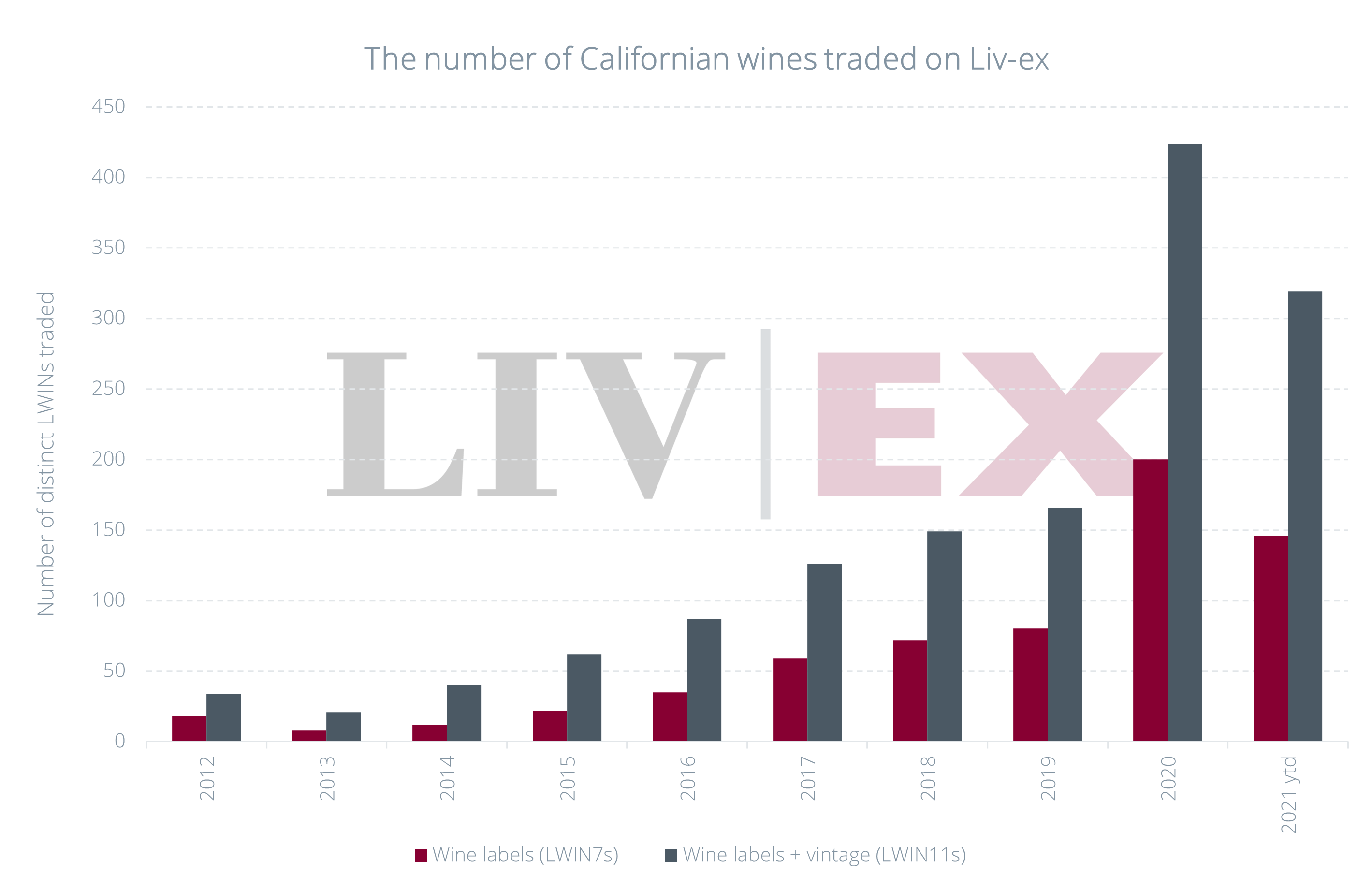

The first trade for Californian wine on Liv-ex happened in 2002. Contrary to expectations, it was a case of Kistler Vine Hill Vineyard Pinot Noir 1999 that kickstarted California’s secondary market presence. Yet it was California’s cult wines that quickly came to dominate trade.

2003 saw trades for Robert Mondavi and Ridge, and in 2004 Dominus and Opus One traded on the secondary market. Harlan made its first appearance in 2009, and garage winery Sine Qua Non saw its first trade in 2010.

The real tipping point, and a sign of things to come, was 2011 when the number of labels (LWIN7) traded rose from four to nine. This doubled again in 2012, from nine to 18.

In 2020, 200 different wines from California traded on Liv-ex, an 809% jump over five years.

The growth in brands trading has outpaced that of other regions which have also been on the move, such as Italy (373%) and Australia (286%).

Young vintages dominate year-to-date trade: 2018 (32.6%), 2016 (16%) and 2017 (14.5%).

The majority of Californian wine that attracts secondary market trade is red; amounting to 97.4% of US market share by value so far in 2021. Sauvignon Blanc and Chardonnay are also finding buyers, however. Oakville, Napa, and Sonoma Coast might just be the American Viticultural Areas (AVAs – official delimited, geographical grape-growing areas) to watch for quality whites in the near future.

Chart 1: The number of California wine traded on Liv-ex

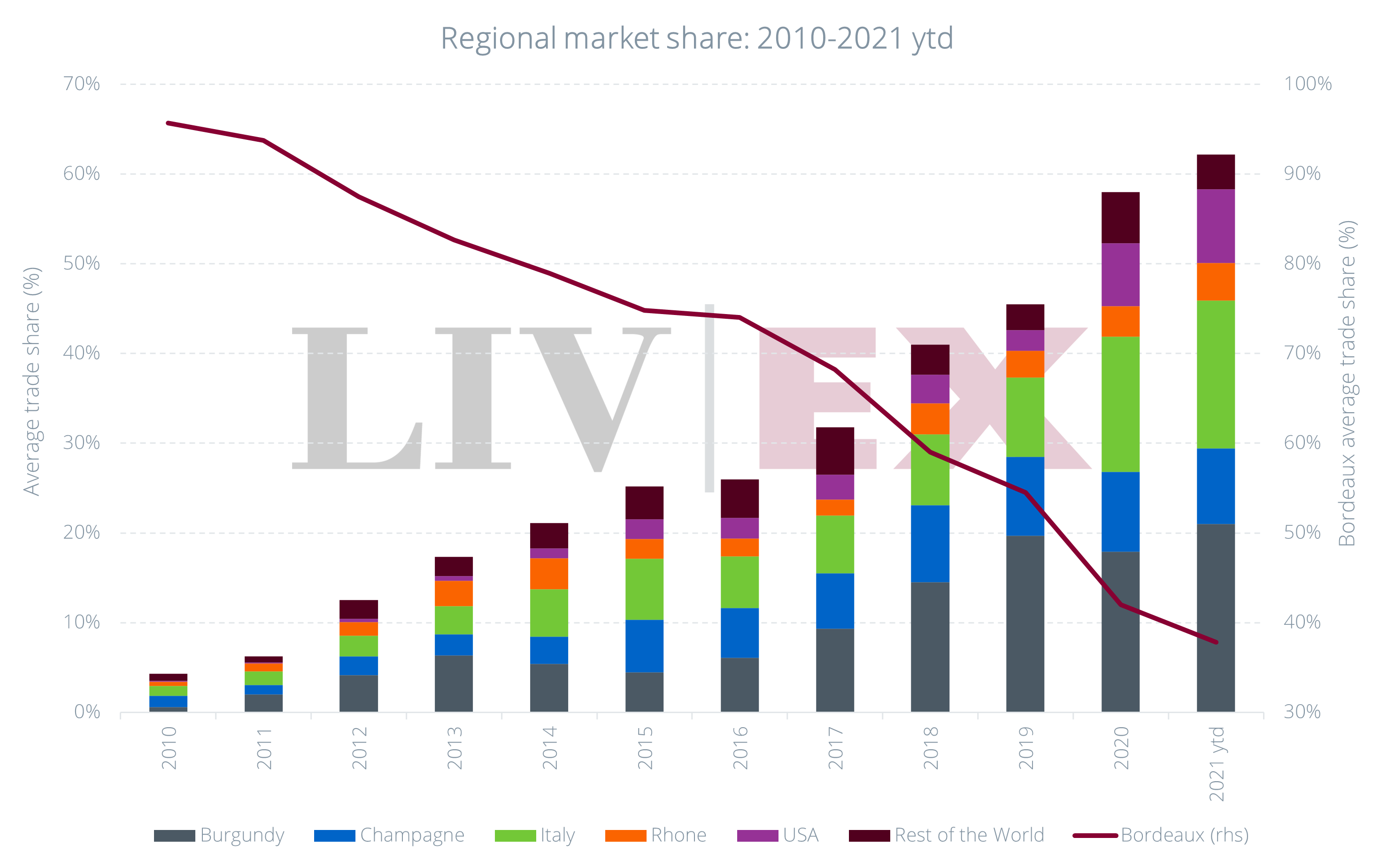

Regional market share

California makes up the majority of USA’s trade share by value, 99.5% in 2021.

It has thus been the main driver behind USA’s ever-growing influence on the fine wine market. Chart 2 puts things into broader perspective.

The USA’s trade share by value has risen from 0.1% in 2010 to 8.2% so far in 2021. It has taken up share from regions that traditionally dominated secondary market trade like Bordeaux, which has fallen from 95.8% of total trade in 2010 to 37.8% year-to-date.

Chart 2: Regional market share 2010-2021

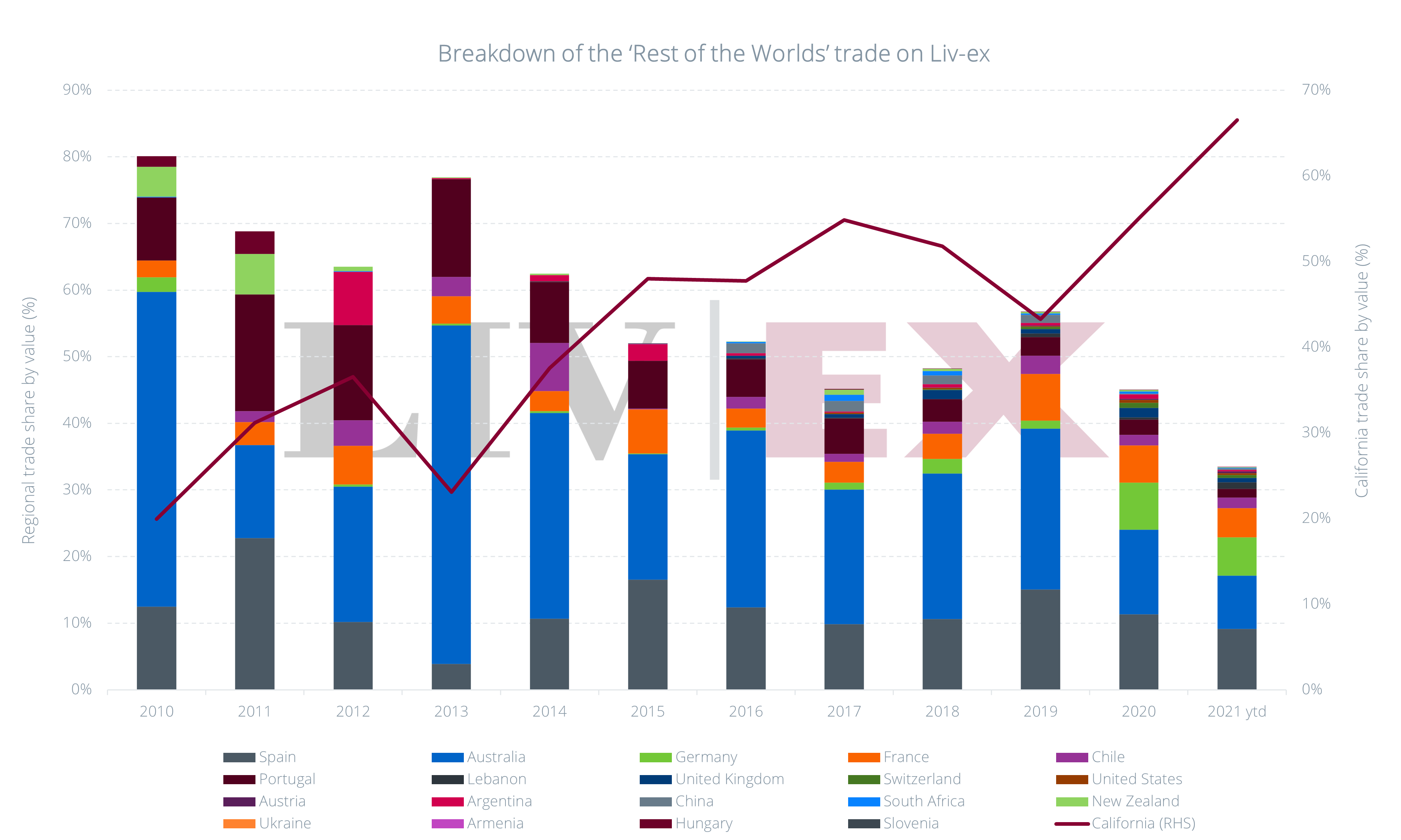

The USA has taken up the lion’s share of the ever-broadening Rest of the World (RoW) category, which also includes other European fine wine producing countries such as Spain, Germany and Portugal.

Driven by California, the USA’s increasing market share looks even more impressive when compared to fellow New World wine country Australia.

In 2010, the USA accounted for just 19.9% of RoW’s trade by value; Australia dominated with 47.3%. In 2021, this looks very different, with the USA taking 66.5% and Australia a mere 8%.

Chart 3: Breakdown of ‘Rest of the World’ trade on Liv-ex

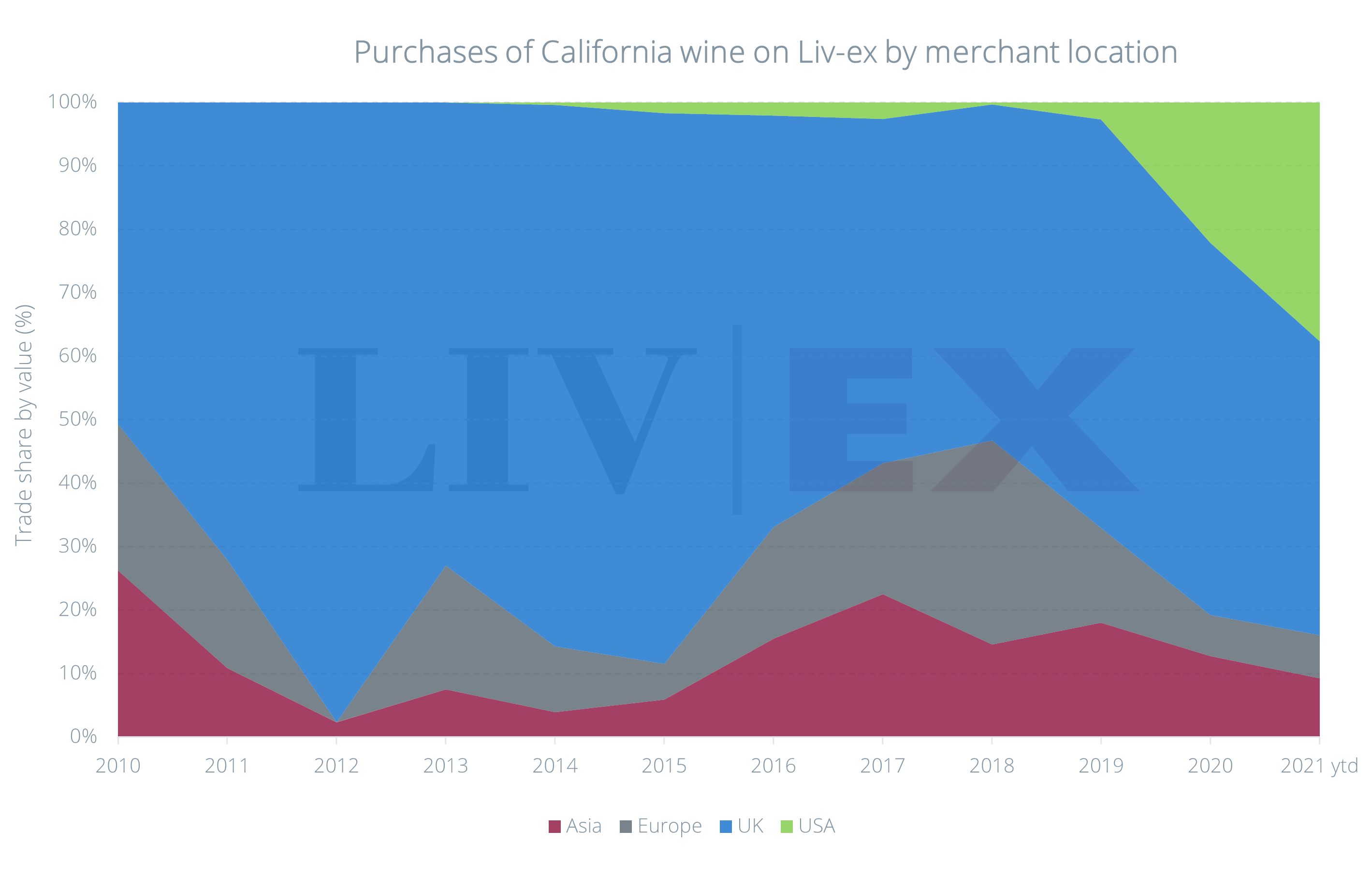

Where does demand come from?

According to the Californian Wine Institute, the top export markets for California wines in 2020 were Canada (US$424 million), the United Kingdom (US$236 million) and the EU (US$191 million).

On the secondary market, buying demand for Californian wine has historically been UK-driven. In 2019, UK buyers accounted for 64% of value trade for Californian wine. This has dipped to 46% year-to-date, partly due to an emerging US market, which has taken another 38% in 2021. The USA has long been an active seller of Californian wine, contributing to its global appeal. Now, US wine businesses are emerging as active buyers on the secondary market too.

Meanwhile, Asia’s share has continued to decrease, from 18% in 2019 to 9% so far this year, partly due to the ongoing economic slowdown in China and Hong Kong, and due to the tariffs placed on US wines.

Chart 4: Purchases of California wine on Liv-ex by Merchant location

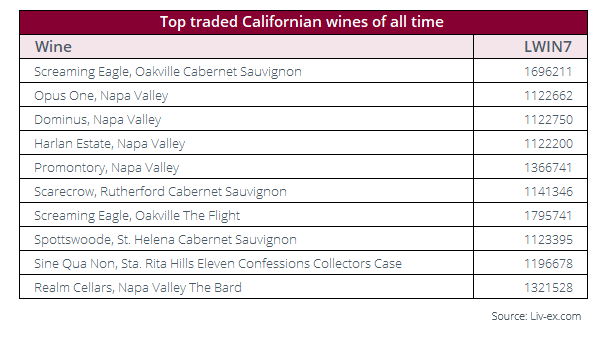

The most traded wines by value

Secondary market trade is still centred around a core of key brands. The most traded wines by value (LWIN7) can be found in the table below. Screaming Eagle tops the list, with Opus One and Dominus coming in second and third place.

Table 1: Top traded Californian wines of all time

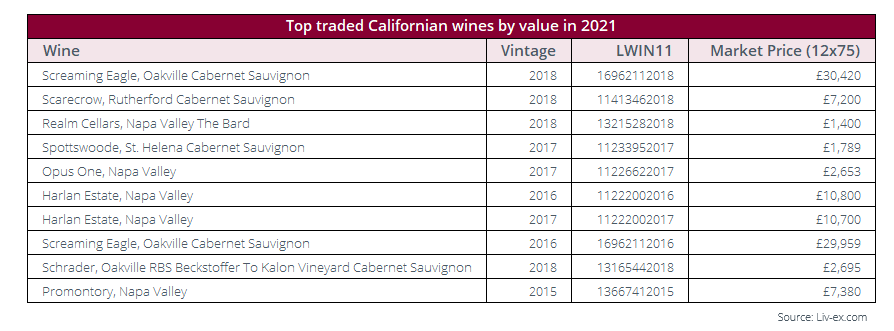

The list of the top traded distinct wines (LWIN11s) by value so far in 2021 is dominated by recent physical vintages of high-value cult wines. Although many of the wines in the table below have been released in the past year, they have already seen interest from buyers around the globe.

Harlan Estate features twice in the top 10, with its 2018 and 2017 vintages, as well as Screaming Eagle with its 2018 and 2016 vintages.

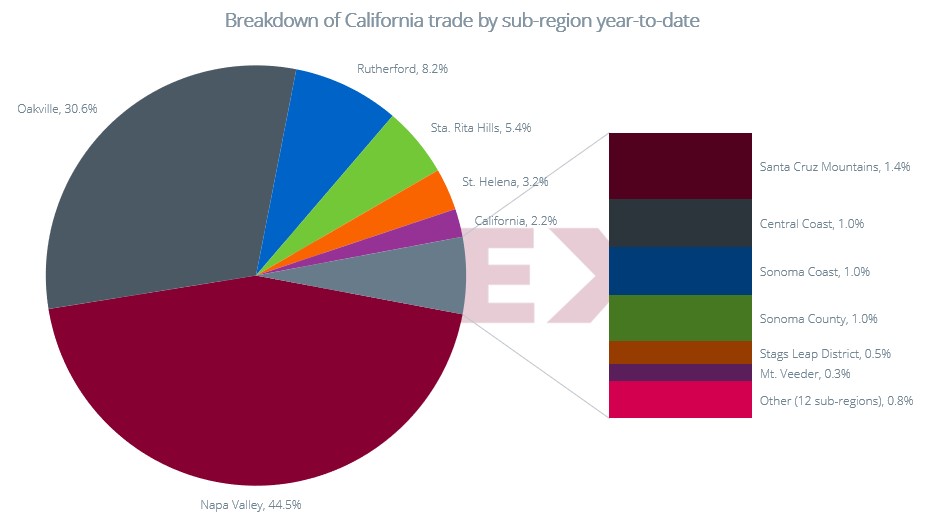

Delving deeper: diverse sub-regional trade

Perhaps not surprisingly, Cabernet Sauvignon-based wines from Napa still account for most trade. It is worth noting that Napa is home to some of the most expensive wineries and wine labels in the world, making its secondary market dominance somewhat incontestable. The impact of the broadening market has not bypassed California, however.

So far in 2021, wines designated as “Napa Valley” have accounted for less than 90% of California’s trade share by value, down from 93% in 2010, as other Californian regions and varieties have found new buyers.

Even within Napa, increasing demand for a wider array of wines has seen a growth in sub-regional trade for AVAs such as Oakville, Rutherford and Stag’s Leap. Wines from Howell Mountain (Abreu and Dana Estates) have been traded for the first time this year as well.

The Central Coast (1%) is largely represented by the boutique Sine Qua Non.

Chart 5: Breakdown of California trade by sub-region year to date

Napa vs Sonoma

Although Napa might lead the way for the most expensive and most traded wines by value, a wine from Santa Cruz has been the best performing wine index (as discussed in the next section of this report).

Napa’s flagship grape varieties are Cabernet Sauvignon, Chardonnay, and Merlot. It’s the home of benchmark wineries such as Robert Mondavi, Stag’s Leap, Chateau Montelena, Screaming Eagle, Duckhorn, and Rombauer. The more full-bodied style of many Napa wines often suggests ageing potential, which in turns makes them a collectible item.

Sonoma, meanwhile, is famous for its Chardonnay, Pinot Noir, Zinfandel, red blends and sparkling wines. Its flagship wineries include St. Francis, Ravenswood, Kendall-Jackson, and Francis Ford Coppola. While many have attracted investment interest, Sonoma is generally seen as a more accessible and diverse Californian region, with over 450 wineries ranging from small and independent, to larger top producers.

Other names of note from Sonoma that are starting to make waves on the secondary market include Vérité, Marcassin, Peter Michael, Aubert and Kistler.

Price Performance

Buying into the top tier

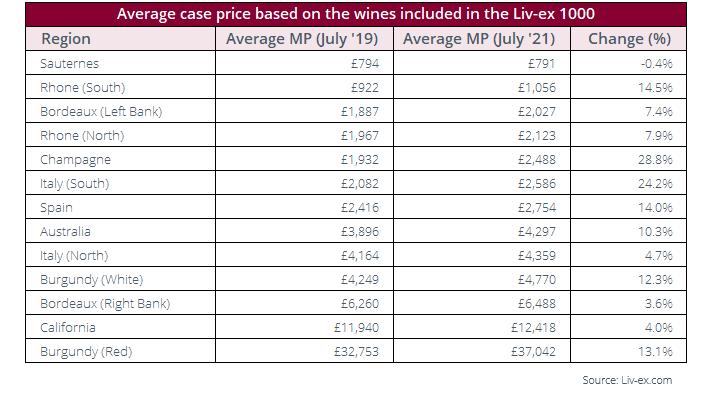

Prices for Californian wine are notoriously high, but where do they stand against other premium regions?

Looking at the average Market Prices of those fine wine labels in the Liv-ex Fine Wine 1000 index, we can see that the three Californian labels punch hugely above their weight. With an average case price of £12,418 (12×75), they are second only to red Burgundy.

This is chiefly due to the inclusion of superstar Screaming Eagle, however. It has an average Market Price of £30,957 per dozen, far above that of its fellow Americans in the Fine Wine 1000 – Opus One and Dominus – which cost just £2,602 per case on average.

This highlights the extremes of California. On the one hand, there are fine wines that cost as much as the average Super Tuscan, on the other there are wines that exist on an entirely different pricing plane. Taken together and there’s little doubt that the cost of entry to California is steep.

Table 3: Average case price based on the wines included in the Liv-ex 1000

Pricing patterns

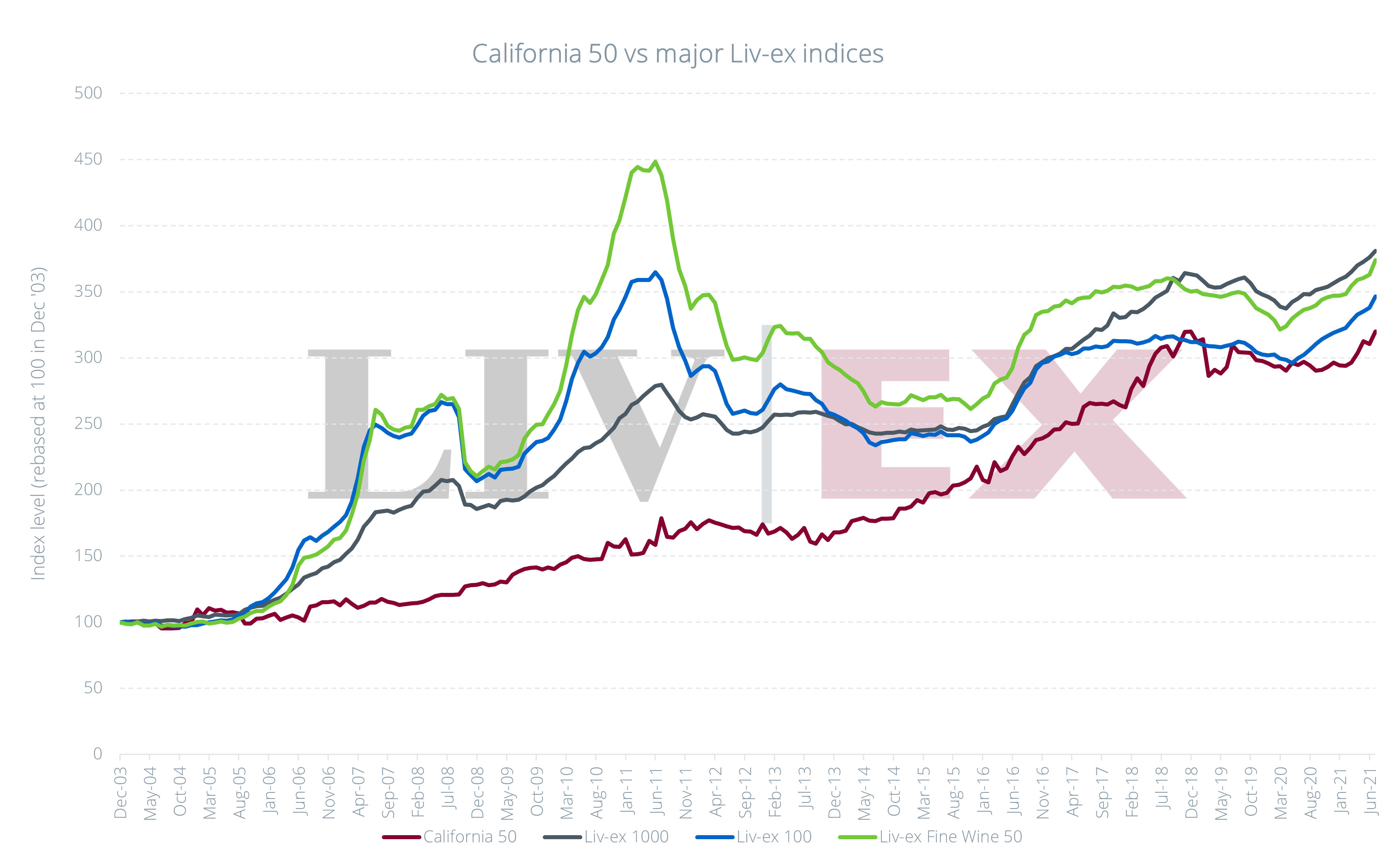

California’s secondary market price performance, however, has been characterised by low volatility and slow but steady increases over the past 18 years. In July 2021, the California 50 index reached an all-time high at 320, having risen 8.7% so far this year.

The California 50 index tracks the price movements of the last 10 physical vintages across five of the most traded brands (Dominus, Opus One, Harlan, Ridge, and Screaming Eagle). It has risen 220% since December 2003.

By comparison, the broadest measure of the market, the Liv-ex 1000, has appreciated the most, up 280%, pushed by a strong performance from Burgundy in 2018 and Italy in 2020. The Liv-ex 1000 does not include the California 50 index as a sub-index.

The industry benchmark, the Liv-ex 100, which is currently 55% weighted towards Bordeaux, is up 247% during the same period, while the Bordeaux First Growths, represented by the Liv-ex 50 index, have risen 274%.

Chart 6: California 50 vs major Liv-ex indices

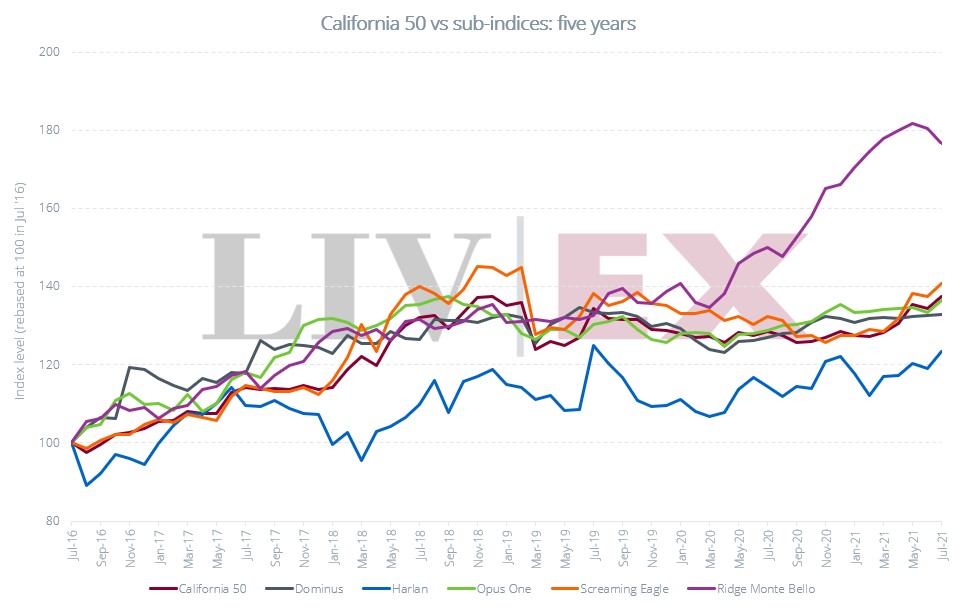

Individual wine labels performance

As alluded to above, Ridge Monte Bello is the best performing Californian wine label. Over the past five years, the Ridge index is up 76.6%, against 40.7% for Screaming Eagle, 36.6% for Opus One, 33% for Dominus and 23.4% for Harlan, which has been the slowest riser.

Ridge Monte Bello is the only wine from Santa Cruz in the index, and the most affordable among the five brands that comprise the California 50 index. Its production is also low compared with Bordeaux or Italy’s top labels (circa 3,000 cases), contributing to price appreciation. Traditional supply and demand dynamics, along with high quality at lower prices have meant that Ridge has had room to rise.

Chart 7: California 50 vs sub indices: five years

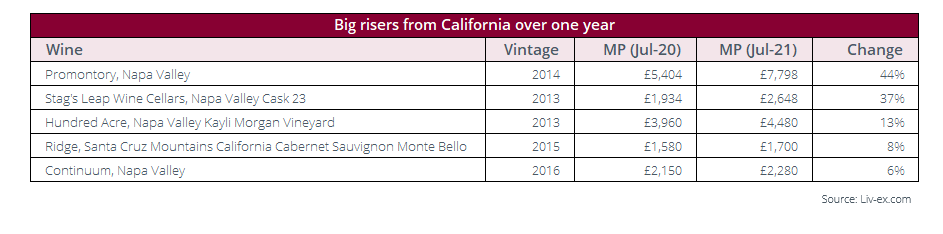

But it has not just been the California 50 index. Other wines from California have also moved in value over the past year – see the major movers in Table 4.

Table 4: Big risers from California over one year

The Snowball effect

Quality

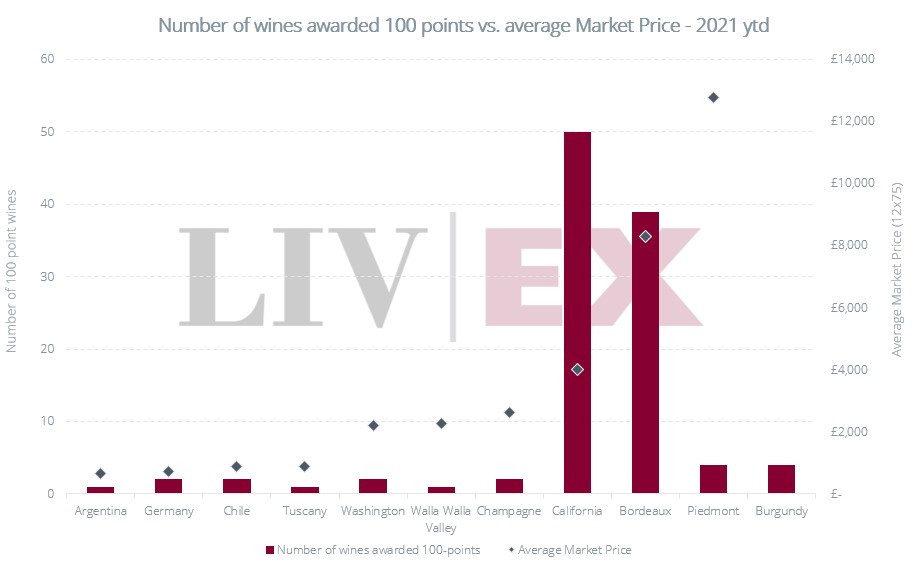

Vintage quality has played a key role in price formation. Critics have been full of praise for wines from all over the state so far this year. In-depth reports from Antonio Galloni (Vinous), Jeb Dunnuck, Lisa Perrotti-Brown MW (The Wine Advocate) and others have already netted California the highest number of 100–point wines awarded so far in 2021, as seen in Chart 8.

Chart 8: Number of wines awarded 100 points vs average Market Price – 2021 year to date.

*Average Market Prices for Burgundy are not included in the chart because the most recently scored vintage has yet to be released

Distribution

A contributing factor in California’s rising trade and prices has been the expansion of the distribution network, particularly as many leading brands have joined La Place de Bordeaux – the historic system of merchants used to distribute the wines of Bordeaux globally.

Each September La Place now releases some of the most in-demand and prestigious wines from other corners of the world, with an ever-expanding number from the US.

Opus One – Mouton Rothschild’s California collaboration with Mondavi – was the first to distribute exclusively via La Place back in 2004. It was a prescient step that others have since followed, including Vérité, Joseph Phelps and Inglenook. The wineries benefit from the well-established global network La Place offers, and in turn, they help bolster sales for the Bordeaux négociants (especially in years when En Primeur has struggled).

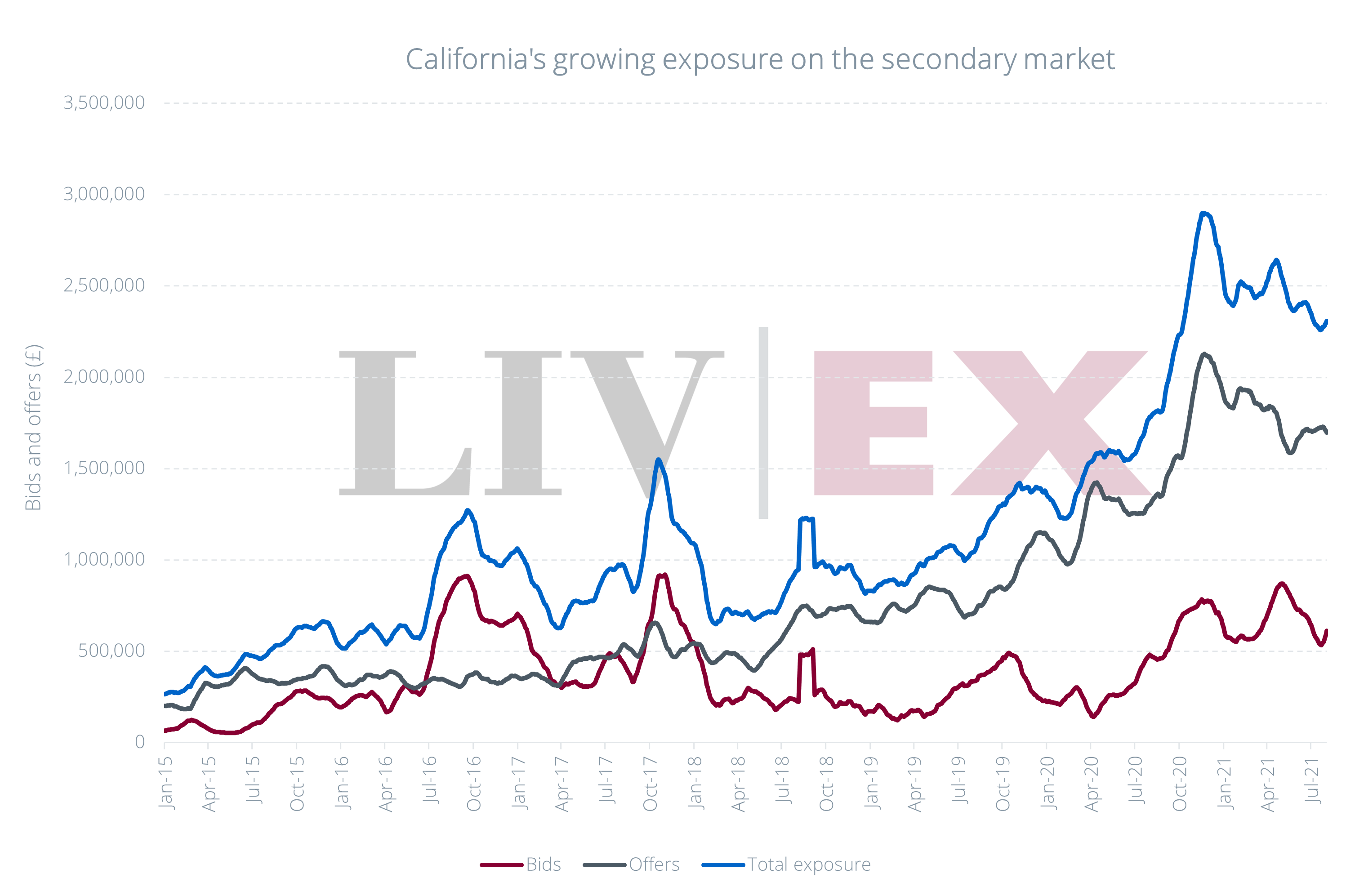

Growing exposure

Increased distribution has led to California’s growing exposure on the secondary market. This usually rises in September, when new La Place releases hit the market. The seasonality of the rise in bids and offers is reflected in Chart 9.

Chart 9: California’s growing exposure on the secondary market

The future of California

In the last few years, unprecedented droughts and fire events have put a question mark over the future of California as a wine region, however.

Wineries and vineyards have been destroyed by fires and crops tainted with smoke. The cost of water is also rising, piling the financial pressure on numerous operations across the state, not only those impacted by wildfires.

The fires in 2020 proved particularly devastating. There is a steadily growing rollcall of estates, including the likes of Colgin and Schrader, which have already announced they will be producing no wine from that vintage at all.

The exact impact of these natural hazards on the secondary market is less clear but producers in California are facing climate change challenges whose effects are bound to have knock-on repercussions for the trade and collectors at every stage.

The USA: Outside the Golden State

While California is the focus of this report, other US regions have also attracted secondary market trade in recent years: Oregon (0.2%) and the Washington/Oregon AVA of Walla Walla Valley (0.2%) which is outpacing Washington State (0.1%).

Trade in the wines of Oregon has been centred around its Pinot Noir and dominated by the vintages 2014 and 2013.

Walla Walla Valley has seen secondary market trade for its top Syrah, and vintages 2016, 2015 and 2014 have been the most active.

Wider Washington State, meanwhile, has seen active buying of its Cabernet Sauvignon and red blends, with the vintages 2016, 2005 and 2013 leading the way.

All three regions have seen the number of wines trading triple over the past three years.

Conclusion

After years of revving its engines on the fringes of the fine wine market, the full power of Californian wines’ turbocharged v8 is now being felt.

Modern and shiny, the region is not losing its momentum any time soon. Cult wineries dominate the very top tiers, but diversity abounds.

Few other fine wine regions offer high-quality and collectible Pinot Noirs as well as Cabernet Sauvignons, Chardonnay and Sauvignon Blanc, Zinfandel and Rhône blends. Thanks to over 139 AVAs and counting, the Californian wine market is undergoing a massive expansion. Sub-regional trade is deepening and broadening.

The rising tide of demand prompted Liv-ex to launch a weekly stock collection service to members across the Golden State. Retailers in the state therefore have a new opportunity to sell local wines, facilitating trade.

The recent announcement of the UK’s scrapping of VI-1 forms comes with far-reaching implications that could certainly boost California’s secondary market still further. This change promises to remove import certification from all wine imports and level the playing field by making it substantially easier for the UK trade to buy wines from both inside and outside the EU. The anticipated result: more choice and better prices.

California is well-poised for future growth in the secondary market and shows little sign of slowing down.