Print and read offline instead.

Introduction

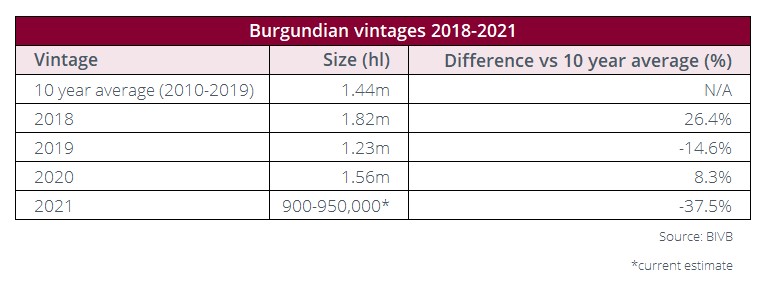

The 2020 Burgundy vintage, deemed high quality across both colours, finds itself squeezed between two low-yielding years. Scarcity, the main driver behind Burgundy’s spiralling prices, presents less of a concern this year, but future shortages are looming in the background.

In some cases, but by no means all, producers are releasing full allocations to merchants and importers, to make up for the imminent shortfall. Meanwhile, the trade continues to report an insatiable global buying appetite that has led to reduced allocations to collectors despite another year of rising prices. Merchants are allocating ever greater numbers of premier and grand crus in three-packs.

Price increases are not limited to the primary market. The 2020 vintage is being offered into the teeth of a bull market for Burgundy that, bar an 18-month pause in 2019 and 2020, has been running hot since 2015. The industry benchmark, the Liv-ex Fine Wine 100 index, has (at the time of publication) recorded 20 consecutive months of gains.

Burgundy was heavily represented in last year’s top price performers. Over the past year, the region has challenged Bordeaux as the fine wine market’s dominant force. For a few years now, Burgundy has been outperforming in terms of prices, but recent weeks have also seen it dominate trade share. So far in 2022, Burgundy has been the most traded region by value, taking 28.8% of the market against Bordeaux’s 25.7%.

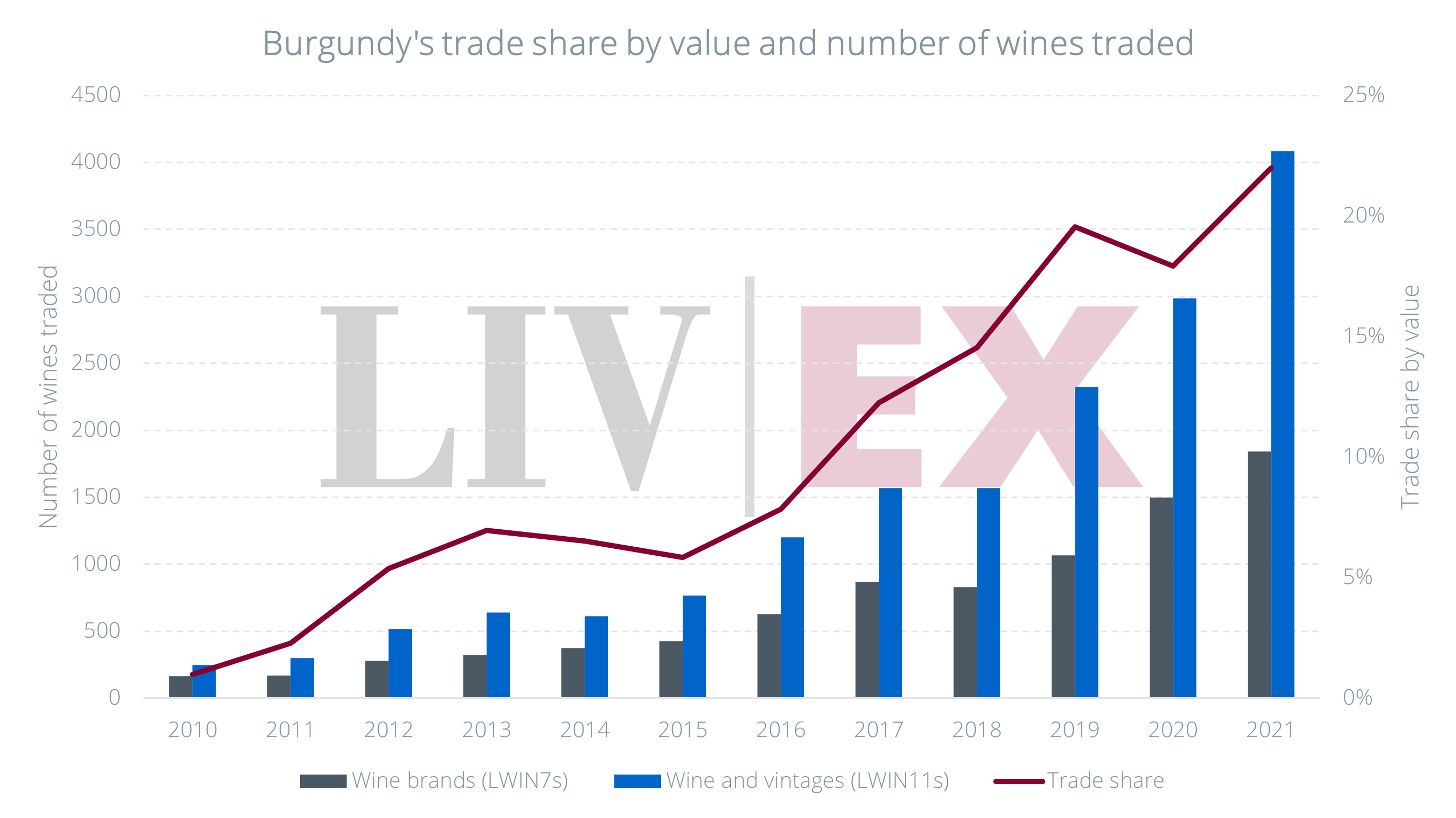

The number of Burgundian wines trading has climbed above all other regions, with 4,084 different wines (LWIN11s) changing hands on Liv-ex in 2021.

The broadening of the Burgundy market is a continuation of the trends set in recent years; buyers searching for value (or stock) within the regions’ appellations. As last year’s report, Burgundy: A journey of discovery suggested: ‘If just five years ago, the secondary market for Burgundy belonged to a strong but restricted group of traditional heavyweights, now its diversity is on full display’.

Indeed, current live bids on Liv-ex range from £24 per 3×75 to £95,000 per 3×75. There is demand at every level.

But Burgundy’s positive performance on the secondary market is complicated by the question of production. Will the ample 2020 vintage satisfy the seemingly insatiable market demand? With a dramatically reduced 2021 release in the offing, few believe it will.

State of the 2020 vintage

‘The reference point of where Burgundy’s sweet spots are, has been changing’. – Jasper Morris MW

Initial reviews of Burgundy 2020 point to a high-quality vintage. Tasting reports suggest that it is the first vintage since 2015 to be equally strong for reds as for whites. Purity of fruit, intensity, density, ripeness and acidity come up as key descriptors. According to Jancis Robinson MW, 2020 is ‘remarkably successful’ across the board, ‘with ripeness and freshness in both colours’.

The vintage was characterised by an unusually long growing season, warm summer, and one of the earliest harvests on record. For many producers, all the grapes were picked by the end of August. For one of the oldest estates in Burgundy, Bouchard Père et Fils, 2020 was apparently the earliest harvest in 300 years.

Climate conditions lead to stylistic variations

While quality is reportedly high across the board, merchants are widely advising their clients to buy whites from top to bottom but pointing out stylistic variation with the reds. The summer drought concentrated sugar and acidity in the Pinot Noir, resulting in higher alcohol (broadly between 13.5%–14.5%) and high acidity. However, vineyard location, terroir, the aspect of the vineyard, vineyard management and vinification have all made huge differences.

Burgundy expert Jasper Morris MW told Liv-ex that the ‘three excellent recent white wine vintages – 2014, 2017 and 2020 – share the fact that they are really successful everywhere’.

For the reds, Morris pointed out that there were more noticeable differences between producers and sites. He said that, ‘the reference point of where Burgundy’s sweet spots are has been changing’; a change he linked to climate conditions.

‘Areas, somewhat overlooked in the past, that can retain more moisture like Pommard, have done really well in these hot dry vintages,’ said Morris. Conversely, areas that tend to ripen early because the vineyards are more exposed, like Volnay, have been more at risk. Therefore, choosing the right picking date has become an essential skill.

In his Burgundy 2020 report for Vinous, Neal Martin concurred. He wrote: ‘On reflection, while terroir naturally plays an important role across all the 2020 reds, the crucial decision on picking date seems to govern style and quality as much as or, at least at this early stage, even more than location’.

Variable volumes

Although outwardly the 2020 vintage sees a return to ‘healthy’ volumes, the detail is more nuanced. To begin with, it is squeezed between the low-yielding 2019 vintage and the miniscule 2021 – the result of destroyed crops and halved yields in an immensely challenging year.

Moreover, like quality, volumes have been inconsistent in 2020, especially with the reds.

According to Morris, many growers in 2020 had, ‘yields for the reds about [the same] or less than in 2019’. In parts of the Côte de Nuits, both 2020 and 2021 have been ‘reduced to about half a crop’. In the Côte de Beaune, 2020 volumes are above 2021, but still very reduced.

On the other hand, the amount of white wine produced in 2020 makes up for the shortfall of the reds. Yields for the whites have been just below the maximum permitted, at around 40-45 hl/ha. Morris says that many growers ‘have made just 10%-20% off where they would like to be, and for some, it’s exactly right’.

‘There is no need to worry about volumes too much; except that in the whites, they have made virtually no wine in 2021,’ he continued. ‘So they have to take that into account’.

Supply puts pressure on pricing

Morris explained that supply shortages have often led producers to release full allocations to importers in 2020, rather than in the usual two instalments. Allocations are generally above the 2019 offers but below the bumper 2018 provisions. Prices are up markedly, with smaller increases for the lower value wines but bigger for the high-end ones, in part due to the quality but also because of the next vintage on the horizon.

‘Everybody has got to think about what they’ve got the following year. Therefore, they have made their pricing high not just because it [2020] is a good vintage, which is clearly going to be in demand, but also because they have to make up for the shortfall next year,’ said Morris.

‘What they don’t want to do is keep the price level in 2020, and then put it up hugely in 2021. It makes much more sense to do it across the two years than in one go’.

No ceiling for Burgundy’s prices

As prices continue to rise, many question if there will ever be a point Burgundy buyers eventually capitulate and call it quits.

Despite the trade and customers voicing pricing concerns, Morris suggested that the continuing lack of stock is a tell-tale sign that Burgundy always seems to find a market, older vintages and new releases alike.

‘The high-end wines benefit from an international audience, and prices are rising more strongly than the regional wines where the audience has a finite budget,’ he added.

The following section examines the price performance of Burgundy’s top wines and how it has led to a secondary market expansion.

State of Burgundy’s secondary market

‘The secondary market for Burgundy thrived in 2021, recording new record levels of trade and its highest ever share of the overall market. Blue-chip labels continued to command significant attention even as the category broadened to encompass new growers and appellations, a trend that will likely continue in 2022’. – Anthony Maxwell, Sales Director at Liv-ex

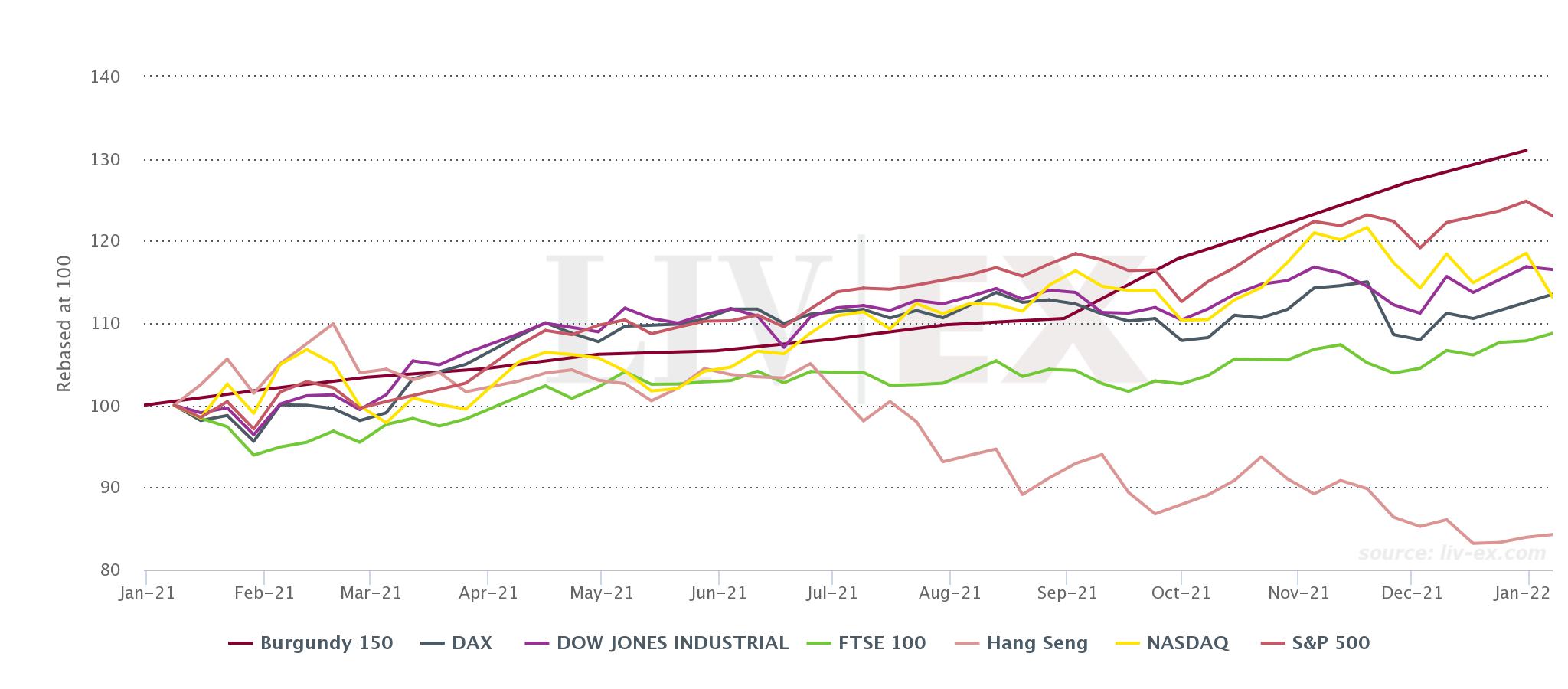

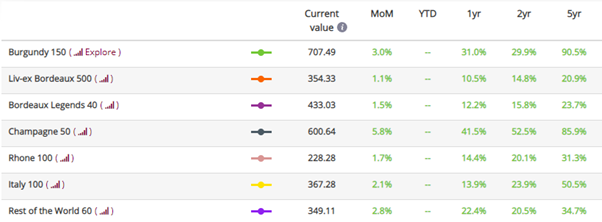

The 2020 Burgundy vintage arrives in a boom time for the secondary wine market. Demand and trading activity for Burgundian wines are at an all-time high and prices are rising faster than ever. In the past year alone, the Burgundy 150 index, which tracks the performance of the most traded Burgundian names, has risen 31.0%.

The index has outperformed mainstream equities, including the S&P 500 (23.0%), Dow Jones Industrial (16.5%) and the FTSE 100 (8.8%), proving that top Burgundian wines were a better investment than most stocks in 2021.

Burgundy outperforms equities in 2021

*made with the Liv-ex Charting tool.

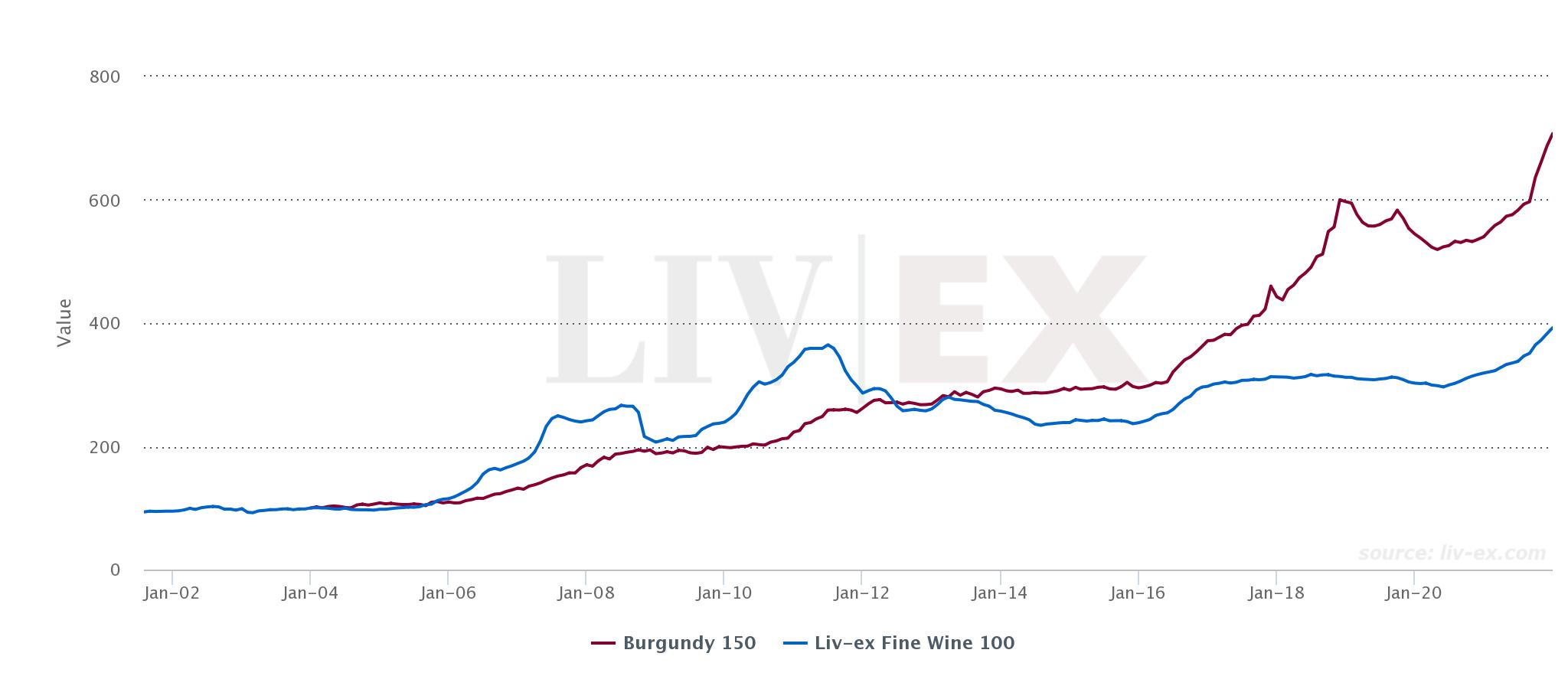

A long-term champion

Burgundy is a long-term winner. Since the index’s creation in 2003, the Burgundy 150 has delivered almost double the returns of the Liv-ex 100 index, the industry benchmark.

In 2021, the Burgundy 150 surpassed its November 2018 peak (599.99), ending the year at a new level of 707.49.

After a combination of US tariffs, Brexit uncertainty and the Covid pandemic slowed its progress in 2019/2020, it has only rebounded stronger than ever.

Burgundy 150 vs Liv-ex 100 index

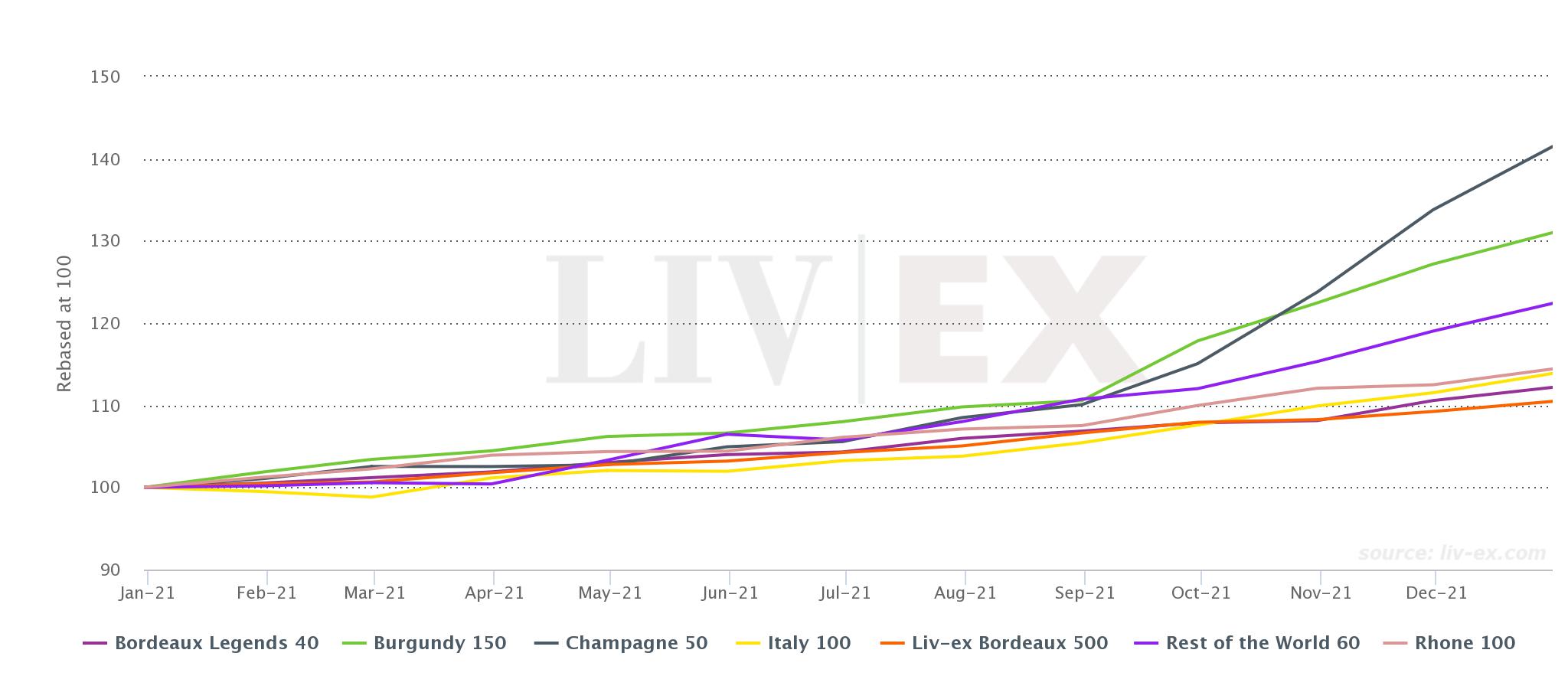

Burgundy versus other fine wine regions

Burgundy outperformed most other regions in 2021. The Burgundy 150 index was the second best-performing Liv-ex 1000 sub-index, surpassed only by the Champagne 50 (41.5%).

Liv-ex 1000 sub-indices performance in 2021

Burgundy overtakes Bordeaux in value traded in early 2022

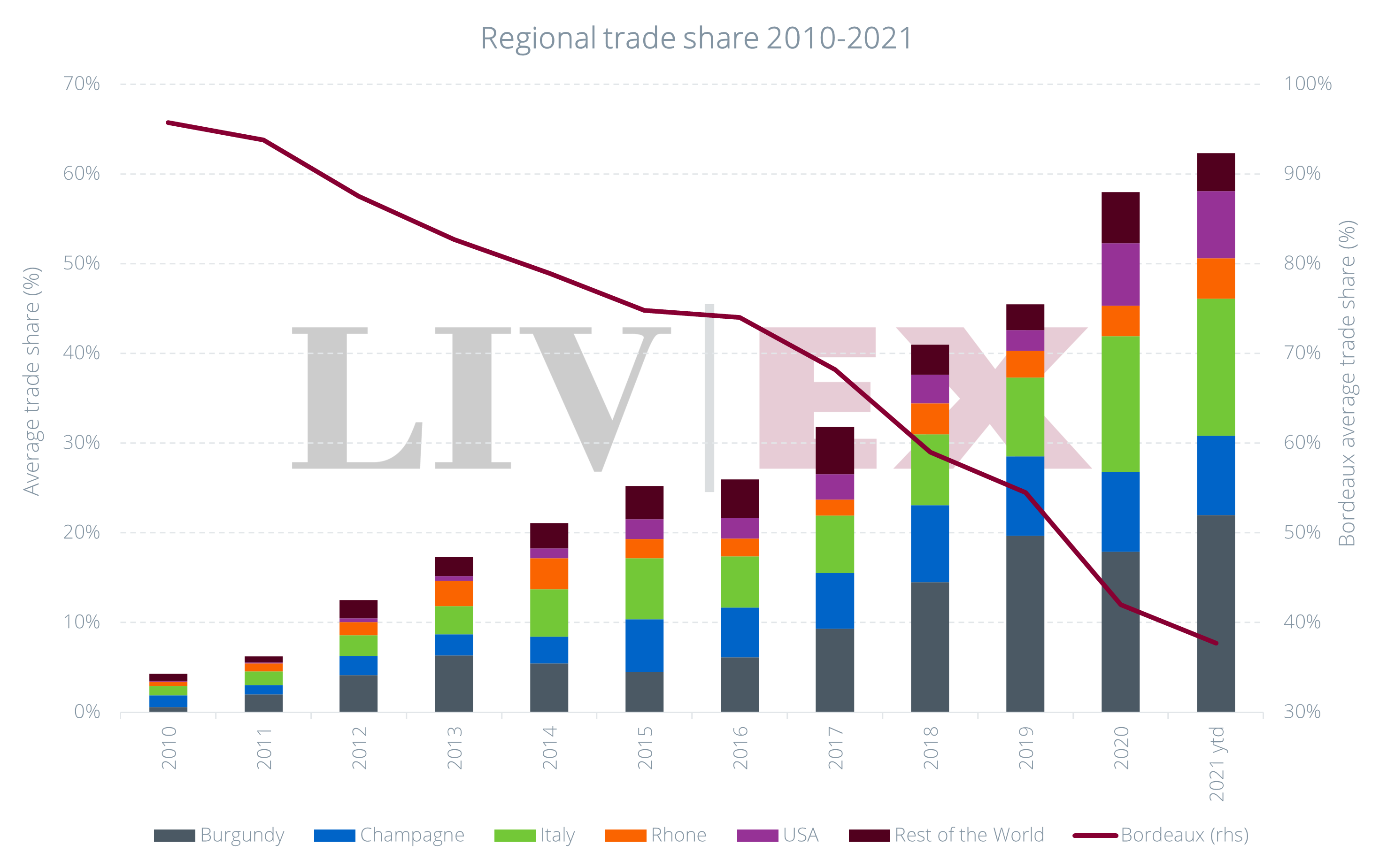

Since the start of 2022, Burgundy has been the most traded region by value (28.8%), overtaking the longest standing secondary market player, Bordeaux (25.7%).

In 2021, Burgundy’s trade share of the total market by value hit a new high of 22.0% (its previous highest share of trade was 19.7% in 2019).

In some markets, its dominance was even more pronounced. In the UK, for instance, Burgundy established itself as the most traded fine wine region last year, taking 31.5% of total trade versus 28.1% for Bordeaux.

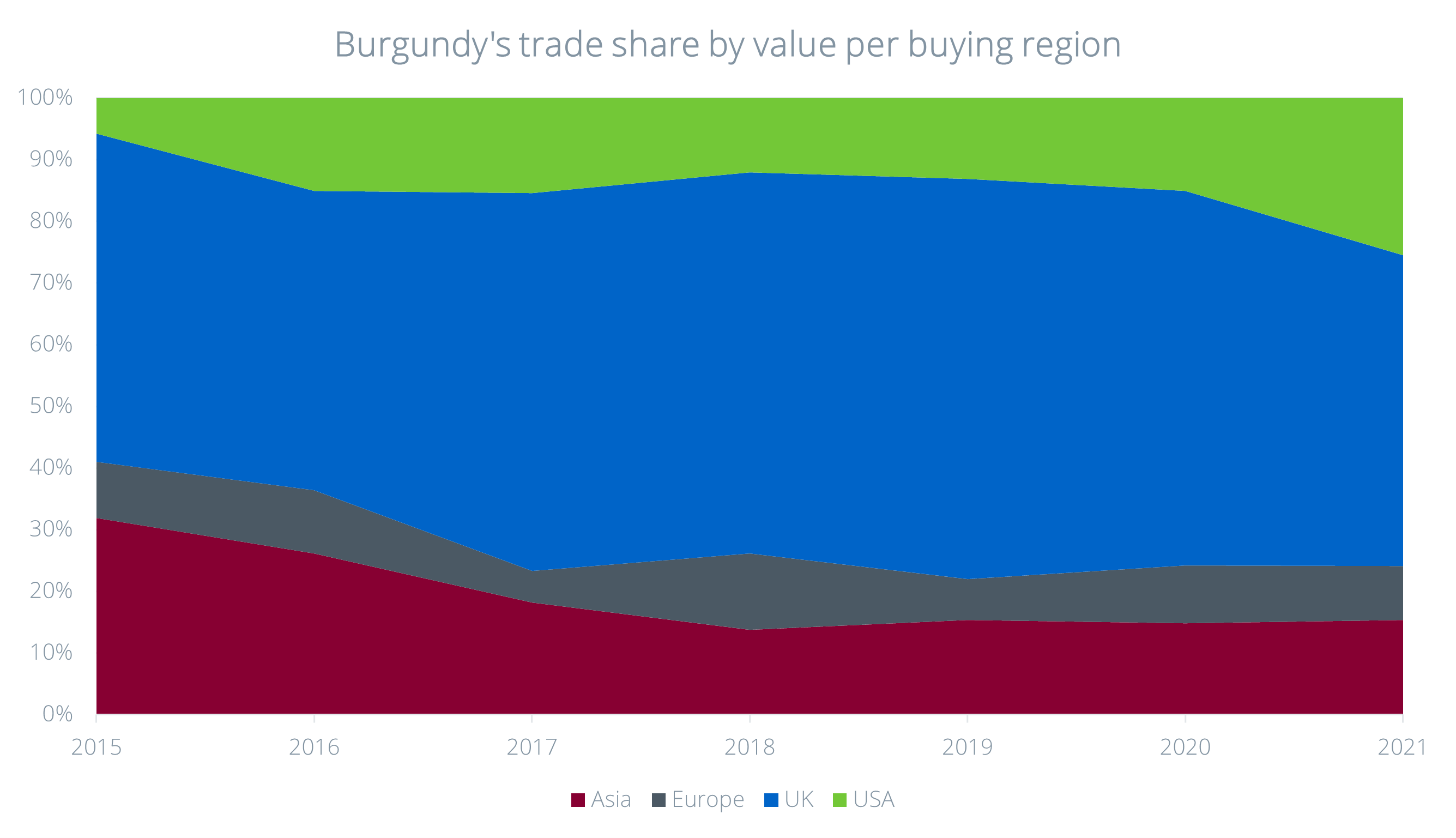

Burgundy benefits from more US buying

While the UK remains its main market, accounting for half of the value traded, Burgundy also benefitted from its wider international renown in 2021, enjoying renewed interest from Asia.

More impactful, however, was the lifting of the US trade tariffs, which were suspended in March and formally abolished in June. US buyers were eager to replenish their supplies of many classic European wines and the US’s share of Burgundy buying rose from 15.1% in 2020 to 25.5% in 2021.

The fine wine market’s most tradeable asset

Buying demand was spread across more than just the top-end wines. The number of different Burgundian wines trading (LWIN11s) rose 36.8% year-on-year in 2021.

Burgundy was the region with the highest number of wines trading in 2021 – 4,084 in total. Could diversity be the solution to Burgundy’s pricing bubble?

As our annual Fine Wine Market in 2021 report highlighted, the Burgundy market is undergoing a massive expansion as price conscious buyers seek value within the region’s appellations.

Are rising prices enhancing secondary market diversity?

The record number of Burgundian wines attracting a secondary market is a testimony to buyers’ willingness to explore. Rather than moving to other Pinot-producing regions, they are turning their attention to less famous villages and communes within Burgundy.

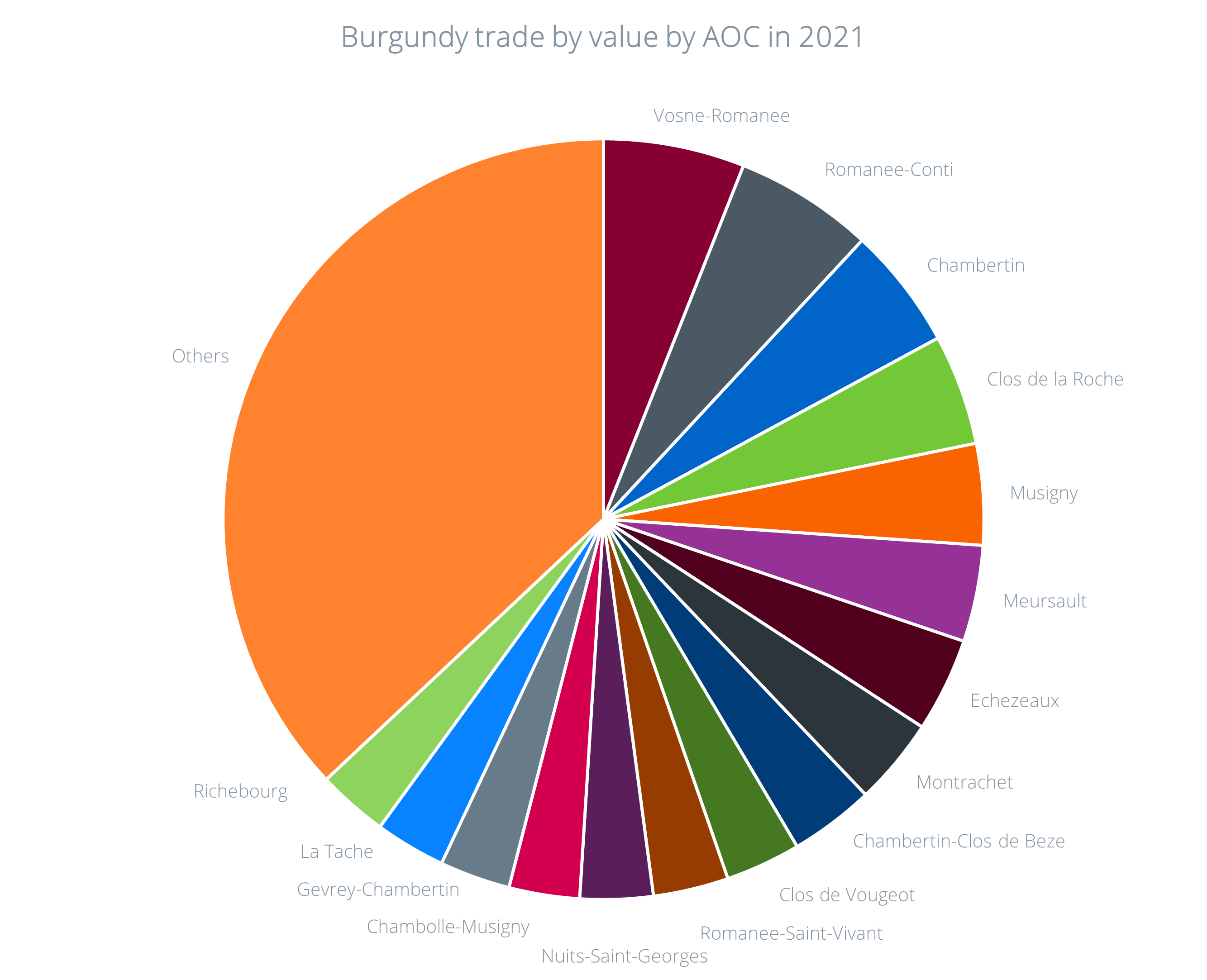

In 2021, wines from 73 Burgundian AOCs traded on Liv-ex, and there has been a change in the nature of trade across these regions.

In 2020, for instance, 12 Burgundian AOCs had a trade share of 3% or more of total Burgundian trade. Last year, 16 appellations had share of 3% of more.

The change in Burgundy buying was also evident in the appellations that were traded most. The top-traded AOCs (by value) in 2020 were Romanée-Conti (8.3%), Chambertin (6.0%), Vosne-Romanée (5.8%), Montrachet (4.2%), Musigny (4.2%) and Meursault (3.9%). In 2021, Vosne-Romanée (6.0%) took the top spot, followed by Romanée-Conti (5.9%), Chambertin (5.9%) and Clos de la Roche (5.2%).

It is worth noting, however, that while some AOCs saw their share of overall Burgundian trade decline, the value of their trade in 2021 was still greater than it was in 2020, as a result of the region’s broadening secondary market. For example, the total value of Romanée-Conti sold in 2021 was greater than in 2020 even as its share of Burgundian trade declined from 8.3% to 5.9%.

Meanwhile, communes that in the past were less prominent in the secondary market made up a third of the total trade last year. These included Pommard, Morey-Saint-Denis, Clos de Vougeot, Aloxe-Corton, Montagny, Mercurey and Rully, among others.

Critics have noted that previously undervalued areas are increasingly impressing with their quality. As Neal Martin put it in his latest report, ‘forget the notion that Grand Cru > Premier Cru > Village Cru > Regional. It is a framework for potential quality. But there is fluidity between ranks, so that premier crus can surpass their grand cru, village crus punch at premier quality, and so on’.

Jasper Morris partly attributes this trend to a generational shift in Burgundy:

‘I really couldn’t imagine someone buying Volnay and Vosne-Romanée trading down within Burgundy. But what we didn’t take into account is the incredible energy of young people either taking over family domains or creating something themselves from scratch, working with less famous appellations, making wines which are just absolutely gorgeous. I am so excited by what I’m tasting. It’s scratching the Burgundy itch for me.’

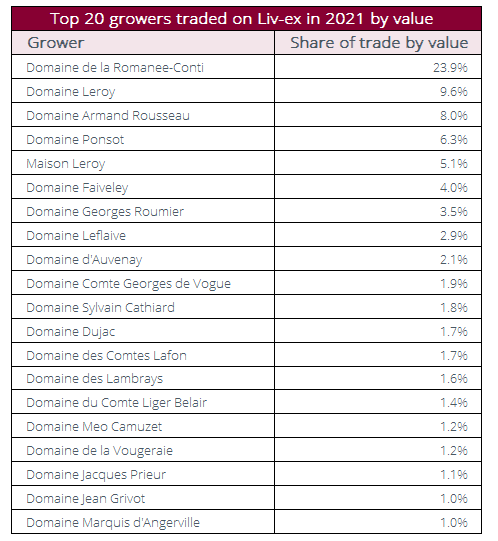

In line with the trend of more Burgundian AOCs trading, wines from 166 Burgundy growers traded on Liv-ex in 2021, up from 156 in 2020 and 78 in 2015.

Conclusion

Rising Burgundy prices have not discouraged buying. On the contrary, they have led to greater diversity and a more robust market.

Building on its muscular performance last year, and perhaps spurred on by the favourable commentary surrounding the current release, Burgundy has become the dominant fine wine region in terms of price performance, number of wines trading, and trade share in these early weeks of 2022.

It is an enormous leap, considering that only a decade ago it accounted for a mere 2.3% of the market by value. Back then, trade was focused almost entirely on Domaine de la Romanée-Conti and Domaine Leflaive. Today 166 domains are enjoying active and sustained demand.

The trade is reporting strong sales of the 2020 vintage but supply shortages remain a major concern. Tight allocations for premier and grand crus mean eager Burgundy buyers will have to continue their journey of discovery into different appellations if they wish to keep their cellars stocked with the region’s wines.

The market for Burgundy is both exciting and uncertain. The continued squeeze on supply as a result of global demand and a string of small vintages will be especially evident next year with the release of the 2021 vintage.

The ‘Burgundian paradox’ suggests that the harder wines are to find and the more prices rise, the greater the demand seems to be. But not necessarily across the board. The air is getting increasingly thin at the very top. The higher the prices, the fewer the buyers. The more expensive a particular domain or appellation becomes, the more buyers double down on seeking viable alternatives within Burgundy, fuelling its growth in the secondary market.

If this were any other region, buyers would surely have decamped to another source for their fill of Pinot Noir or Chardonnay. But Burgundy’s spell is compelling and as winemakers both young and old continue to deliver exceptional wines and create new ‘sweet spots’ across appellations, so they keep giving collectors reasons to return.

As long as this remains the case, the onward march of demand and prices seems assured.