Bordeaux 2023 – In the Balance

Introduction

Bordeaux is, and has been for centuries, the most important fine wine region in the world. No other region has come close to matching its ability to produce benchmark wines in large quantities over a long history. This prominence has come with great scrutiny, both of quality and of price. To a large extent, this is justified: a long and complex supply chain of businesses is dedicated to supporting the promotion and sale of Bordeaux wines. In turn, many of these businesses depend on its wine for much – or even all – of their annual revenue. Missteps are costly for many players.

With this, there has rarely been a moment in recent history where commentors have not closely scrutinised Bordeaux prices. Just last year, in our En Primeur concluding report, Where is the Magic?, we suggested that the campaign offered “little compelling value” to buyers. Would we have been happier 15 years earlier? If Robert Parker’s 2005 vintage report is to be believed, the answer is no. In it, he was similarly unhappy about Bordeaux’s “astonishing price climbs”.

The picture was no rosier in the 1980s. In 1986, English Journalist Auberon Waugh wrote that “only the very rich” could buy top Bordeaux, compared to “fifteen years ago [when] any well-off person could reckon to fill his cellar” with these wines. But fifteen years before that, in an article entirely dedicated to Bordeaux pricing, Terry Robards of the New York Times complained of the “seemingly endless escalation of price rises” for top Bordeaux.

Will we ever be satisfied?

Perhaps. Despite decades of upset over pricing, thirst for top Bordeaux has continued. Producers might therefore be forgiven for believing that their supply chain partners are crying wolf when warning against further price rises this year. With an awareness of this, the report that follows will reflect on the current position of Bordeaux in the fine wine market, the role of En Primeur within it, and what the chateaux’s decisions during this year’s campaign might indicate for the future of the region – and the future of En Primeur.

The fine wine market today

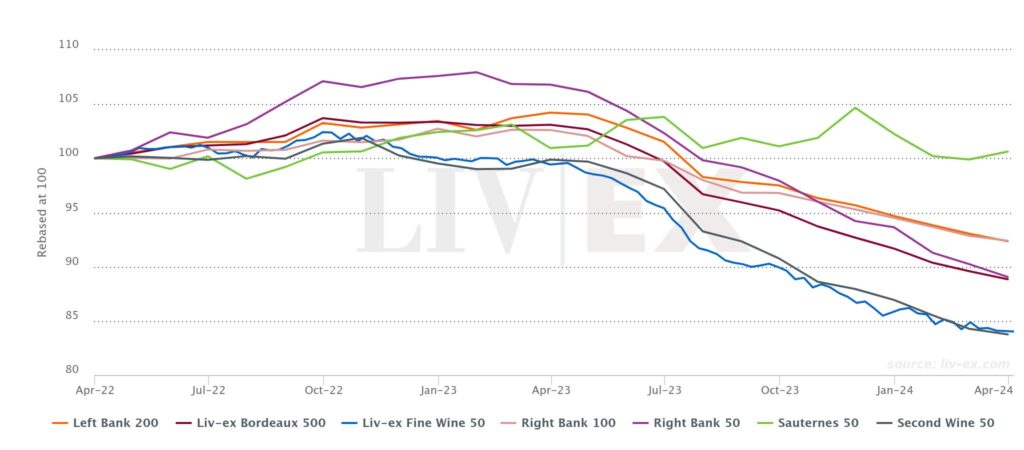

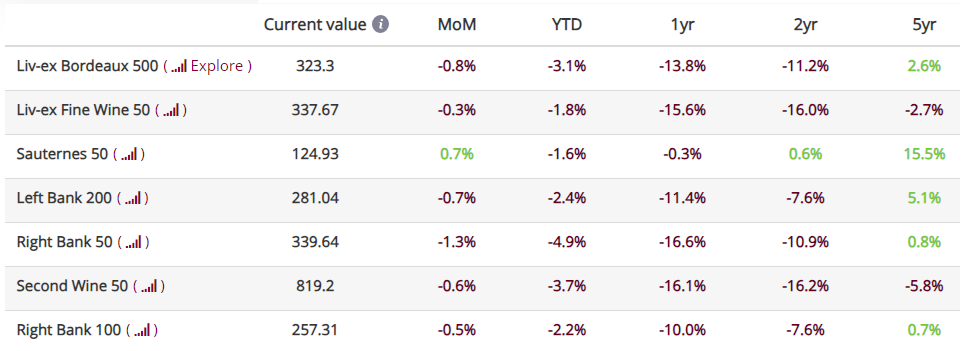

The market for top Bordeaux has been drifting for the past two years. Since February 2022, the Bordeaux 500 Index – the broadest measure of the Bordeaux fine wine market – has dropped 10.3%. The most collectible wines have fallen hardest: The Fine Wine 50 Index, which tracks prices of the five First Growths, is down 15.3%. In contrast, the Sauternes 50 Index, historically the most sluggish, has been the most resilient, holding steady (+1.6%) over the same period.

*Made using the Liv-ex Charting Tool

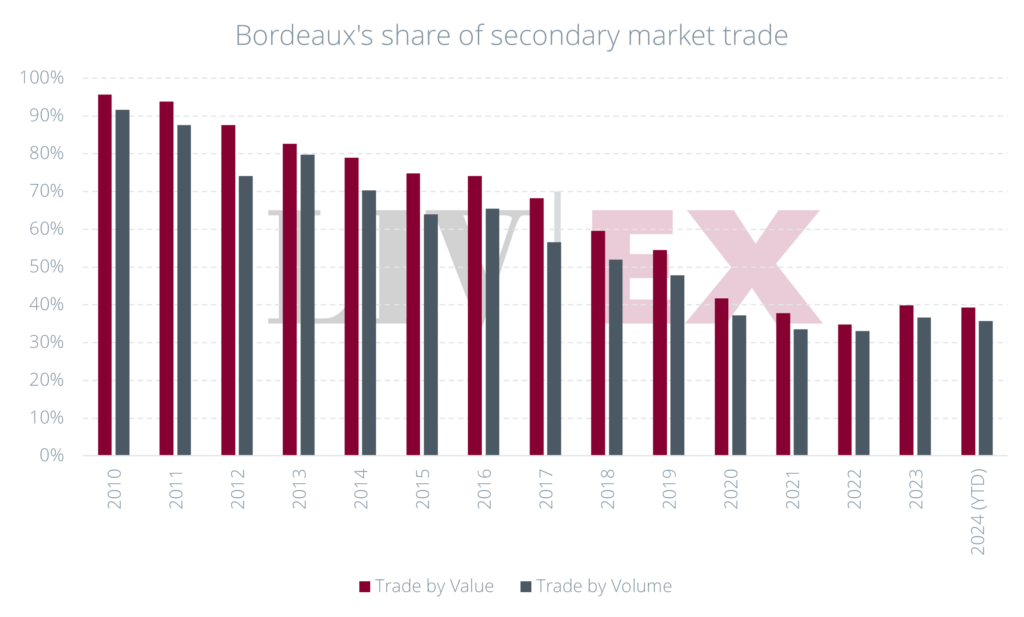

At the same time, Bordeaux’s share of trade on the secondary market has been declining as it gives way to other classic wines, primarily from Burgundy, Italy, Champagne, and the USA. As Chart 3 shows, in 2023, Bordeaux accounted for 40% of trade by value compared to 60% just five years earlier in 2018. This illustrates that while Bordeaux remains the single most important region for the fine wine market, it now shares far more of the spotlight with competing regions than it did even five years ago.

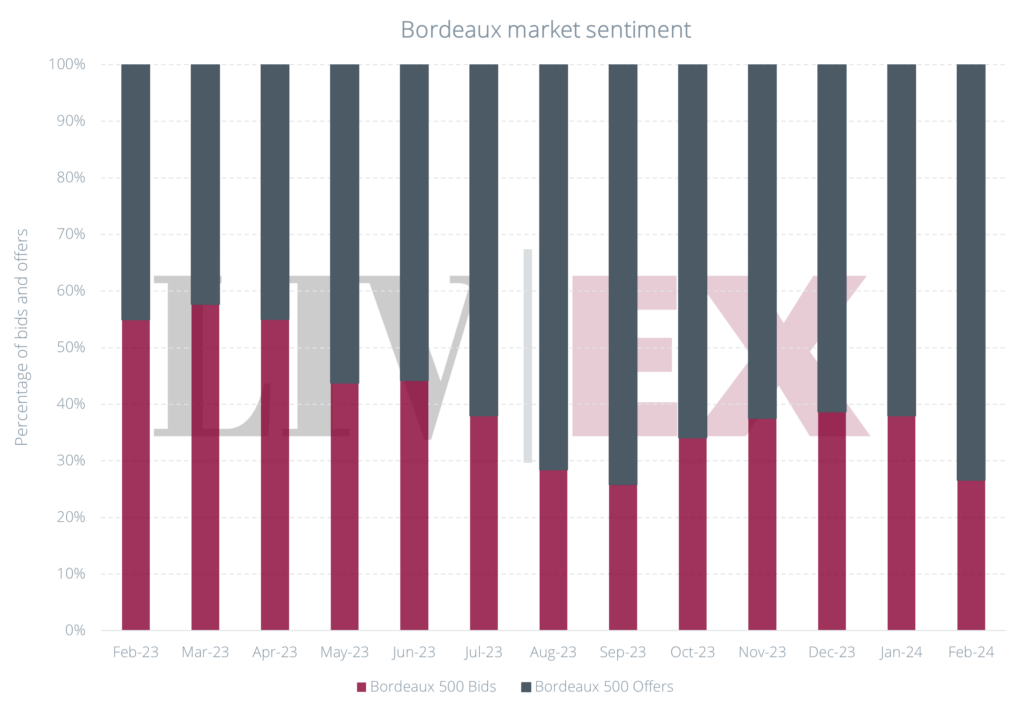

The clouds gathering overhead are further illustrated by a snapshot of current buying and selling activity. Chart 4 compares the total value of bids (commitments to buy) to the value of offers (commitments to sell) on the fine wine market over the past 12 months. A year ago, the value of Bordeaux sought by buyers was roughly equal to the value of Bordeaux looking for a home. Today, there is more than three times as much Bordeaux for sale than the fine wine market is looking to absorb. All indicators, therefore, suggest that we are in a particularly slow period for Bordeaux.

Bordeaux Opportunities for Buyers

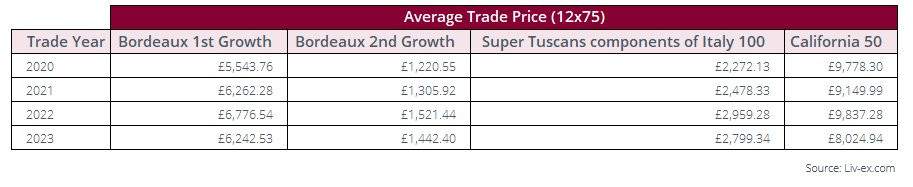

None of this is to say that there is a lack of wines from Bordeaux that offer outstanding value to collectors. On the contrary Bordeaux’s ability to produce in high volumes wines that age elegantly means that buyers have plenty to choose from. Chart 5 compares prices of top-tier Bordeaux with the leading Cabernet-based wines of Tuscany and California. The First Growths, and particularly the second growths, look attractive compared to their American counterparts which are produced in much lower volumes.

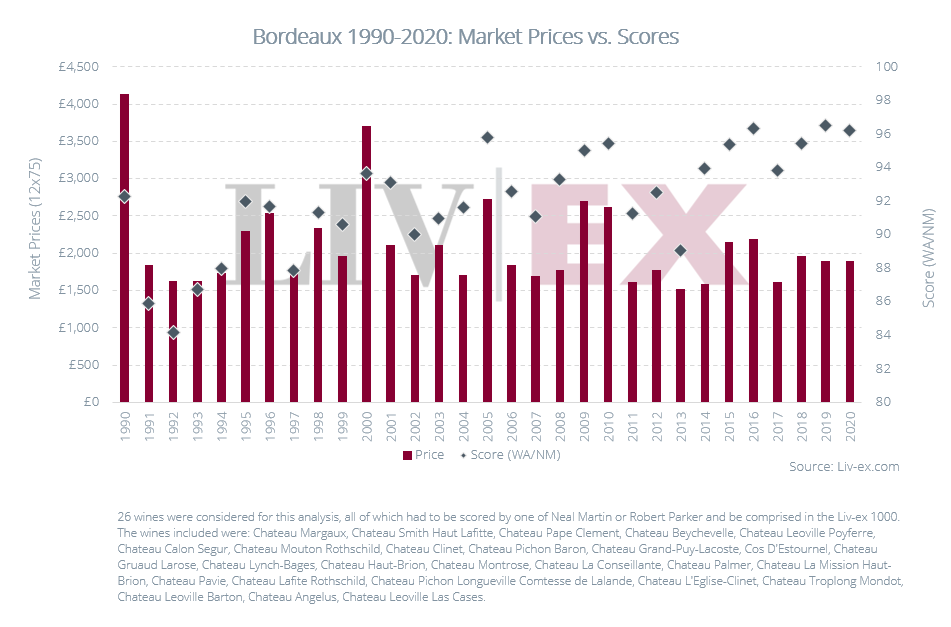

Further, buyers are spoiled for choice when it comes to buying back vintage Bordeaux. As Chart 6 shows, vintages such as 1995, 1996, 2001 and 2012 come with good critical reception, maturity, and prices at a very similar level – or even below – the most recent releases.

What’s coming?

Early indications of the 2023 vintage

For an early understanding of the vintage being released into this environment, we contacted Bordeaux-based critic Jane Anson of Inside Bordeaux. On April 2nd, she wrote:

“Where 2021 and 2022 were studies in contrast – the first being largely cool and wet vintage with low alcohols and some dilution, and 2022 being an extremely hot vintage with concentration, depth and sometimes extreme flavours – we can expect 2023 to be somewhere in between.

Looking closer, it tips further towards 2022, as it was above averagely warm for most of the growing season, after a wet start that meant the most intense mildew pressure since 2018. Less extremes during the growing season, but two heat spikes in late August and early September meant some shriveling and over-concentration on the drier soils.

This means that yields vary depending on estates and terroirs – something that we have got used to over the last few years.

We will really begin tasting as of next Monday (8th), but so far, it’s looking like a year where there will be some excellent wines, but very much up and down. Lots to follow, and let’s hope the estates listen to the market in terms of prices!”

To summarise, early signs suggest that this is a good – but not great – vintage with mixed yields. It will be released into a market that already has declining prices and plenty of supply. Producers will need to think carefully about how to engage the supply chain if – and in some cases this is a very big “if” – they are committed to selling wine through to the end consumer this spring.

En Primeur Today: The State of Play

The En Primeur system, when it works well, offers advantages for stakeholders throughout the supply chain. Producers can ensure cash flow. The negociants of La Place de Bordeaux, and merchants around the world, can generate significant revenue through sales. And many buyers – including private collectors, but also wholesale and retail buyers – can purchase wine at preferential prices, secure allocations of wine that might be difficult to find later, and order wines in non-standard bottle formats.

As a recent press release from the Union des Grands Crus de Bordeaux (UGCB) said, En Primeur is “a unique system in the wine world and an unmissable annual event”. It went on: “For the occasion, over 5,000 visitors from around 50 countries will travel to the vineyards and chateaux to assess the full potential of the 2023 vintage still ageing in barrel”.

There is, quite simply, no other event that attracts as many buyers and media to focus on one single wine region for several weeks. Or, as the UGCB’s press release says: “These ‘En Primeur’ tastings shed light on the diversity and dynamism of the Bordeaux Great Growths”. This should be the envy of every other wine region in the world. It provides Bordeaux producers with the opportunity to build relationships with, and generate goodwill across, a large and very powerful supply chain.

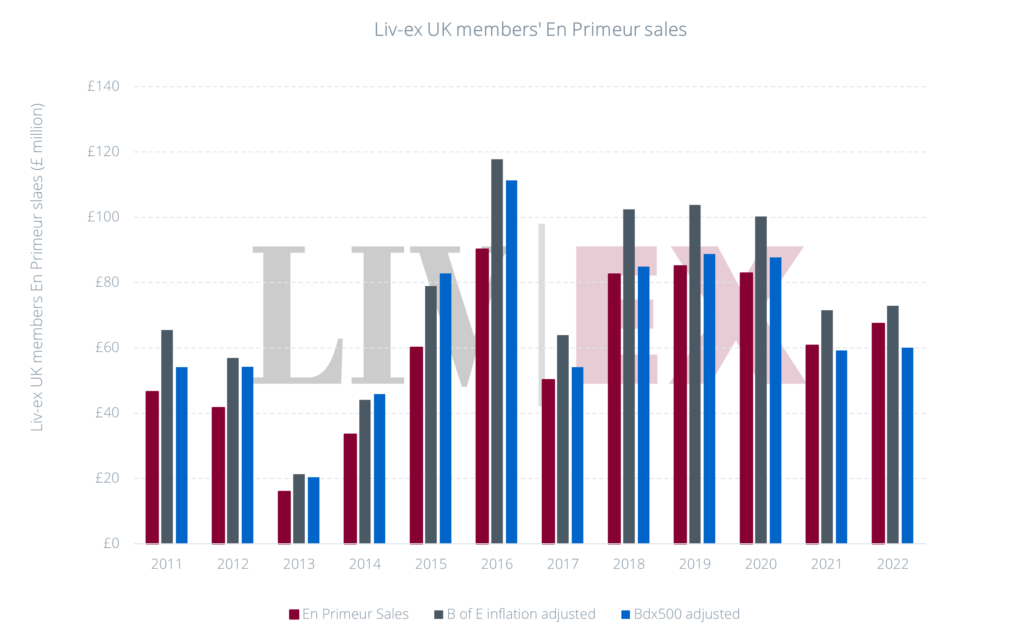

Recent returns

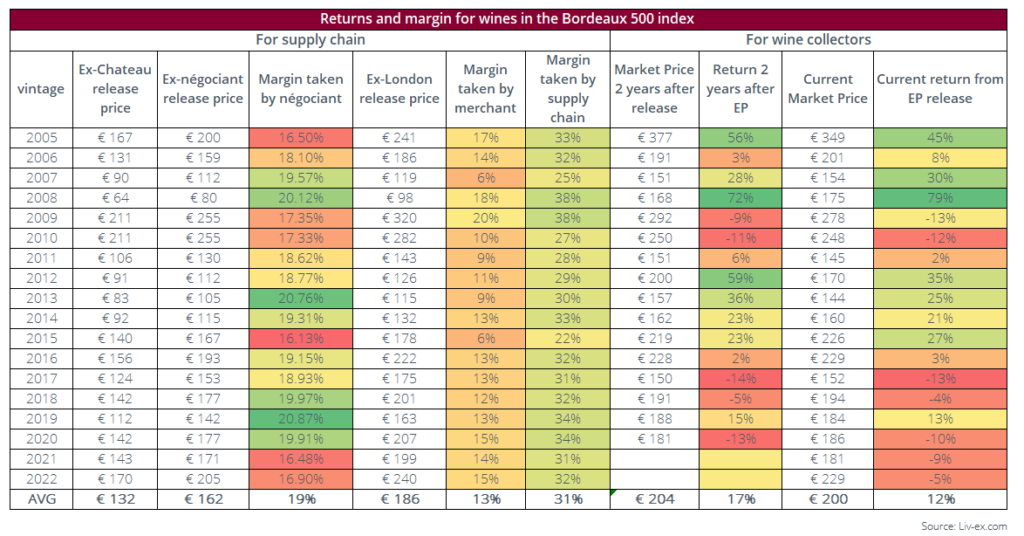

In recent years, this goodwill has been eroded. Buyers who purchase En Primeur are, too often, seeing the same wines enter the physical market at the same or lower prices further down the line. Chart 7 shows the returns and margins for leading Bordeaux wines purchased En Primeur going back to the 2005 vintage. In four of the past five campaigns, current market prices are lower than release. A glimmer of hope for collectors is 2019 – a highly rated vintage released into the eye of the Covid storm. Buyers have been rewarded with returns of 13% since release. Not a stellar return given today’s interest rates, but a positive number all the same.

The broadly negative market sentiment, rather than purely overpricing at En Primeur, might in part explain these price declines. For context, the Bordeaux 500 index has fallen 11.2% in the last two years. However, price performance of individual chateaux from En Primeur reveals that only a handful of properties are propping up the overall market.

When looking at the 2017 to 2021 vintages, only four of the 45 labels represented by the Bordeaux 500 Index (Le Pin, Lafleur, Petrus, Latour and Forts de Latour would bring the total to 50 but are excluded here) show positive returns on average since release. The three Right Bank estates above provide some of the greatest returns but are tightly allocated and only available to a lucky few (so not included in the table above). Of those available on the open market, Carruades de Lafite, Beychevelle, Calon Segur and Lafite Rothschild have provided positive returns.

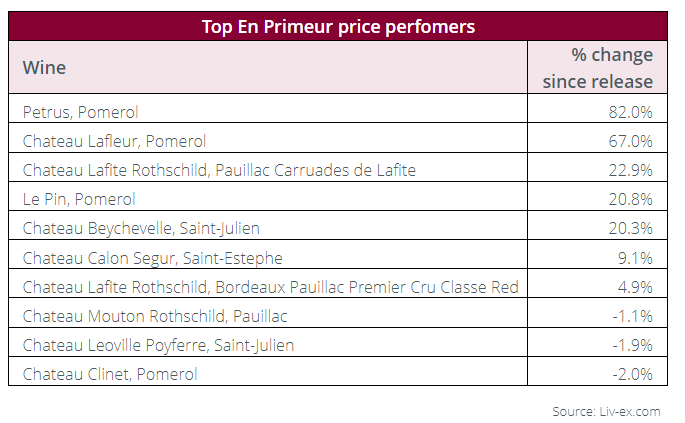

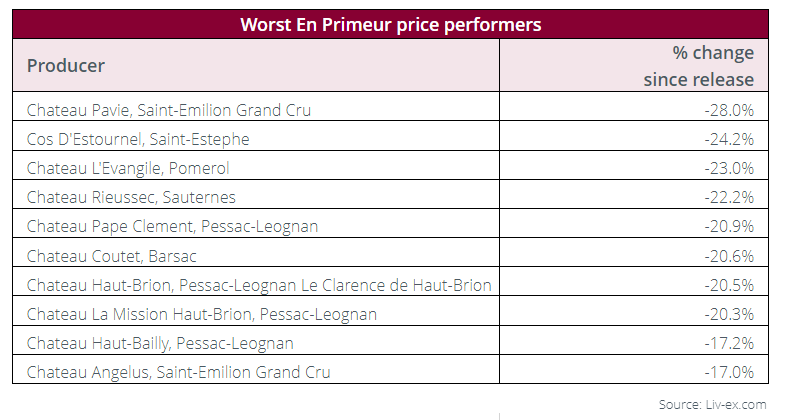

Investing in En Primeur more broadly, however, has been loss making. Chart 9 shows the ten wines that have averaged the greatest losses since release over the past five vintages. Pavie leads the pack: its past five physical vintages are available at a 28% discount to release on average.

Indeed, the wine that has fallen furthest since release is Pavie 2018, which came out at £3,504 in London but now has a market price of £2,258 – a 36% discount. At the time, we noted that it had been released above ‘fair value’, a calculation based on comparing price with scores from critic Neal Martin. It was also priced above almost all other recent vintages, including the 100-point 2009 and 2010, making it a difficult proposition for buyers.

Liv-ex ‘Fair Value’ methodology helps in determining the right price for a given wine so you can make smarter trading decisions.

List Studio during En Primeur

During En Primeur, use our ready-made lists (such as ‘First Growths’ and ‘Right Bank’) in List Studio to rapidly understand how back vintages stack up against each other, and instantly place a bid or offer when you spot an attractive opportunity to trade…

The volume story

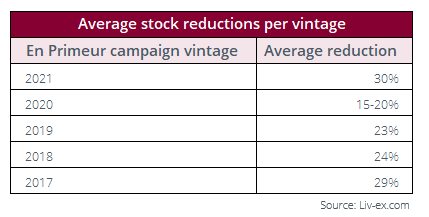

Price is only half of the story. There is very little data available on volumes released by the chateaux each year, but Liv-ex has compiled available information to indicate where reductions have been made. The overall picture is that many estates are reducing the amount of wine offered En Primeur in favour of drip-feeding the market with more mature vintages. This is shown in Chart 10.

Some estates have openly shared their intention to reduce the volume of wine offered En Primeur, partially following in the footsteps of Chateau Latour. This includes Mouton Rothschild, which announced that it would be decreasing the volume of wine released En Primeur from the 2015 vintage in favour of more library releases. In a similar vein Chateau Palmer announced a series of “N-10” releases in 2020, in which 10-year-old vintages would be sold every September.

The high prices set by some chateaux likewise suggest that En Primeur sales are of little interest to them. After Chateau Lascombes was acquired by billionaire-owned Lawrence Wine Estates in November 2018, Robert Nicholson, principal of International Wine Associates, who advised on the acquisition called En Primeur a “complicated commercial structure” in an interview with Meininger’s Wine Business International. He said: “Maybe the example of Latour leaving La Place de Bordeaux may stimulate others to consider this alternative route to market.”

In March 2023, the ambitious estate went on to appoint Axel Heinz, formerly of Ornellaia and Masseto, as Estate Director. In June of the same year, it released its 2022 vintage at £746 per case, around 30% higher than other recent vintages could be purchased for at the time. Priority appears to have been given to brand repositioning over sales.

Historically, En Primeur has been declared a success if wine sales are high. When wines fail to sell in volume, campaigns are deemed a failure. But if many well-funded chateaux, no longer in need of an early cash injection, do not need nor intend to sell large amounts of stock at En Primeur, perhaps this measurement of success is no longer relevant to all participants.

Supply Chain Impact

The Negociants

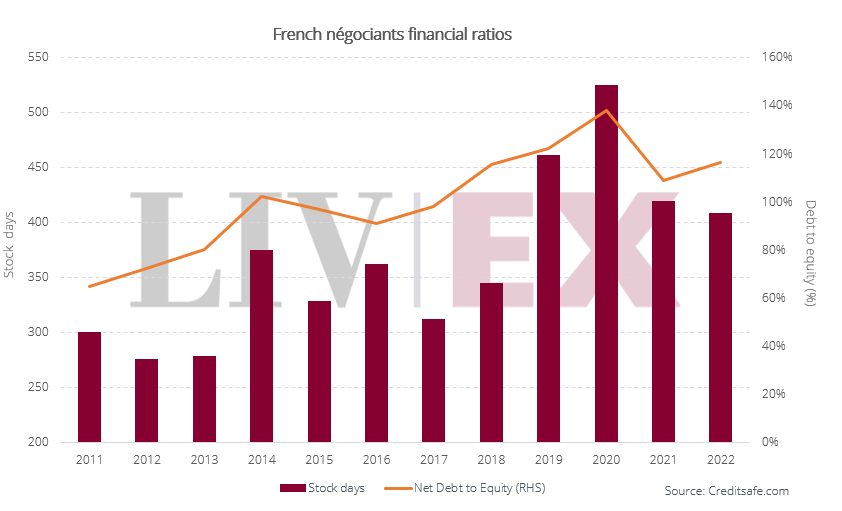

Other members of the supply chain are likely to take a different view. Data from Creditsafe suggests that French Negociants are holding stock for longer, and have considerably more debt relative to equity, than a decade ago. The good news is that both measures have improved since peak in 2020. However, in a high interest rate (and high storage cost) environment, it is unlikely that negociants will be happy about purchasing more stock that cannot be sold quickly. Often, to secure allocations of top wines, this is the reality.

This was highlighted by Jane Anson in a recent interview with fine wine think tank Areni Global. She suggested that the strain on negociant balance sheets was such that some have reduced spending on less prestigious wines, leaving some producers in difficult financial positions.

The Merchants

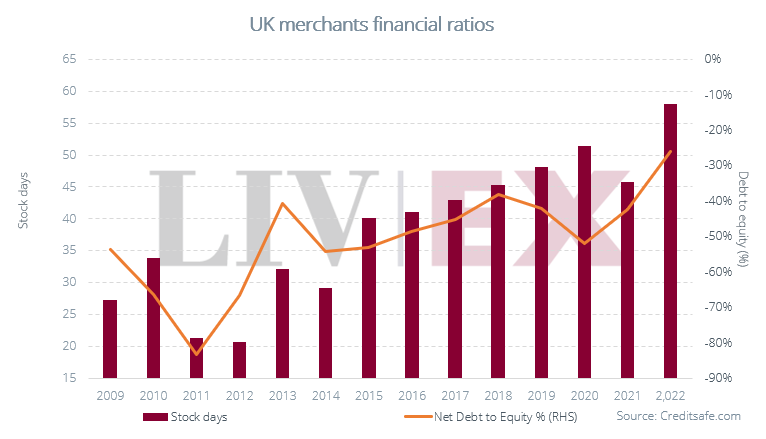

Across the channel, UK merchants have remained in a net cash position, though this has been eroded slightly from last year. At the same time, stock days increased from 46 days in 2021 to 58 days in 2022. Although slightly weakened, they remain in a strong position to be engaged overall – if the tone of the campaign is correct.

Leading UK merchants saw a decline in sales during the 2021 and 2022 campaigns, following three steady years, as Chart 12, which is based on UK merchant sales, shows. A straw poll of international members provided some context. On the one hand, some indicated disenchantment among private clients due to pricing issues. Some also suggested that cellars are filling up. Others, including one member based in Switzerland, are more optimistic. Those with private clients who are more concerned about provenance and allocations than securing the best price remain well positioned to sell En Primeur this year.

Some commented on the resource required to participate in En Primeur. This includes the time and cost of sending a team to the tastings, as well as the dedication of sales teams working on the releases. Justifying this investment requires healthy sales and good margins. But as one member said: “A lot of time and expenditure goes into Bordeaux. For single digit returns on the stock, this is very hard to justify. Burgundy and Barolo are more attractive. They are smaller campaigns for us, but the margins are way better”.

The chateaux

For the chateaux, early indications suggest that releasing mature vintages into the market without the spotlight of En Primeur – those 5,000 visitors and a highly visible global campaign – can be challenging. The recent release of Latour 2017 met with a mixed reception. And after three years of releases, Chateau Palmer’s N-10 campaign, which was due to re-introduce the estate’s 2013 vintage to the market, was paused last September.

On top of this, much of the trade, and some collectors, are increasingly aware that stock is building in the visibly large, newly built cellars in Bordeaux. This brings potential for more and more back vintages to quietly enter the market. This is good news for those looking to acquire ready-to-drink wine with perfect provenance. It is less good news for those who are buying early to secure the best price. It risks undermining confidence in this segment of buyers.

Liv-ex members can easily buy and sell En Primeur stock on our trading platform, without any added risk.

Glimmers of hope for En Primeur

Getting it right

There are reasons for optimism.

The market is grinding lower but attendance at the UGC En Primeur week (22nd April) is still expected to be high, pointing to continued interest in Bordeaux from around the world. While the quality of the vintage will not be fully measured until then, there is already much talk of price reductions. Few expect the vintage to match the 2019 in terms of quality, but there is a broadening consensus that a drop to at least 2019 release prices (approx. 30% lower than 2022) will be needed to engage buyers. It is further expected that the First Growths will lead by example, so the tone of the campaign will be set in early May and indeed might be all but done in early June.

In addition, swathes of fine wine price data are available to chateaux who want to price their wines attractively and accurately. This was another point made by Anson in the Areni Global interview. She referenced Liv-ex and Wine Searcher as examples of data sources. For our part, we have devised the ‘fair value’ methodology, which allows producers to benchmark release prices against the prices and scores of wines already in the market. The producers who have adopted this most successfully have focussed on the private client purchase price. Whilst ex-chateau prices might look justifiable against the market price of physical vintages, unless the prices make sense at the end of the supply chain (add 30%), stock will remain unsold.

Those who have one foot outside of En Primeur might look to other regions, particularly in the New World, for inspiration. Often producers state a desire to be “closer to the end consumer”. This is something that requires savvy sales and marketing teams. Selling wine at the scale – and price – of Bordeaux is something that requires considerable investment and creativity on the ground in global markets. Time will tell if those who have left, or partially departed, the En Primeur system have found success in their change of direction.

Thinking outside the Bordeaux 500

For price-conscious buyers, there are reasons to remain engaged with En Primeur. There is, from some leading producers, and in certain years, value to be found. There are also smaller estates that look attractive. In his report on the 2022 Bordeaux vintage, The Wine Advocate’s William Kelley highlighted 12 wines to look for En Primeur. Ten years ago, you might have expected this list to be filled with top blue-chip wines. Instead, not a single wine in Kelley’s list features in the Bordeaux 500 Index, the group of the most actively traded investment-grade wines in Bordeaux.

One member of this group, the organic certified Chateau Mangot, received a score of 93-95 points from the critic. This is the same barrel range as much more famous wines such as Cos d’Estournel and d’Issan, but Chateau Mangot 2022 can be pre-ordered for £20.50/ €23.93/$26.50 per bottle. Wines like this, which do not have active secondary markets, might not be of interest to investors hoping to trade it later at a higher price, but do act as a reminder that opportunities exist in Bordeaux – including at En Primeur – beyond the most famous estates.

Conclusion

The market has scrutinised Bordeaux prices for decades. The fact is that today, this benchmark region offers plenty of value to collectors – just rarely at En Primeur. There are well-priced back vintages from leading estates, and for intrepid buyers, emerging boutique producers offering high quality at modest prices.

They are not, however, the focus of En Primeur week. The 5,000 visitors traversing the globe to make their way to Bordeaux are, for the most part, there to taste wines from the classified growths. Based on pricing strategies, reduced volumes, and in some cases public statements, their commitment to selling wine En Primeur – at least with the intention of it reaching the end consumer – appears to be waning. Many have one foot outside of the system.

This has put pressure on partners who act as ambassadors for Bordeaux in global markets. Negociants are holding more stock, and many global merchants, observing recommended retail pricing, are seeing reduced sales. While some collectors are happy to purchase regardless of price (indeed buying EP has become a habit) there is evidence of a longer-term waning of interest. The “next generation” of buyers remains elusive.

This year, the chateaux will be releasing a good, but not great, vintage into a weak market. Balance sheets are stretched, and the era of easy money is a distant memory. Further price increases are off the table. For well-funded estates, this might not matter in the short term. But chateaux who still believe in the power of En Primeur should think carefully. The global fine wine market could be forgiven for asking a pertinent question: Why dedicate so much resource to Bordeaux if producers are unwilling to play ball on price? Their goodwill hangs in the balance.

Stay up-to-date with the latest En Primeur with Liv-ex alerts – sign up below.