February Market Report

Share this article | Print this article

- All of the major Liv-ex indices fell once again in January.

- The Bordeaux Legends 40 recorded one of the mildest declines of the Liv-ex 1000’s sub-indices, falling 0.7% month-on-month.

- The California 50 has shown relative resilience in recent months, but its long-term bullish trend is under threat. We turned to technical analysis to identify potential future movements.

- Domaines Barons de Rothschild’s acquisition of Domaine William Fèvre puts Chablis under the spotlight – we consider what the impact of this high-profile transaction may be on the region.

- Monica Larner lauds the quality of the 2019 vintage in Brunello di Montalcino, but how will these wines’ release prices go down?

- As a closing remark, we look at Château Montrose, the reliable ‘Super Second’, specifically at its 2005 vintage.

Introduction

Between a rock and a hard place

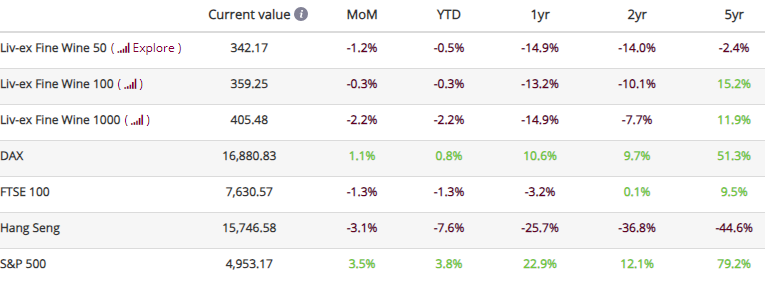

*data taken on the 14th of February 2024. The FTSE 100 was last updated on the 31st of January. The Liv-ex Fine Wine 50 is updated daily.

The year began much as the last one ended, with all major Liv-ex indices recording declines in January. The Liv-ex Fine Wine 100 fell 0.3% in January, closing at 359.25. Although January marked the 10th consecutive month of decline, the fall was less pronounced than the previous month and the Liv-ex 100 was the best performer among the major indices. The Liv-ex Fine Wine 50 (which tracks the movement of First Growths and is updated daily) dipped by 1.2% month-on-month, steeper than the 0.8% fall it recorded in December.

Looking at the broader market, the Liv-ex Fine Wine 1000 (which tracks 1,000 wines from around the world) fell 2.2% to close at 405.48. Meanwhile, mixed performances were recorded by major financial indicators. The DAX rose by 1.2% month-on-month and the S&P 500 by 4.9%. Conversely, the FTSE 100 fell by 1.3% and the Hang Seng by 0.9%.

The start of the year saw an increase in both the number of brands (LWIN7s) and individual wines (LWIN11s) traded on the secondary market. Both trade value and volume recorded an uptick, but exposure (the value of bids and offers on the exchange) took a slight dip.

Major Market Movers

The Bordeaux Legends 40 shows resilience

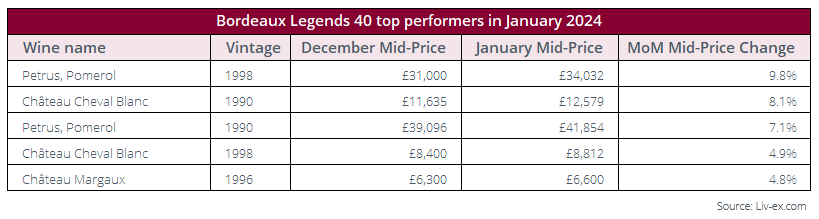

In January, the Liv-ex 1000 sub-indices recorded declines across the board, ranging from -0.7% for the Bordeaux Legends 40 and the Italy 100 to -4.3% for the Rhône 100.

All but one of the sub-indices recorded steeper falls month-on-month: the Bordeaux Legends 40 fell just 0.7% compared to its 1.6% fall in December. Within the index, 23 components saw their Mid-Prices fall, six ran flat and 11 recorded positive movements in January.

Among the wines that recorded positive movements were several vintages of Petrus, Château Haut-Brion and Château Cheval Blanc as well as one each of Château Margaux, Château Mouton Rothschild, Château Léoville Las Cases and Château Lafite Rothschild.

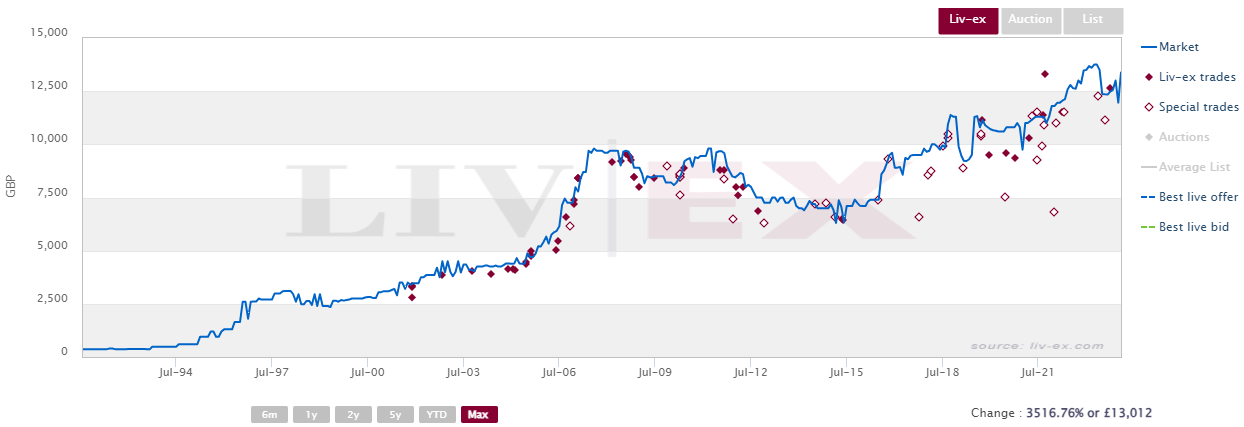

Château Cheval Blanc 1990 was released ex-château at €31.30 per bottle and has since seen its Market Price rise to £13,382 per 12×75. The wine was scored 98 points by both Neal Martin and Jeb Dunnuck.

Château Cheval Blanc 1990 trades on Liv-ex

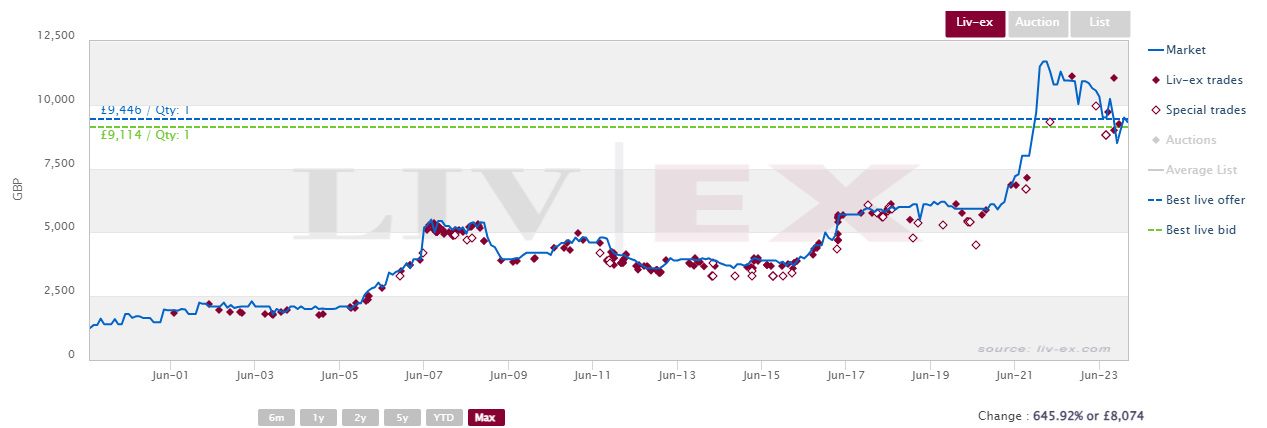

Château Cheval Blanc 1998 was released at €83.80 per bottle ex-château and has since seen its Market Price rise to £9,373 per 12×75. The wine was scored 100 points by Lisa Perrotti-Brown and 95 points by Neal Martin.

Château Cheval Blanc 1998 trades on Liv-ex

At the other end of the scale, the weakest performers in the index were spread out across labels, but interestingly, ten out of the bottom 15 performers were from the 2000 vintage.

Chart of the Month

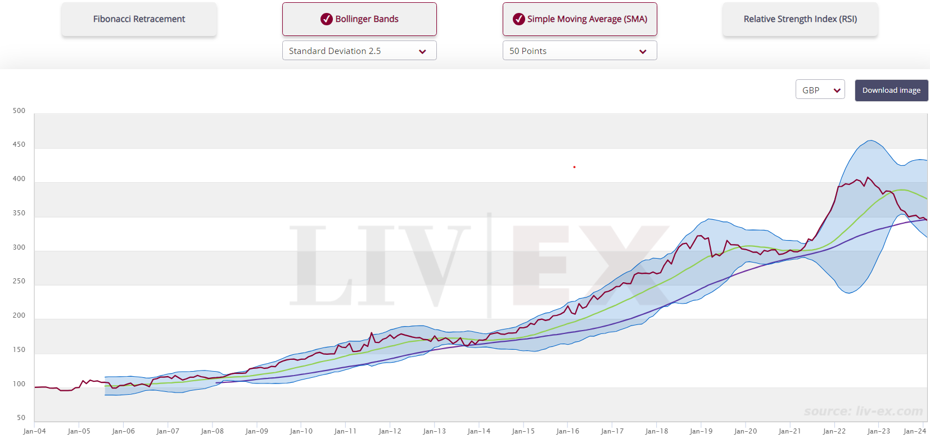

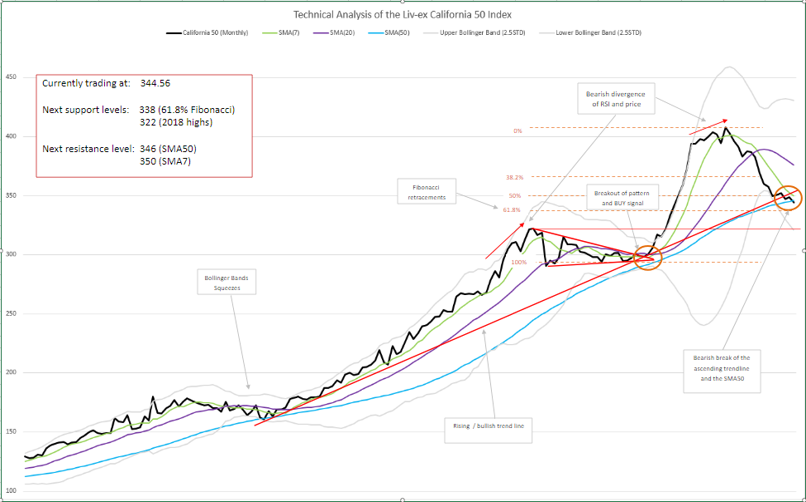

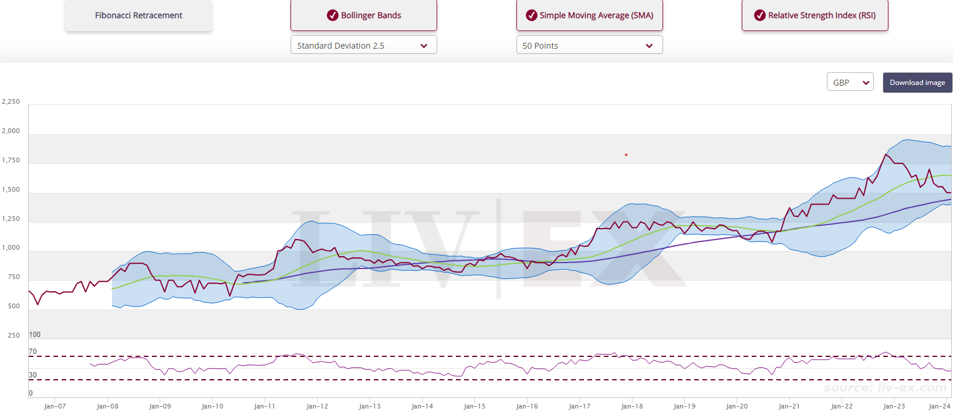

A critical time for the California 50

Amid the release of Napa’s 2021 wines, California has seen an uptick in trade on the secondary market over the last few months. In the second half of 2023, the California 50 index remained relatively flat and even rose in September and October, producing one of the better one-year performances of the Liv-ex indices.

However, technical analysis shows that the California 50’s long-term bullish trend is coming under threat of a reversal; in October 2023, the index broke its 10-year-old ascending trendline. This could be a major bearish signal, especially since it has been followed by the break of the Simple Moving Average 50 months (SMA50) in January 2024. The Bollinger Bands (BB) are now wide open, which suggests a possible further downward movement.

The index’s short-term trend is now bearish; the index has recorded several lower highs and lower lows since its all-time high in September 2022. It looks likely to test the 61.8% Fibonacci retracement level at 338, but there is an important horizontal support zone at around 322, which is the level of the index’s 2018 high.

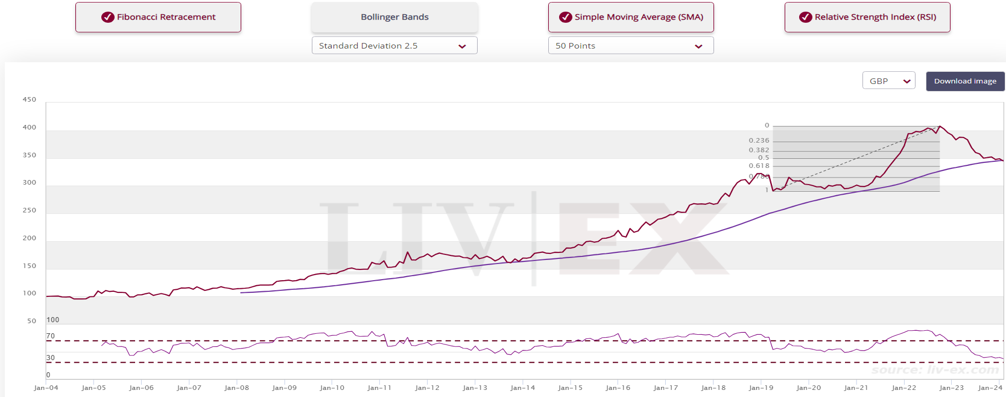

The Relative Strength Index (RSI), charted below on Liv-ex’s Technical Analysis tool, is firmly into bearish territory but still some way outside ‘oversold territory’ (i.e. below the ’30 line’). Further RSI action in the coming month should be monitored, as proponents of technical analysis would expect it to accelerate downwards.

While we would expect some reaction following the break of the SMA50 (perhaps a re-test?), at the time of writing, 322 is the main objective and zone to monitor. The ongoing bearish short-term trend would be invalidated if the price re-tests the long-term ascending trendline and its SMA50 and if the Bollinger Bands turn around upwards.

Liv-ex recently released a Technical Analysis tool, available for members on Gold packages and above. If you are interested in upgrading your package, please contact your Account Manager using the form below:

News Insight

Domaines Barons de Rothschild bets on Chablis

On the 12th of January, it was announced that Domaines Barons de Rothschild acquired famed Chablis estate Domaine William Fèvre, marking DBR’s first foray into Burgundy.

Despite the current downturn in the Burgundy market, led by the very top red Burgundy producers after prices soared to unprecedented heights in 2021/2022, their white counterparts have been relatively spared. Not only do the white wines of Burgundy have the scarcity the region is known for, they are also bought to be drunk earlier than reds. As the volumes available decrease at pace, prices remain buoyant.

Indeed, white Burgundy continues to enjoy the limelight even as the broader market declines. Caroline Morey and Hubert Lamy both featured among the top ten brands in terms of price performance in the Liv-ex 2023 Power 100, while Joseph Drouhin/Drouhin-Vaudon and Louis Jadot were among the best performers in terms of number of wines traded.

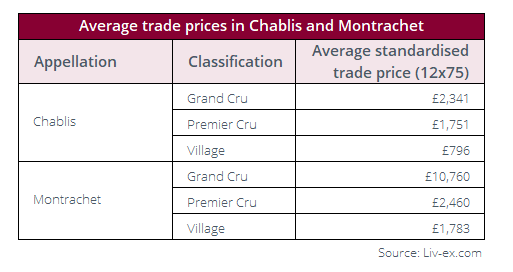

But despite high prices, great Chardonnay is not out of reach. Chablis is the appellation with the lowest average Grand Cru price across the whole region.

The contrast with Montrachet, home to some of Burgundy’s most sought-after white Grands Crus, is particularly striking. Of course, reputation and the exceptional quality of these wines play important roles in pricing, but the fact remains that in 2023, for the price of one case of a Grand Cru from Chassagne-Montrachet or Puligny-Montrachet, one could on average secure 4.5 cases of a Chablis Grand Cru. Likewise, a case of Village wine from Puligny-Montrachet or Chassagne-Montrachet was on average over £1,000 more expensive than the Chablis equivalent.

To cite just one example, Joseph Drouhin’s Montrachet Grand Cru, Marquis de Laguiche 2019 was scored 94 points by Neal Martin (Vinous) and has a Market Price of £7,200 per case. Domaine William Fèvre Chablis Grand Cru Les Clos 2019, despite being scored one point higher by the critic, boasts a Market Price of £1,080 per case.

Chablis’ share of trade on the secondary market has been gradually increasing, from just 0.17% in 2019 to 0.50% in 2023. If history is anything to go by, this acquisition will likely do much to improve reputation and production facilities at Domaine William Fèvre. Combined with the fact that Chablis’ traditionally cooler climate is now more akin to that of the Côte d’Or, this suggests there is great potential in the Domaine and the region in general.

Critical Corner

Monica Larner on Brunello 2019

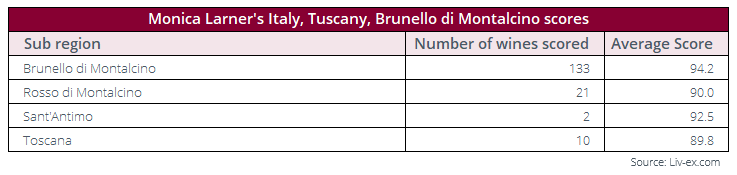

Monica Larner (The Wine Advocate) recently reviewed 178 wines with a focus on 2019 Brunello di Montalcino. The report also included some 2018 Brunello di Montalcino Riservas, some 2021 Rosso di Montalcino and a selection of IGT Toscana red blends.

Her report primarily focused on the ‘highly successful’ 2019 vintage for Brunello di Montalcino, following the ‘lackluster 2018 wines and the sunbaked 2017’. For Brunello enthusiasts, Larner suggests investing in and collecting ‘2019 village bottlings (or annata wines), selections and single-vineyard expressions’.

In her report, Monica Larner scored 110 2019 Brunello di Montalcino wines, giving them an average score of 94.5 points.

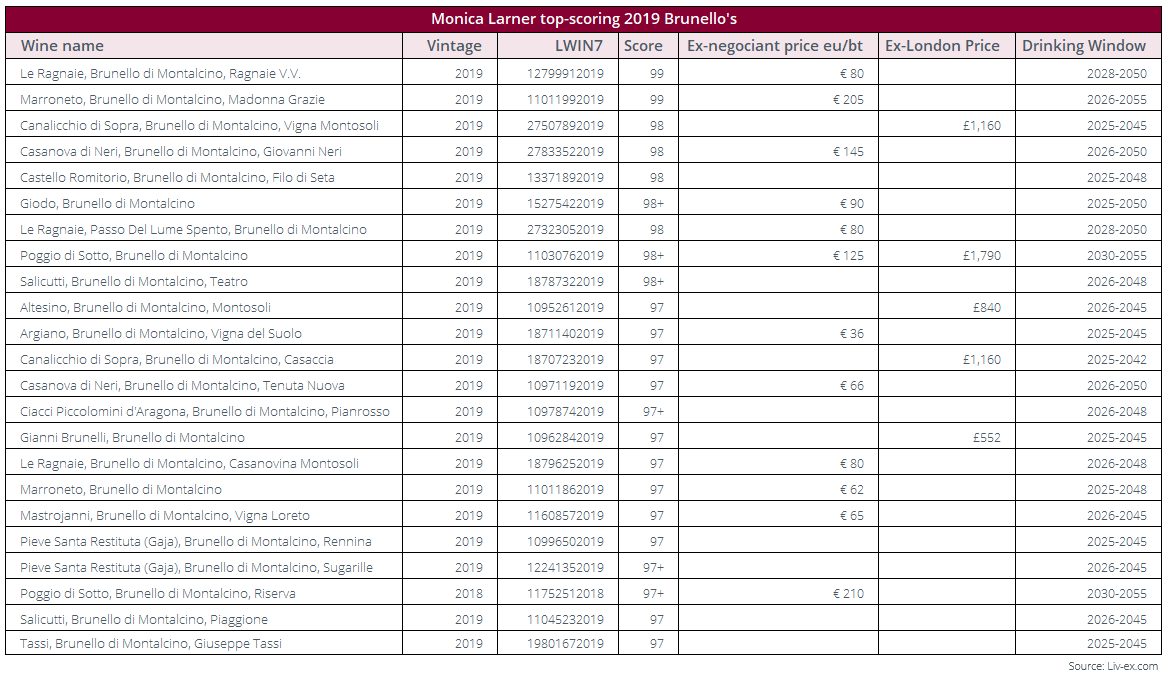

Two wines received her highest score of 99 points: Le Ragnaie, Brunello di Montalcino, Ragnaie V.V. 2019 and Marroneto, Brunello di Montalcino, Madonna Grazie 2019. The wines have been released at €80 and €205 per bottle respectively.

While no wines received a perfect 100 points, Larner noted the absence of some renowned names and hints at a forthcoming second round of Brunello reviews. She does however highlight a notable increase in wines scoring in the very high nineties (97 to 99 points), featuring many new names compared to previous years.

The critical acclaim garnered by the 2019 Brunellos has meant many producers have increased their prices year-on-year. Casanova di Neri, Brunello di Montalcino Tenuta Nova 2019 was released internationally for £925 per 12×75, up 16.3% on the 2018’s release price. Similarly, Poggio di Sotto, Brunello di Montalcino 2019 was released at £1,790 per case, up 17.0% on the previous release.

Il Poggione, Brunello di Montalcino 2019 was released internationally for £320 per 12×75, down from the 2018’s release price of £350 per 12×75. It’s worth noting, however, that the 2018’s current Market Price is £296 per case.

After weeks of its 2018 vintage being at the forefront of trade after being named the Wine Spectator’s 2023 Wine of the Year, Argiano released its 2019 Brunello di Montalcino at £380 per case, up 15.2% on the previous release.

Some might justify the price hikes on the 2019 releases by their better scores compared to the 2017s and 18s (for most wines, at least). However, these vintages were priced up on the popular and critically-acclaimed 2016s, which are still widely available on the secondary market, many below the prices of the latest releases.

Will positive critical opinion be enough to buoy the 2019s, or are these release prices based in hubris? The market will tell us in time.

Final Thought

Time to consider Château Montrose 2005?

Almost a decade on from the monumental renovation works at Château Montrose, we take a look at this Super Second’s secondary market performance.

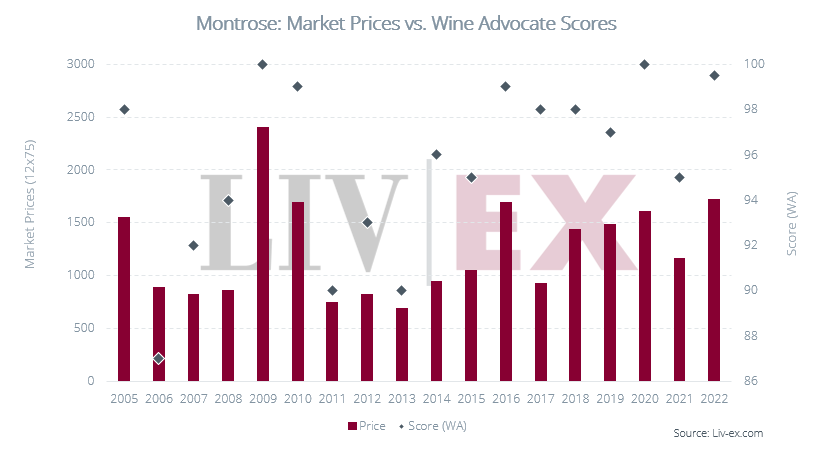

In 2023, Château Montrose came in as the 8th most sought-after Bordeaux 500 label based on the number of bids it received. Among its vintages, the 2005 was the second most popular, closely behind the 2010 vintage.

Last year, the label saw considerable interest on the market.

In 2023, Montrose was searched for 13,715 times on Liv-ex, surpassing Château Léoville Las Cases, Cos D’Estournel and Château Lafleur.

The 2010 vintage attracted the most attention, likely due to its 100-point scores from Lisa Perrotti-Brown and Antonio Galloni (although Lisa Perrotti-Brown downgraded it to 99 points in her subsequent review for The Wine Advocate). Since its release, the wine has seen its Market Price increase by 10.6%.

While carrying slightly lower scores of 98 points from both Lisa Perrotti-Brown and William Kelley, the 2005 has proved a wise purchase. Released at £635 per case, the wine has seen a steady rise in its price, now trading at £1,550 per 12×75. Those clever enough to have bought En Primeur will have seen a 140% return.

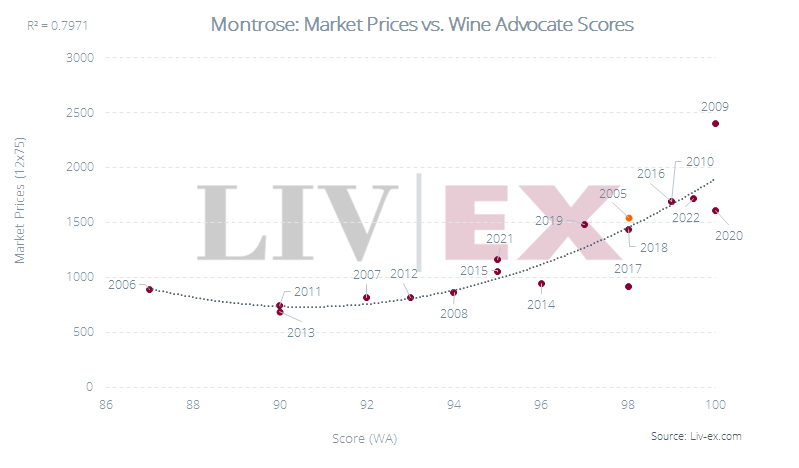

What does the Fair Value chart say about the 2005 vintage?

Château Montrose Market Prices are 80% correlated with Wine Advocate scores. At its current Market Price, the 2005 vintage sits slightly above the Fair Value line.

However, its true value becomes apparent when considering its age and quality.

Despite the wine sitting above the Fair Value line, it stands out as one of Montrose’s better-scoring (at least according to The Wine Advocate), well-priced back vintages. While the 2010 and 2009 vintages may boast slightly higher scores, the 2005 comes at a 35.4% discount to the 2009 and an 8.4% discount to the 2010 vintage.

Does the 2005 vintage still have legs?

Looking at its historical price chart, we can see that Château Montrose 2005 has undergone a correction since reaching its all-time high at £1,827 in October 2022.

Despite this, its long-term bullish trend remains intact, supported by indicators such as the ascending Simple Moving Average 50-month (SMA50) and an upward trendline dating back to 2010. While it is significantly below the current price, the trendline intersects with a major horizontal support level at £1,250, which gives it greater significance.

Currently, Montrose’s price appears to be ‘stuck’ between its Simple Moving Averages over 20 and 50 months, indicating a potential exhaustion of the long-term bullish trend. However, the fact that both SMA20 and SMA50 are still rising provides some reassurance to bullish investors.

The Bollinger Bands (BB) are flat, with the lower BB just below the SMA50, potentially defining the lower band of a trading range for the next few months.

The Relative Strength Index (RSI) has been hovering below the ’50 line’ since October 2023. While it is in ‘bearish’ territory, it is neither oversold nor showing signs of an imminent acceleration of the bearish momentum at present. If the SMA50 is breached, however, it may signal an acceleration of the bearish momentum, with a price objective of £1,250.