2023 Liv-ex Classification

Introduction

First published in 2009 with a focus purely on Bordeaux, the Liv-ex Classification has evolved significantly since its inception.

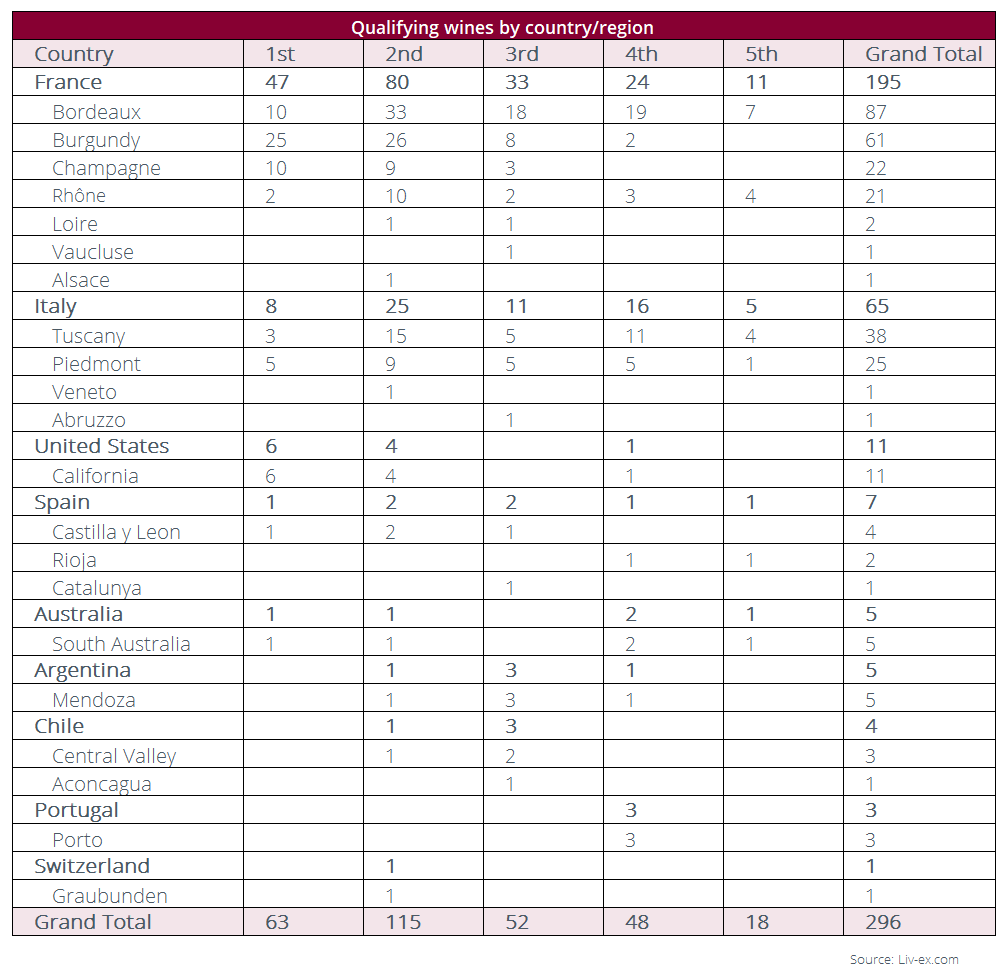

In 2017, when the Classification’s scope was broadened to incorporate wines from all corners of the world, it included wines from six countries. This number expanded to nine in 2019, and then dropped to eight in 2021. This year, the number has increased again, with nine countries represented.

Of the nine countries in this year’s Classification, some have seen an increase in the number of their wines included, such as Spain (40.0%) and Chile (100%), while others have recorded declines, including France (-12.9%), Italy (-21.7%), the United States (-50.0%), Australia (-16.7%) and Portugal (-50.0%).

Argentina has re-entered the Classification after dropping out in 2021, this time coming in with five wines compared to just one in 2019. The other newcomer is Switzerland, which has replaced Germany with a single wine in the 2nd Tier.

The primary purpose of the Liv-ex Classification remains unchanged: to use price alone to determine a hierarchy of the leading labels in the secondary market. Its inspiration is the 1855 Classification from Bordeaux, which ordered the wines from top estates from Fifth to First growths based on their price.

Given the scope of wines being considered today and with prices for certain labels rising to great heights (especially in regions such as Burgundy), a minimum level of activity and number of vintages traded over the last year were also required for a wine to qualify.

This means that one vintage of one very rare label trading just once for a very great price alone is not enough to secure a place in the Classification. The full methodology – which was slightly amended from 2021 to restrict the influence of older vintages on the average trade price – is outlined in the next section.

This year, the number of qualifying wines was 296 wines – down slightly from 349 in 2021, bearing in mind the change in methodology.

Methodology

To construct the 2023 Liv-ex Classification, the following methodology was used.

In order to qualify for inclusion in the Classification, a wine must have traded on Liv-ex between 1st July 2022 and 30th June 2023 in either a 75cl or 150cl bottle format. Standard in Bond, Standard En Primeur, Duty Paid trades and Special trades were all considered.

Two additional criteria must have been met for a wine to qualify:

- Five or more vintages of the wine must have traded during the period.

- The wine must have traded 12 or more times during the period.

An amendment was implemented in this year’s Classification:

- Only the last 10 physical vintages for each wine were taken into account, starting in 2020.

This modification aims to give a fairer balance to the Classification by focusing on recent vintages where supply is broad enough to reflect traded value, eliminating the influence of limited supply and variation in condition often present in older vintages.

Once a wine qualified for inclusion in the rankings, the average trade price per 12x75cl was calculated by dividing the total value traded by the number of 9L cases traded (ie. total the volume traded).

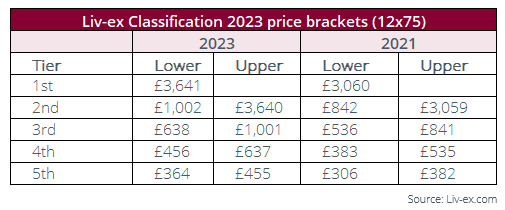

The price bands of each tier are updated every two years to reflect the changing market. This year, we adjusted our price bands in accordance with the performance of the Liv-ex 1000 index – the broadest measure of the market which tracks the performance of wines from across the globe.

Between June 2021 (when we last updated our Classification) and June 2023, the Liv-ex 1000 rose by 19.0%, so the price bands for each tier were adjusted accordingly. The lowest price bracket was for the 5th tier (between £364 and £455 per 12×75); therefore, wines that failed to achieve an average trade price of at least £364 per 12×75 did not qualify.

The price bands for the Liv-ex Classification 2023 (and the bands from the 2021 edition) are as follows:

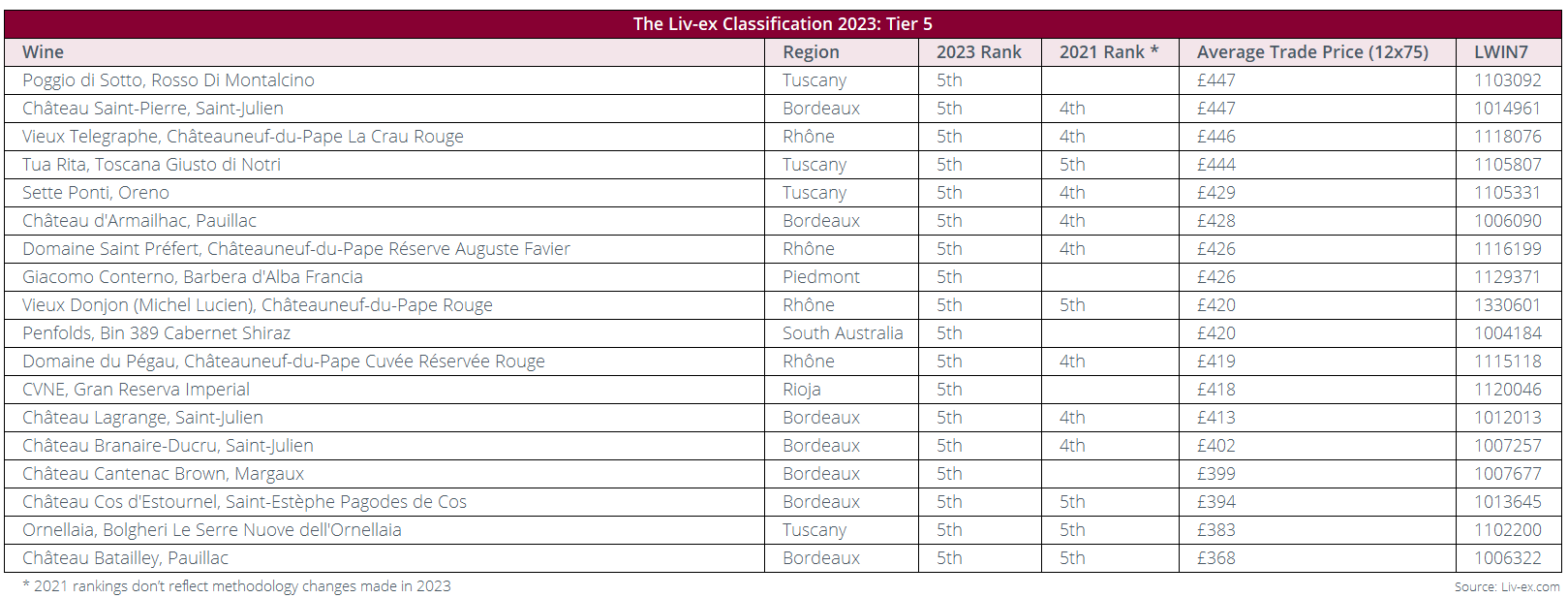

5th Tier

The 5th tier in the 2023 Liv-ex Classification is composed of 18 wines that fall into the price range of £364-£455 per 12×75. It is the smallest tier in this edition of the Classification.

Newcomers

Within this tier, five wines are making their debut in the Classification: Poggio di Sotto, Rosso Di Montalcino from Tuscany, Giacomo Conterno, Barbera d’Alba Francia from Piedmont, Penfolds, Bin 389 Cabernet Shiraz from South Australia, CVNE, Gran Reserva Imperial from Rioja and Château Cantenac Brown from Bordeaux.

A French focus

A significant portion (61.1%) of the wines in the 5th tier hail from France, with seven originating from Bordeaux and five from the Rhône. While this pattern aligns with previous Classifications, the newly-introduced wines mentioned above underscore the expanding variety of wines trading on the secondary market.

Château Cantenac Brown has entered the Classification with an average trade price of £399 per 12×75. The wine’s 2022 vintage was released En Primeur at £486 per 12×75, up 18.5% on 2021’s opening price of £410 per case. It will be interesting to see whether this wine can maintain its average price and its position in the next Classification considering the price increases of more recent vintages.

La Croix Ducru-Beaucaillou just missed out on entering the Classification with an average trade price of £356 per 12×75.

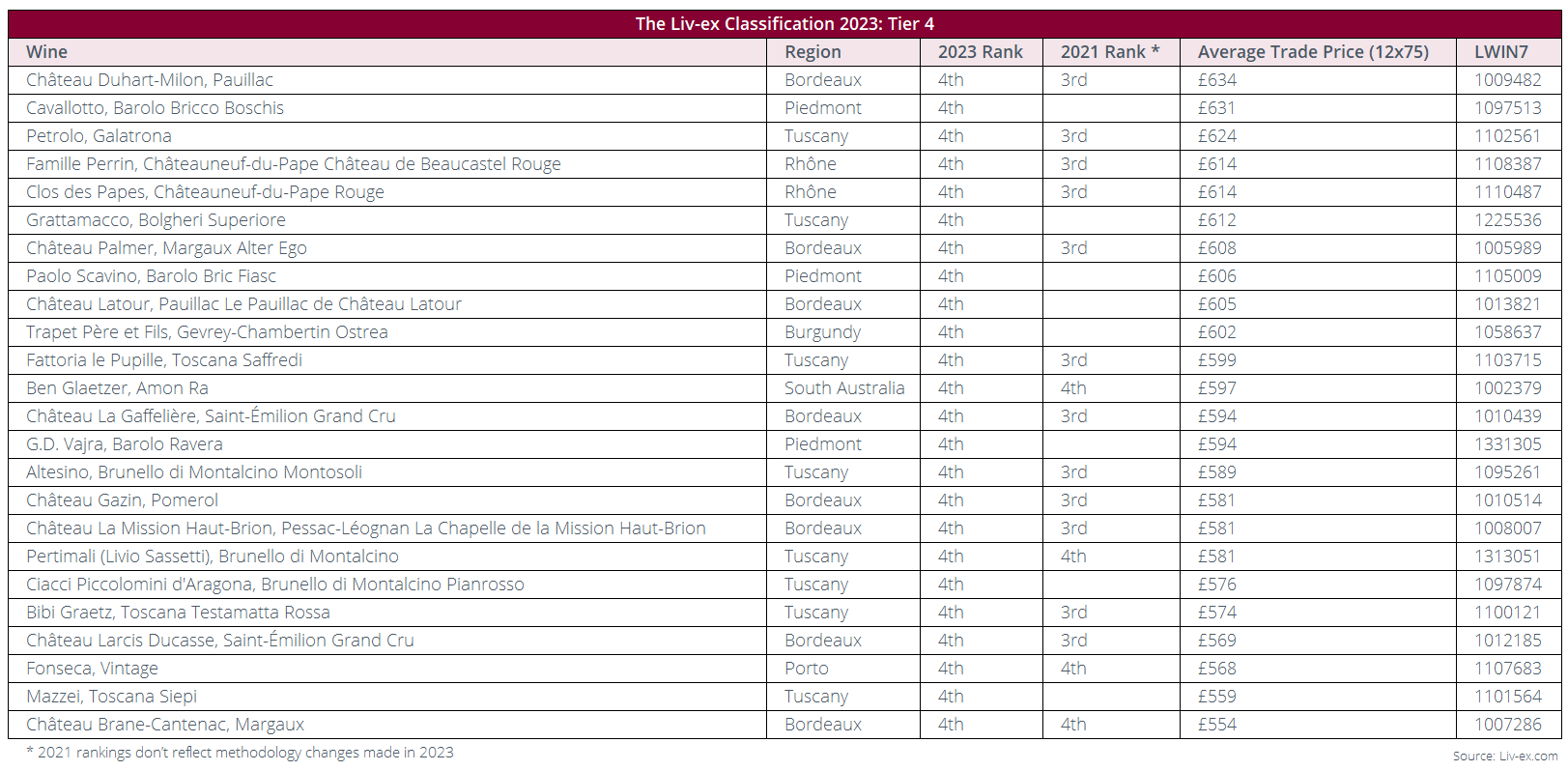

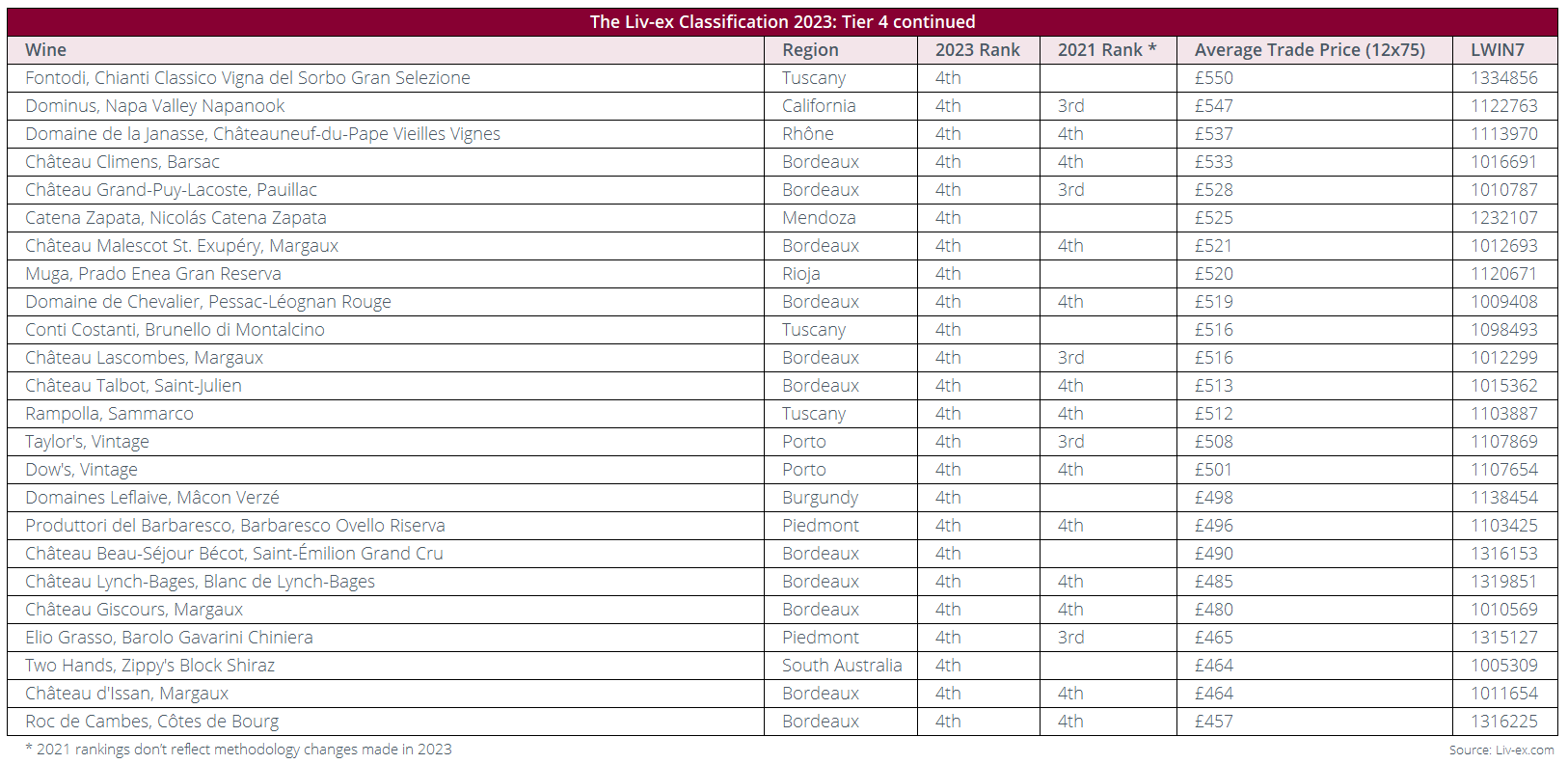

4th Tier

The 4th tier within the Classification is the second smallest, comprising 48 wines falling within the price range of £456-£637 per 12×75.

Regional diversity

Tier four is a testament to the ongoing expansion of the market, encompassing a diverse array of regions. France takes the lead with 24 wines, followed by Italy with 16, Portugal with three, Australia with two, and one each from Spain, the USA, and Argentina.

Bordeaux resurgence

Proportionally, Bordeaux has the strongest presence in the 4th tier compared to any other tier, accounting for 39.6% of the tier’s composition.

Two new Bordeaux wines make their entry into this tier in 2023: Château Latour’s Pauillac de Latour and Château Beau-Séjour Bécot.

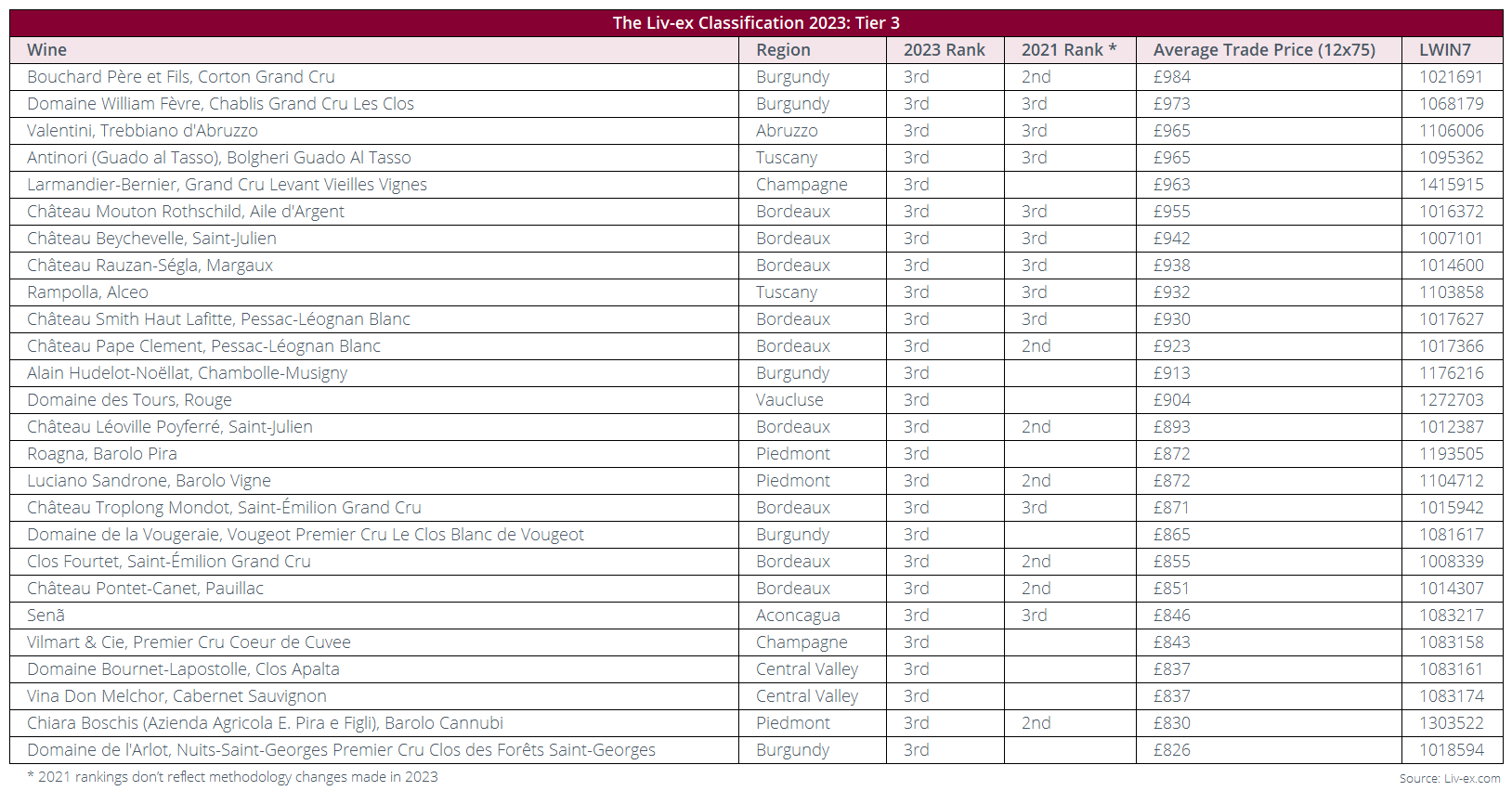

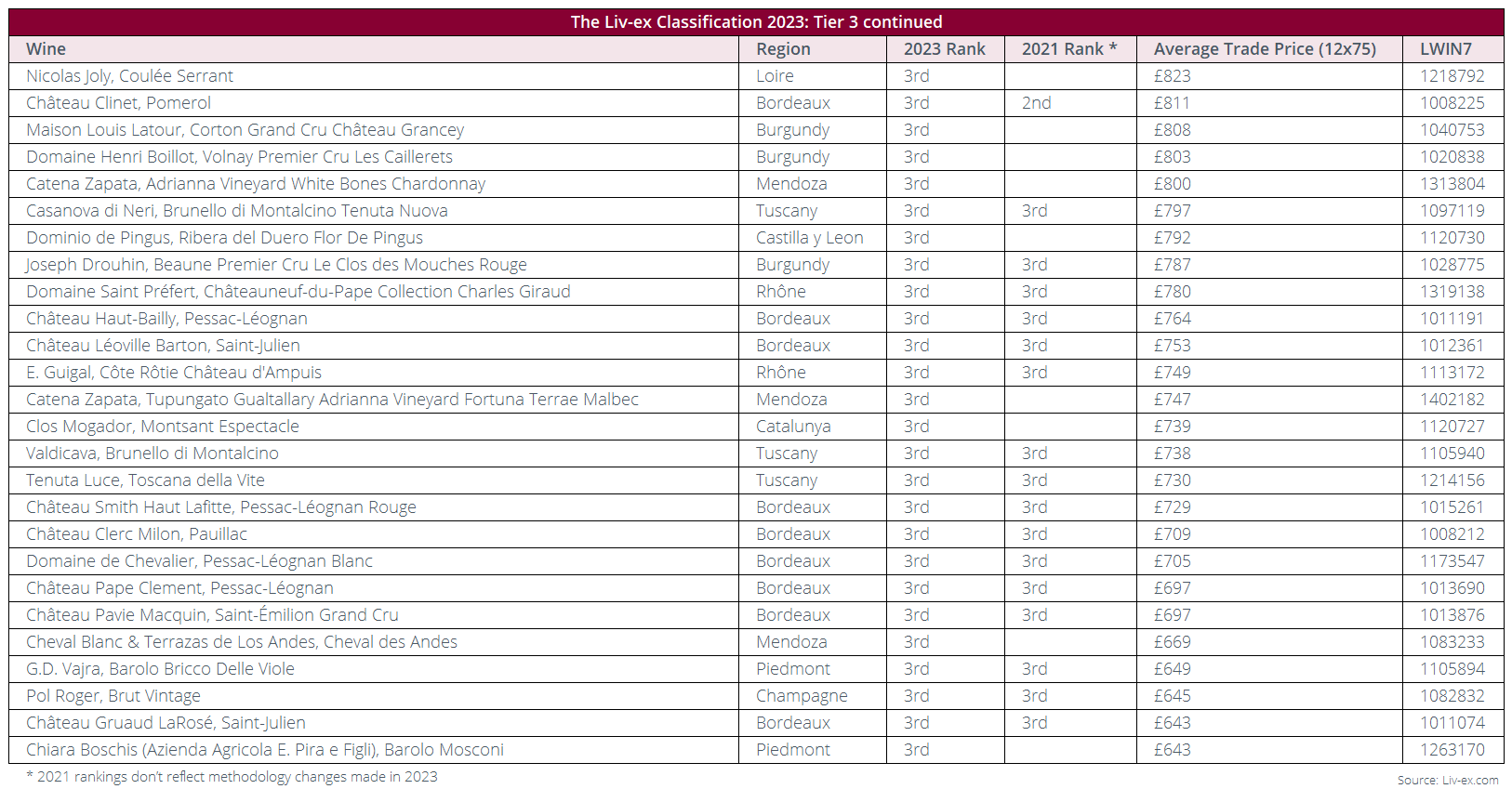

3rd Tier

The third tier is predominantly composed of wines from France and Italy. France has expanded its presence with five additional wines from Burgundy, and Italy makes its mark with two new entries from Piedmont.

Bordeaux maintains a firm grip on this tier, accounting for the majority of wines with 18 hailing from the region. However, there is added diversity as France introduces new regions into the third tier, one from the Loire and another from Vaucluse, a brand-new region to enter the Classification. The 2021 Classification included Domaine Didier Dagueneau, Pouilly Fumé Silex in the 2nd tier, which has been replaced

New World influence

Apart from France and Italy, South American wines are prominent in this tier of the Classification. Notably, three wines from Mendoza, Argentina have made their entry: Cateña Zapata, Adrianna Vineyard White Bones Chardonnay, Cateña Zapata, Tupungato Gualtallary Adrianna Vineyard Fortuna Terrae Malbec and Cheval Blanc & Terrazas de Los Andes, Cheval des Andes.

Chilean wines also claim their presence in this tier, with two wines from Central Valley including Domaine Bournet-Lapostolle, Clos Apalta, and Vina Don Melchor, Cabernet Sauvignon and one from Aconcagua: Seña.

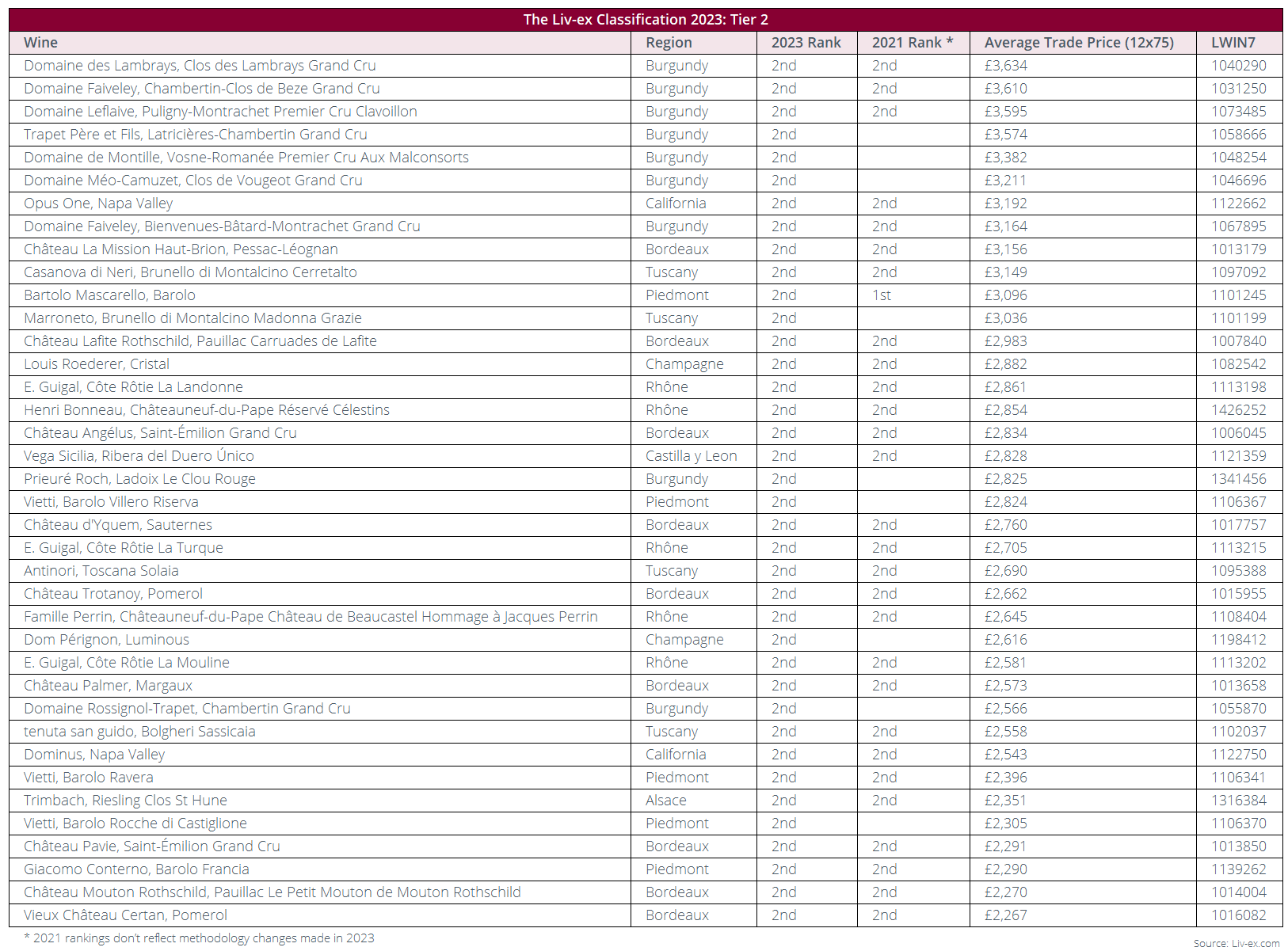

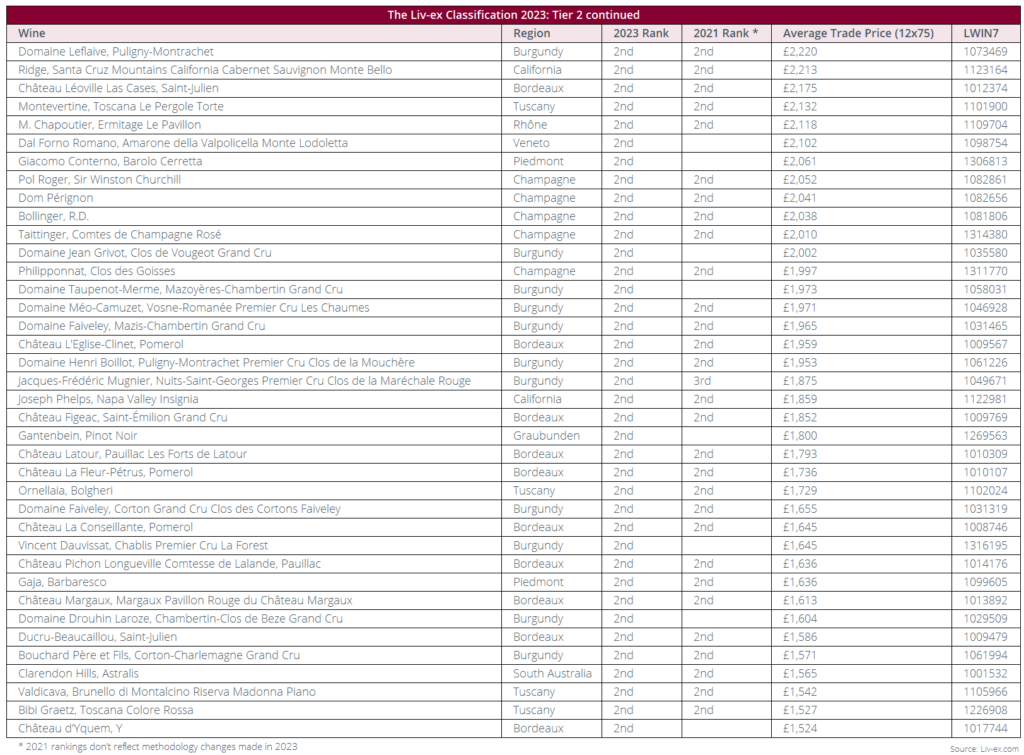

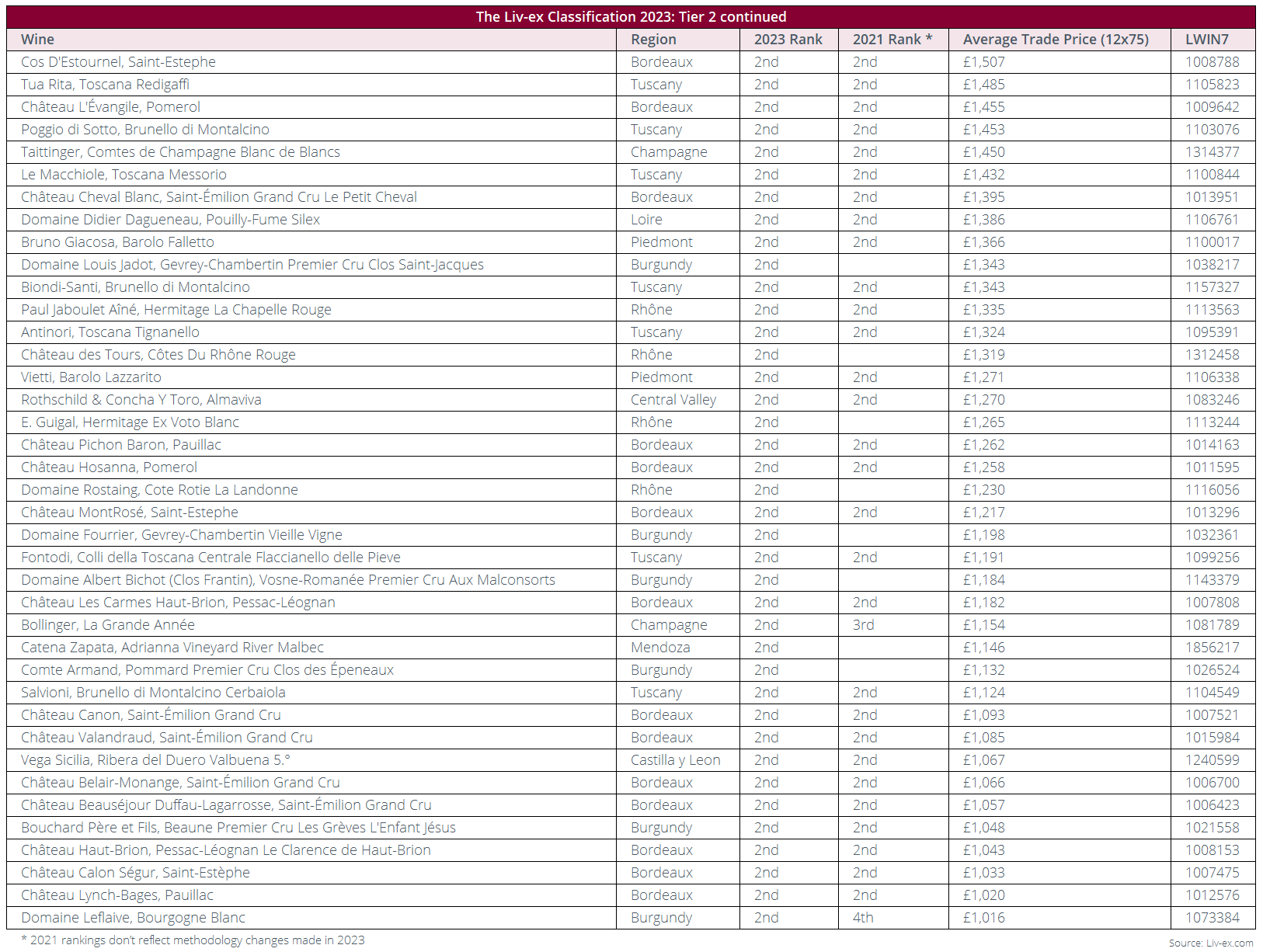

2nd Tier

Staying consistent with past editions of the Liv-ex Classification, the 2nd tier continues to be the largest, with 115 wines within the price range of £1,002-£3,640 per case. The 2nd tier also has the highest level of diversity, with wines originating from Chile, the USA, Italy, France, Spain, Australia, and Argentina. Switzerland has also joined the Classification with Gantenbein Pinot Noir, replacing Egon Müller’s Scharzhofberger Riesling Spätlese from Germany which featured in the 2nd tier in 2021.

Broadening Burgundian presence

There are 25 new entries in this tier, 13 of which hail from Burgundy. Even applying our amended methodology to the 2021 Classification, Burgundian wines form the majority of new wines in the 2nd tier (10 of 15 new entrants).

This influx can be attributed to a surge in demand in the summer and autumn of 2022, resulting in an expansion of the number of Burgundy labels trading as buyers sought wines that were relatively affordable compared to the most established growers that for many are no longer within reach.

This pattern was noted in the Liv-ex Power 100 2022, titled All About Burgundy, which considered the period between September 2021 and October 2022. Back then, Burgundy was the fastest-expanding region in the secondary market, with some wines from the region seeing their prices rise over 1,000%. So far in 2023, 1,639 individual wines (LWIN11s) have traded on Liv-ex, compared to 1,962 for the whole of 2022.

Interestingly, while there is a considerable number of new entrants from Burgundy, the proportion of wines from the region within the whole Classification is almost flat compared to the 2021 edition. This suggests these new entrants have replaced other Burgundy labels which have seen less trading activity. In the 2nd tier, for example, Prieuré Roch, Ladoix Le Clou Rouge, Domaine Louis Jadot, Gevrey-Chambertin Premier Cru Clos Saint-Jacques and Domaine Trapet Père et Fils, Latricières-Chambertin Grand Cru made their entrance in 2023.

Domaine des Lambrays, Clos des Lambrays Grand Cru which was ranked in the 2nd tier four Classifications in a row, narrowly missed out on the 1st tier this year with an average trade price of £3,634 per 12×75.

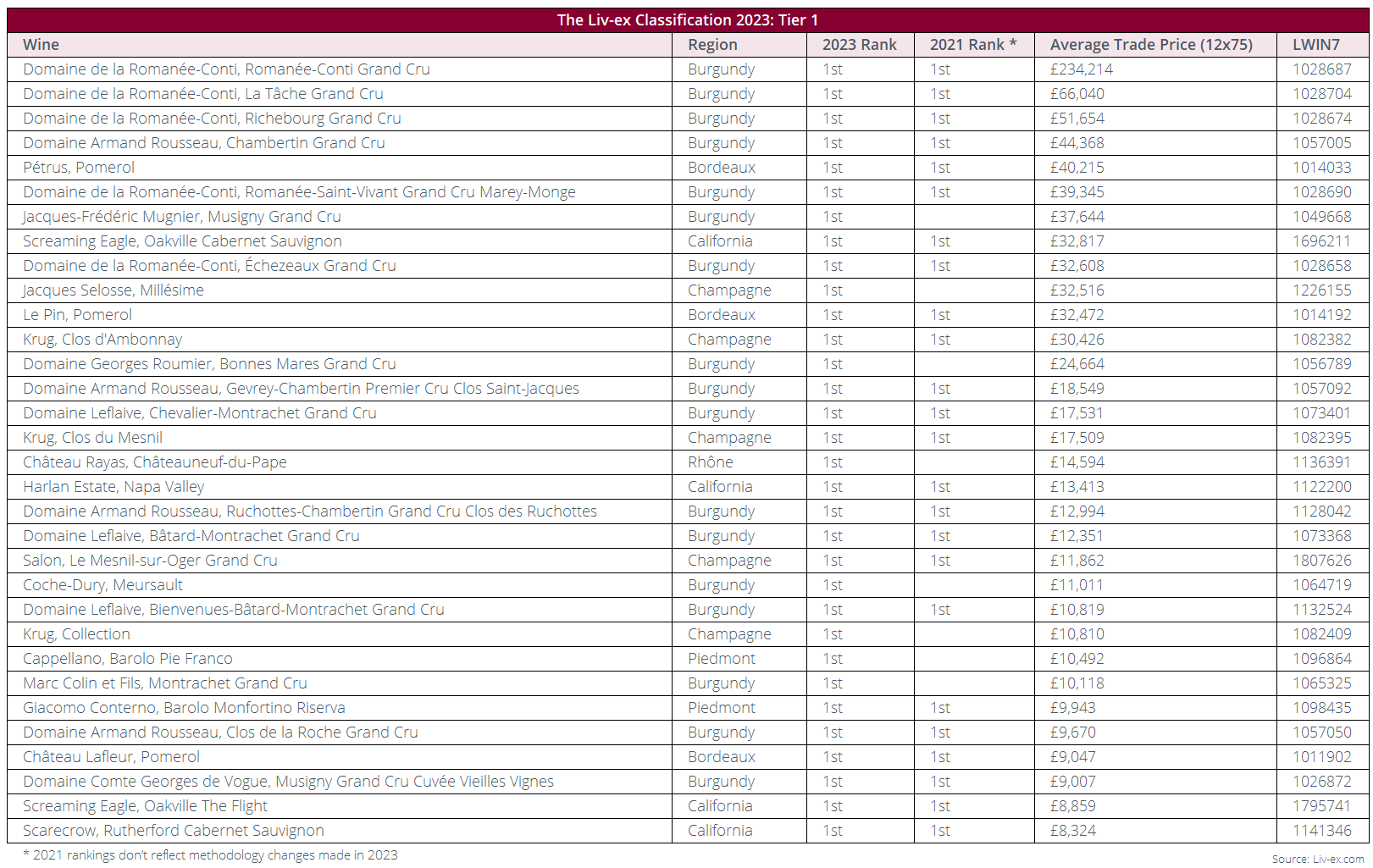

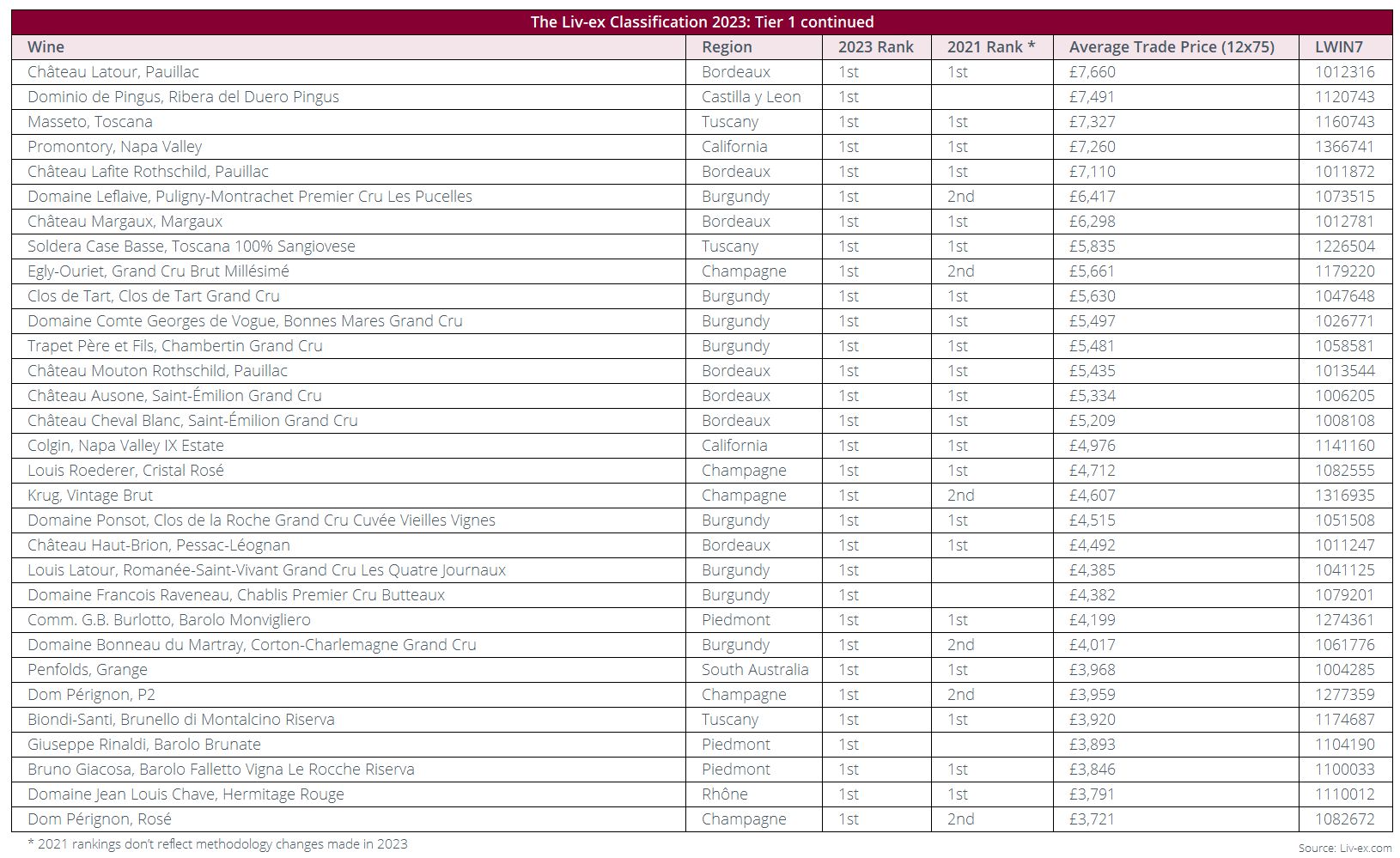

1st Tier

The 1st tier is composed of 63 wines from five countries. As expected, the lion’s share of 47 wines emanates from France. Among these, Burgundy takes the lead with 25 wines, followed by Bordeaux with ten, Champagne with ten, and the Rhône contributing two.

Burgundy’s influence

Once again, Burgundy’s impact is evident with six out of the 12 new additions to this tier originating from Burgundy. The region holds the most significant presence in this tier, accounting for 39.7% of the tier’s composition.

The first four positions in terms of average trade price are all occupied by Burgundy wines; Domaine de la Romanée-Conti, Romanée-Conti Grand Cru remains the most expensive wine in the Classification, with an average trade price of £234,214 per 12×75.

These four wines, as well as Pétrus from Bordeaux which comes in fifth in terms of average trade price, are carried over from the 2021 Classification (and would have been using the new methodology in 2021), showing a continued interest in the most prestigious (and expensive) brands in the world as buyers seek security.

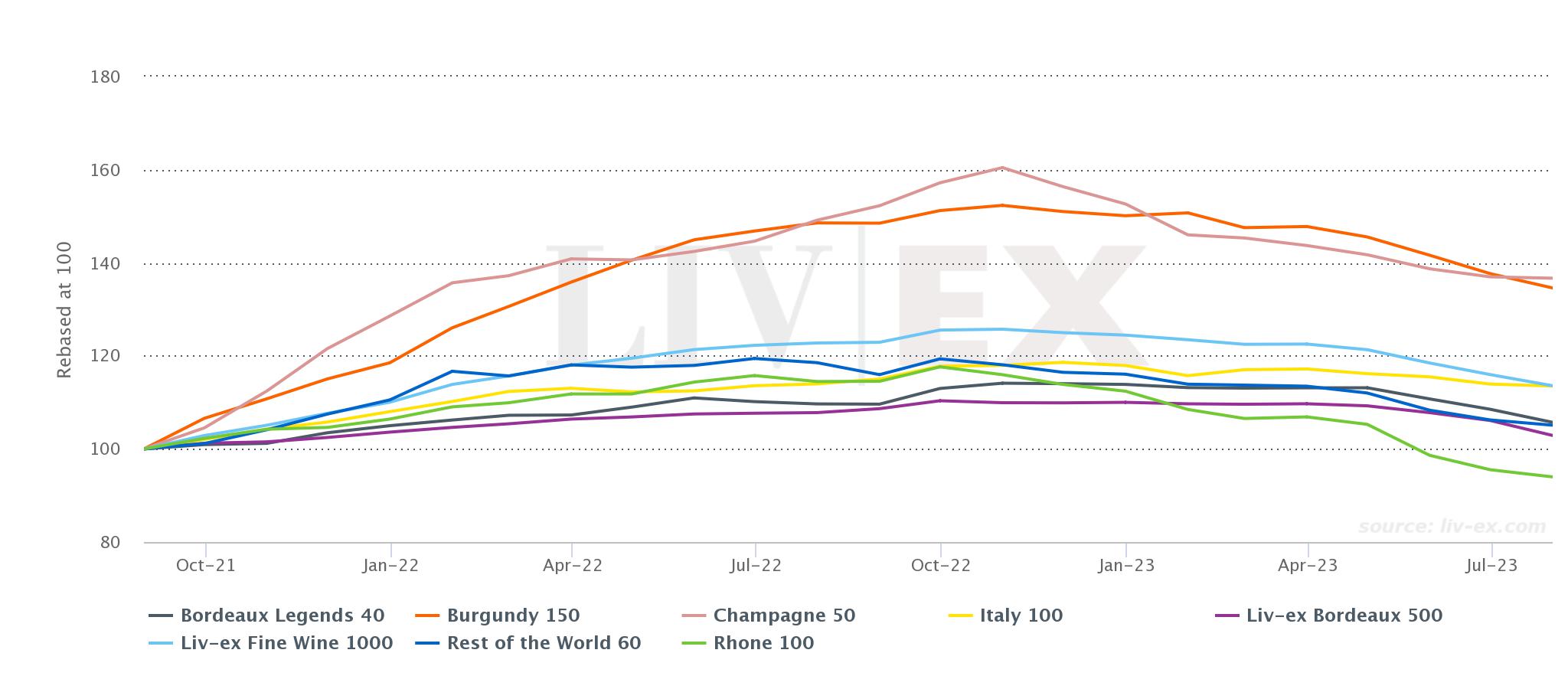

Interestingly, the prices for the biggest brands from the Burgundy have been falling consistently since the start of the year, as evidenced by the Burgundy 150 index movements. The index tracks the last ten physical vintages of 15 white and red Burgundy (six of which are Domaine Romanée-Conti labels).

After peaking at 909.38 in October 2022, the Burgundy 150 is down 10.3% year-to-date and 9.4% year-on-year, closing at 803.43 at the end of July. While this decline is the most significant recorded by the index since its inception, it is not enough to push these wines from their positions as the most expensive in the world – yet.

Bubbles float to the top

The majority of Champagne wines are in the first tier (10), while the other 12 are in Tiers 2 and 3. The region accounts for 7.4% of the total Classification in 2023.

Similarly to Burgundy, Champagne prices surged in summer 2022, as shown by the Champagne 50 index peaking at 749.63 in October 2022. Since then, the index has recorded a steady decline; it is down 10.4% year-to-date and 8.3% year-on-year.

While prices have been falling across the board since late 2022, the average trade price for Champagne wines in the 2023 Classification is a lot higher than in 2021, implying the effects of this correction have either not yet been reflected in the data, or that sustained demand and relatively consistent trade are buoying the region’s performance.

Conclusion

Global expansion

The 2023 Liv-ex Classification reflects continued broadening in the fine wine market. This edition marks the introduction of two new countries – Argentina (which is technically re-entering after dropping out in 2021) and Switzerland.

The amendments made to the methodology help to reflect this broadening and give an accurate picture of what is trading on the secondary market today – enabling newer brands to enter while limiting the influence of some rarer ones which occasionally trade expensive older vintages.

The Burgundy paradox

A significant trend observed this year is the surge of new entrants from Burgundy. A total of 26 new wines from the region have made their way into the Classification this year. Among these, 13 are in the 2nd tier, six in the 1st tier, five in the 3rd tier, and two in the 4th tier. As mentioned above, the number of Burgundian wines in the Classification is more or less flat on 2021, implying these new entrants are replacing others which have fallen out due to limited trade in the past year.

While the number of wines from the region trading (including some lesser-known labels as buyers seek value in a region characterised by illiquidity and high prices) is growing, some things never change. The usual suspects remain at the top in terms of average trade price: Domaines de la Romanée-Conti and Armand Rousseau once again establish themselves as some of the most expensive brands in the world, as they have been in the last two editions of the Classification.

The changing place of Bordeaux

Bordeaux has gone from the only region with a Classification and the sole focus of Liv-ex’s very own ranking to being one of many players in the market. In 2023, the region accounts for 29.4% of all wines in the Classification, a number more or less flat on 2021.

Considering the Bordeaux 500 index was only up 2.9% in the last two years, compared to the Liv-ex Fine Wine 1000 which was up 19% and the Champagne 50 and Burgundy 150 which climbed 36.7% and 34.6% respectively, this pattern may well continue in future editions of the Classification.

The market as it stands

The picture painted by this Classification reflects the state of the current market and continues the trend observed in the previous edition. The price brackets for the tiers are up 19%, in line with the Liv-ex 1000, and the 2023 Classification is quite top-heavy, the first two tiers being among the largest.

The year considered in this edition was one of two halves – a strongly bullish market until the end of 2022, with high levels of activity in summer 2022 and resulting price increases across the board, which was reflected in the Liv-ex Fine Wine 1000 sub-indices peaking towards the end of the year (most notably the Champagne 50 and Burgundy 150).

Since then, there has been a slowdown in the market. The chart above clearly shows the Liv-ex Fine Wine sub-indices declining year-to-date, reflecting a sceptical market sentiment. Turbulent macroeconomic conditions and rising costs have translated into more cautious trading patterns and prices declining across many regions. The fact that the same five wines figure at the top of the list once again betrays the search for continuity and safety amid the current downturn.

Is the bullish trend in the market that had prevailed since 2015 well and truly over, or is this simply a corrective phase? The next edition of the Classification will reveal whether this downturn is a temporary correction or a long-term trend shift.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. We have over 620 members from start-ups to established merchants. We supply them with the data, trading and logistics services they need, to price, source and sell wine more efficiently. Liv-ex exists to make the fine wine market more transparent, efficient and safe.

We publish the actual prices at which wines are transacted. Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines.

If you’re a registered wine business and interested in Liv-ex membership, please fill in the form below and a member of our team will get in touch.