The fine wine market in Q2 2023

Introduction

Going into the third quarter of 2023, the global economy continues to face significant challenges. One prominent issue is the rise of inflation in major economies, adding to the complexity of the current economic landscape.

In the United States, concerns about a potential recession loom and market speculation has contributed to increased volatility. Despite this uncertainty, the gradual and uneven slowdown of the US economy might postpone the onset of a recession until 2024.

Europe is also grappling with multiple challenges. The ongoing war in Ukraine, potential gas shortages, and high inflation rates have created a turbulent environment. The European Central Bank raised interest rates to the highest level seen in the last two decades and expects to raise them once again in July, leading to concerns about the cost of living and the possibility of a recession.

The United Kingdom is attempting to curb inflation while carefully monitoring potential risks to economic growth. The Bank of England has been forced to raise interest rates at a faster pace than anticipated, driving sterling’s strong performance this year so far.

China, despite maintaining accommodative monetary policy due to low inflation rates, is facing a slowdown in growth. This deceleration primarily stems from cautious consumer behaviour and a slow recovery in the property market.

Shifting our focus to the fine wine market, the En Primeur campaign began in May and concluded in June, to mixed reviews. Whilst there was no doubt about the high quality of the wines, the campaign also recorded the highest average release price increase in recent history, and some merchants found they could not sell the wines regardless of cost.

The industry-leading benchmark for monitoring fine wine prices, the Liv-ex 100, experienced a further decline in June, dropping by 2.9% compared to the previous month and 6.1% year-to-date. These figures reflect a challenging time in the fine wine market, but not one without opportunities for those who know where to find them.

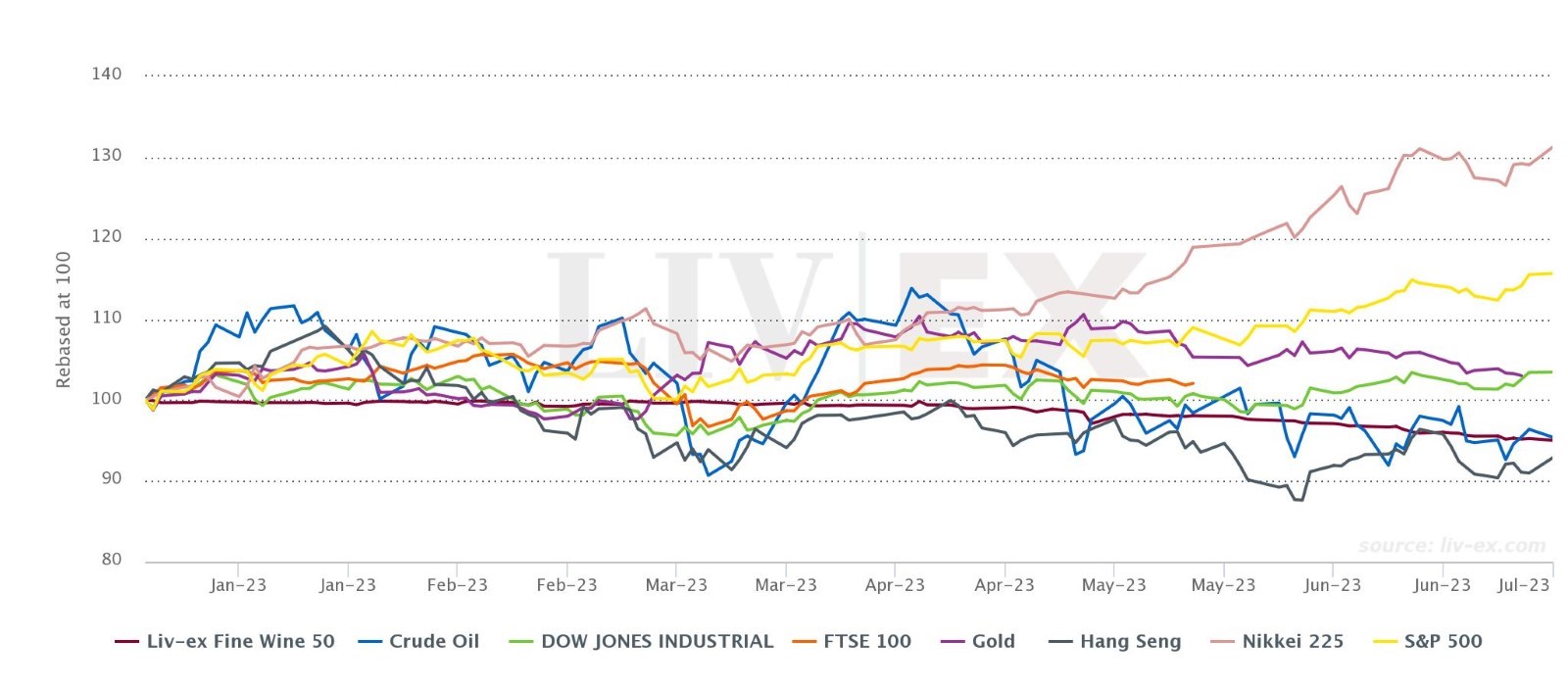

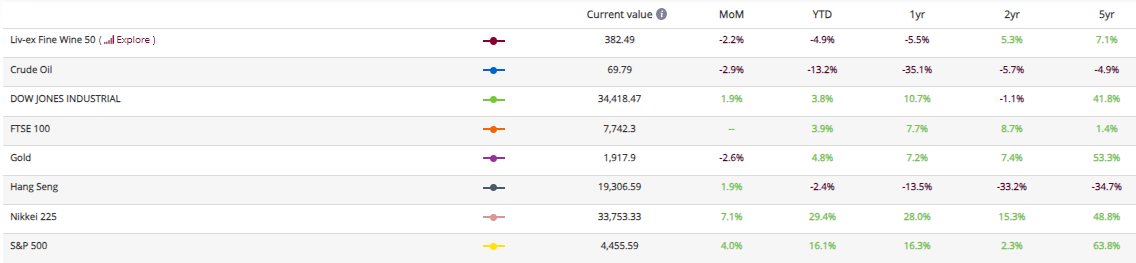

Fine Wine 50 vs equities

*made using the Liv-ex Charting Tool. Data taken on 04.07.2023.

In contrast to the fine wine market, the S&P 500 and the Dow Jones Industrial have shown positive performance over the past year, increasing by 16.3% and 10.7% year-on-year respectively. The fine wine market (represented by the Liv-ex Fine Wine 50) experienced a decline of 5.5% in the same period. In the first quarter of 2023, the decline recorded in the index was only 0.9%.

Among other indices, only two fared worse than the Liv-ex Fine Wine 50: Crude Oil and the Hang Seng. Over the same past year, the Hang Seng index has struggled, falling by 13.5% due to tech stock drops, while Crude Oil experienced a decrease of 35.1% due to ongoing conflicts.

While major financial markets have seen positive gains in June and over the past year, the fine wine market is facing a slowdown, reflecting the uncertainty of the macroeconomic context and the general caution prevailing in the market.

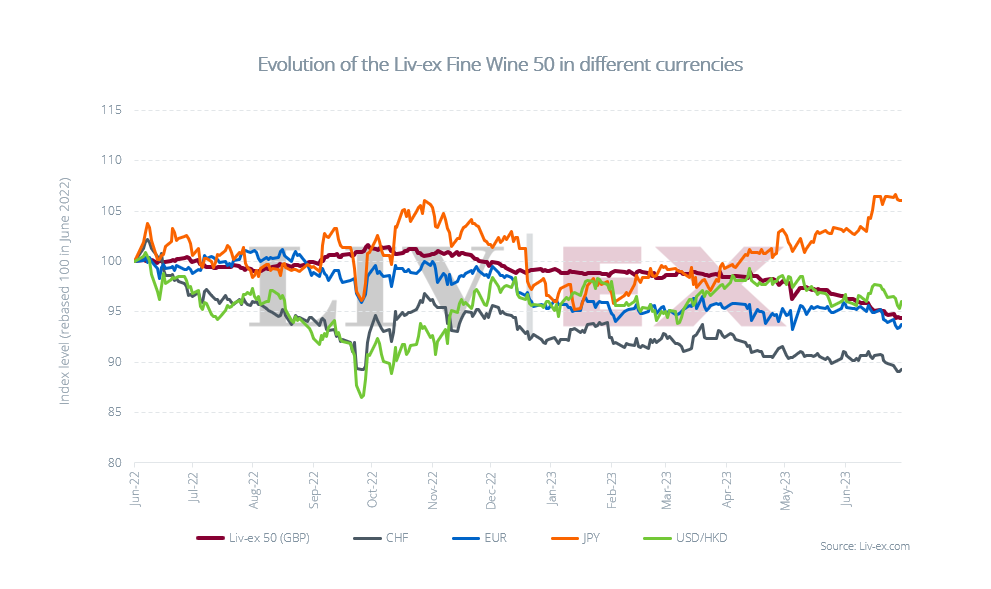

Currency overview

The chart below shows the Fine Wine 50 in Sterling and in alternative currencies.

During the second quarter, Sterling demonstrated resilience, rising around 3% against the US dollar. This upward movement can be attributed to policymakers raising interest rates as a means to manage inflation. Additionally, the pound had a remarkable quarter against the yen, recording a 12% climb, the highest since 2012. This surge was driven by the Bank of Japan’s decision to maintain an extremely loose monetary policy, which is reflected in the rise of the Liv-ex Fine Wine 50 in Japanese yen (in orange below).

In terms of other currencies, the Liv-ex Fine Wine 50 in EUR, CHF, and USD/HKD showed stability throughout the quarter. This brings advantages to buyers operating with these currencies, as it creates a more predictable environment in which to conduct their purchasing decisions.

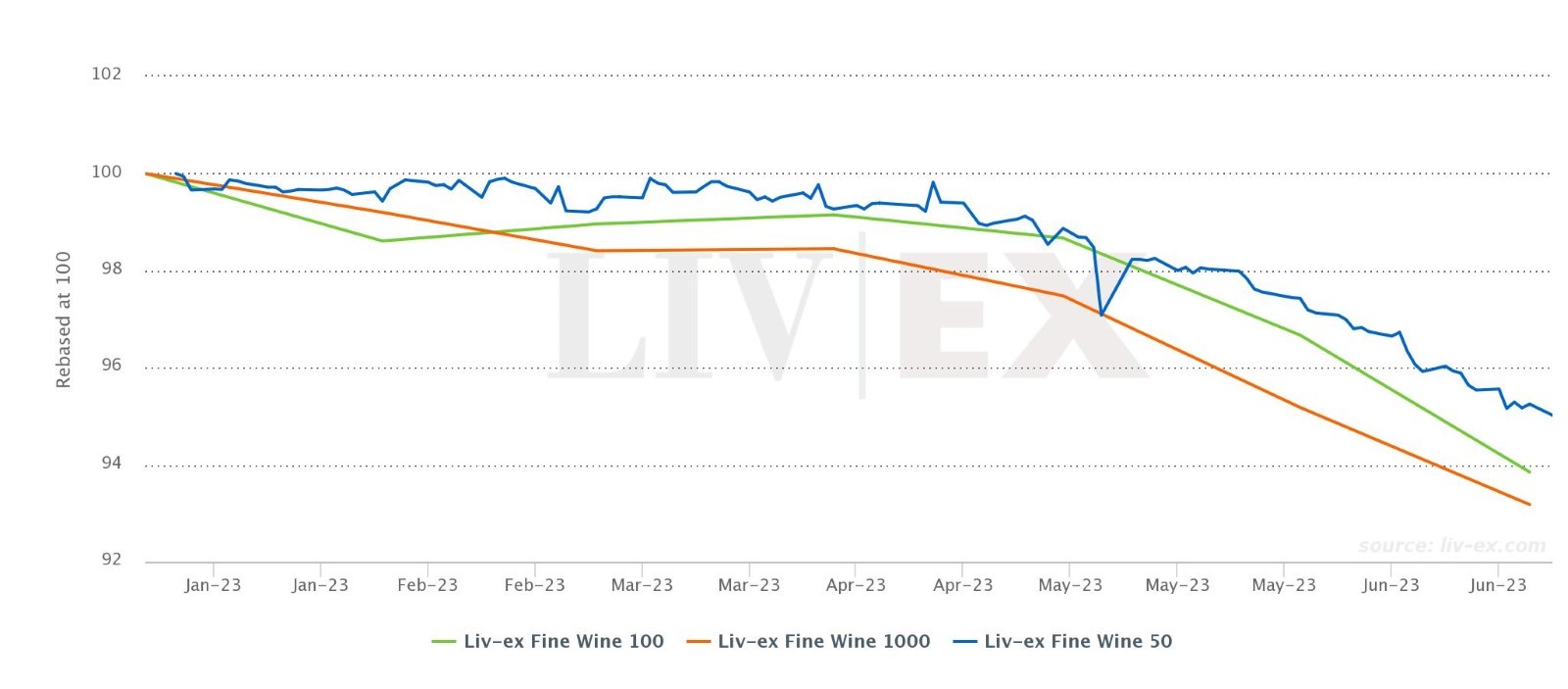

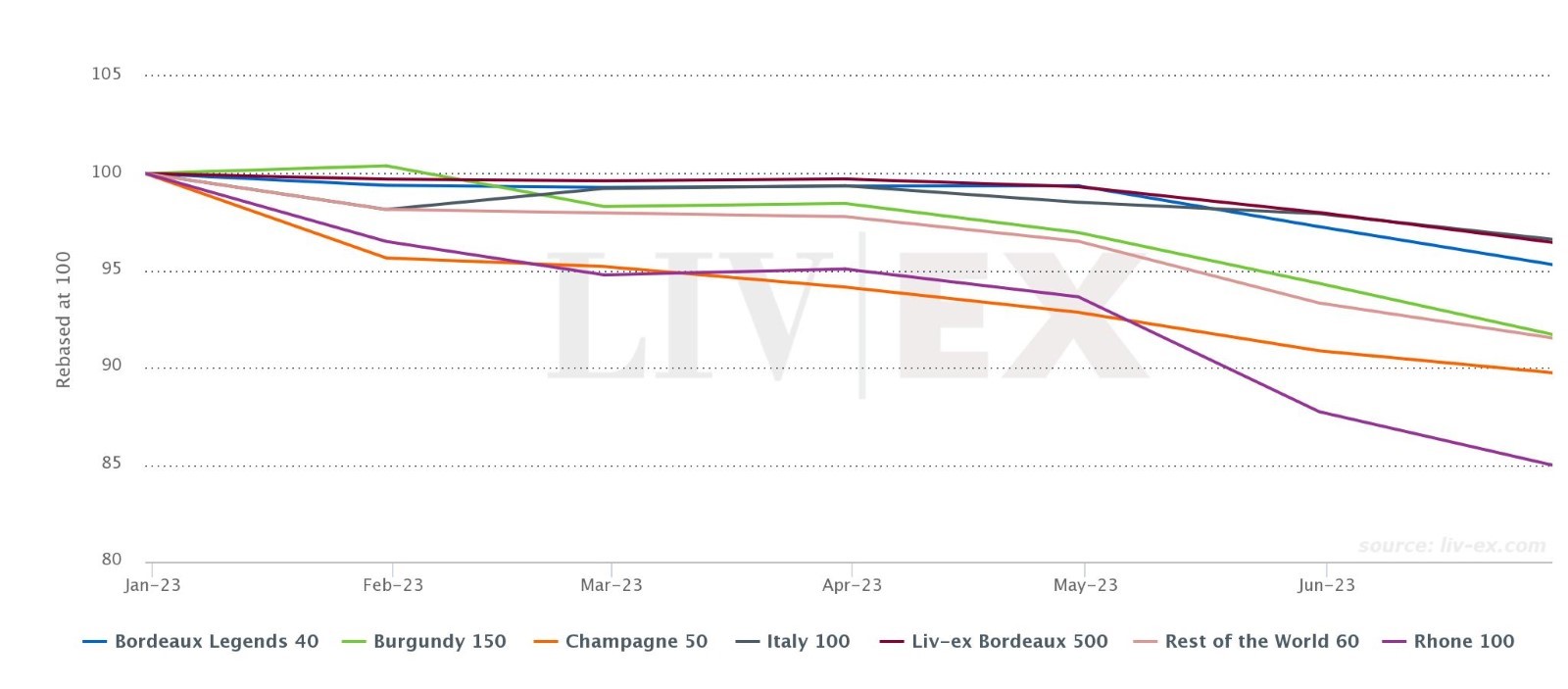

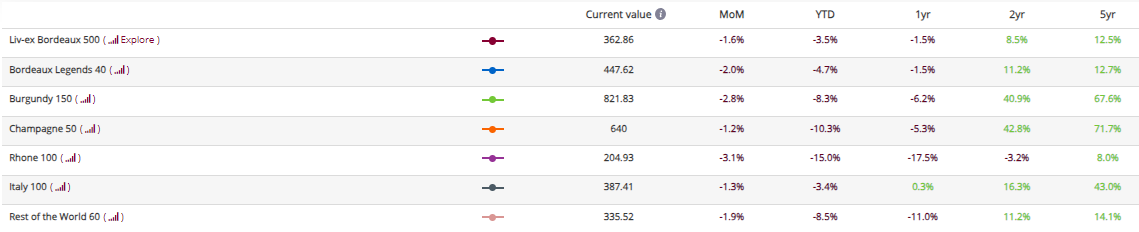

Liv-ex 1000 sub-indices

*made using the Liv-ex Charting Tool. Data taken on 04.07.2023.

As mentioned earlier, the fine wine market is currently experiencing a downward trend, evidenced by all the major Liv-ex indices falling. In June and year-to-date, all the indices have recorded a decline. The benchmark Liv-ex 100 index, tracking the 100 most-traded fine wines on the secondary market, has dropped by 6.1% since the start of the year. Similarly, the Liv-ex Fine Wine 50, which monitors the price of First Growths, has experienced a decrease of 5.2%. The broadest measure of the market, the Liv-ex Fine Wine 1000 is also down 6.8% year-to-date.

Looking at the sub-indices within the Liv-ex 1000, we also observe a consistent downward movement. All the sub-indices experienced a decrease both in June and year-to-date. The Champagne 50 has recorded a significant decrease of 10.3% in its year-to-date performance. The Rhône 100 faced the largest decline in June, falling by 3.1%.; it is also the poorest performer year-to-date, with a substantial drop of 15%.

Despite the En Primeur campaign happening this quarter, the Bordeaux 500 and Bordeaux Legends 40 have also suffered declines, perhaps testament to the mixed reception it encountered. In June, the Liv-ex Bordeaux 500 was down 1.6%, while the Bordeaux Legends 40 dropped by 2%. Year-to-date, these indices have declined 3.5% and 4.7% respectively.

*made using the Liv-ex Charting Tool. Data taken on 04.07.2023.

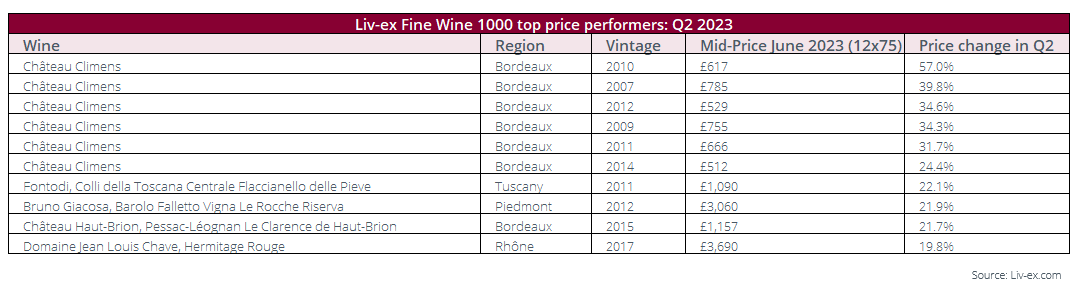

Top price performers

As mentioned in our July Market report, Barsac’s price performance remained strong, with prices for back vintages of Château Climens and Château Coutet continuing to rise last month. This trend has been consistent over the quarter, with six of the top ten price performers from the Liv-ex Fine Wine 1000 being from Château Climens, namely the 2010, 2007, 2012, 2009, 2011 and 2014 vintages.

The 2022 vintage of Château Climens was released at €106.25 per bottle ex-négociant with a recommended retail price of £1,340.40 per 12×75. However, higher-scoring back vintages benefitting from a few years in bottle and offered at a lower price than the 2022 release are available on the market. The relative scarcity of Château Climens releases, which have been strongly affected by bad weather in recent years, means it is not surprising that these back vintages dominate the rankings.

Fellow Bordeaux wine Le Clarence de Haut-Brion 2015 also featured in the top price performers, its Mid Price increasing 21.8% over the quarter. The 2022 vintage of Le Clarence de Haut-Brion was released at €132 per bottle ex-négociant and offered by the international trade for £1,584 per 12×75.

The prices shown in the table above are Liv-ex Mid-Prices. The Mid-Price is the mid-point between the highest live bid and lowest live offer on the market. These are the firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 620+ of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable. Prices given are for 12x75cl trades, or 6x75cl converted to a 12x75cl price.

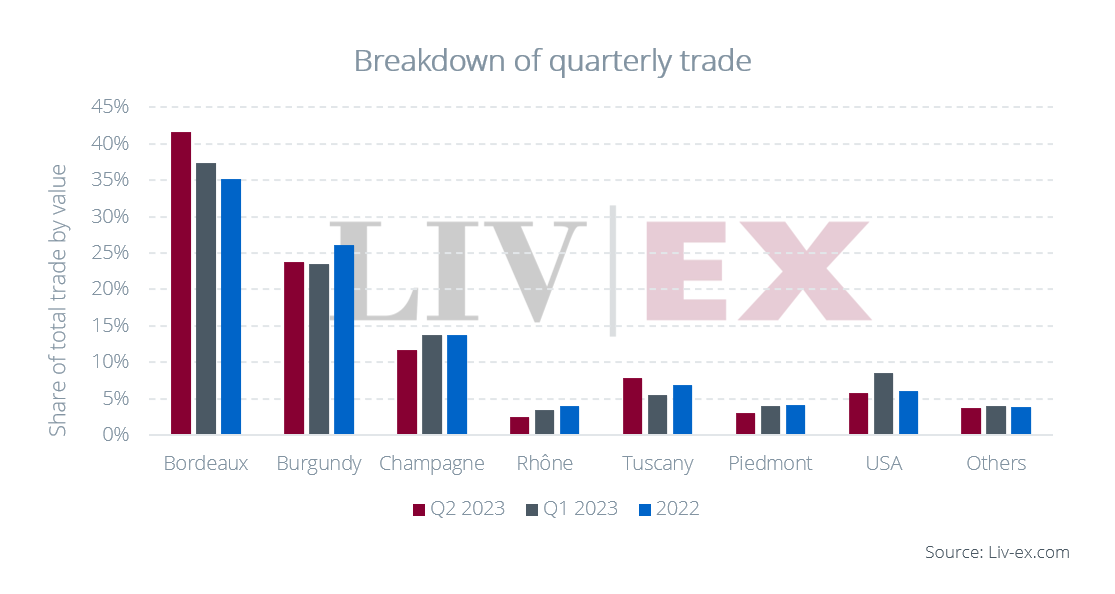

Trading overview in Q2

Bordeaux maintained its leading position in the last quarter, accounting for 41.6% of total trade by value, up from 37.3% in Q1. This exceeds its 2022 average of 35.1%. Demand was driven by Europe and the USA, accounting for 37.7% and 25.8% of Bordeaux buyers on Liv-ex respectively.

Tuscan wines also had a positive quarter, with 7.8% of trade by value, above the region’s 2022 average of 6.9%. Burgundy experienced a slight improvement, its market share increasing to 23.8% from 23.5% in the previous quarter.

On the other hand, all other regions including Champagne (11.7%), the Rhône (2.5%), Piedmont (3.1%), the USA (5.8%), and the ‘Others’ category recorded declines in their trade shares.

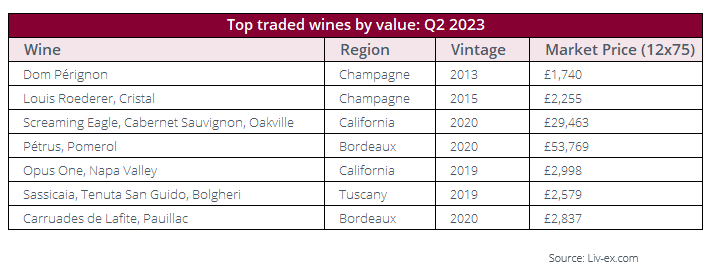

Top-traded wines in Q2 2023

As Champagne prices continue to decrease, buyers are actively seeking deals at favourable prices. Dom Pérignon 2013 was the top-traded wine by both volume and value in Q2 and year-to-date. Its market price of £1,740 has fallen since the end of May, when it was £1,830 per 12×75. Louis Roederer Cristal 2015 was also among the top-traded wines by value this quarter.

It is interesting to note that five out of the top seven wines traded by value were either from the 2019 or 2020 vintages. Opus One 2019, was released in September 2022 for £3,024 per 12×75 and scored 97-99 points by the Wine Advocate. Screaming Eagle was also recently released in January 2023.

In terms of volume, Bordeaux dominated the top-traded list, with four out of the top seven wines, namely Château Lynch-Bages 2017, the 2014 and 2016 and Château Pontet-Canet 2015. Champagne followed closely, securing three of the top seven spots as buyers took advantage of attractive prices, including for Taittinger, Comtes de Champagne Blanc de Blancs 2012.

The prices shown in the table above are Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. It is always presented for a 12×75 case unless otherwise stated. To calculate the Market Price, we look at list prices from a large group of trusted international merchants. Preference is given to prices from stockholders over brokers, to cases over single bottles, and to recent prices over older prices. The algorithm behind it runs every day, evaluating a pool of over 1 billion data points to determine the most accurate Market Prices for 240,000+ wines.

Conclusion

The fine wine market in Q2 faced considerable challenges amid a complex global economic landscape. The discrepancy between the fine wine market’s performance and the positive gains observed in major equities raises questions about the factors influencing the former’s declining trend.

By staying informed about market trends and leveraging data, buyers can make informed decisions and capitalise on emerging opportunities. The stability displayed by certain currency indices also offers a predictable environment for buyers operating within those. For sellers, setting the right price and adapting to market dynamics can lead to trade.

By seizing opportunities offered by this softer fine wine market, both buyers and sellers can navigate find success in the second half of the year.

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 60 of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable.

Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.