Print and read offline instead.

Fine wine holds steady as mainstream markets react to war

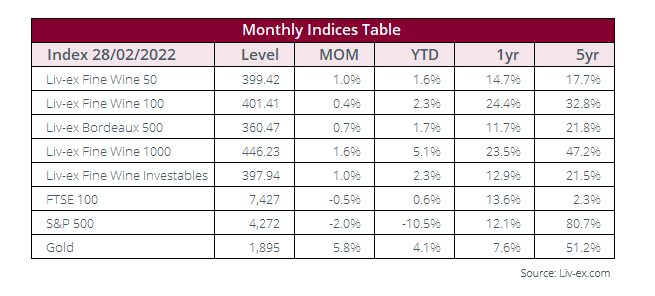

Fine wine managed to maintain its upward movement in February despite the headwinds that affected mainstream assets, including slowing GDP growth, rising inflation and Russia’s invasion of Ukraine.

The Liv-ex indices rose again in February although their gains were smaller than those made in previous months. The Liv-ex 100 moved up 0.4%, while the broadest measure, the Liv-ex 1000, went up 1.6%. Its performance was pushed by the Burgundy 150 (3.6%) and the Italy 100 (2.0%). The Rest of the World 60 was the only sub-index in decline, dipping 0.9%.

The ‘others’ category also lost some trade share in February, taking just 3.7% of the market by value. Bordeaux (32.3%), Burgundy (26.3%), Champagne (12.8%), the Rhône (5.8%) and Tuscany (7.0%) all made gains. Demand was mostly UK and US-led, with small but discernible decline in Europe.

The limited-edition Salon Le Mesnil-sur-Oger Oenotheque Assortment Case led trade by value in February, selling for as much as £7,940 per 1×600. Screaming Eagle Cabernet Sauvignon 2019 was the second-most traded wine, enjoying heightened demand ahead of the Super Bowl.

High marks for Lafleur

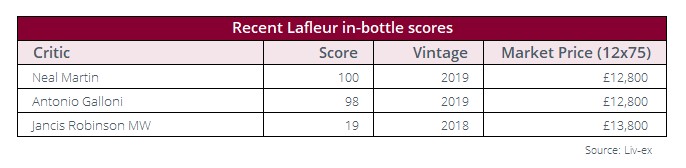

Château Lafleur has received multiple high scores from leading critics in February. The Pomerol estate’s 2019 and 2018 vintages were recently reassessed by Neal Martin, Antonio Galloni (both Vinous) and Jancis Robinson MW as part of wider retrospectives.

Robinson rated the 2018 19-points, saying it had ‘real energy’. The wine has a current Market Price of £13,800 (12×75) and has appreciated in price over 100% since its release.

The 2019, meanwhile, was scored 100-points by Martin during his in-bottle tasting of the vintage. He deemed it an ‘awe-inspiring Pomerol’ that ranked alongside the 1982 and 2000. He did add that it was wine that needed time ‘to reach its zenith’.

Fellow critic at Vinous, Antonio Galloni, rated it 98-points. He agreed with Martin that it was a wine that needed time and that, its energy ‘focused inward’, but one where ‘the purity of flavours is just unreal’.

The wine currently has a Market Price of £12,800 (12×75) and is likewise up over 100% since its release in 2020.

Bordeaux 2009 and Tuscany 2016 move the market

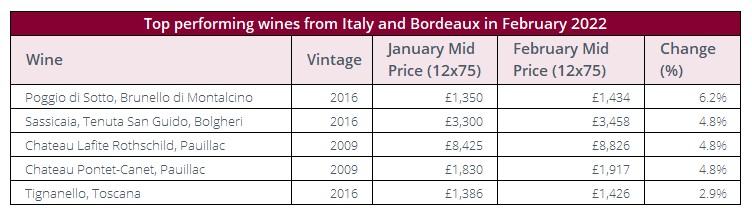

Fine wines prices saw a modest increase in February. Among the biggest movers were two wines from Bordeaux’s 2009 vintage, which went up 4.8%. But while Château Pontet-Canet has more than doubled in value since release, Château Lafite Rothschild remains available at a discount to its release price.

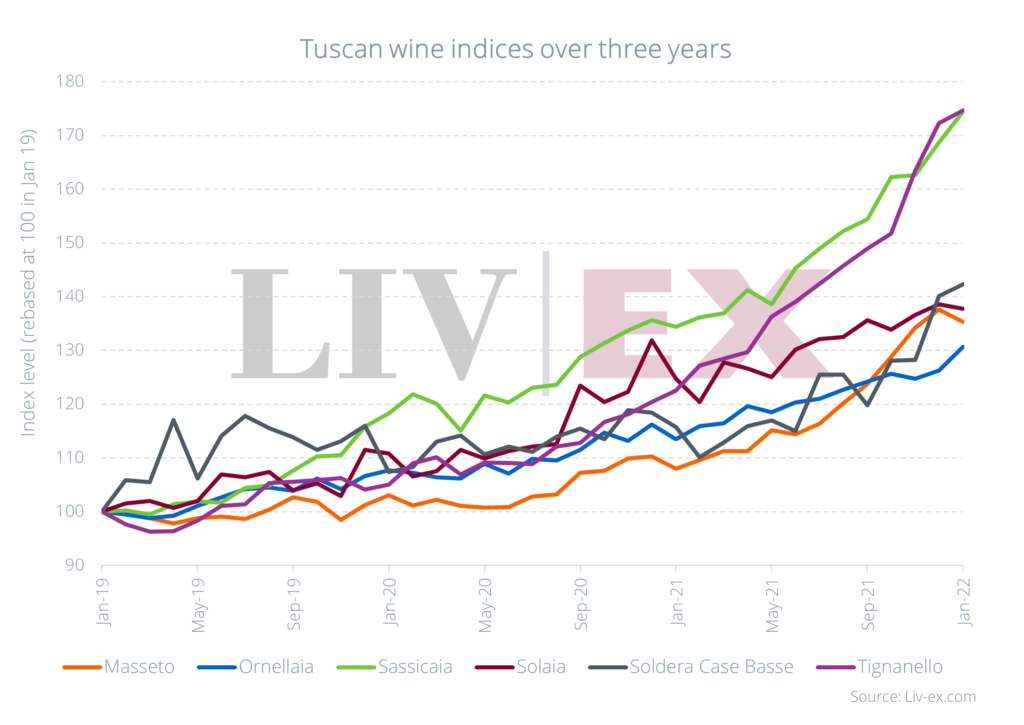

The Super Tuscans Sassicaia and Tignanello 2016 also rose 4.8% and 2.9% respectively. The two brands are Italy’s best-performers over the past three years. The top-performer in February, however, was Poggio di Sotto Brunello di Montalcino 2016 which went up 6.2%.

Rising demand for rosé Champagne

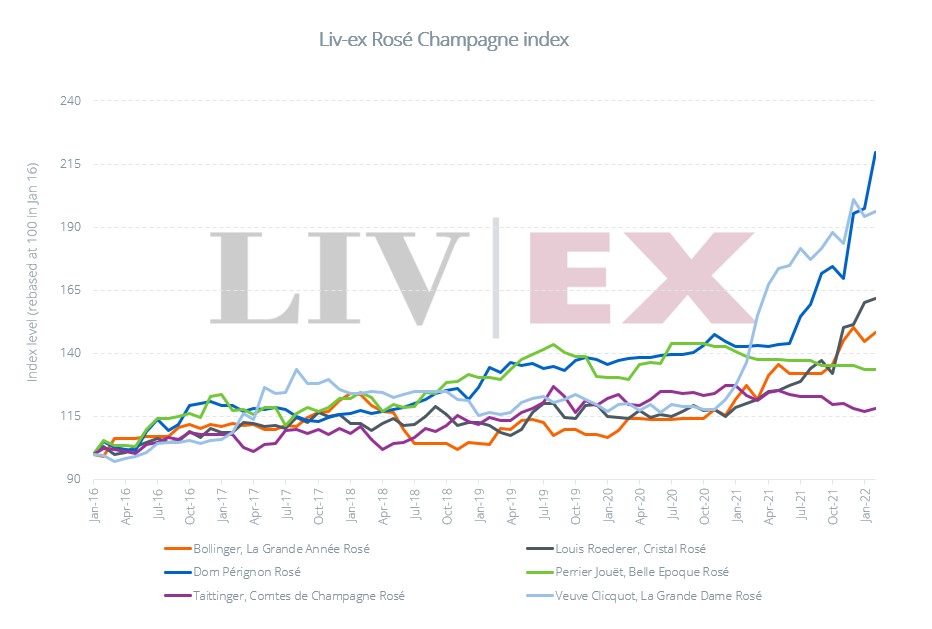

In 2021, the Champagne 50 index was the best-performing sub-index of the Liv-ex 1000. Although the index is led by classic ‘blanc’ Champagne, demand for Champagne as a whole is also driving trade in the pink version too.

Rosé accounted for 16% of total Champagne trade in 2021, driven primarily by demand for four key labels: Dom Pérignon, Taittinger’s Comtes de Champagne, Louis Roederer’s Cristal and Bollinger’s La Grande Année. The price performance of the individual wines can be seen in the chart above.

Industry News

Rioja winery suspends Russia trade

Spanish estate La Rioja Alta has announced it is suspending all exports to Russia. The decision was taken following Russia’s invasion of Ukraine. The bombardment of Ukraine’s capital Kyiv has resulted in the destruction of the warehouse operated by importer Good Wine, which represents La Rioja Alta and many other well-known labels in Ukraine. Numerous other wineries and drinks groups have announced similar measures, as well as charitable donations to various causes in aid of the growing refugee crisis sparked by the conflict.

New appointments in Bordeaux

Château Pichon Baron, Château Montrose and Château Lafon-Rochet have both announced new appointments at their respective estates. Pichon Baron has named Pierre Montégut as its new technical director. He replaces the retiring Jean-René Matignon who is stepping aside after 36 years. Pierre Graffeuille, formerly director at Léoville-Las-Cases, will be joining Montrose in the same capacity. And Lafon-Rochet has appointed Christophe Congé as its new managing director. Congé was previously an oenologist at Château Lafite Rothschild and its stable of properties.

Yquem announces new release programme

Château d’Yquem recently revealed its new release programme and ‘Lighthouse’ scheme. The Sauternes estate announced last year that it was henceforth moving the release date of its new vintages to March, with the 2019 vintage due for release on the 22nd. The domain is also launching a by-the-glass programme with a selection of ‘Lighthouse’ on-trade accounts around the world where Yquem will be served by the glass.

François Pinault invests in Champagne

The owner of Château Latour, François Pinault, has taken a minority stake in Champagne Jacquesson. The deal adds a Champagne brand to Pinault’s portfolio of wine estates under his Artémis Domaines holding group, which also includes; Clos de Tart, Château-Grillet and Eisele.

New Masters of Wine

Two new Masters of wine were announced at the end of February. Justin Martindale MW and Jonny Orton MW, both based in the UK, bring the total number of MWs to 420.

Alain Graillot dies

Rhône winemaker Alain Graillot has died aged 77. Graillot became the standard-bearer for Crozes-Hermitage in the 1990s and his wines were frequently cited in leading wine publications.

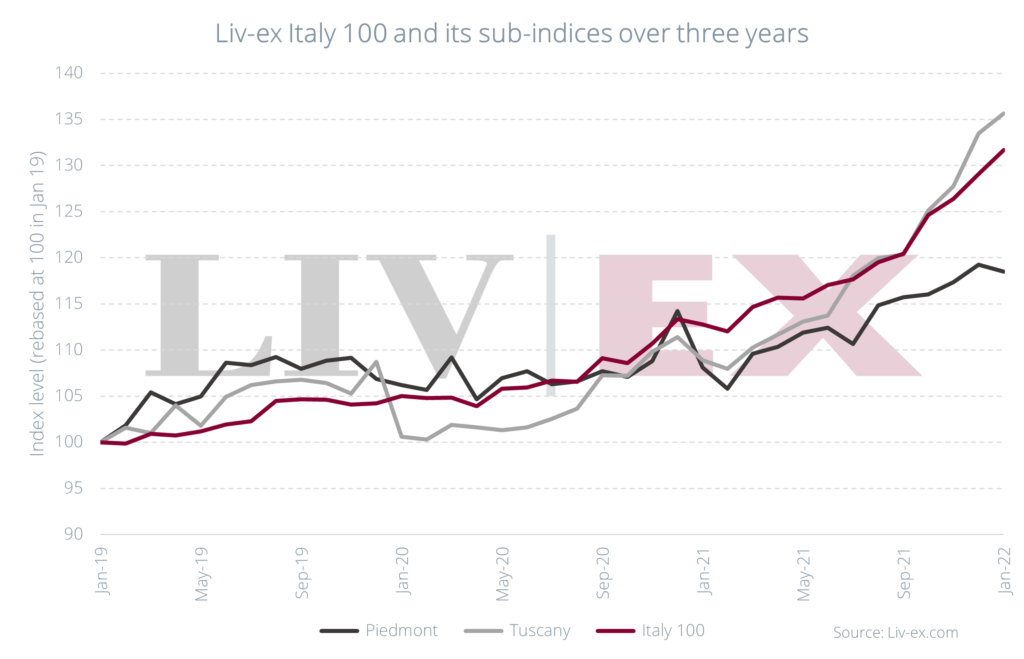

Inside Italy’s regional price performance

Italy is one of the fastest expanding regions in the secondary market. The country has seen a sustained increase in the number of wines trading – which have grown fivefold in the last five years – pointing to heightened demand for its fine wines. Over the same period, the number of Italian regions traded on Liv-ex has risen from 16 to 68.

With more ‘drinking’ wines enjoying secondary market demand, a greater number of Italian regions are starting to trade. But regular investment interest remains centred on Tuscany and Piedmont. These two regions combined account for 97% of the country’s trade by value and are home to many of the country’s top-performing wines.

Tuscany and Piedmont’s contrasting entry points

The entry point into the Tuscan market is lower than it is for Piedmont. In 2021, the average Market Price of the six Tuscan wines included in the Italy 100 index (Masseto, Soldera Case Basse, Solaia, Sassicaia, Ornellaia and Tignanello) was £3,139 per 12×75 across their last 13 vintages, compared with £4,411 for the four Piedmont labels (Giacomo Conterno Barolo Monfortino Riserva, Giacomo Conterno Barolo Francia, Bartolo Mascarello Barolo, and Gaja Barbaresco).

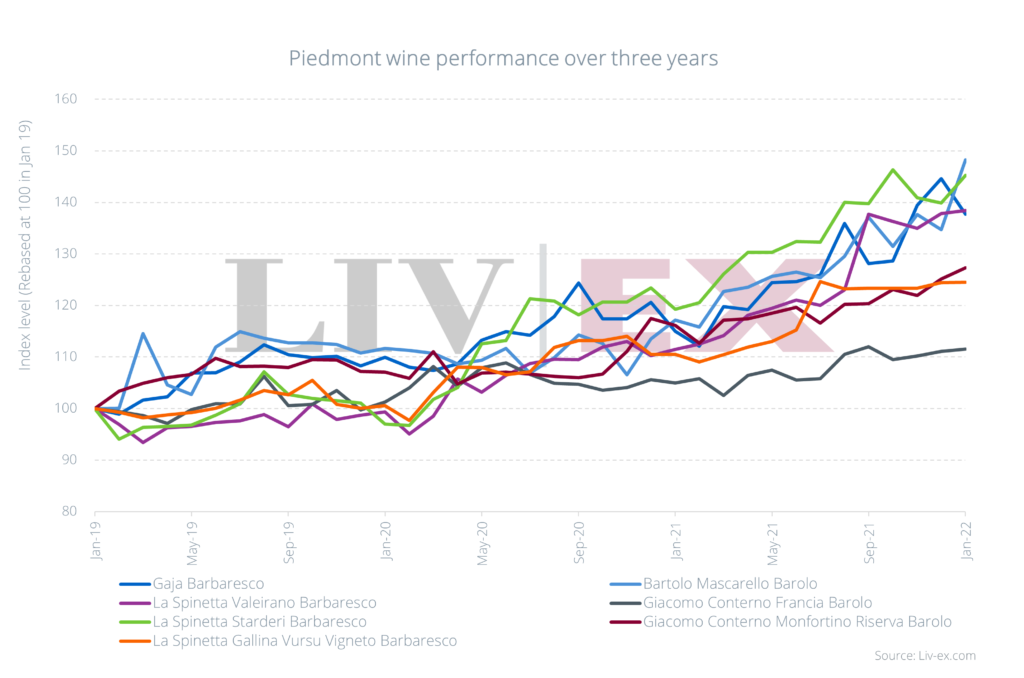

But the Piedmont market is not uniform when it comes to price positioning and market performance. The top three Barolo wines cost £5,344 per case on average; the top-traded Barbaresco labels – La Spinetta’s Starderi, Valeirano and Gallina Vursu Vigneto, and Gaja, trade at just £1,235 a case.

The Super Tuscans are getting more expensive

Over the past three years, Tuscany has rewarded collectors with the best returns. As the chart below shows, the Tuscany index (35.6%) has outperformed the broader Italy 100 index (31.7%) and its northern neighbour Piedmont (18.5%).

Tignanello and Sassicaia are brands on the move

The most affordable Super Tuscan Tignanello has been Italy’s biggest riser. The brand’s value has increased 74.7% over the past three years, just above that of Sassicaia – 74.4%. From Tignanello, the 2018 vintage has led both activity (by value and volume) and price performance in the last year. The wine has been the third-most traded from Tuscany overall, surpassed only by Sassicaia 2017 (2nd) and 2018 (1st).

Over the past three years, Soldera Case Basse has risen 42.4%, Solaia 37.8%, Masseto 34.3%, and Ornellaia 30.7%.

Movement within Piedmont

Meanwhile, Piedmont’s most active wines have risen between 11% and 48%. Bartolo Mascarello Barolo has been the top-performer, up 48.2%. Its 2017 and 2016 vintages have been the most active, while 2010 and 2009 have seen the biggest price rises.

La Spinetta’s Starderi (45.2%) and Valeirano (38.4%) have also been subject to heightened demand and have gone up in value. Gaja’s Barbaresco (37.7%) has been driven by strong performances from its 2010 and 2012 vintages.

Strong positioning

Italy offers accessible points of entry and strong investment returns. Its expanding secondary market is attracting drinkers and collectors, while its biggest brands continue to deliver impressive performances. In recent years, Piedmont has gained a larger share of the market by value, while Tuscany is seeing its fine wines record greater price gains. So far in 2022, both Piedmont and Tuscany have accounted for equal levels of trade.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 560+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.