Burgundy 2022 – Hair of the dog

Introduction

On paper, the Burgundy 2022 vintage is everything producers and buyers were after: good quality, highly-rated wines in decent volumes (at least, in comparison to 2021).

The exceptionally low yields in 2021 led many producers to hike prices simply in order to keep the lights on. Some had nothing to release at all, while the great majority were forced to cut allocations hard due to the scarcity of the wines. But pushing through large price increases on some of the world’s most expensive wines just as the market was beginning to turn was never going to be a popular call.

For many, the Burgundy 2021 En Primeur campaign was the straw that broke the camel’s back, highlighting the unaffordability of Burgundy even at the village level. Granted, most of the wines sold out, but much of that can be attributed to volumes being slashed rather than a surge in demand.

A little over a year into a correction that has seen the benchmark fine wine indices record double-digit declines, the Burgundy market desperately needed some good news. It needed a decent yield to satiate a dangerously thin market – it got that, to the relief of growers and merchants alike. It needed decent quality to help move the greater volumes of wine at the region’s now elevated prices. According to critics, it got that too. And some. The cherry on the cake would be prices that encouraged buyers, old and new, to participate and clear the stock available.

It seems that producers have broadly listened to the market and kept price hikes to a minimum. A small proportion (roughly 10%) lowered their prices year-on-year, while about 40% of producers raised their prices, even if only modestly, which has made selling tricky in some quarters. That said, most allocations have been restored, and merchants remain hopeful the 2022 vintage will eventually sell through, albeit at a slower pace than in recent years.

Have buyers stepped up to the mark and ‘filled their boots’ with 2022 Burgundy, as advised by Neal Martin? It’s still too early to say. The news flow is a little mixed as some merchants have only just started their campaigns, but what is clear is that it has so far gone better than many dared imagine late last year.

Critics and trade view on the vintage – Mind the gap

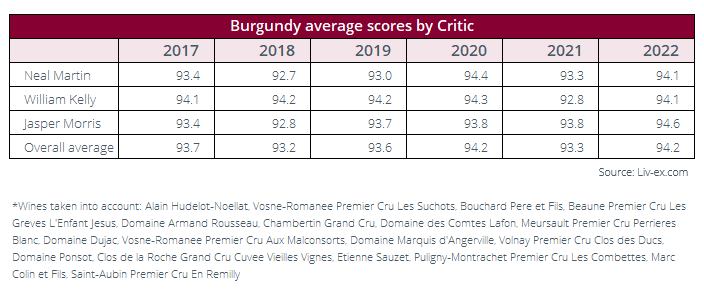

Despite 2022 breaking temperature records and the month of June bringing localised hailstorms and even flooding in some areas, the 2022 vintage will be remembered as an answered prayer for most producers. Indeed, it was the first year at ten-year average yields (between 40-45hl/hectare) after a series of small vintages, and the cold nights preserved acidity in the grapes, leading to high-quality wines across the board.

‘I cannot remember a Burgundy vintage that elicited so much joy from barrel’, writes Neal Martin about the 2022 vintage. The wines, according to the critic, ‘are primed for early consumption’, but are also ‘blessed with the balance and substance to mature exquisitely in bottle’. His scores reflect his enthusiasm for the latest vintage; on average, they are second only to the 2020s.

Jasper Morris was similarly enthused about the 2022s. The name of his vintage report, ‘Bountiful and Beautiful’, is a good summary of his feelings towards the wines. As Martin does, he recommends ‘going large in 2022’, ‘a pleasingly consistent vintage in both colours and across classification levels’. His average score for the nine wines considered was the highest of the last six vintages.

However, Neal Martin followed his rave reviews of the wines with a ‘fair warning’ about the Burgundy market, which he likens to being strapped into a sports car in which the accelerator has become stuck. Pricing, he advises, ‘ought to be using prices consumers are willing to fork out’, which of course is affected by the challenging macroeconomic context.

A look into the reason behind price increases is necessary, however, according to Morris who highlights the rising cost of grapes and juice (about 15% up in 2022, according to Wine-Searcher) for winemakers who buy them in. Deciding on pricing is thus not only dependent on the volume or quality of the vintage; many winemakers’ cost base is currently ‘out of kilter with the reality of where the market is’.

While the volumes of 2022s (and 2023s) should offer relief to producers, the challenging market conditions means the gap is widening between their release prices and what buyers are willing to pay. Considering that the upward momentum of the Burgundy market relies in no small part on scarcity, which will not be a problem this year or next, prices may need to adjust down to attract significant demand.

The state of the Burgundy market

One year into the downturn

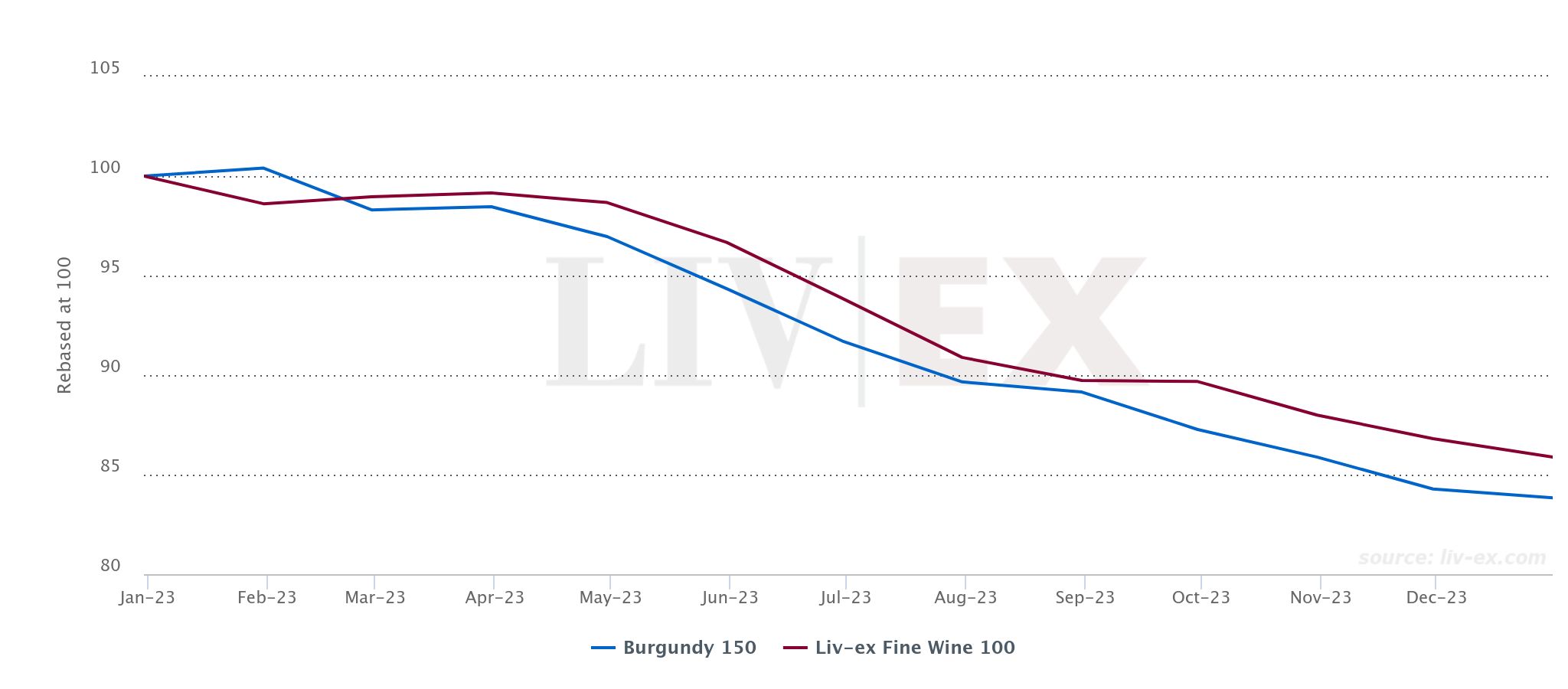

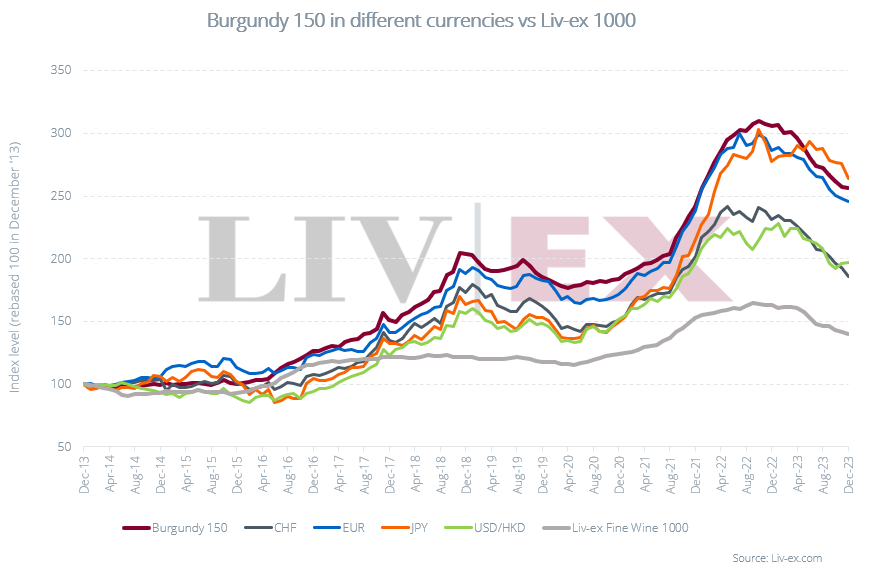

The Burgundy 150’s latest peak was in October 2022. Since then, the index has fallen 17.4%, more than the Liv-ex Fine Wine 100, the industry benchmark tracking the most traded wines on the secondary market.

*Made with the Liv-ex Charting tool.

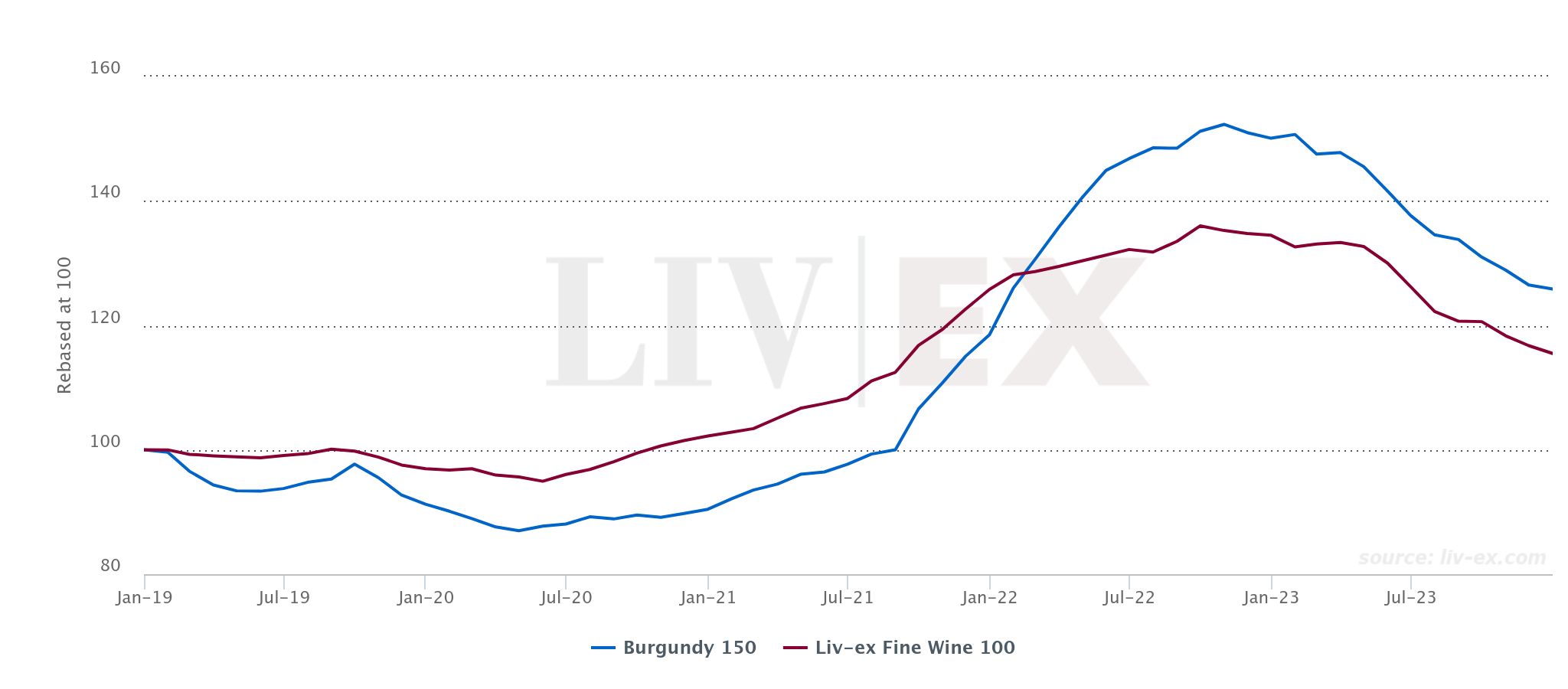

However, it’s worth noting that on a five-year basis, the Burgundy 150 remains up on the Liv-ex 100, having peaked considerably higher in October 2022.

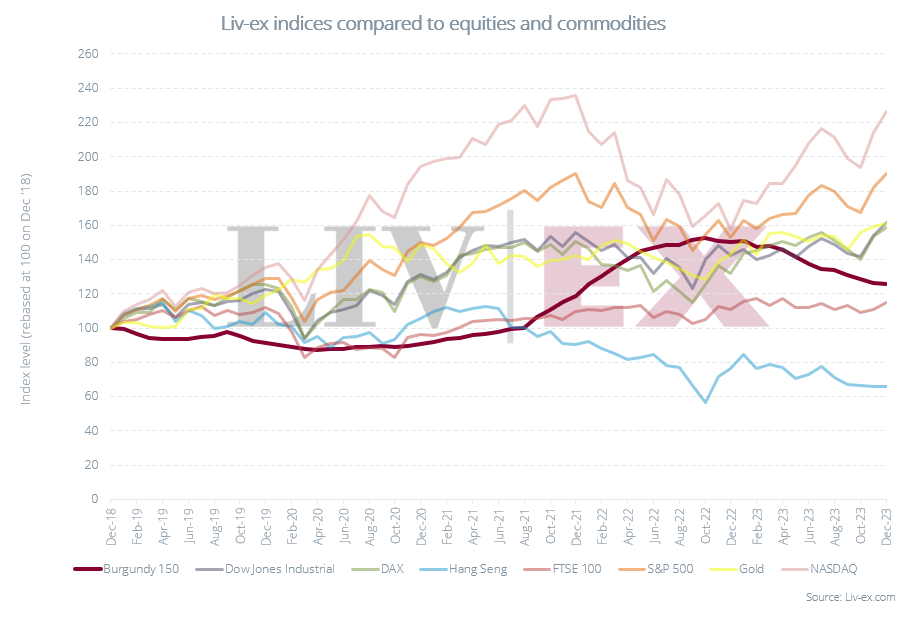

Compared to equities and commodities, the Burgundy 150 looks far less buoyant than it did at its peak. Back in October 2022, it was outperforming most major financial indicators including Gold; fast-forward to December 2023, and only the Hang Seng and the FTSE100 are lagging behind.

Viewed in different currencies, the strength displayed by the US Dollar means that the pullback will have been felt less harshly by buyers in USD/HKD, with the October 2022 peak being far less pronounced.

Burgundy 150 components

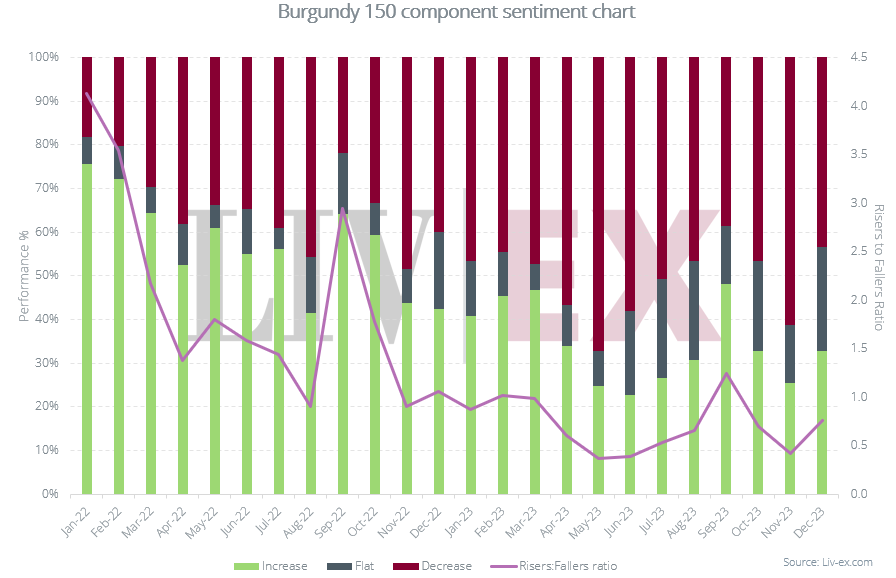

Looking at the chart below, the evolving sentiment toward Burgundy is clear: over the last two years, an ever-decreasing number of the Burgundy 150’s components have recorded monthly rises.

Interestingly, sentiment rallied in September 2022 and 2023, the result of a pickup in activity after the summer recess. The reasons are unclear, but it is possibly a result of buyers positioning themselves ahead of Thanksgiving and Christmas.

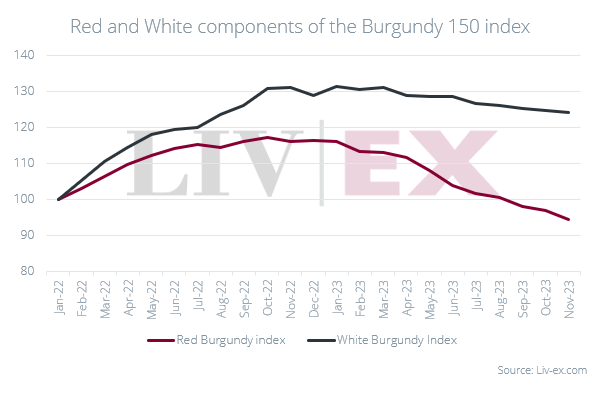

The Burgundy 150 ended 2023 with 57% of its component wines running flat or falling month-on-month, slightly up from November. The index’s white wine components were noticeably more successful in 2023 than their red counterparts, as shown in the chart below.

In the 2023 Liv-ex Power 100, we highlighted the positive performance of white Burgundy brands. White Burgundies tend to be drunk earlier than reds, meaning their prices remain buoyed by diminishing supply, limiting the impact of overall market declines (driven by the broader market sentiment).

That said, there is growing encouragement from critics and merchants alike to ‘be braver’ when it comes to their Burgundy consumption. David Roberts MW, buying director at Goedhuis, told the Drinks Business that ‘the ‘22 vintage offers that opportunity to change our mindset to be able to drink red Burgundy, and also white Burgundy young, as well as ageing it long-term’. Were buyers to embrace that advice, prices over the year ahead might find greater support, helping to offset the potential negative effect of the larger volumes coming to the market. Burgundy 2023 already looms large in the minds of many.

Prices by classification

When analysing the Burgundy market, considering only the Burgundy 150 is limiting. Indeed, the region’s top 15 Grands Crus operate in a league of their own in terms of the prices they command. They represent the pinnacle, the most collectible, but rarely the most accessible. It is important to consider how prices are evolving across all classifications.

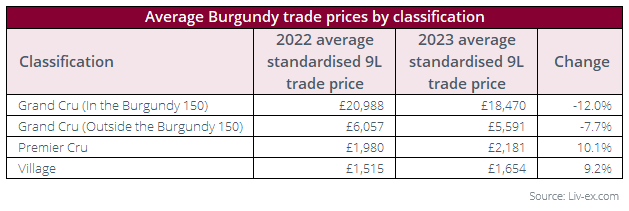

Looking at average trade prices, the very top Grands Crus have seen the biggest dip year-on-year. The wines in the Burgundy 150 recorded a 12.0% fall in their average trade price, compared to 7.7% for Grands Crus outside of the index. Even more striking is the fact that Premiers Crus and Village wines traded on average 10.1% and 9.2% higher in 2023 than in 2022.

That said, these increases are nowhere near the ones recorded in 2022, when Grands Crus were trading on average over 50% higher than in 2021, versus 31.3% for Premiers Crus and 57.7% for Village wines. It’s also worth noting that these trade prices are averaged out over a year, which means they might be skewed by a rather more buoyant start of 2023. Indeed, the trade value of Burgundy wines was down 31.8% from January to December 2023, and volume was down 31.2% from its peak in March 2023 to December 2023.

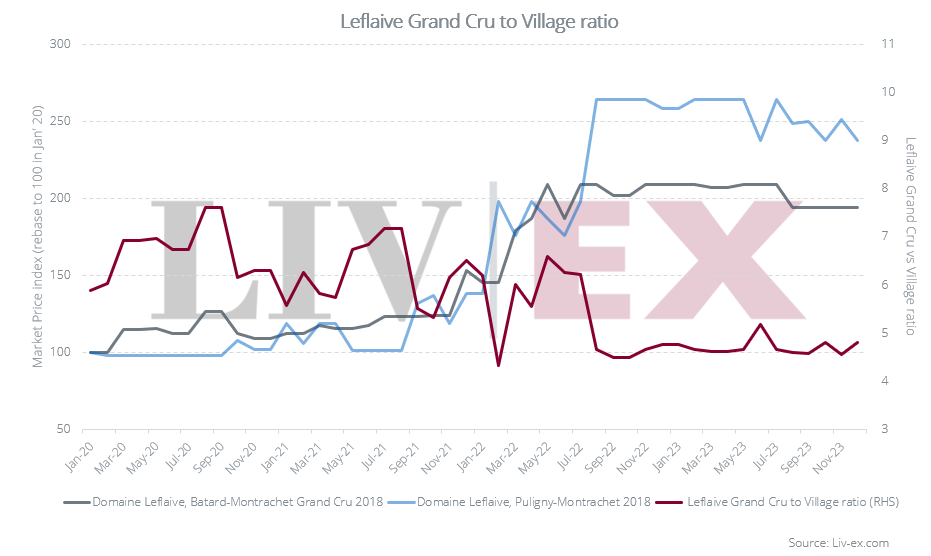

This discrepancy between Village wines and top Grands Crus, however, is an interesting one. Indeed, many Village wines have become disproportionately expensive compared to Grands Crus, as demonstrated by the Domaine Leflaive wines below.

Both the 2018 Bâtard-Montrachet Grand Cru and the Puligny-Montrachet saw their prices rise between September 2021 and September 2022, but the Village wine greatly outperformed its grand sibling and had not yet retreated as of the end of 2023.

Comparing the average trade prices of Burgundian wines to Bordeaux First Growths and Super Tuscans further emphasises the scale of the problem. The average traded price of a Super Tuscan is only 1.3x that of the average traded price of a Burgundy Village wine while the average traded price of a Bordeaux First Growth is only 3.15x higher.

For illustration purposes, for the price of one case of Domaine Armand Rousseau, Gevrey-Chambertin Premier Cru Clos Saint-Jacques 2018, one could secure six cases of Sassicaia 2018 or two cases of Château Lafite Rothschild 20181. Ten years ago, a single case of Rousseau Clos St Jacques 2005 would have bought you only 3.5 cases of Sassicaia 2005 or 10 bottles of Lafite Rothschild 2005.

Of course, Burgundy’s reputation and the rarity of its wines contribute to the high price tags they command, but it becomes increasingly harder to justify these prices during a market downturn.

Is there any value to be found in Burgundy?

Keen followers of our insights will recall us asking precisely the same question last year. In theory, falling prices in the region imply that it is easier to find pockets of opportunity, but these falling prices are partly the result of purse strings being tighter than they were this time last year. Indeed, demand may be on the wane.

Undoubtedly, there are some areas where prices are more attractive than others. The Grands Crus of Chablis, for example, still have the lowest average Market Prices of all; Clos des Lambrays, Clos de Vougeot and Corton-Charlemagne also sit comfortably below the average Market Price of Burgundy Grands Crus.

Burgundy trade overview

In 2022, Burgundy was the fastest-expanding region on the secondary market in terms of the number of wines traded. 2023 saw a further broadening of the market with over 2,000 LWIN7s traded, but value and volume traded were considerably down year-on-year.

It’s worth noting that this decline was not equal across classifications – Grand Cru trade volume was down 32.1% year-on-year versus just 15.4% for Village wines. Over the last seven years, Grand Cru trade volume increased by 33% and 23% for Village wines, but trade value reveals the extent of price rises in the region: Grand Cru trade value over the same period was up 124%, and 222% for Village wines.

Buyer geography

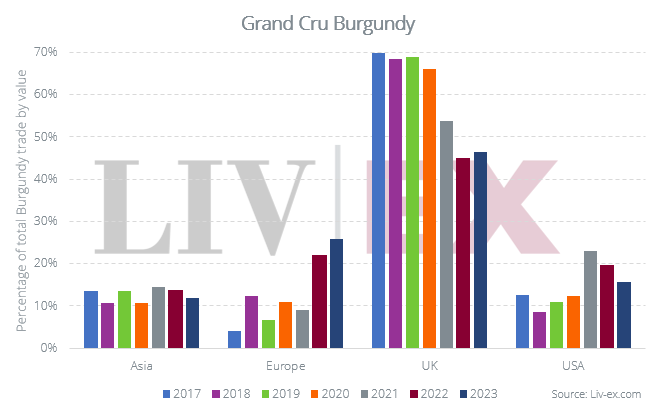

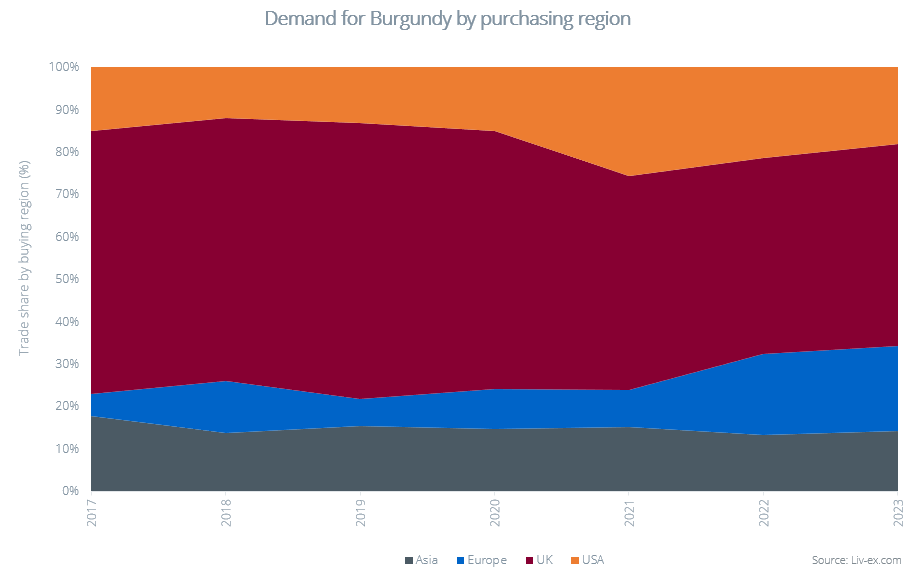

Breaking down Burgundy trade by geography and according to classification yields interesting results.

Asia’s share of Grand Cru trade, for example, has remained remarkably stable since 2017, while the UK’s dropped considerably in 2021 as Europe and the USA’s rose.

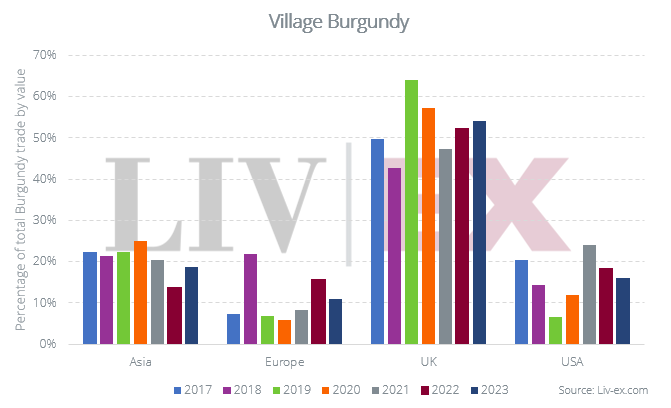

At Village level, however, the UK’s share of trade continued to increase in 2023, at the expense of Europe and the USA.

Asian buyers also rallied after a dip in 2022. Their share of Village wine trade is almost back to 2021 levels, pointing to sustained demand for Burgundian wines in the region, but perhaps a gradual move away from the top tiers.

The USA’s trade share was down across the board once again in 2023, despite US buyers no longer being throttled by EU tariffs imposed during the aircraft dispute and benefiting from their currency‘s relative strength (see above). One reason for this could be the rise in popularity of the US’s very own Pinot Noirs and Chardonnays.

Oregon still constitutes a very small proportion of trade on the secondary market but has nonetheless seen its share increase tenfold since 2018. Likewise, California is increasing its presence and accounted for 6.2% of total trade on the secondary market in 2023.

The trends above are mirrored in the chart below, which maps out demand for Burgundy by purchasing region. The UK and Europe’s shares have been gradually increasing at the expense of the USA’s, while Asia’s has remained remarkably flat over the last few years.

An evolving distribution system

At the distribution level, there is big change afoot in Burgundy, particularly at the Grand Cru level or among the ‘cult’ wines of the region.

Increasingly, companies such as Crurated are seeking to bypass négociants and merchants, taking some producers’ wines direct-to-consumer. In a market where it is famously hard to secure allocations and the wines are scarce, this might be an appealing option for a growing number of Burgundy buyers.

Proponents of this distribution system will say it allows new buyers to enter the primary market more easily, particularly younger generations, without relying on existing relationships with merchants to secure these coveted allocations, ultimately democratising access to Burgundian wines. However, the addition of blockchain technology by some, intended to safeguard the wine’s authenticity, can also be used to control secondary market trade. Not all collectors will be comfortable with this idea. For some, this will take away an incentive to buy; not everyone drinks every bottle of Burgundy they buy, especially at the current prices.

Critics will point out that by cutting merchants out of the equation the growers will lose valuable long-term partners who, along with their clients, have supported the Domaines through good times and bad. Much of what gives wines their value is the sharing of their history and following the grower through the vintages as he or she develops their story. Merchants are a critical part of this story, gathering dedicated followers among their collector bases.

One might argue too that simply selling wines to the highest bidder further removes these wines from the reach of most buyers, narrowing the pool of holders, reducing liquidity further still.

Navigating the Burgundy market has always been a tricky affair. Whether the introduction of new routes to market will complicate matters further is up for debate. Should these new routes reduce transparency and the freedom to trade, the market will lose its allure for many, reducing already limited liquidity. As any student of international markets will attest, prices will almost certainly suffer as a result.

Conclusion

At the turn of the year many feared that Burgundy 2022 was going to be a campaign too far.

A near 20-year bull run had come to an end. Yields were up while secondary market prices were continuing to come down. Burgundy’s bid-to-offer ratio is the lowest among major regions on the secondary market, a reflection of heightened risk aversion and a sign that the ongoing price correction has further to go.

It has not been a campaign without its challenges. There are reports of allocations turned down, old hands balking at the prices. Yet, these high-quality wines would seem to be the ‘hair of the dog’, the hangover cure many buyers needed to keep buying (and drinking) Burgundy, supported in no small way by the views of major critics.

But is this just a stay of execution? Burgundy 2023 is a big crop, whose quality is yet to be declared. It would seem prices can’t go up any further, so perhaps they must come down.

The outlook for 2024 is challenging: conflicts in Ukraine and Palestine, a weak Chinese economy and anemic growth in Europe, elevated interest rates and reduced government spending will do little to increase discretionary spending that is required to improve the mood in the fine wine market.

What always helps, however, are delicious wines released at sensible prices. Burgundy 2022 has walked a fine line. Next stop: Bordeaux 2023.