The Fine Wine Market in 2023

Introduction

Even PR experts would struggle to put a positive spin on the numbers above. 2023 has been a challenging year, not only for the fine wine market, but also for financial markets and consumers at large.

The IMF’s October projections predicted world economic growth slowing from 3.5% in 2022 to 3% this year, well below historical averages but maintaining a trajectory above recession levels.

Many economies are still reeling from the effects of the pandemic and the Russian invasion of Ukraine, which is widely credited for contributing to energy and food price rises. The conflict in Israel and Palestine is further adding to the feeling of insecurity in markets, which among other things has been driving investors back to safe investments like gold. While we haven’t yet seen a marked increase in oil prices (and thus, energy costs) as a result of the conflict, it is a possibility which could put further pressure on supply chains.

While inflation figures are coming down from the heights reached in 2022 and early 2023, core inflation (excluding energy and food) remains high across the board, the IMF predicting that most countries are not likely to return it to target until 2025. The last 12 months have seen a series of interest rates hikes by central banks attempting to keep inflation under control, which notably impacts mortgages and other lending sectors. Across major economies, interest rates are at their highest since the 2008 financial crisis.

In the UK, the Consumer Prices Index (CPI) was down to a 4.6% rise in the last 12 months to October 2023, compared to 6.7% in September and from its peak of 11.1% in October 2022. The 12 months to October 2023 marked the lowest levels of gas and electricity inflation since records began, as gas prices fell by 31.0% and electricity by 15.6%. That said, energy prices remain higher than two years ago, about 60% for gas and 40% for electricity. The rise in the cost of living driven by these price rises is widely affecting UK consumers, 62% of whom are reportedly spending less on non-essentials.

Over on the other side of the Atlantic, things are looking a bit rosier: the latest Federal Bank press conference highlighted strong economic activity, and the US’s third quarter GDP was estimated to have risen by 4.9%, boosted by consumer spending. The unemployment outlook has been revised to a lower figure in October, pointing to the likelihood of what the IMF is calling ‘a soft landing’ for the US, whereby inflation should keep coming down without a major economic downturn.

Overall, emerging and developing economies are reportedly remaining more resilient than their ‘advanced’ counterparts in the face of the above challenges. China is a notable exception to this; economists have lowered their forecasts for the country’s 2023 full-year economic growth to 5% year-on-year. The struggling real estate sector, which accounts for about 30% of China’s GDP, is cited as the biggest culprit for this, as evidenced by the Evergrande group filing for bankruptcy in August. That and a growing personal debt crisis have led Moody’s to downgrade its outlook on the country’s credit rating to negative on December 7th.

All this means consumers have less money than they did two years ago, everything (including borrowing) costs more, and most indicators point towards very slow recovery, the full impact of which is likely to be seen in 2024. The implication for the fine wine market is clear: buyers are not prepared to spend as much as they were last year, if they are prepared to spend at all. The ongoing market correction is a reflection of that.

The fine wine market in 2023

If there is anything we can repeat from last year’s fine wine market review, it’s that 2023 certainly put the market to the test.

2022 was a year of two halves, the first one of rapid growth and booming trade, the second marked by rising risk aversion and the start of a downturn in the fine wine market.

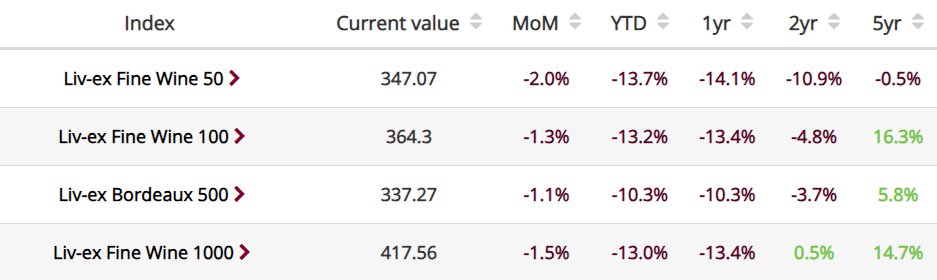

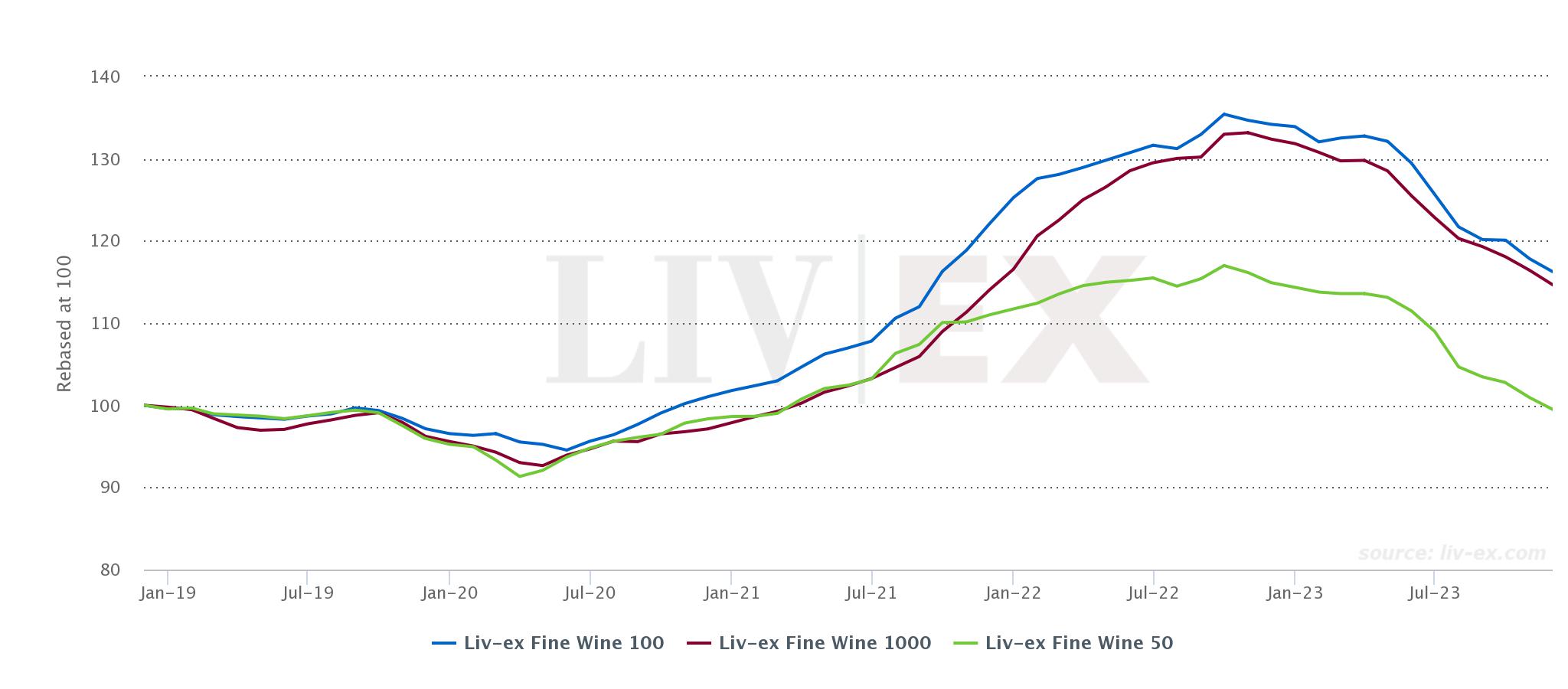

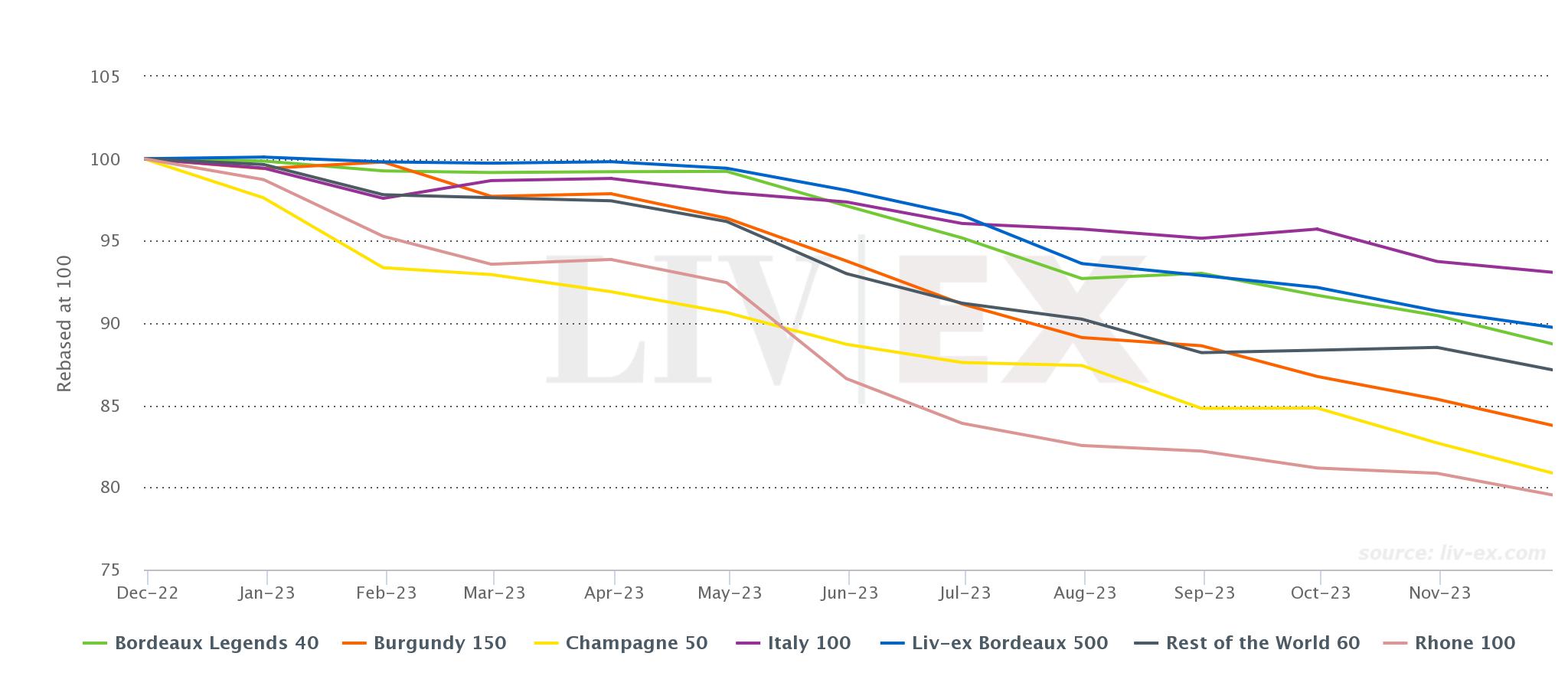

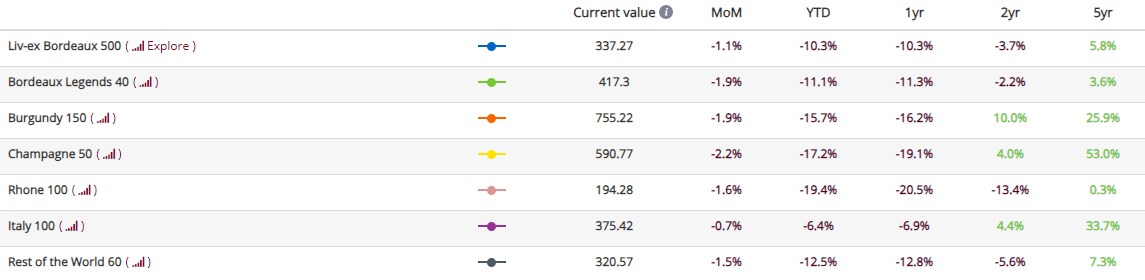

2023, on the other hand, was nothing if not consistent. Major Liv-ex indices (which turn 20 this month!) have retraced most of the growth they recorded in the previous two years; the Liv-ex Fine Wine 100, the industry benchmark, is down 13.4% year-to-date, and both the Fine Wine 50 (which tracks the movements of First Growths) and Fine Wine 1000 (the broadest measure of the market) are down 13.0% over the same period.

There was little letup in the downward movements of the indices in 2023, and the latest update didn’t give an indication that the bottom was in sight.

*Made using the Liv-ex Charting Tool.

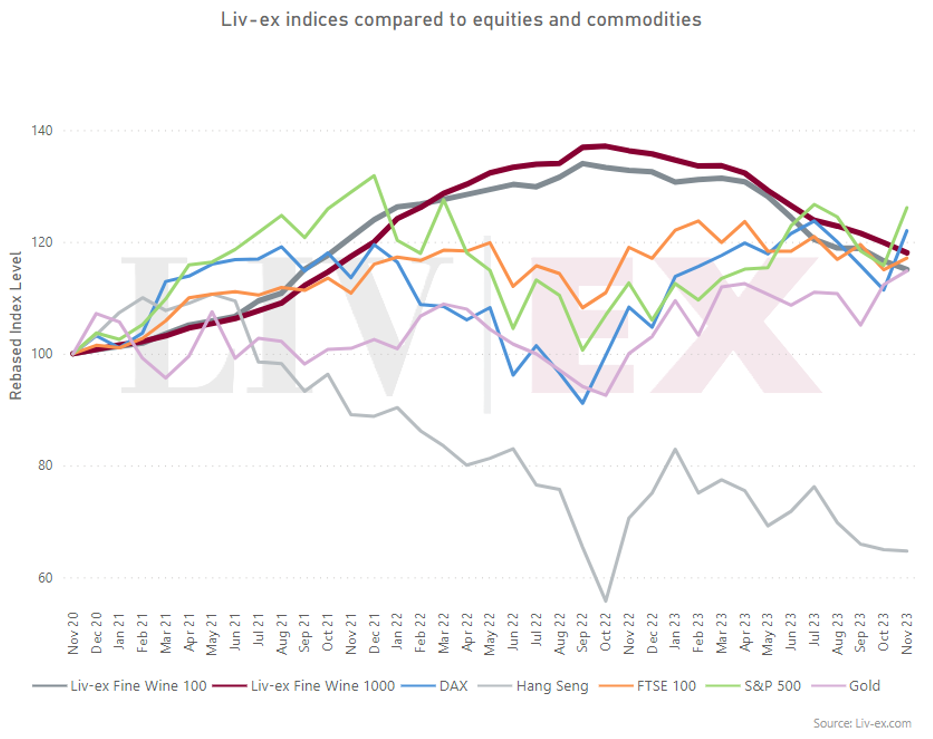

In 2022, the Liv-ex 100 and 1000 significantly outperformed other financial indices, including gold. Fine wine established itself as a powerful alternative asset in times of economic turmoil, a beacon of stability amid a volatile equities market.

One year on, this is no longer the case. The S&P 500 has made a comeback after a tough year in 2022, closing at a 20-month high on the 1st of December 2023. Gold also reached an all-time high a few days ago, most recently buoyed by concerns over conflicts in Ukraine and in Israel and Palestine. Optimism around lowering inflation rates and the potential for interest rates cuts in the UK renewed retail investors’ interest in the stock market, further boosting equities.

While fine wine indices are looking markedly less buoyant than their counterparts in other markets, it’s worth noting that for now, they remain at comparable levels.

The Hang Seng is a notable outlier, trailing way behind other international indicators including fine wine indices. Back in 2022, the index fell to a 13-year low as Chinese growth slowed and investors were sceptical of recovery plans proposed to stimulate the economy. After a brief period of recovery following the G20 summit in November 2022 and Covid lockdowns easing, the Hang Seng has been on a downward trajectory as foreign investors have dumped more than $25bn worth of shares. Moody’s credit rating downgrade is unlikely to be good news for the index.

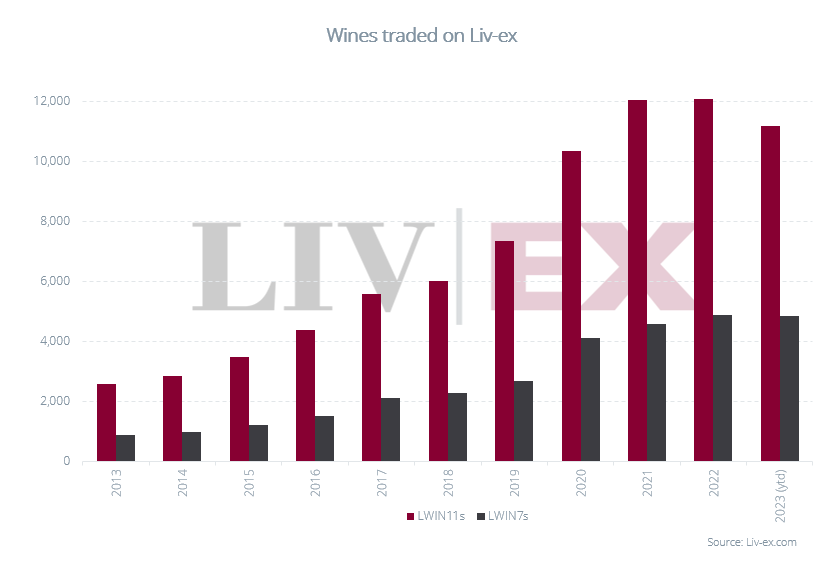

After ten record-breaking years for the number of wines traded on the exchange, 2023 is coming in just shy of 2022. The number of labels (LWIN7s) traded on the exchange is comparable year-on-year, but there is a notable gap in the number of individual wines (LWIN11s) traded.

An LWIN (Liv-ex Wine Identification Number) is 7-, 11-, 16 or 18-digit numbers, depending on the level of detail. The 7-digit code refers to the wine itself (i.e. the producer and brand, grape or vineyard). The longer codes include information about the vintage, bottle and pack size.

As we reported in the 2023 Power 100, all indicators are pointing towards a flight to quality whereby collectors are narrowing their focus to the most established brands in the market, the ones most likely to hold their value. The reduction in the number of individual wines trading on the exchange is a continuation of this trend, highlighting the fact that even inside brands, buyers are shifting their attention to the highest-quality vintages, particularly those now in their drinking windows.

Currency overview

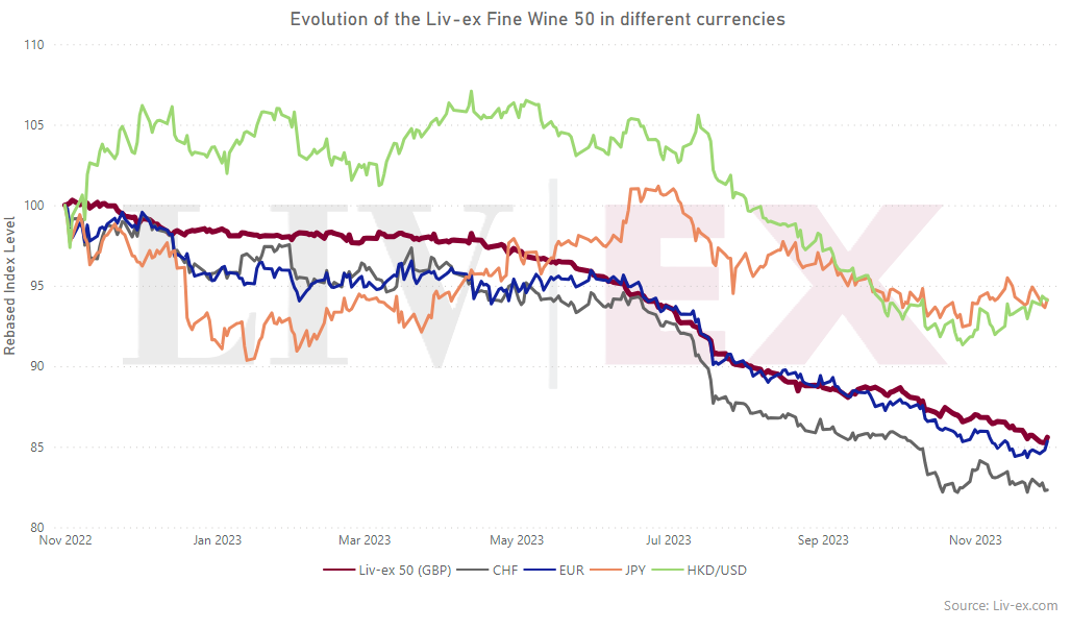

The Fine Wine 50 tracks the daily movement of First Growth prices. The graph above shows something we already know: right now, these wines are cheaper by the dozen than they were a year ago.

But when viewed in US dollar terms (and the linked HKD), the index is off only 5%, the Dollar having weakened 8% against Sterling since November 2022. This, as well as the relative strength of the US economy in 2023, explains why buyers in that region are more sanguine about the state of the fine wine market.

Regional breakdown of trade

Bordeaux bucks the trend

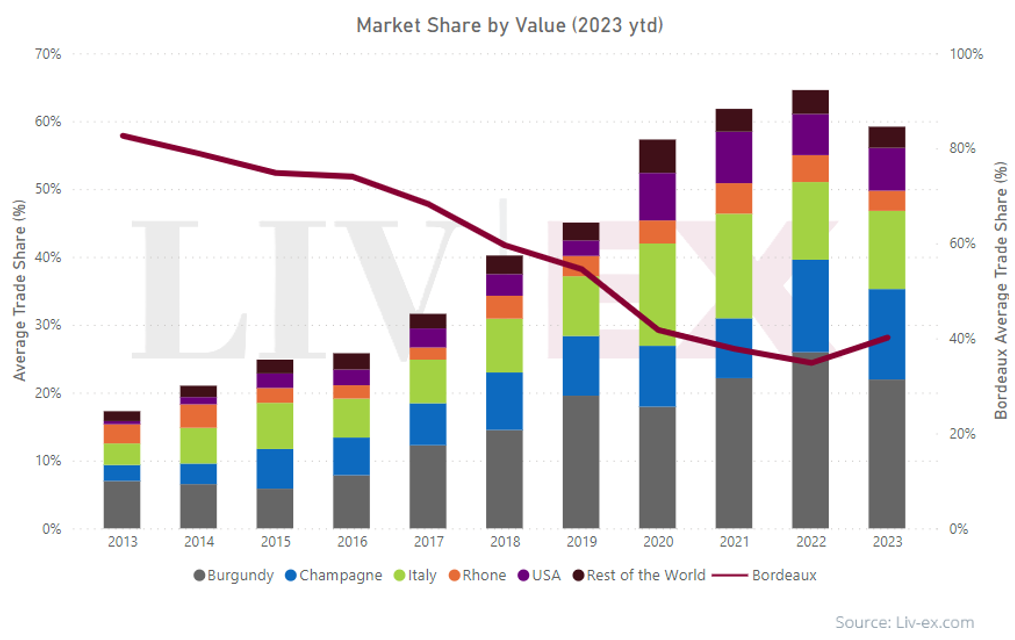

For the first time in ten years, Bordeaux’s share of regional trade by value is on the rise.

This comes despite a very lukewarm reception for the En Primeur 2022 campaign; the high release prices across the board at best did little to reinvigorate the market and at worst alienated some merchants who are left with large amounts of stock to shift, not least among the négociants in Bordeaux.

Bordeaux does have liquidity on its side in terms of trade value; in a downward market, there is a natural tendency for sellers to offload wines with a relatively high amount of stock to free up some cash (and warehouses ahead of the next vintage). Many young Bordeaux wines are thus trading not only below market, but also below their ex-London and ex-négociants prices.

But Bordeaux’s market share gains also lies in the fact that it is the safest, best-known market that many collectors default to in times of turmoil. The market’s flight to quality mentioned above naturally benefits Bordeaux, as buyers seek comfort in a region where they know what to expect, namely proven quality at a certain price.

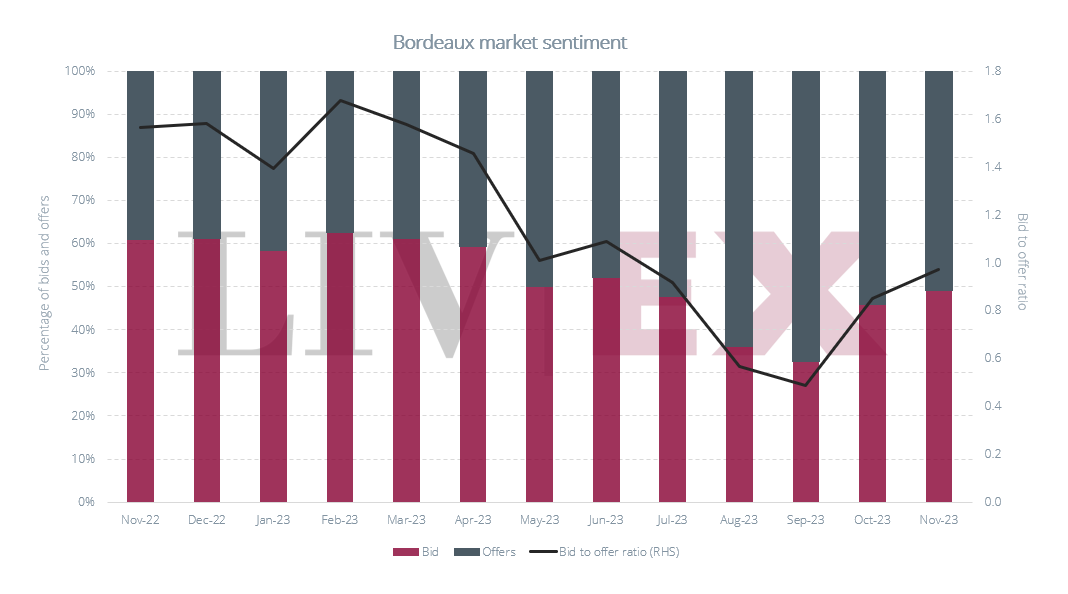

As seen in the chart below, Bordeaux’s bid-to-offer ratio (measured as the number of bids to every offer) is close to 1.0, meaning that for almost every offer there is a bid. This is considerably higher than other major regions traded on the exchange, which shows that no matter what’s going on in the rest of the market, there is demand for Bordeaux, at a price.

Bordeaux’s comeback comes at the expense of all other regions, which saw their trade shares decline fractionally. Burgundy was the only region to take a considerable hit, its share of regional trade dropping from 31.2% of the total last year to just 24.0% in 2023.

Burgundy was one of the regions collectors flocked to in summer 2022, which sent prices for the region’s wines soaring as a result. Now, as risk aversion strengthens its hold on the market, cautious collectors are no longer prepared to pay the same prices they paid for these wines last year.

This is especially true for a lot of newer, less-established brands which appealed to collectors in recent years as alternative entry-points into an expensive region. As we noted in the 2023 Power 100, some of these brands have taken a hit in terms of price performance and trade numbers following two years of unsustainable price rises.

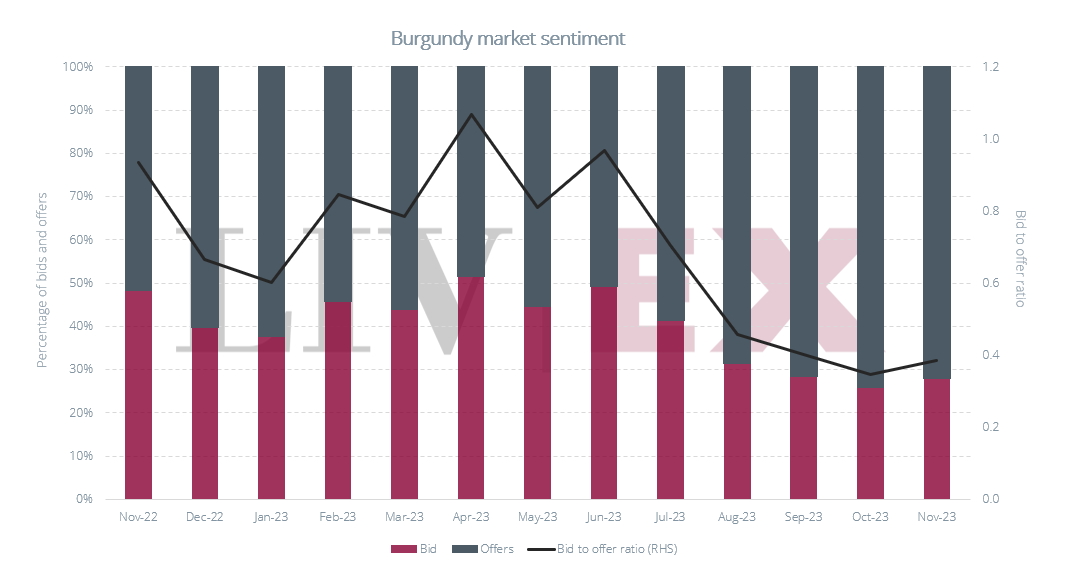

Burgundy’s market sentiment chart looks very different to Bordeaux’s – its bid-to-offer ratio is the lowest among the major regions on the exchange. Prices across the region’s wines have started to adjust, as shown by the Burgundy 150’s 15.7% retracement year-to-date, but on the whole, they are not yet at a level that buyers are willing to wholeheartedly engage with.

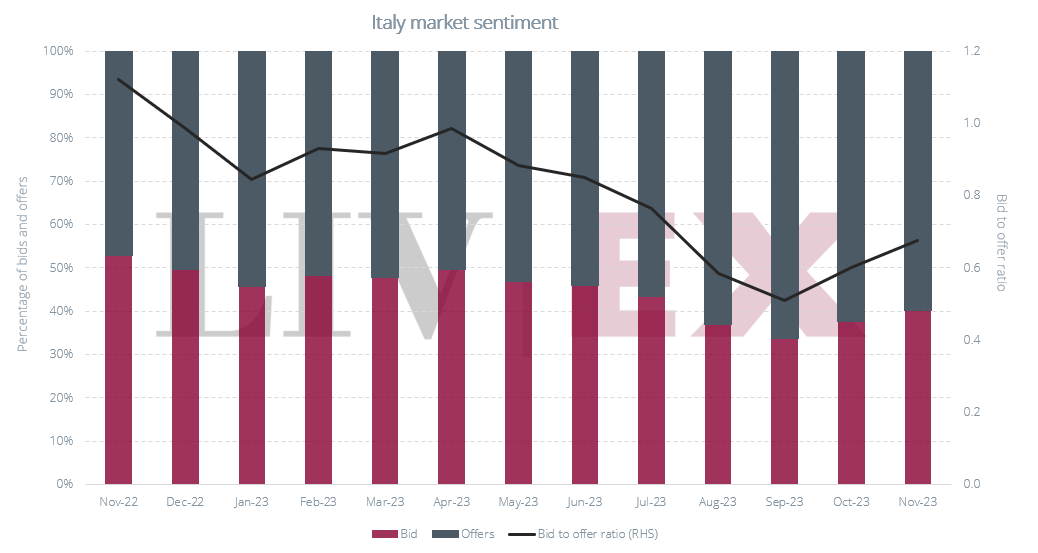

The face of resilience: the Italy 100

The Italy 100, which tracks the price performance of the ten most recent physical vintages of five ‘Super Tuscans’ and five other leading Italian producers, was the best performer among the sub-indices of the Liv-ex Fine Wine 1000 in 2023. The sub-index is the only one to have recorded a single-digit decline, falling 6.4% year-to-date compared to 10.3% for the Bordeaux 500, the next best performer. At the other end of the scale are the Rhône 100 (-19.4%) and the Champagne 50 (-17.2%).

Considering the current market conditions, Italy’s bid-to-offer ratio is healthier than Burgundy’s, for example. This more sustained demand is helping to keep prices of the region’s wines relatively steady.

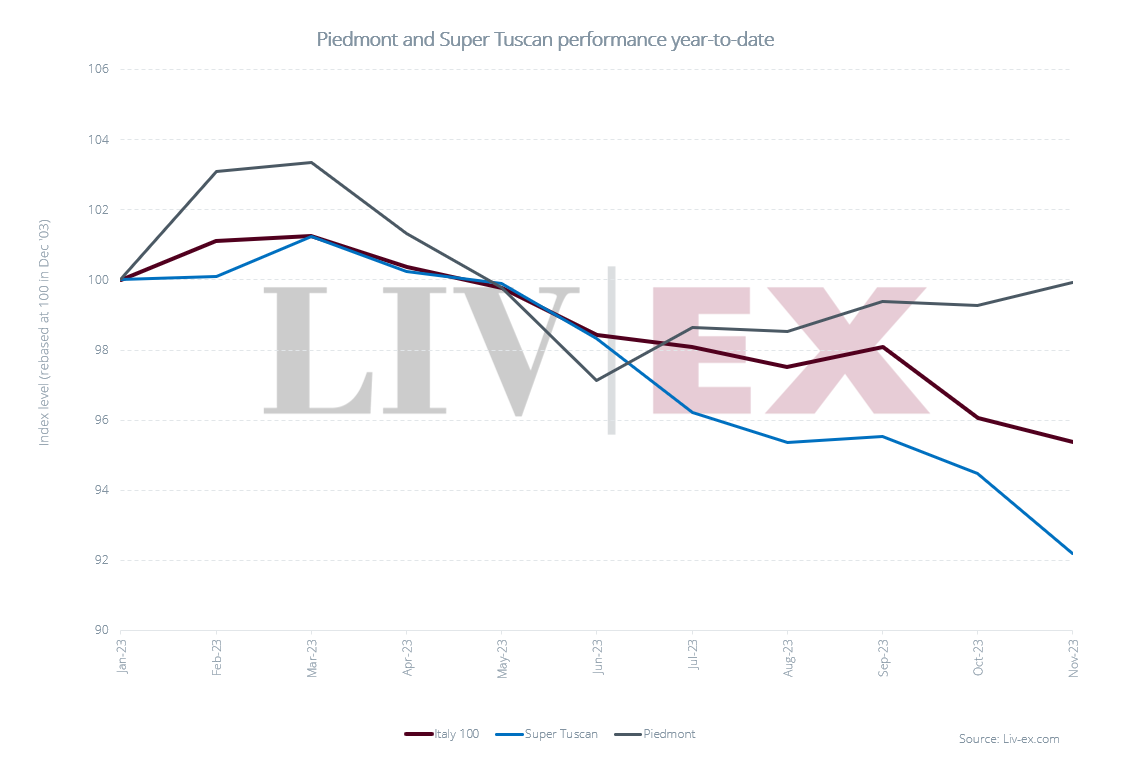

Dividing the index into its Tuscan and Piedmontese components shows considerably better resilience from the latter, which are counteracting the negative impact of Super Tuscan wines on the Italy 100.

Indeed, the best price performers inside the index year-to-date are Piedmont wines such as Giacomo Conterno, Barolo, Monfortino Riserva 2001 (+40.1%), Gaja, Barbaresco 2010 (+19.9% ytd), 2015 (+18.1% ytd), 2011 (+13.2% ytd), 2012 (+11.8% ytd) and 2019 (+9.4% ytd).

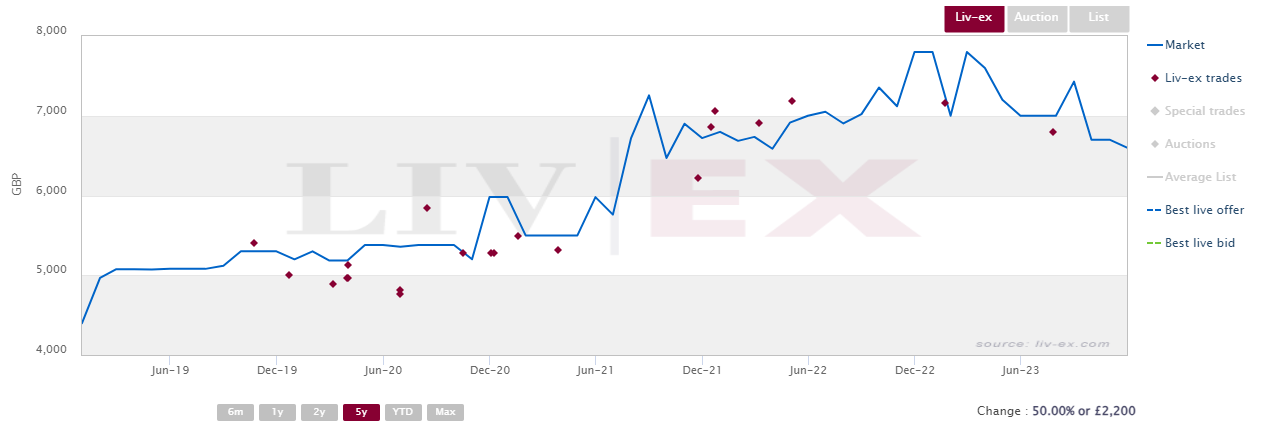

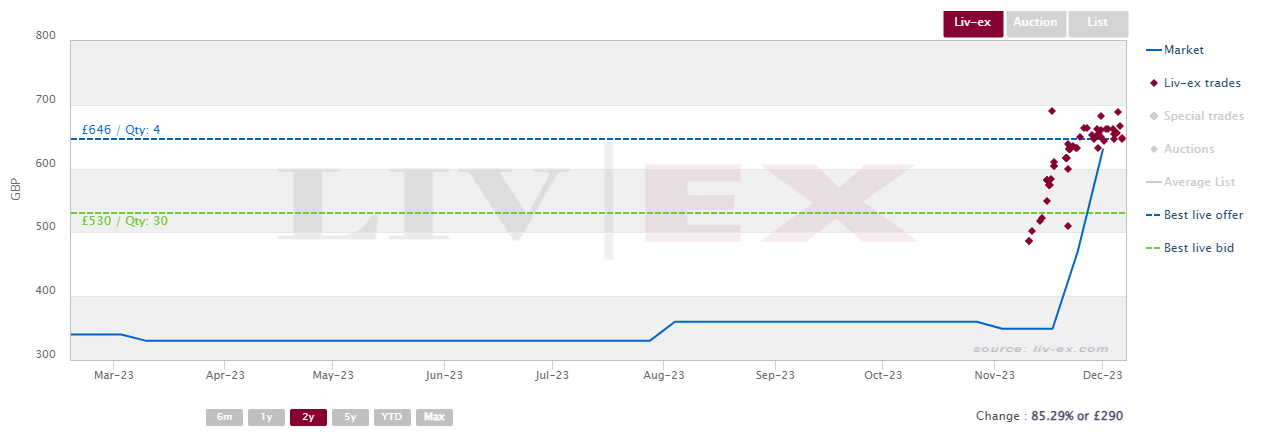

Among the worst performers in the index are several vintages of Masseto, a (relatively) small-production Super Tuscan wine that is hard to source on the primary Italian market. The 2013 vintage, for example, was rated 97 points by Antonio Galloni (Vinous) and Monica Larner (The Wine Advocate) and was released at £4,000 per case, which at the time made it one of the cheapest vintages on the market.

Its Market Price rose steadily from 2020 to early 2023, when it traded at £7,160 per case. Since then, however, its price has been correcting, suggesting for now, that its price has peaked.

Masseto 2013 trades on Liv-ex

The most-traded wines on Liv-ex

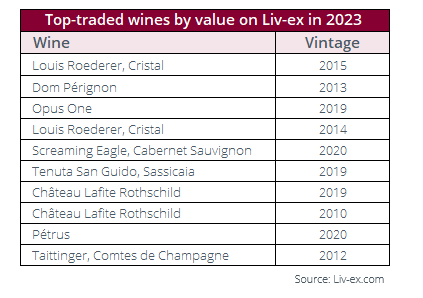

Until very recently, the most traded wine by both value and volume in 2023 was Dom Pérignon 2013, which was released in January at £1,830 per 12×75. In the last few days, another Champagne released in 2023 bumped it out of the most-traded spot by value: Louis Roederer, Cristal 2015. It has a Market Price of £2,068 per case to Dom Pérignon 2013’s £1,646.

Two Californian wines are represented in the top-traded wines by value: Opus One 2019 and Screaming Eagle 2020. Both appear in the rankings above Château Lafite Rothschild, as does Sassicaia 2019 – a reminder that the broadening of the fine wine market is a phenomenon that stretches all the way to the very top.

The two vintages of Château Lafite on the list, the 2010 and 2019, are both Wine Advocate 100-pointers,as is Pétrus 2020, reflecting the flight to quality we highlighted throughout the rest of this report.

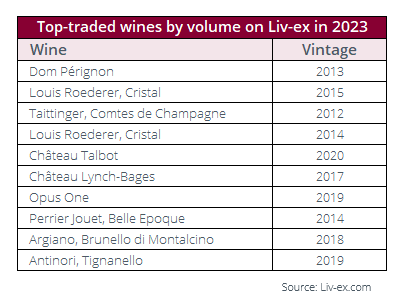

Unsurprisingly, in terms of volume, the most-traded wines in 2023 are dominated by Champagne. The region benefits from high liquidity and the fact that it appeals to drinkers as well as collectors, which means large quantities of Champagne get sold (and drunk) every year.

As well as Dom Pérignon 2013, Cristal 2015 and 2014 and Taittinger Comtes de Champagne 2012 which are all among the top-traded wines by value, Perrier Jouet Belle Epoque 2014 features on the volume rankings.

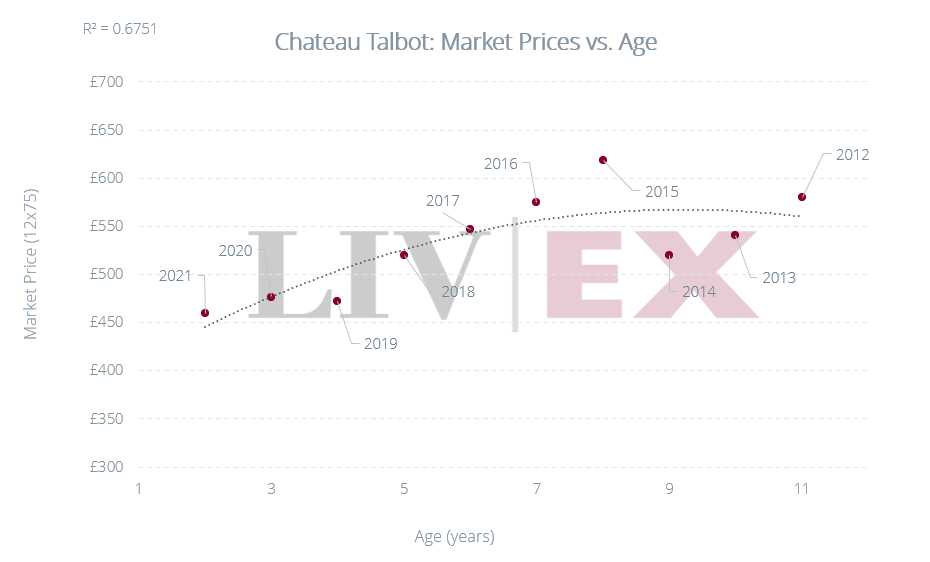

The rest of the list is comprised of relatively more affordable Bordeaux, such as Château Talbot 2020 which has a Market Price of £476 per case. According to Liv-ex’s Fair Value methodology, Chateau Talbot Market Prices are 61% correlated with age, meaning they tend to appreciate with the passing of time. The 2020 vintage falls on the fair value line (see chart below), meaning it is a good opportunity for buyers to secure a wine likely to appreciate with age.

Liv-ex members on Silver packages and above have access to similar analysis for many more wines through the Fair Value tool.

We’d be remiss if we didn’t mention (again!) that the Wine Spectator’s 2023 Wine of the Year, Argiano, Brunello di Montalcino 2018, features on the list of most traded wines on Liv-ex this year. Prior to the announcement, the wine had never traded on the exchange, but it has since sustained high levels of activity on Liv-ex as collectors seek to secure the wine.

Argiano, Brunello di Montalcino 2018 trades on Liv-ex

Conclusion and 2024 outlook

Something’s gotta give

In upward-trending markets, there is room for exploration and experimentation. In the fine wine market, this translated to a broadening of the secondary market, which extended both to previously overlooked regions and to lesser-known producers among already popular ones.

The current downturn has come with a shift to safe havens in the market, older Bordeaux vintages being an example. Even inside specific regions, this flight to quality is discernible as collectors focus on established brands and the highest-quality vintages.

Some brands that collectors speculated on during the boom of 2021/2022 which saw their prices rise at rapid rates have suffered the same fate as some crypto currencies did a year ago. The likes of Domaine Arnoux-Lachaux, Salon and Château Lafite are trading well below the level they were trading at last summer, if they are trading at all.

Purse strings are a lot tighter than they were in 2022, and cash-strapped sellers are left with plenty of stock acquired at high prices that buyers are no longer willing to front. For the trade, 2024 looks bleaker than 2023, which was redeemed by a strong first quarter. Many collectors have become net sellers as a consequence of the rising costs of holding and storing wine and a sense that growers are demanding too much for their new releases, further adding to the pool of wine to be shifted.

The prospect of incoming high-yielding (and high quality) vintages from Burgundy, Tuscany, California, Bordeaux and Champagne is daunting – is there a place for large volumes of expensive wines in the current market? In 2024, the role of campaigns such as Burgundy and Bordeaux En Primeur will be more crucial than ever – as will the pricing of the wines released, if distributors hope to sell them.

We’ve reached the usual impasse typical of bear markets – buyers won’t buy wines at their current market price sellers are reticent of lowering their prices and taking on losses. Meanwhile, stock is accumulating in warehouses and cellars, and there is more on the way. Until the macroeconomic context improves and interest rates come down, a compromise must be reached between the two sides of the market; the ongoing price correction has thus far not been enough to coax buyers back in large numbers. Prices look set to remain under pressure in the short term.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently over £100m of bids and offers across 20,000 wines.