The fine wine market in Q3 2023

Introduction

As we approach the end of the year, made obvious by the early appearance of Christmas decorations in shops, it’s a fitting time to reflect on the state of the fine wine market during the third quarter of 2023.

Across the globe, countries have continued to grapple with a series of economic challenges.

In the United States, the all too common dispute between Republicans and Democrats over government spending once again raised the spectre of a government shutdown, marking the fourth such threat in a decade. However, as Q4 began, a bill was successfully signed to avert this.

Similarly, developed economies worldwide are contending with the impact of monetary tightening. Europe, for instance, stands on the precipice of recession brought on by declining bank lending and money supply, along with contracting manufacturing indicators. The European Central Bank has hinted it may be done with interest rate hikes, but it intends to leave them high for the foreseeable future. Europe is also feeling the repercussions of China’s economic downturn, reflected in weakening export demand.

In the United Kingdom, economic growth has been sluggish. While it has managed to avoid a technical recession thus far, despite a 15-year high in interest rates set by the Bank of England at 5.25%, low productivity, rising unemployment and falling house prices, which have seen some of the sharpest declines since 2009, dominate the financial newswires. However, it is not all doom and gloom, as the UK economy showed a stronger recovery from the pandemic than previously estimated.

Meanwhile, China faces the challenge of escalating debt and a slumping property market. Officials are pinning their hopes on China’s ‘Golden Week’ to provide a much-needed boost to the economy.

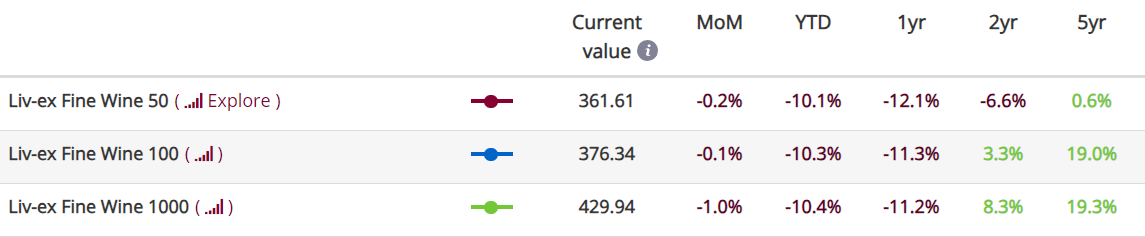

Shifting our focus to the fine wine market, the last quarter was characterised by downward movements in all the major Liv-ex indices, leaving buyers and sellers wondering where the bottom might lie. However, September saw increased market volatility with contradicting trends recorded across indices, suggesting the market may be looking for a turning point.

In September, the Liv-ex Fine Wine 100 (the industry leading benchmark which tracks the 100 most-traded fine wines on the secondary market) experienced a slower decline compared to the previous month, hinting at a potential stabilisation. Conversely, the Liv-ex Fine Wine 1000 (our broadest measure of the market, which tracks 1,000 wines from across the world) recorded a faster decline than the month before, suggesting turbulence at the global level. Meanwhile, the Bordeaux 500 (the most comprehensive index for Bordeaux wines) mirrored the decline recorded in the previous month.

Finally, La Place de Bordeaux’s Autumn Releases came and went with mixed results. Many merchants expressed dissatisfaction with the high volume of releases of relatively unknown wines at unrealistic prices.

Given the current volatility and the fact that no clear bottom is in sight, the fourth quarter will reveal which direction the market heads in.

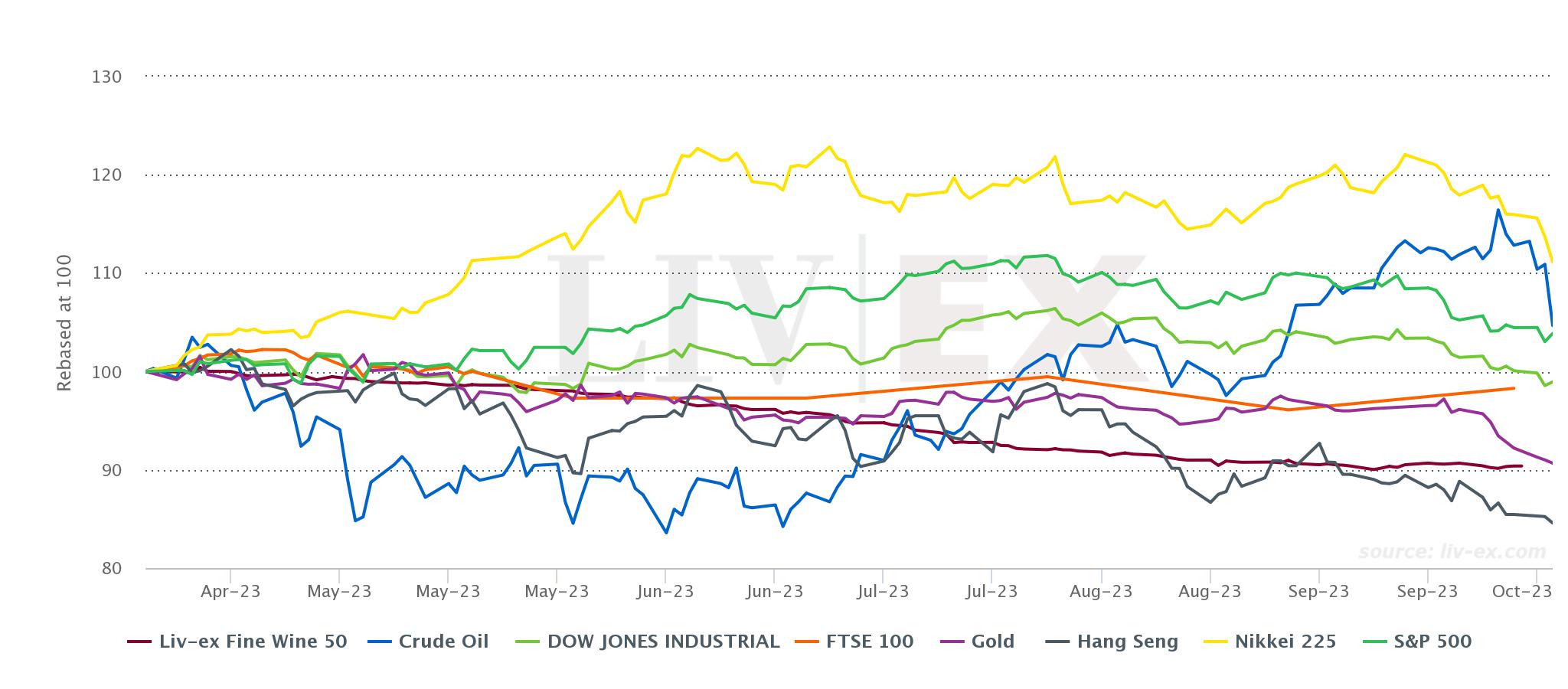

Fine Wine 50 vs equities

*made using the Liv-ex Charting Tool. Data taken on 05.10.2023.

In contrast to the fine wine market, the S&P 500 and the Dow Jones Industrial have recorded positive performances over the past year, increasing by 17.7% and 16.7% year-on-year respectively. The fine wine market (represented by the Liv-ex Fine Wine 50) experienced a decline of 12.1% in the same period. In the first quarter of 2023, the decline recorded in the index was only 0.9%, meaning the sell-off only took hold during the second and third quarter.

Among other financial indices, only one has performed worse than the Liv-ex Fine Wine 50 year-to-date: the Hang Seng, which has declined by 13.1%. The index entered bear-market territory in August after it dropped almost 21% from its high point reached in late January this year. This index has continued to slide after a bearish flag breakdown in early September, encountering resistance from a concurrent downtrend. The deterioration in its performance can be attributed to growing pessimism among investors regarding China’s post-pandemic recovery and concerns over the country’s debt levels and slumping property market.

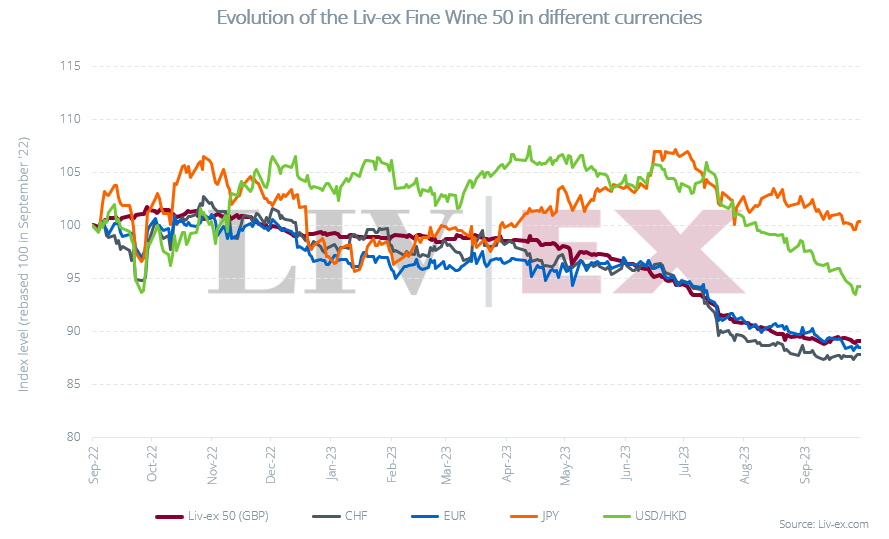

Currency overview

In the third quarter of 2023, the US Dollar displayed a strong performance, outperforming major currencies like the British Pound (GBP), Japanese Yen (JPY), and Australian Dollar (AUD).

As shown in the chart below of the Fine Wine 50 in Sterling and alternative currencies, buyers using US Dollars have benefited from being able to purchase wines in the Liv-ex 50 at more favourable prices compared to those trading in British Pounds. This is reflected in the fact that in Q3, there was an equal proportion of buyers from the USA and the UK on Liv-ex, accounting for 32.3% each. This represents a significant increase in US buying compared to the first two quarters of 2023.

The Euro recorded a mixed performance during Q3. It initially saw a moderate depreciation against the US Dollar after a brief uptick in early July but managed to gain some ground against the Japanese Yen and British Pound in foreign exchange markets.

The Liv-ex Fine Wine 50 in Euros (EUR) and Swiss Francs (CHF) maintained stability throughout the quarter. This stability was advantageous for buyers using these currencies, providing a more predictable environment for their purchasing decisions.

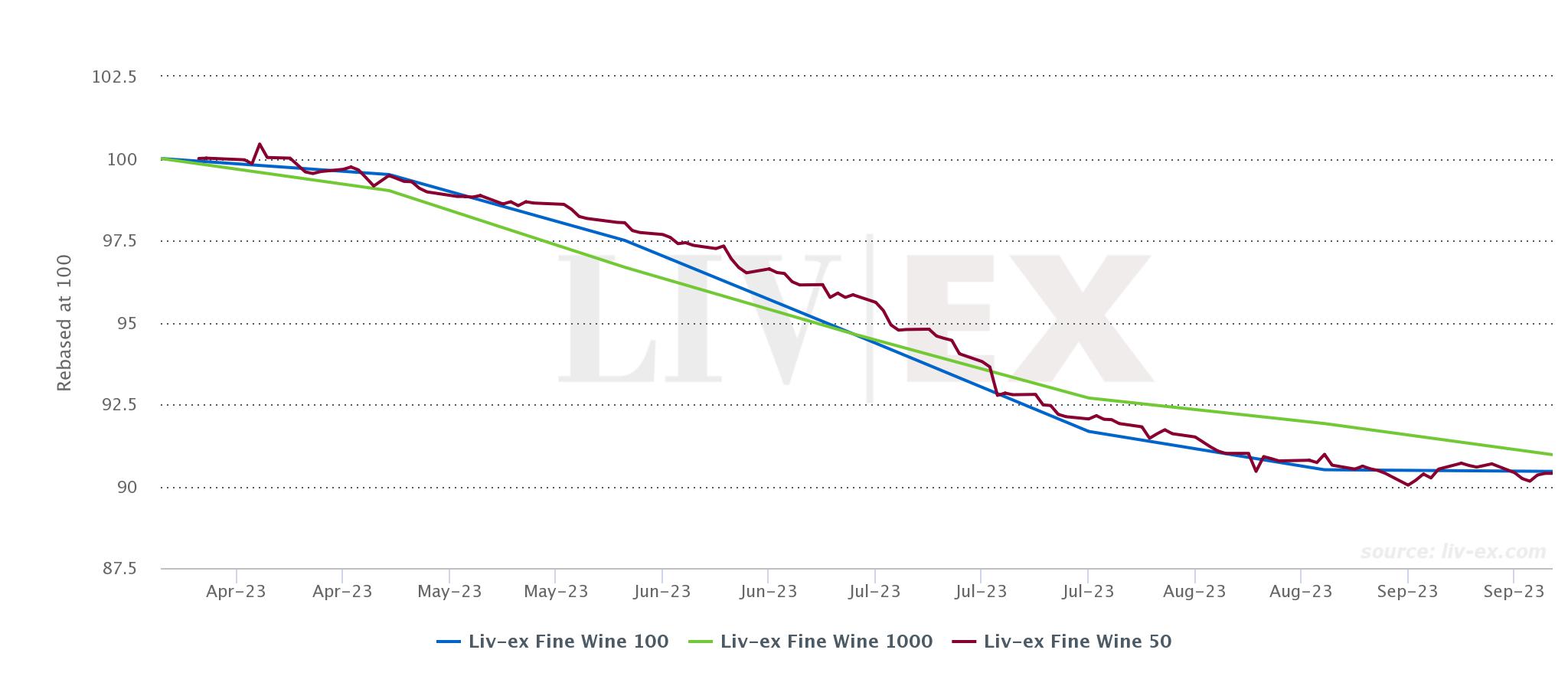

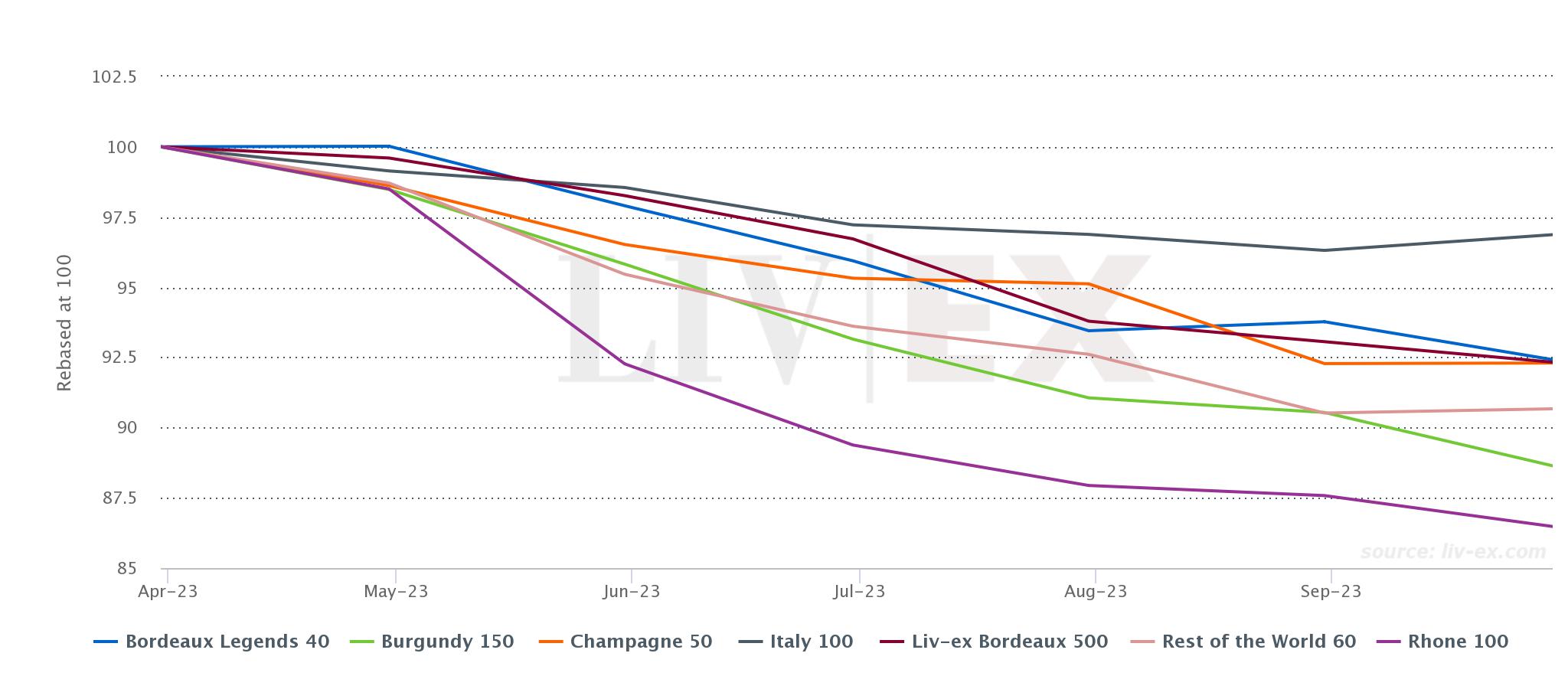

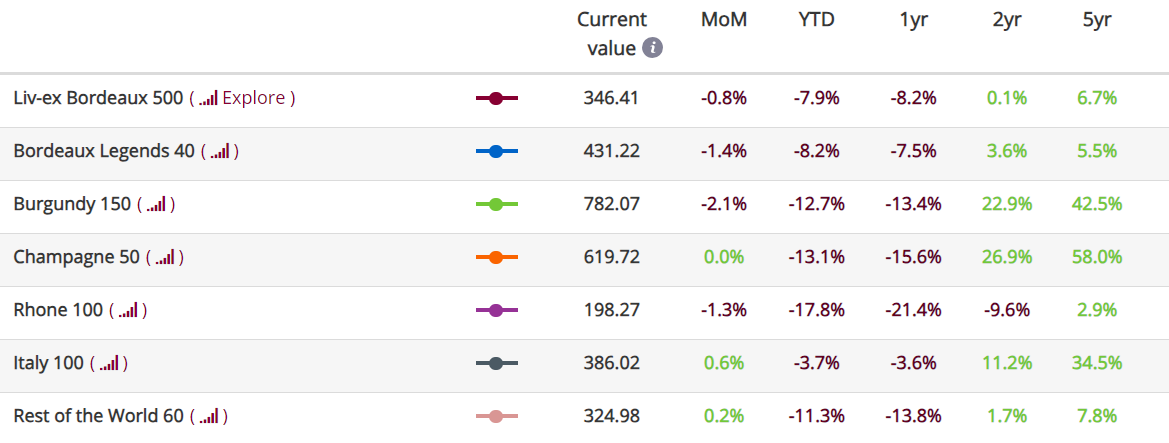

Liv-ex 1000 sub-indices

*made using the Liv-ex Charting Tool. Data taken on the 5th of October 2023.

As previously mentioned, the fine wine market is currently experiencing increased volatility. While all major indices fell over the quarter, there was a deceleration in the rate of their decline since the start of the year. In September, we observed divergent trends: while the Liv-ex 50 and Liv-ex 100 exhibited milder declines compared to the previous month, the Liv-ex 1000 experienced a more pronounced drop.

Year-to-date, all indices have decreased by more than 10%. The Liv-ex 100, the Liv-ex Fine Wine 50 and the Liv-ex Fine Wine 1000 have declined by 10.3%, 10.1% and 10.4% respectively since the start of the year.

Looking at the Liv-ex 1000’s sub-indices, the chart below shows a clear downward trend year-to-date. However, in August, there was a notable change: the Bordeaux Legends 40 index recorded an increase. In September, we saw even more positive movements: the Italy 100 and the Rest of the World 60 rose by 0.6% and 0.2% month-on-month respectively and the Champagne 50 ran flat.

Over the past 12 months, the Rhône 100 stands out as the weakest performer of the Liv-ex 1000, with a 21.4% decline primarily attributed to the underperformance of wines from Château Rayas. The Italy 100 was the best performer with a 3.7% decline over the same period, displaying remarkable resilience in the downward market.

*made using the Liv-ex Charting Tool. Data taken on 05.10.2023.

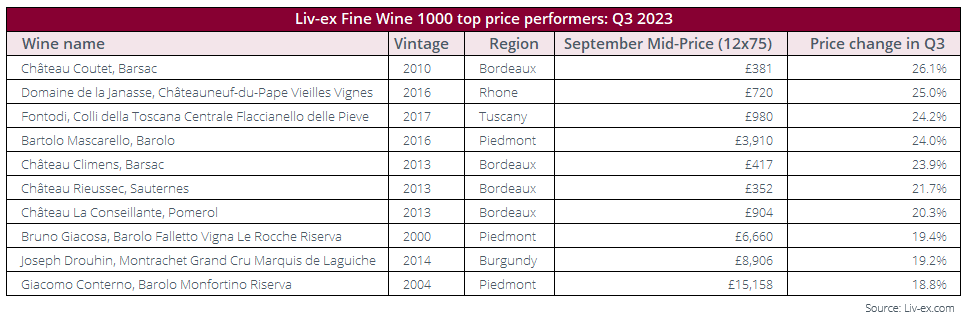

Top price performers in the Liv-ex Fine Wine 1000

In the second quarter, Barsac wines dominated the top price performers list, with six of the top ten coming from Château Climens. However, in Q3, the top price performers in the Liv-ex 1000 showed more diversity, with only three of the top ten wines still originating from Sauternes or Barsac.

Notably, Bordeaux 2013 wines showed some of the highest increases, with Château Climens 2013 (+23.9%), Château Rieussec 2013 (+21.7%) and Château La Conseillante 2013 (+20.3%) featuring on the list of top price performers. Despite the Rhône 100 being the worst performing index year-to-date, Domaine de la Janasse, Châteauneuf-du-Pape Vieilles Vignes 2016 ranks second on the list of best performers, albeit after a somewhat volatile year for the wine.

Italy was also well represented in the list, which is to be expected considering the Italy 100 is the best-performing sub-index of the Liv-ex 1000 year-to-date. Three wines from Piedmont and one from Tuscany featured among the top price performers, among them Fontodi Colli della Toscana Centrale Flaccianello delle Pieve 2017, which rose by 24.2% over the quarter.

The prices shown in the table above are Liv-ex Mid-Prices. The Mid-Price is the mid-point between the highest live bid and lowest live offer on the market. These are the firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 620+ of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable. Prices given are for 12x75cl trades, or 6x75cl converted to a 12x75cl price.

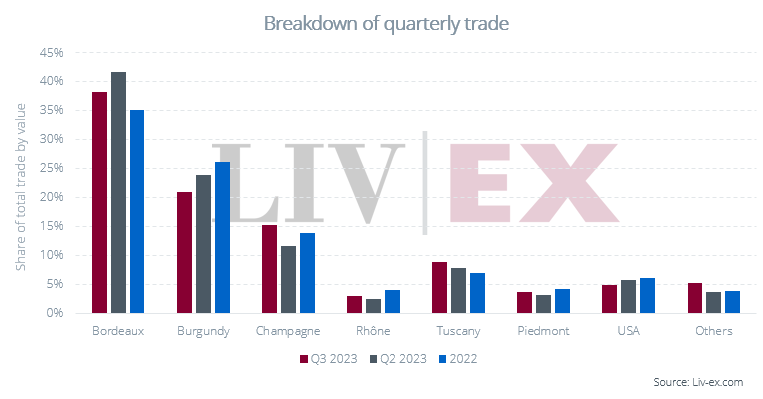

Trading overview in Q3

In the third quarter, Bordeaux retained its leading share of the fine wine market, although this decreased slightly to 38.3%, down from 41.6% in Q2. This could partly be attributed to an expensive En Primeur campaign in Q2, that left many Bordeaux buyers bewildered. Despite this dip, its Q3 share exceeds its 2022 average of 35.1%.

Demand for Bordeaux wines continues to be fuelled by European and American buyers, with the percentage of US buyers exceeding that of European buyers in Q3, potentially due to the relatively strong dollar. In contrast, European Bordeaux buyers exceeded US buyers in both Q1 and Q2 this year.

Burgundy and the USA also experienced declines in their regional trade share over the quarter.

On the other hand, all other regions including Champagne (15.2%), the Rhône (3.0%), Tuscany (8.8%), Piedmont (3.6%) and the ‘Others’ category saw their trade shares increase this quarter.

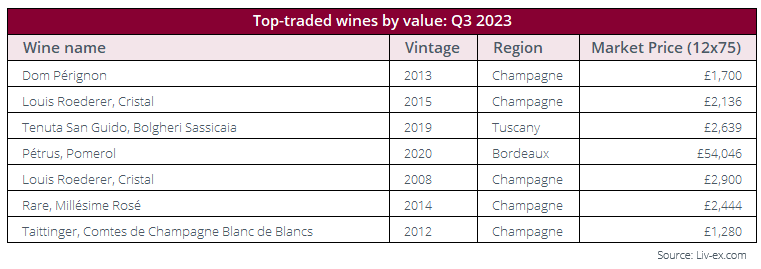

Top-traded wines in Q3 2023

Champagne enjoyed popularity during the third quarter, which can partly be attributed to the region’s lower Market Prices as the Champagne 50 has fallen 16% from its peak in October 2022. This decline was a blessing for some, who seized the opportunity to acquire wines at sharp prices. It’s worth noting that the region generally enjoys relatively high volumes of trade throughout the year, with peaks around summer and Christmas when many people drink it. As such, it frequently features in lists of top-traded wines, both by value and volume.

Indeed, Dom Pérignon 2013 maintained its position as the top-traded wine both in terms of volume and value throughout Q3 and year-to-date. Its Market Price, which currently sits at £1,700 per case, has dipped from £1,830 per 12×75 since the end of May. It traded at £1600 at the end of the quarter.

Activity in the region extended beyond Dom Pérignon, with four other Champagnes sitting among the top seven most traded wines by value last quarter.

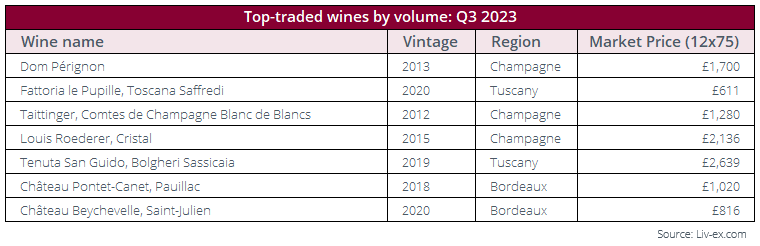

In terms of volume, Champagne again dominated the rankings, with Louis Roederer Cristal 2015 and Taittinger Comtes de Champagne Blanc de Blancs 2012 featuring on the list. Bordeaux secured two spots with wines from recent vintages (2018 and 2020), reflecting the tendency for sellers to shift more recent stock, of which they typically hold higher volume, to generate cash in a tight market. Wines from Tuscany have also made their mark in the top-traded wines by volume.

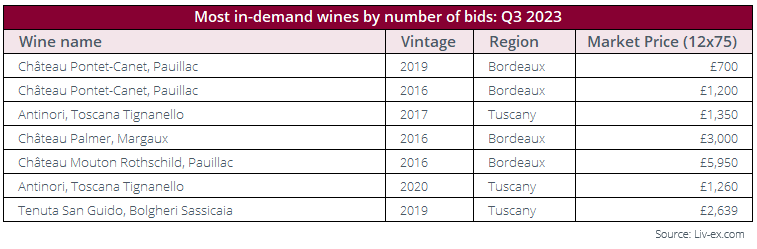

However, when we look at the most sought-after wines based on the number of bids they received during the quarter, Bordeaux truly came into the spotlight with wines from renowned brands and exceptional vintages such as 2016 and 2019. Once again, Tuscany emerged as the other popular region in Q3, benefiting from significant buyer interest for Super Tuscan wines.

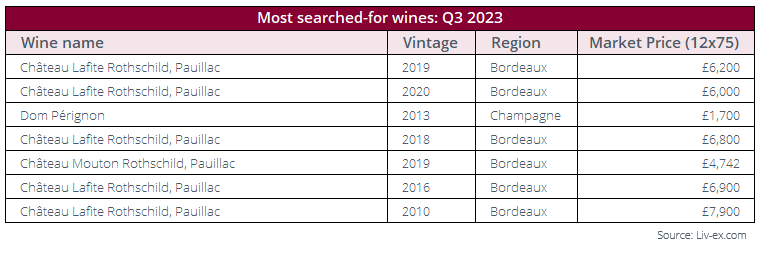

The market shifts further in Bordeaux’s favour when we look at the most searched-for wine, as the region accounted for six of the top seven most searched-for wines (five of them Château Lafite Rothschild). But does this point to demand?

The prices shown in the tables above are Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. It is always presented for a 12×75 case unless otherwise stated. To calculate the Market Price, we look at list prices from a large group of trusted international merchants. Preference is given to prices from stockholders over brokers, to cases over single bottles, and to recent prices over older prices. The algorithm behind it runs every day, evaluating a pool of over 1 billion data points to determine the most accurate Market Prices for 240,000+ wines.

Conclusion

As we look back at the events and trends that shaped the third quarter of the year, it’s evident that the global economic landscape has continued to be marked by challenges. Political disputes in the United States, monetary tightening in Europe, and economic strain in the United Kingdom and China have all contributed to fostering the environment of uncertainty that has shaped 2023 so far.

Within the fine wine market, Liv-ex indices continued to experience declines throughout the quarter. September introduced a period of volatility marked by some contradictory signals, with the Liv-ex 100 showing signs of potential stabilisation, while the Liv-ex 1000 faced increased turbulence.

Currency fluctuations played a significant role in fine wine transactions during Q3, with the US Dollar performing strongly against major currencies, influencing purchasing decisions for wine buyers using different currencies. Compared to the first two quarters of the year, US buyers were particularly active in Q3, accounting for 32.3% of trade, coming in just behind UK buyers which accounted for 32.4%.

Bordeaux maintained its prominence in the fine wine market, but its share of total trade by value slightly decreased this quarter, possibly off the back of a challenging En Primeur campaign. Champagne gained popularity due to lower market prices, with Dom Pérignon 2013 remaining a top-traded wine.

Overall, the fine wine market in Q3 2023 has been characterised by a mix of challenges and opportunities. Despite the downward trend in most indices, there have been pockets of strength, which alongside shifting dynamics in trade reflect the resilience and adaptability of the market. As we move forward into the final quarter of the year, it will be interesting to see how these trends continue to evolve and shape the secondary market.

About the Liv-ex indices

Our indices track the prices of the most traded fine wines on the world’s most active and liquid marketplace; Liv-ex.

They are calculated using our Mid Price; the mid-point between the highest live bid and lowest live offer on the market. These are firm commitments to buy and sell at that price; transactional data rather than list prices. It represents the actual trading activity of 620+ of the world’s leading fine wine merchants. Because Liv-ex does not itself trade, this data is truly independent and reliable.

Stretching back over 20 years, the Liv-ex 100 is quoted on Bloomberg and Reuters screens.

About Liv-ex

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 20,000 wines. Independent data, direct from the market.