Liv-ex October Market Report

- Fine wine continued to out-perform equities in September.

- The leading indices rallied after an August lull, in part due to the on-going weakness of Sterling.

- Bordeaux’s share of trade rose again led by demand for ‘on’ vintages both young and old.

- The autumn releases from La Place de Bordeaux struggled to make an impression.

- Neal Martin gave fresh scores for Bordeaux 1982 as he reviewed the ‘2’ vintages

- We examine the market for Rosé Champagne, a growing niche in the fastest growing category of the secondary market.

| Index | Level (31/09) | MOM (%) | YTD (%) | 1y (%) | 5y (%) |

|---|---|---|---|---|---|

| Liv-ex Fine Wine 50 | 411 | 1.5% | 4.5% | 6.3% | 17.7% |

| Liv-ex Fine Wine 100 | 424 | 1.9% | 8.1% | 16.4% | 37.8% |

| Liv-ex Bordeaux 500 | 377 | 1.6% | 6.5% | 9.0% | 21.9% |

| Liv-ex Fine Wine 1000 | 484 | 2.1% | 14.1% | 22.0% | 50.8% |

| Liv-ex Fine Wine Investables | 415 | 1.5% | 6.8% | 10.0% | 23.5% |

| FTSE 100 | 7,041 | -3.1% | -4.6% | -2.0% | -6.6% |

| S&P 500 | 3,774 | -5.3% | -21.0% | -15.4% | 44.7% |

| Gold | 1,713 | -0.6% | -5.9% | -4.9% | 30.4% |

Fine wine indices rise in September

After a quiet August, the benchmark fine wine indices all made gains in September. The Liv-ex Fine Wine 100 rose 1.9%, the Fine Wine 50 1.5% and the Fine Wine 1000 2.1%.

The Liv-ex 1000 saw biggest increase thanks to the positive performance of all seven of its sub-indices. The Champagne 50 was the best-performer for the fourth month in a row rising 3.2%, while the Bordeaux Legends 40 had its strongest month of the year – up 3.1%.

As in August, Sterling weakness was key to the market’s on-going success. As the Liv-ex indices are measured in Sterling, any weakness in that currency boosts the buying power of those using the Euro or US Dollar making fine wine prices look more affordable.

On the 27th September Sterling crashed to a historic low of US$1.07 in the wake of a ‘mini-budget’ announced by UK Chancellor, Kwasi Kwarteng. This caused an immediate surge in buying by US-dollar based merchants. Although Sterling has since recovered from this run it remains highly depressed against the Dollar.

Fine wine continues to hold up well versus traditional equities which have looked increasingly bearish of late following a brief rally in the summer.

Chart of the Month

Bordeaux’s trade share climbs over 40%

Bordeaux’s trade share increased last month from 32.2% of the total in August to 40.5% in September. A growing trend has been rising demand for ‘on’ vintages, with the 2019, 2018, 2009 and 2010 leading trade last month. Pétrus, Château Lafite Rothschild and Château Lynch-Bages were the most active labels from the region.

Champagne, Tuscany, Piedmont and the USA also saw heightened demand compared to August. The Super Tuscans (Sassicaia, Masseto, Ornellaia, Tignanello and Solaia) accounted for 75.6% of all Tuscan trade last month.

From the USA, Screaming Eagle and Promontory were at the forefront of activity. The ‘others’ category was dominated by Australia (0.7%), followed by Chile, Germany and Spain, which accounted for 0.4% each. Wines from Lebanon, Hungary and Switzerland also carved a small niche in September’s market activity.

Major Market Movers

Bordeaux’s best-performers

Compared with Burgundy and Champagne, the Bordeaux indices continue to rise at a much slower pace. The Bordeaux 500 is up 6.5% year-to-date, with only one sub-index – the Right Bank 50 – up by double digits (10.1%).

Nonetheless, as mentioned in the previous section, a growing trend has been demand for top vintages, with activity highest for the 2009, 2010, 2015, 2016, 2018 and 2019.

As the table above shows, the five best-performing Bordeaux wines in the Liv-ex Fine Wine 100 last month were all from one of these vintages.

Among them was Figeac. It received its anticipated promotion to Premier Grand Cru Classé ‘A’ in the St-Emilion classification last month. The news caused a number of vintages to hit new trading highs. The 2015 has two 100-point scores to its name as well, one from Jane Anson and the other from Jeb Dunnuck.

News Insights

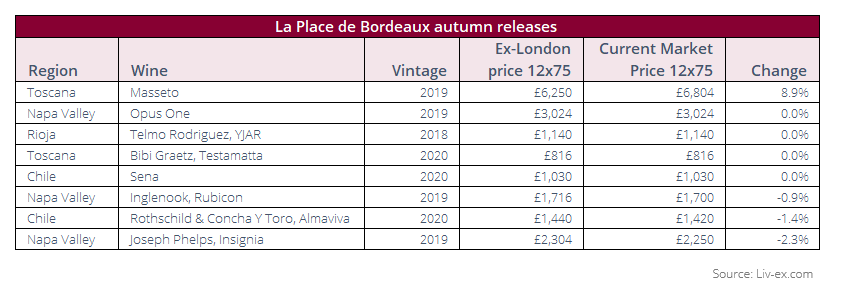

Autumn campaign fails to deliver

September was dominated by the swathe of new fine wine releases coming through La Place de Bordeaux.

Over the years La Place has evolved to become a primary distribution network not just for Bordeaux but for wines from a plethora of regions and countries around the world.

As detailed in our report on the changing nature of La Place, this year’s campaign was the biggest yet with well over 100 different wines being released.

The autumn campaign (there are also releases in the spring) tends to follow a more structured path than Bordeaux En Primeur. Nonetheless, the report did note that the fortunes of these wines on the secondary market was increasingly mixed and, furthermore, voiced concerns that the increasing number of releases threatened to drown out smaller releases especially if they did not offer the all-important relative value.

Even for more established names with more clout in the secondary market, the importance of offering fair value with each new release is paramount – especially in light of the prevailing economic conditions.

Unfortunately, both the pace and volume of releases and many pricing strategies fell short of the mark. Even now, considerable numbers of wines remain available on merchants’ websites – occasionally in sizeable quantities.

As the chart below shows, with the exception of Masseto, several of the keynote releases have held their value or declined. Overall, it seems this campaign has served largely to leave more wine backed up in the supply chain and weighing heavily on merchants’ books.

That being said, a few wines did hit home. Initial reports suggest the 2019 wines from Opus One and Masseto appear to have sold through with little trouble. Demand for Masseto has already translated into a price increase of 8.9%.

Critical Corner

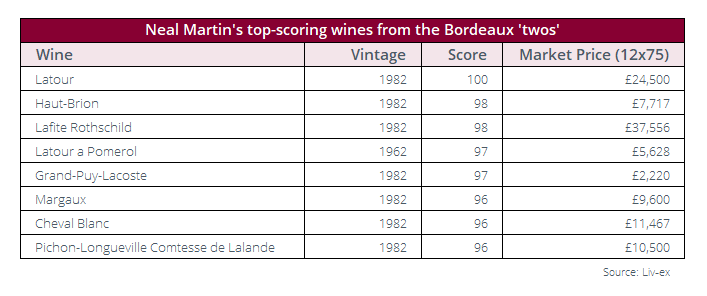

Neal Martin on the Bordeaux ‘twos’

Neal Martin (Vinous) recently revisited all Bordeaux vintages ending in ‘two’ from a 10-years-on tasting of the 2012s to the now 110-years-old 1912.

His highest scores went to wines from the 1982 vintage, awarding only Château Latour a perfect 100-points. He described it as ‘the most consistent of the First Growths in this auspicious vintage’ and that ‘it exudes class and majesty’.

Meanwhile, the ‘harmonious and effortless’ Haut-Brion and the ‘magnificent’ Lafite Rothschild also from 1982both received 98-points. Overall, Martin explained that while ‘one might assume that it was a shoo-in for estates during that year […] 1982 was a growing season with obstacles to overcome right to the very end’.

A wine from the 1962 vintage also appears among his top-scorers that boast over 96-points. On the vintage in general, Martin revealed that it was ‘perpetually overshadowed by 1961’; however, there ‘are gems to be found in this growing season’. He singled out the ‘breathtaking’ Latour a Pomerol as one of them.

Meanwhile, the most recent of the vintages he reviewed, the 2012, ‘has been overshadowed by 2015 and 2016, often paired with 2011 as the comedown duo after 2009 and 2010’. He further described it as ‘a solid vintage without fireworks’ on the Left Bank, and one offering ‘diversity of styles’ on the Right Bank.

His full report can be read here.

Final Thought

The state of the market for rosé Champagne

The history of rosé Champagne is relatively recent in comparison to other fine wines. Historians at Champagne Ruinart have found documents recording sales of pink fizz dating back to 1764. However, most Champagne houses only introduced rosé to their portfolios in the 20th century, such as Dom Pérignon in 1959 and Louis Roederer in 1974 – as a partner for Cristal blanc.

The production of rosé requires a different approach and greater effort from Champagne producers, and many of the reputable houses have invested in vineyards that supply them with suitable red wines for their blends. Volumes are thus naturally more limited, and the wines command a premium to their white counterparts.

Secondary market demand

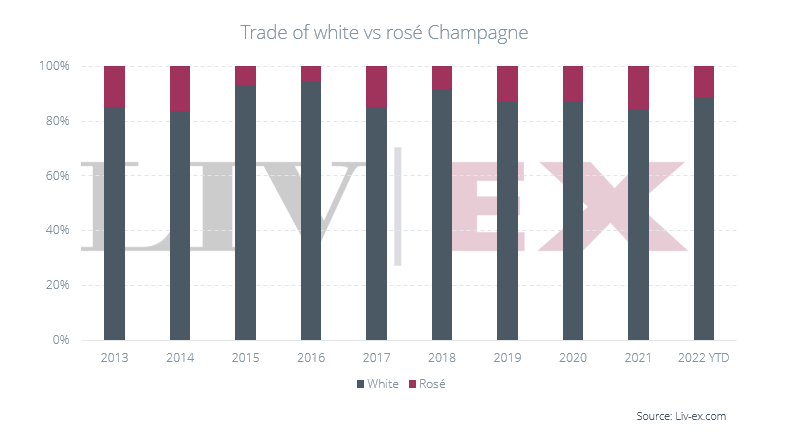

Rosé Champagne has carved out its own niche in the secondary market. Trade has peaked in some years, like 2014 when it accounted for 16.4% of the total for the region. However, the secondary market for Champagne was much smaller than it is now. In 2014, Champagne only represented 3% of the fine wine market, compared to 12.8% so far this year.

Last year, rosé accounted for 16.1% of the total Champagne trade, principally driven by US buyers, who were taking advantage of the region’s exemption from President Donald Trump’s 25% tariffs on European wines. Between 2020 and 2021, the value of rosé Champagne bought by US merchants rose 230.1%.

However, so far this year its trade share has declined to 11.1%, as white Champagnes have led demand and price performance. As our recent report highlighted, only one rosé has featured among the top traded Champagnes year-to-date – Louis Roederer Cristal Rosé 2013.

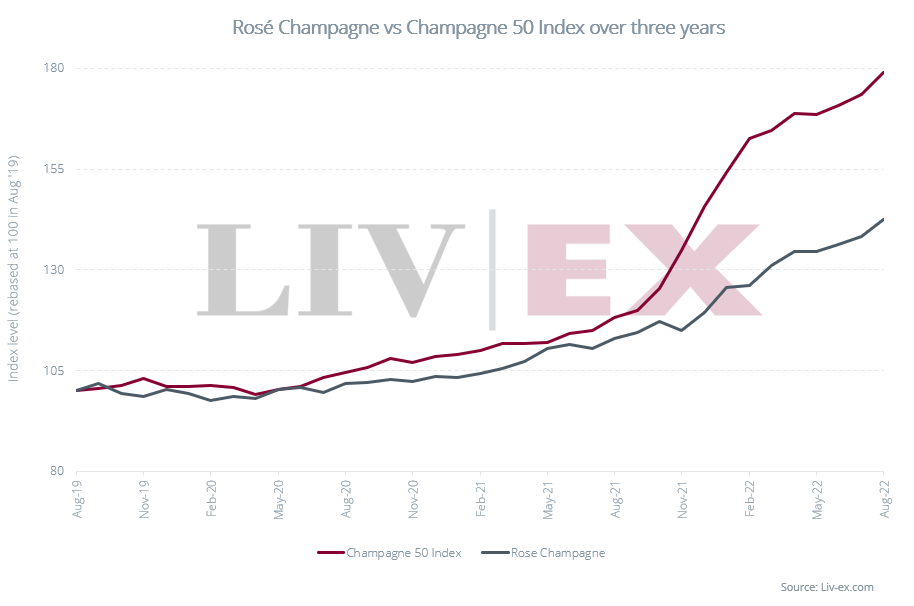

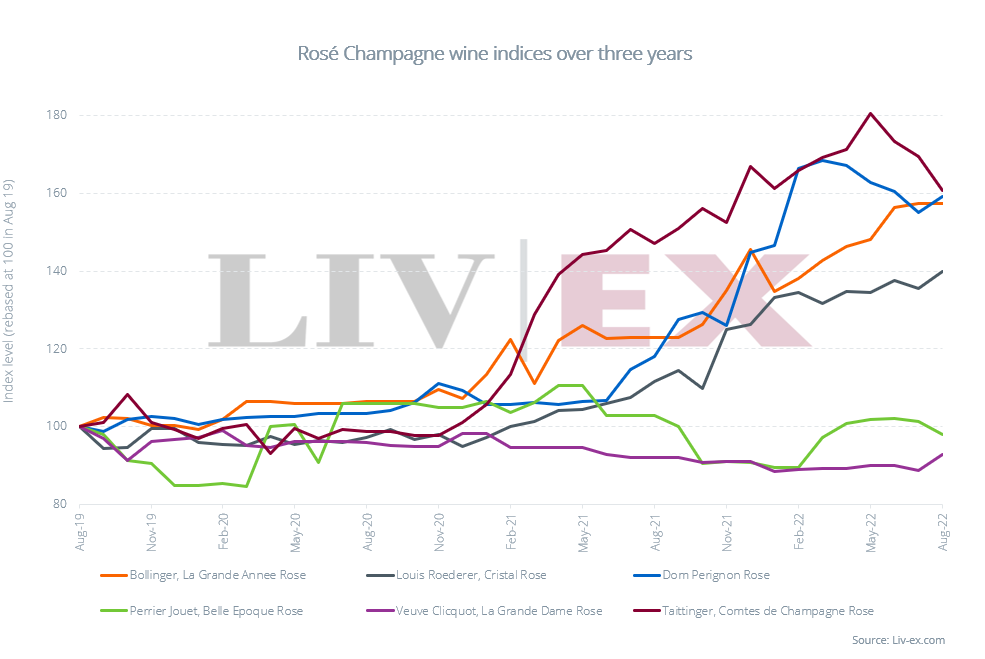

The price performance of rosé Champagne

In terms of price performance, pink bubbles have also lagged behind white Champagne. On average, rosé Champagne prices have risen 29.0%, compared to 52.3% for the Champagne 50 index over the past year.

This year’s rankings of the top 10 best-performing wines from the region also featured just one rosé – Louis Roederer Cristal Rosé 2008.

When it comes to wine labels, Dom Pérignon Rosé has been the top-performer in the last year, up 34.8%. It has been followed by Bollinger La Grande Année Rosé, up 27.9%.

Over three years, however, Taittinger’s Comtes de Champagne Rosé has outperformed the rest, with a 61% increase. The wine is up 9.5% in the past year.

The direction of the market

It remains to be seen what direction rosé Champagne might take as this market sector grows. It has always been a part of the secondary market for Champagne but the size of its presence has fluctuated – one strong year followed by declining trade over the next two. As the Champagne market expands, drawing in more houses and growers, the volume of white Champagnes is naturally relegating the less-commonly produced pinks to a smaller niche.

However, the fact that brands such as Cristal, Comtes de Champagne and Dom Pérignon have rosé cuvées of their own will be of great benefit to the rosé category. Not only do these brands have the capacity to produce rosé at a reasonable scale, as the wider Champagne market evolves, buyers can easily identify and trust these big names when looking for other options outside of white cuvées.

Of course, being produced in smaller quantities and with higher average prices, the market for rosé Champagne was always going to grow at a slower rate than for the white wines. However, as this market segment evolves this lack of liquidity, if it is coupled with rising demand, could one day make rosé Champagnes some of the best price performers around.

Read our latest report, ‘Champagne: The growing secondary market for luxury’, here.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines. Independent data, direct from the market.