The fine wine market in Asia-Pacific

Fine wine as an investment

Fine wine has long held an allure as an investment asset. While the market has its intricacies, it has worked on a simple premise: as fine wine gets older and supply diminishes, its value is expected to rise.

One of fine wine’s key investment benefits is its tangibility. Due to its finite supply, both as a physical good and a vintage product, and rising demand from a growing global market, its price tends to appreciate over time.

Physical assets are also seen as stable sources of value in uncertain times. While stock markets can crash overnight, physical assets do not cease to exist (unless, in this case, they are drunk). Fine wine can be compared to real estate but without the maintenance costs or being reliant on a single economy.

Fine wine also provides an effective hedge against inflation and recession, a particularly pertinent theme at present. Its past performance has proved that it can successfully weather rising prices and economic downturns.

Its low volatility and low correlation to mainstream markets makes it a popular alternative investment, as it reduces the overall risk of a portfolio, protecting wealth and providing returns.

There are some downsides. Investing in wine doesn’t pay a dividend like a share or coupon rate as a bond does. Storing wine incurs costs too and the trading cost is much higher than a share. Finally, fine wine has been the target of counterfeiters, so provenance is an important consideration.

The development of fine wine investment

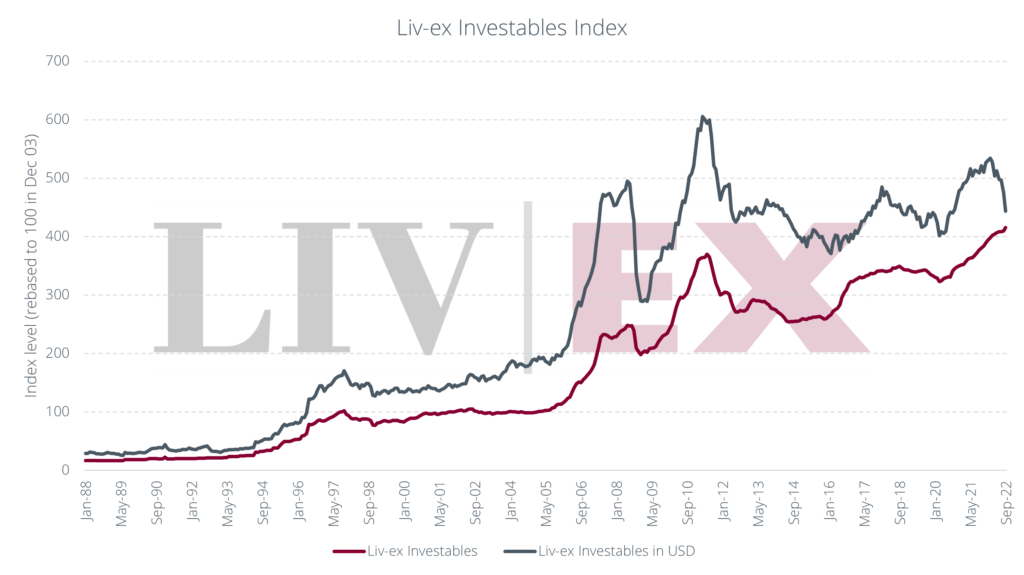

The Liv-ex Investables index, seen in the chart below, provides an insight into the evolution of fine wine prices. Launched in 2009 but backdated to January 1988, the index tracks the performance of wines commonly found in an investment portfolio.

Like all Liv-ex indices, the Investables is measured in Sterling. Its current level of 415.4 marks a record high for the index, which has risen 308.9% over the last two decades.

However, when converted to US Dollars, the index is currently 26.7% below its April 2011 peak (when it reached 605.1 points). The index is now at its lowest level since September 2020. This creates a unique opportunity for Dollar-buyers, who can take advantage of the strength of the currency, while the value of their collection continues to rise in Sterling.

*The Liv-ex Investables index includes wines that have 95-points or above from a leading wine critic. The top eight Bordeaux ‘brands’ – the five First Growths, Ausone, Cheval Blanc and Petrus – are included on the basis of a score of 93 or above. Wines produced in the last 15 vintages can be included in the index; prior to that only wines from strong vintages qualify. The wines must be physically available in the UK market.

Fine wine’s development within Asia-Pacific

Like all markets, fine wine is driven by cycles impacted by world events. From the Second World War, to the oil crisis of the 1970s, recessions of the 1990s and 2008, to the recent Covid pandemic, markets rise and fall.

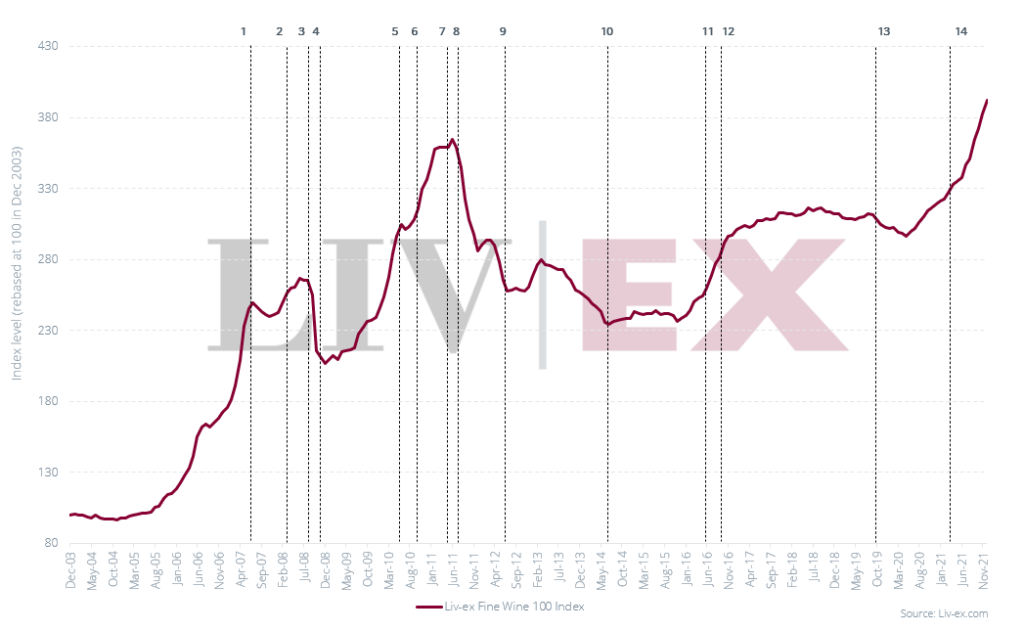

These more recent cycles are reflected in the performance of the Liv-ex investables index above, but even more so in the Liv-ex Fine Wine 100 index, which represents the price movements of the top 100 most sought-after wines on the fine wine market.

As the chart below shows, one of the sharpest increases in wine prices was when China tuned in to the fine wine market in 2008. Spurred on by stimulus packages in the billions, with the elimination of import taxes of wine in Hong Kong and the much-hyped releases of the 2009 and then 2010 vintages from Bordeaux, by 2011 the secondary market had risen to a peak. But the fervour and speculation proved a dangerous cocktail. In 2012 China’s government introduced a gift-giving ban that would prove to be the mortal blow to the speculative clamour surrounding Bordeaux. Overnight demand collapsed and merchants were left with cancelled orders and excess stock that would take years to deplete.

Timeline of key events:

1. July 2007: Hong Kong cut duty from 80% to 40%.

2. March 2008: Hong Kong cut duty to 0%.

3. September 2008: Lehman Brothers file for bankruptcy, signalling the start of the financial crisis.

4. November 2008: China announces economic stimulus programs: 4 trillion yuan of investments in areas such as infrastructure, transport, industry, tax cuts and finance. Chinese interest in fine wine, a popular gift among officials, steadily increases.

5. June 2010: The Bordeaux 2009 vintage is released En Primeur at all-time high prices.

6. October 2010: China’s economic stimulus package was a success and purchases of luxury goods in the country were booming.

7. May 2011: The Bordeaux 2010 vintage is offered for sale at record prices, testing the strength of the market.

8. August 2011: The fine wine market peaks before experiencing a downturn in prices.

9. July 2012: China announces a crack-down on gift-giving of luxury goods among government officials.

10. July 2014: The market hits its lowest point since before the China-led boom.

11. June 2016: Sterling weakens following the UK’s ‘Brexit’ vote. This provides a boost to the market as stock held in the UK is effectively discounted to overseas buyers.

12. September 2016: Liv-ex saw its first ever trade for Chinese wine, when a 6×75 case of Ao Yun 2013 traded.

13. October 2019: Following disputes over the WTO’s ruling on the Airbus/Boeing dispute, the US introduces 25% tariffs on European goods, including wine. Regions exempt from the tariffs saw the biggest price appreciation in 2020.

14. March 2021: China formally introduces tariffs on Australian wine.

Change afoot in the Asia-Pacific fine wine market

Since 2010, greater China has remained important to the global market. Buying spikes are witnessed ahead of Chinese New Year, commemorative bottles continue to be released specifically for the Chinese market and global powerhouses like Domaines Barons Rothschild and LVMH continue to invest in their own Chinese vineyards. Secondary market activity for Australian wine also shrank as a result of Chinese tariffs introduced last year.

But even when it is not directly linked to wine, what happens in China has a much wider impact. President Xi Jinping’s zero-covid policy (recently reaffirmed as he was sworn in for a third term) is proving crippling to the recovery of the Chinese economy. The Yuan, like many other currencies is growing weaker against the US Dollar, falling to new lows in mid-October. The property market (a key driver of China’s Gross Domestic Product) is also in crisis, mired in negative sentiment, and while the party has announced a one trillion Yuan plan to boost businesses, there has been no change to borrowing conditions for home buyers or property developers.

At the time of writing, the country also announced a delay to its GDP results for Q3, which does not suggest encouraging results. It would appear China is bound for recession and, as the world’s second largest economy, when it goes under so will others. One casualty already, bound within its orbit, has been Hong Kong. With its currency tied to the US Dollar, Hong Kong would be in an ideal position to capitalise on the strength of that currency in normal circumstances. But with its border to mainland China closed – with the soonest reopening in Q2 2023 – and the city also subject to China’s zero-Covid policy, that opportunity is slipping away.

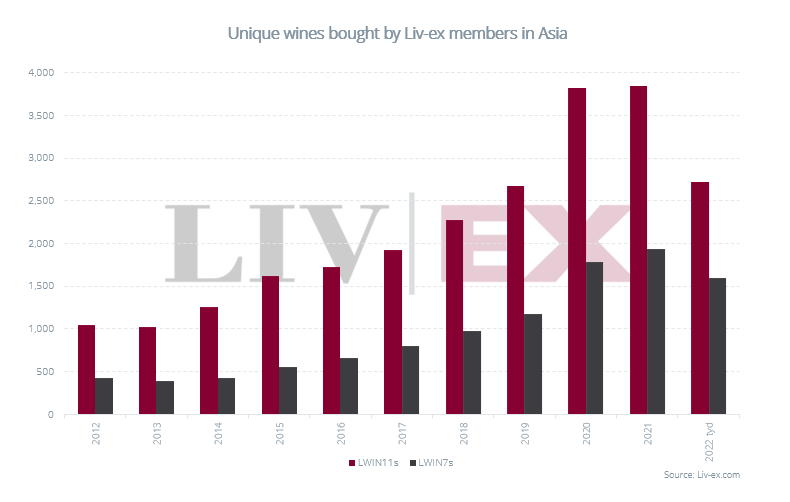

The closing of the border between China and its main supplier, Hong Kong, is undoubtedly the main reason why the number of wines traded in the secondary market by Asian merchants has taken a substantial hit this year, as shown in the chart below.

*LWINs are unique 7, 11, 16 or 18-digit codes. The 7-digit code refers to the wine itself (i.e. the producer and brand, grape or vineyard). The longer codes include information about the vintage, bottle and pack size.

But Hong Kong’s loss is another powerful city’s gain – Singapore’s. Long touted as one of the great Asian hubs for fine wine, Singapore initially found itself a little overshadowed by Hong Kong which enjoyed access to the thriving Chinese market.

But with China on the ropes and Hong Kong hobbled, a shift is occurring. For example, the organisers of the wine show Vinexpo recently announced that Singapore will be the new host city of its flagship event in Asia-Pacific from May 2023. The event had been held in Hong Kong for 20 years previously.

Singapore may not be at the door of mainland China, but it is a key hub for the growing base of collectors in south-east Asia. Its own currency is also tied to the US Dollar which gives it a powerful boost at this critical moment.

Further afield, there is Japan. During the country’s economic boom of the 1980s it quickly became the first market in Asia to embrace collecting fine wine and overall remains the second-biggest market for wine in the region. Like many Asian markets its tastes and buying habits are broadening but the country is held back at present by the weak Yen (which recently fell to ¥150 to US$1, its lowest level since 1990), and inflation is rising – up to 3% in August 2022.

Then there is South Korea, which is becoming one of the fastest-developing markets for wine in Asia. South Korea is also interesting in that it has always had a taste for non-French wines, with Chile and (increasingly) US wines holding a strong presence in the market. The country is also very tech-savvy, as shown by the rising number of data focused wine investment start-ups in the country selling fractional shares in bottles or cases of fine wines rather than the traditional model of full ownership.

Taking a broader view of the Asia-Pacific region

Any discussion of fine wine in Asia naturally centres around China. A country that is too big, too new and too full of potential for the global wine industry to ignore. Its wine market is still in development but developing fast.

Nonetheless, the view on China today seems more grounded. Many who tried their luck in China in the early 2010s found their hopes disappointed. As many have noted, it was and is a market for those taking a long-term approach.

The pitfalls of an over-reliance on China and the potentially capricious nature of its one-party state have also become clearer with time. Australia found out to its cost that falling foul of China can have a catastrophic impact on trade.

At its high point, Australian wine exports to China had exceeded AU$1 billion. After the introduction of punitive tariffs in March 2021, Australian exports dropped 81% in value to AU$223 million by the end of the year. They have fallen further since.

The disappearance of Australia’s largest export market was a salient lesson for other operators in the region. Just as the secondary market is seeing increased stability through diversity, wineries and national wine bodies are also seeking security in other markets.

Wine Australia for example recently announced new Country Managers in both Tokyo and Seoul, where imports are climbing fast. It hints that a spell has been broken. No longer do those seeking a market in Asia need to make an immediate bee-line for China. There is a wider region at their fingertips.

The fine wine market in Asia-Pacific today

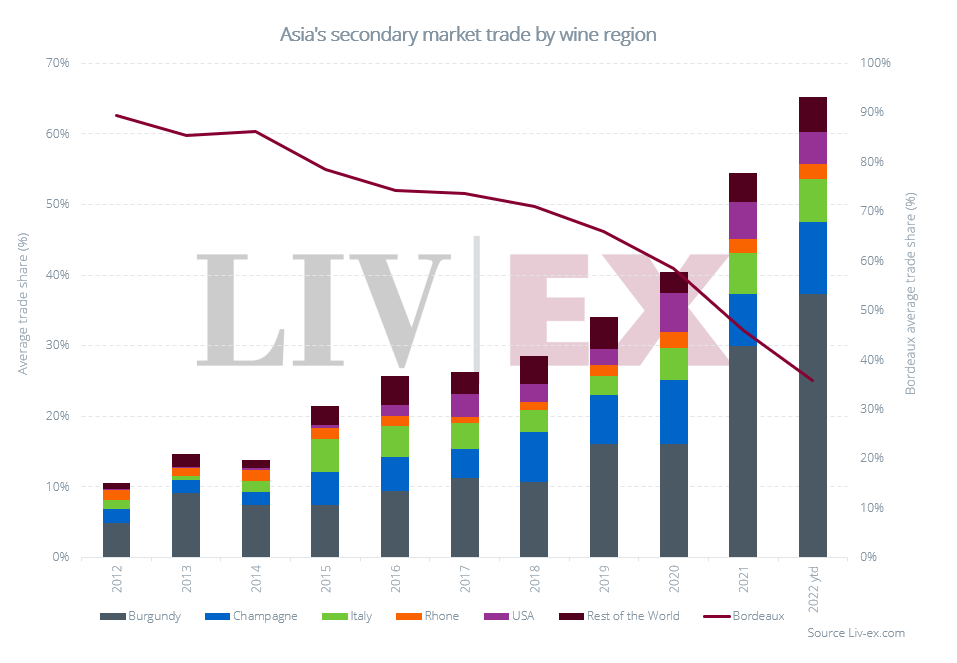

The trend in the secondary fine wine market over the past few years has been one of broadening and diversification. As education grows, tastes evolve and prices rise, buyers cast their nets wider chasing new passions, seeking new wines and looking for value.

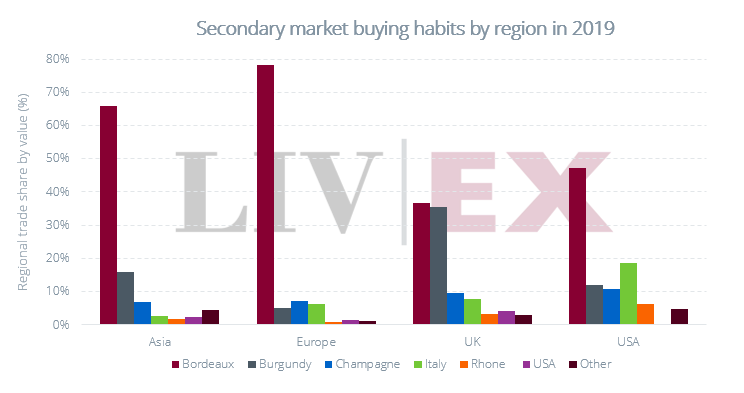

As the chart below shows, in the last decade, buying trends across Asia have followed this progression. New buyers coming to the market from the region’s myriad countries, each with their own cuisines and cultural mores, as well as the activities of wine trade bodies, have all started leaving their mark.

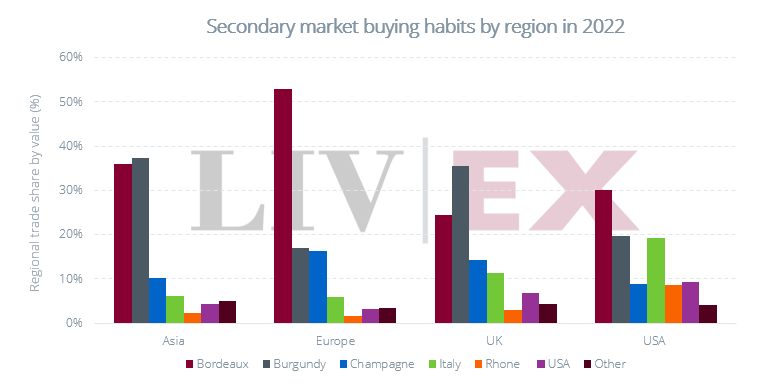

The pace of change has been most marked over the last four years, accelerated by the global pandemic. The following two charts show how the buying trends in Asia have closely reflected those in other major markets from 2019 to 2022.

The most obvious change has been the decline in Bordeaux’s dominance, especially in Asia. In the beginning, many Asian collectors went after the most famous and prestigious names in fine wine. In most cases this meant the Bordeaux First Growths, especially Château Lafite Rothschild.

At the very height of the demand for Bordeaux in 2011, the region accounted for 95.2% of secondary market trade in Asia.

However, as the charts show, since then (and in line with other global markets) demand for Bordeaux has waned. Today it accounts for just 35.9% of Asian demand (as of 30th September 2022).

Burgundy’s rise to prominence

The big beneficiary of this change has been Burgundy, which has risen from less than 5.0% of buying in Asia a decade ago, to 37.3% so far this year.

Rare and exclusive, Burgundy quickly struck a chord with many of Asia’s growing band of wealthy wine collectors. As China and Hong Kong shifted their buying habits, the market for Burgundy accelerated after Bordeaux’s decline. However, the leading market for Burgundy in Asia has always been Japan.

Unlike many other Asian nations which favoured Bordeaux at first, Japan has a long affinity with Burgundy. The country is currently the third largest export market for all Burgundy wines by value and fifth by volume according to the Wines of Burgundy trade body.

Interestingly, 55% of Japan’s Burgundy imports are for white wines – a rarity in a geographic area renowned for its ‘red obsession’. This likely explains why Japan is also the biggest importer of Champagne in Asia. According to the Champagne Bureau, Japan is the third biggest global export market for Champagne by both value and volume. The trade body also reported that the Asian market seeing the fastest growth for Champagne is South Korea, where exports rose 60.7% by value between 2020 and 2021.

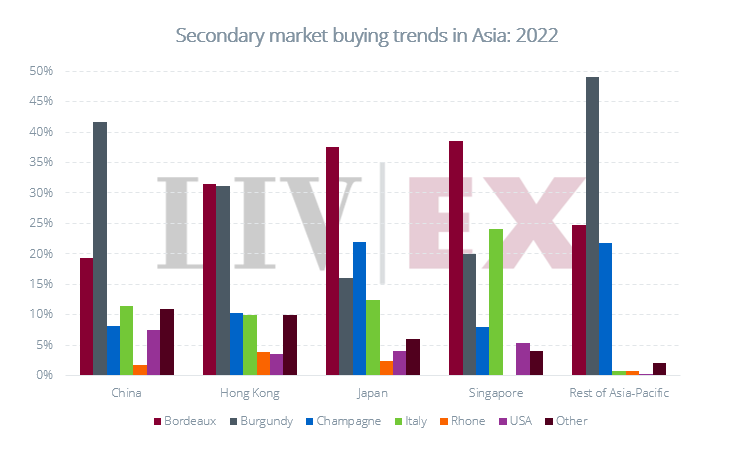

National buying trends in the secondary market

Just as Japan is the biggest importer of Champagne in Asia-Pacific, it also has the greatest interest in Champagne on the secondary market.

However, interestingly its taste for Burgundy has not been reflected in its secondary market demand so far. Given the weakness of the Yen, it may be that Burgundy prices are too great for many collectors, diverting them to better value options such as Bordeaux and Champagne. It may also be tied to consumption habits, drinking high value Burgundy in the on-trade and even a relative degree of supply and demand stability in the market.

China, by contrast, has much higher demand for Burgundy. Because it is a newer market, supplies may not be as readily available for in-demand wines, driving merchants to seek them out on the secondary market.

Elsewhere, Singapore’s taste for Italian wines, US wines in China and Burgundy and Champagne’s popularity in the ‘Rest of Asia’ (driven largely by South Korea) are other national tastes of note.

*Based on the activity of Liv-ex’s Asian members

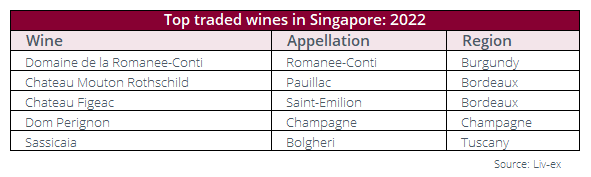

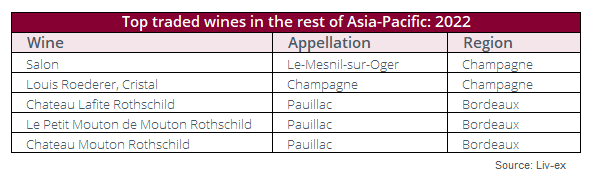

Top traded wines in Asia-Pacific markets

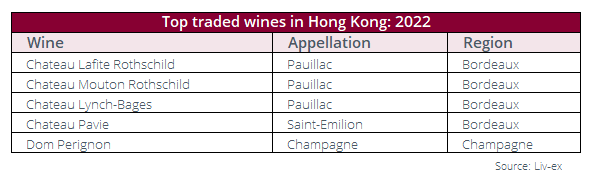

The tables below show the top traded wines (measured as LWIN7s) in the secondary market across key Asian markets year-to-date.

They reinforce many of the national market tendencies examined already; continued strength of Bordeaux in Hong Kong and the popularity of Italian wines in Singapore.

At first glance China’s top-traded list appears to contradict the chart, which shows such strong demand for Burgundy. This is because, while Burgundy commands the largest share of trade overall, when looking at which individual wines (measured as LWIN7s) have been bought the most, it is clear the likes of the ever-popular Lafite and Château Beychevelle (with its dragon-boat label), still hold enormous sway.

This in turn highlights the continued importance of brand power in Asia. As mentioned, many Asian markets in their early stages are highly focused on well-known brands. Names such as Château Lafite and Mouton Rothschild, Petrus and Domaine de la Romanée-Conti have immense traction among newer wine collectors looking for quality guarantees and kudos for good taste.

On the other hand, this is not a trait entirely unique to Asia. A look at the top-traded wines in the UK or USA would also show many of the same names.

Where Asia and many Western markets differ though – as we shall examine next – is which vintages of these famous names they choose to buy.

*The tables above show the top traded wines from each country on Liv-ex by LWIN7. LWINs are unique 7, 11, 16 or 18-digit codes. The 7-digit code refers to the wine itself (i.e. the producer and brand, grape or vineyard). The longer codes include information about the vintage, bottle and pack size.

Top vintages traded in Asia-Pacific

Where Asia is strikingly different, is that it can be less vintage sensitive than other markets. With many buyers acquiring wines as an indicator of personal wealth or for gift-giving, vintage variation is at times less of a concern than it is in the UK or USA, where collectors will often stay away from weaker vintages and make a play for the best-rated.

This is reflected in the table of best-selling vintages (below). For example, trade for the 2007 vintage in the column marked 2004-2022 was driven predominantly by trade for the Bordeaux First Growths. Despite being one of Bordeaux’s poorer vintages of the last two decades, with some of the lower scores for the First Growths (Robert Parker once rated Mouton Rothschild 88-points), it is the seventh best-selling vintage in Asia since 2004.

Similarly, this year’s best-sellers include wines from the 2017 and 2011 vintages. Neither vintage in Bordeaux excited major critics, but what ‘off’ vintages such as these provide is a (relatively) affordable point of entry to famous regions and brands – something Asian buyers have taken full advantage of.

Meanwhile, vintages with the number ‘8’ often do well because of the number’s lucky aura – something producers have pandered to, Lafite branding the bottle of its 2008 vintage with the Chinese character for example.

Conclusion

A deeper look at the secondary market for fine wine in the Asia-Pacific region reveals a region in flux and development, still tied to established names while simultaneously expanding into new categories.

More than ever, it drives home the message that Asia cannot and should not be thought of as a single market entity. It shows that although red wines dominate, there is a far greater demand for Champagne and white Burgundy than many might initially suppose.

The fine wine market continues to broaden and Asia-Pacific is experiencing and driving that trend as much as anywhere else.

Finally, with its own economic future now in doubt, China will not be riding to the rescue of the global wine trade in the difficult years ahead. With the wine world no longer as star-struck by the allure of this economic juggernaut, the time for other Asian markets to shine has come and, perhaps, for a new cycle in Asia to begin.

Liv-ex – democratising fine wine investment

Since its establishment in 2000, Liv-ex’s mission has been to make fine wine trading and investment more transparent, efficient and safe.

In 2001, Liv-ex introduced the SIB (Standard in Bond) contract for transactions on its exchange. Wines sold under this contract must be in perfect condition and stored in bond, among other conditions. This had the dual impact of increasing confidence in trading and enabling accurate price tracking and valuations for wine. Before SIB, it was impossible to know whether two transactions for the same wine could be compared, which increased the risk of mispricing.

Standardised valuations, combined with increased data sharing online brought increased pricing transparency to the fine wine market. With it came trading confidence, greater pricing efficiency, and increased liquidity. Today, there are more fine wine investment opportunities than at any other point in history.

To find out more about fine wine investment and the role of Liv-ex, read our special report ‘Introduction to fine wine investment’.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.