It is no secret that wines from Burgundy are high value. The region accounts for more than half, 59% to be exact, of the most expensive wines on the secondary market (the 1st tier in the Liv-ex Classification 2019). The Burgundy 150 index, which tracks the price performance of the ten most recently physical vintages of fifteen white and red Burgundy wines, has been outperforming all other regional indices and the broader market since 2010.

In January, we published a report, Burgundy – in the spotlight, which examined the region’s market performance and questioned the sustainability of its prices. Using Liv-ex data, the Financial Times explored the topic more recently in “Investing in wine: has Burgundy’s bubble burst?”.

In our extended report, we noted that not only have wine prices skyrocketed but they have also pushed the cost of the terroir. Chateau owners from Bordeaux have moved into Burgundy – in 2017, for example Latour owner Francois Pinault bought the monopole, Clos Tart, for an undisclosed sum. Rumours suggested a price in excess of £10m per acre was paid. What, we asked, may happen to land prices if the wines produced no longer commanded such stratospheric prices?

We also looked at the performance of Burgundy’s brightest star – Domaine de la Romanee-Conti. Last year, DRC had outperformed famous luxury groups Louis Vuitton Moet Hennessy, Hermes and Apple, proving itself as something of a status symbol.

Compared to Bordeaux’s finest – the First Growths, prices for DRC continue to dazzle.

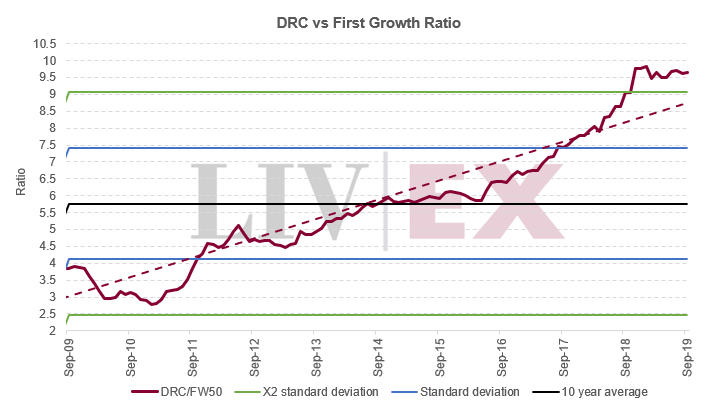

Dividing the average price of the six wines in the DRC index by the Liv-ex Fine Wine 50 gives an indication for their price differential. The ratio (DRC/FW50) currently stands at 9.65: one could still buy almost 10 bottles of First Growths for one bottle of DRC.

It peaked in January, when we last questioned its future, reaching 9.84. Our report stated:

Assuming that over the long term, prices revert to the historical mean (as represented by the ten-year average), DRC prices are looking more overstretched than ever. The ratio (DRC/FW50) has smashed through the X2 standard deviation band. There are two scenarios for the future of this ratio, if it is to return towards the mean: either the price of the First Growths will need to go up, or DRC prices will need to drop.

As the chart above shows, the price gap between DRC and the First Growths has not widened any further in 2019. It has dipped 2% in recent months. Has the limit finally been reached?