Print and read offline instead.

No rest for fine wine in August

Scotland tops trade by value in August

The quiet month of August has historically been one of the most diverse trading periods; this year was no exception. Glenfarclas 1959 60-Year-Old Single Cask led trade by value, driving the UK’s trade share to a monthly record high of 2.6%.

Bordeaux took just over 40% of the market; Burgundy accounted for 18.4%; Italy 16.1%, Champagne 7.5%; the Rhône 4.9%; USA 6.2% and the Rest of the World (of which UK is part) 6%.

The broadening of the market, even within leading categories such as Bordeaux and Burgundy, was reflected in the composition of the 2021 Liv-ex Classification. Ranking the wines of the world by average trade price into five tiers, DRC topped the list of 349 labels, followed by Screaming Eagle. As our most recent in-depth report on California highlighted, Californian estates have some of the highest average prices in the market and are taking increased share of trade (See Final Thought below).

The market is now welcoming new releases from California and other parts of the world, as the autumn La Place de Bordeaux campaign gathers pace. We are covering the main New World, Italian and other European releases.

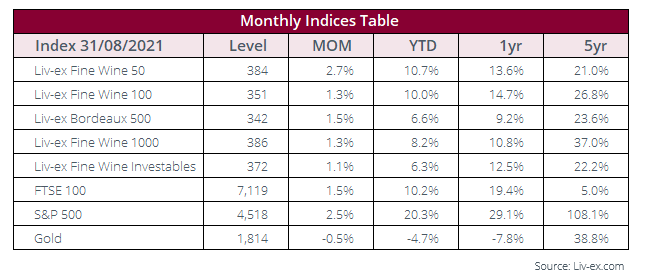

Fine wine prices continued their uptrend in August. Both the Liv-ex 100 and the Liv-ex 1000 rose 1.3%. The industry benchmark (the Liv-ex 100) has now enjoyed 16 consecutive months of gains, while the broadest measure (Liv-ex 1000) has hit another all-time high. The Rest of the World 60 was the best-performing regional index in August, up 2.5%.

News

Becky Wasserman, importer and champion of Burgundian wines in the USA, died aged 84 on 20th August. Having moved to France in 1968, Wasserman began exporting Burgundy to the US in 1976. She is widely recognised as helping drive demand for the region’s wines in export markets.

Recurrent Ventures, a US-based private equity group has acquired Jancis Robinson MW’s website. Terms of the deal were not disclosed but Robinson said there were no planned changes to the editorial team and all was “business as usual”. She added that the increased funding and tech capabilities would be used to implement improvements to the website.

Château Angélus is releasing a new wine. “Hommage à Elisabeth Bouchet” is a 100% Cabernet Franc from some of the oldest vines at the estate. The cuvée will only be made in “exceptional” years. The 2016, 2018 and 2019 have so far been produced with the 2016 released this autumn. Lisa Perrotti-Brown MW rated it 100-points.

Penfolds is the latest New World producer to offer a wine through La Place de Bordeaux. The maker of “Grange” has put its 2018 Bin 169 Coonawarra Cabernet Sauvignon into the hands of six Bordeaux négociants. The brand’s managing director,Tom King, said he wanted to use the distribution system to, “make this great wine available to more collectors around the globe”.

Major Market Movers

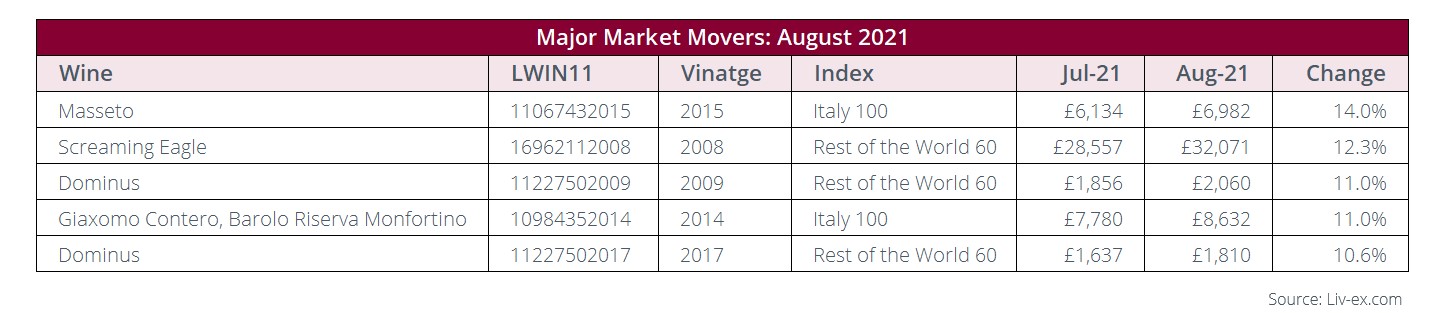

US and Italian wines were among those on the move in September. Screaming Eagle was the second most traded US wines by value in August and is the leader over the course of the year so far.

Giacomo Conterno’s Barolo Riserva Monfortino and Masseto are, respectively, the second and third most traded Italian wines by value so far this year.

Critical Corner – The Wine Advocate on the latest releases from SQN

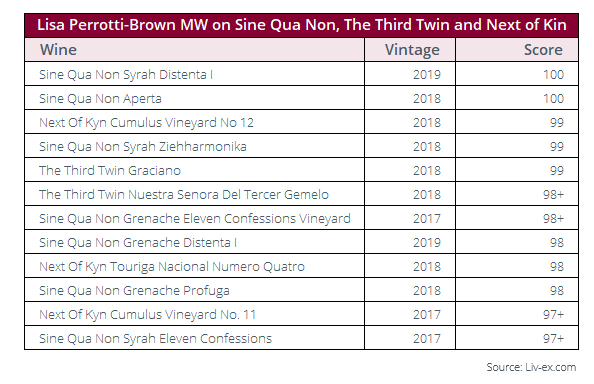

In early August, The Wine Advocate’s Lisa Perrotti-Brown MW paid her annual visit to Sine Qua Non, the California cult winery known for its sought-after Rhône style wine blends and extravagant labels. There she tasted a set of 12 wines including a pair of 2017s that each spent over three years in barrel, the bottled 2018s that she had previously tasted primarily as barrel samples and the very recently bottled 2019s.

Perrotti-Brown observed that “it’s a strong trio of very different vintages” across the estate vineyards. The “three highly sought-after labels they have created: Sine Qua Non, The Third Twin and Next of Kyn” are in “a constant state of evolution,” according to the critic, while she ascribed the success of the owners to “the absence of formulas”.

Her report also mentioned the new Sine Qua Non labels and naming conventions. Below are the scores she awarded to the new releases, including two 100-point wines.

Perrotti-Brown described the “complexity and vivacity” of the 2019 Syrah Distenta as “simply jaw-dropping,” and revealed that “1,999 cases and 600 magnums were made”. The wine is due to be released in spring 2022 ($190 per bottle).

The other 100-point wine is the 2018 Aperta: “a blend of 38% Chardonnay, 25% Viognier, 22% Roussanne, 6% Petit Manseng and 9% Muscat”. Perrotti-Brown said in her tasting note: “This is an astonishingly complex dry white, which I anticipate will age gracefully like an epic white Burgundy”. Production volumes are 906 cases, and the wine is due for release this October ($127 per bottle).

Chart of the month – Developing markets from the Rest of the World

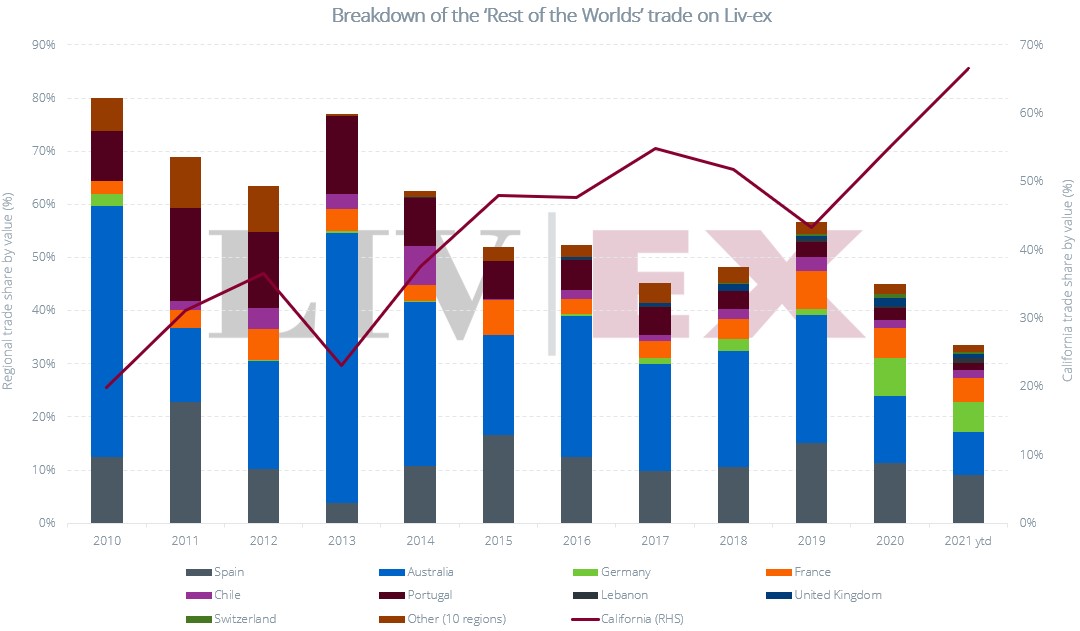

How has the shape of the Rest of the World (RoW) category changed in the past decade?

When it comes to fine wine trade, the Rest of the World category encapsulates everything beyond the mainstays of Bordeaux, Burgundy, Champagne, Tuscany and others of the like. It includes important fine wine regions that have been less active on the secondary market, such as Spain and Germany, emerging ones including the UK, and many of the more established New World players – Australia, New Zealand, Chile, Argentina, and California.

The quiet month of August has historically been buoyant for the RoW category, when smaller regions could leave a mark, before the autumn La Place campaign and active Christmas purchasing of French and Italian wines.

The RoW category has been one of the fastest evolving, benefitting from the market’s expansion. Within it, there have been shifting patterns too.

One of the biggest changes has been in the power balance between Australia and California. Ten years ago, Australia dominated RoW’s trade by value with 47.3% of the total, and California took 19.9%. Today California leads (66.5%), while Australia has taken a backseat (8%), having consistently declined since its peak in 2013 (50.8%).

New Zealand has faced a somewhat similar fate, being more active pre-2010 (on average, 16.8%, 2002-2010), and now accounting for just 0.1% of RoW’s trade by value.

Spain has emerged as the second most-important RoW player, having taken 9.1% trade share so far in 2021. The market for German wines has also developed in recent years, from 0.1% in 2015 to 7.1% in 2020, and sitting at 5.7% year-to-date.

Switzerland, which first emerged in 2017 (0.1%), reached 0.8% in 2020, and now accounts for 0.4%. UK’s trade share rose to a record high of 1.5% last year, pushed by Scotch whisky, and has taken 0.6% so far in 2021.

*Other (10 regions) include: Argentina, Armenia, Austria, China, Hungary, New Zealand, Slovenia, South Africa, Ukraine and other USA.

Final Thought

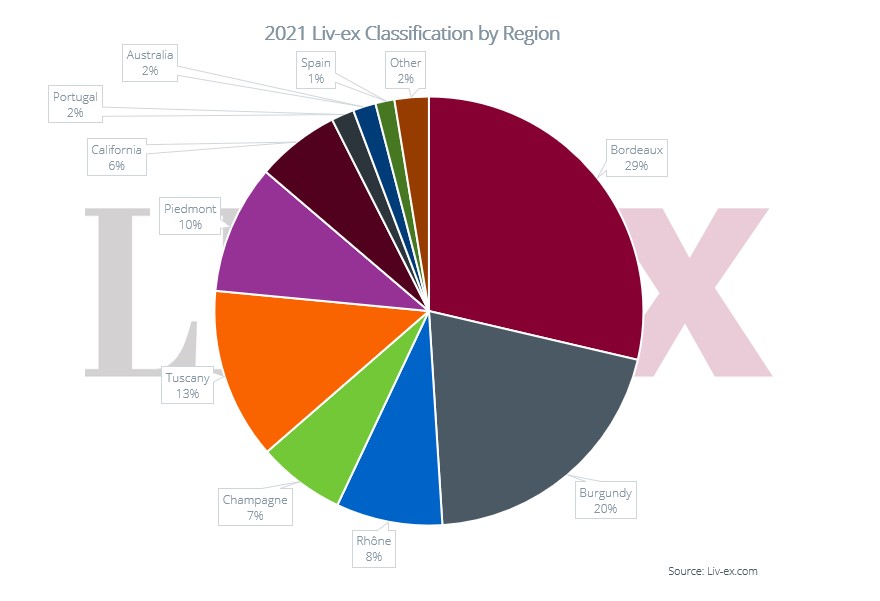

The end of August saw the publication of the 2021 Liv-ex Classification. The classification is published every two years and ranks wine in five tiers based on their average price in the secondary market.

Launched in 2009, the Liv-ex Classification originally focused solely on Bordeaux but was widened to include wines from around the world in 2017.

In 2019 the broadening of the secondary fine wine market became increasingly apparent, and that trend has only strengthened in this year’s list.

Eight countries have wines in this year’s classification, one less than in 2019 but nonetheless with a much more diverse array of labels and regions.

This year’s classification really cements the secondary market trends Liv-ex has highlighted on numerous occasions over the past year and more.

These have included the declining share of Bordeaux trade, the diversification of the market with Italy, Champagne, California and the Rhône seeing increased activity and the broadening of the market even within leading categories, such as Burgundy, as buyers seek value.

The classification is a microcosm of all these trends, and they can be seen across almost every tier.

Bordeaux’s share of trade in the secondary market has been in decline over the past few years. This has been reflected in the composition of the classification over time as well.

In 2019, Bordeaux labels constituted just over 37% over the classification list, this year it is just 28.6%. This is some way below Bordeaux’s actual share of the secondary market by volume or value but is illustrative of the general trend nonetheless.

Interestingly, the number of Burgundian wines on the list also declined by 30%. In 2019 there were 102 Burgundy labels, representing 29% of the total. In 2021 there are just 71, 20% of the whole.

The Burgundy 150 index did decline from late 2018 to early 2020 but has bounced back since. Prices for the leading wines peaked as the category’s momentum slowed. Interest in Burgundy did not go away, however. Instead, it filtered out and down to other grands and premiers crus that looked to offer more immediate value. The scale of the broadening Burgundy market was examined back in April, and showed the rising level of LWINs over the past three years.

The real winners of this year’s classification, however, have undoubtedly been Italy and the US. Italy, with 83 wines, saw a 112% increase from 2019, while the US (entirely represented by California) rose 120% from 10 to 22 wines. Its 6.3% share of the list isn’t far off its 7% share by value of the secondary market either.

The Rhône rose 12% from 25 to 28 wines, Champagne qualifiers increased 27.7% to 23 wines, Chile increased 100% from one to two wines and Portugal held steady on six.

In total there were 120 new entrants to the classification this year – 34% of the total. Over 70% of these were not from Bordeaux or Burgundy. It’s a bold new world for fine wine.