What’s happening in the market?

Sassicaia, across thirteen individual vintages, is the top-traded wine of the week so far, accounting for almost 10% of traded value. The 2020 and 2021 remain in the top positions.

Salon is the second top-traded wine by value, with individual vintages alongside Oenotheque assortment cases changing hands.

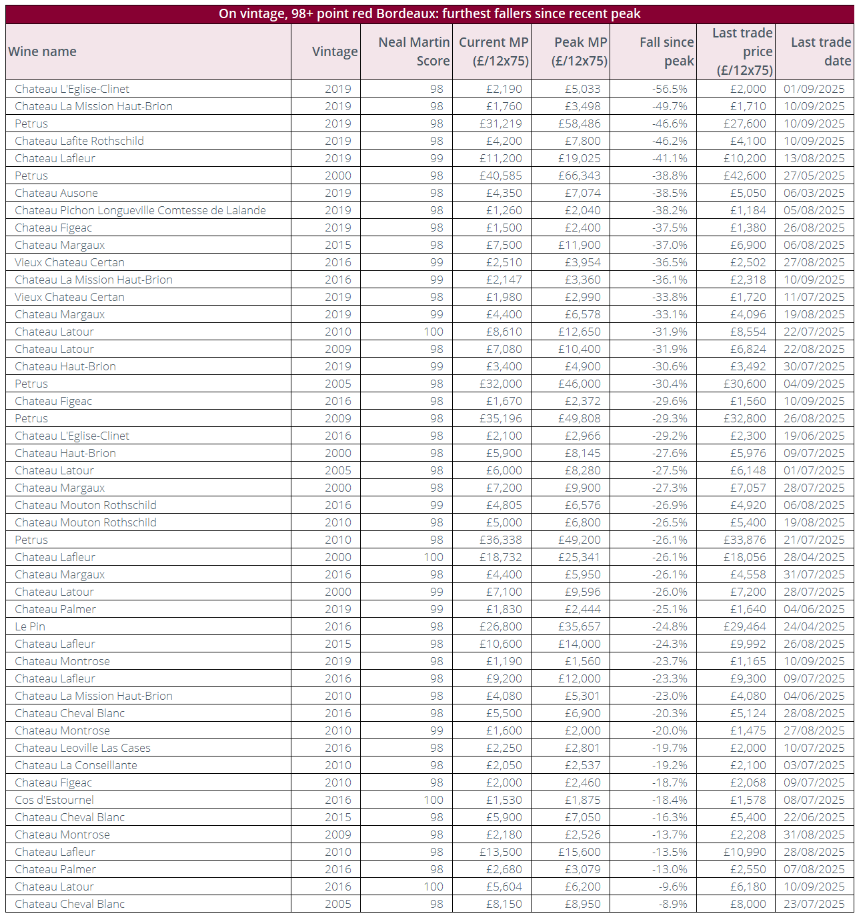

Which Bordeaux icons have fallen the furthest since peak?

- Prices of some exceptional, mature Bordeaux wines have now fallen by over 30% since peak, leaving the possibility of further downside movement increasingly unlikely.

- Analysing trade patterns of those that have fallen furthest provides some insight into which may have found their floor, and which have not.

- Several iconic wines now appear to be stabilising or recovering — Cos D’Estournel 2016, Latour 2010 and Lafleur 2019 amongst them.

A steep price decline doesn’t necessarily guarantee that prices will soon rise – we have seen a number of Bordeaux wines break below critical support levels. These wines, however, have been concentrated in weaker vintages, particularly those that were priced too ambitiously upon release (the 2021 hit hardest). For the best wines from better-received vintages — particularly those that have had extended time on the market — it appears that there is little room for further downside movement.

Considering the top wines from the top Bordeaux vintages of the past two decades – 2000, 2005, 2009, 2010, 2015, 2016 and 2019 – which have fallen furthest since their recent peak?

*Data pulled from the top vintages of Bordeaux 500 component wines with 98+ point scores from Neal Martin.

2019s have fallen furthest

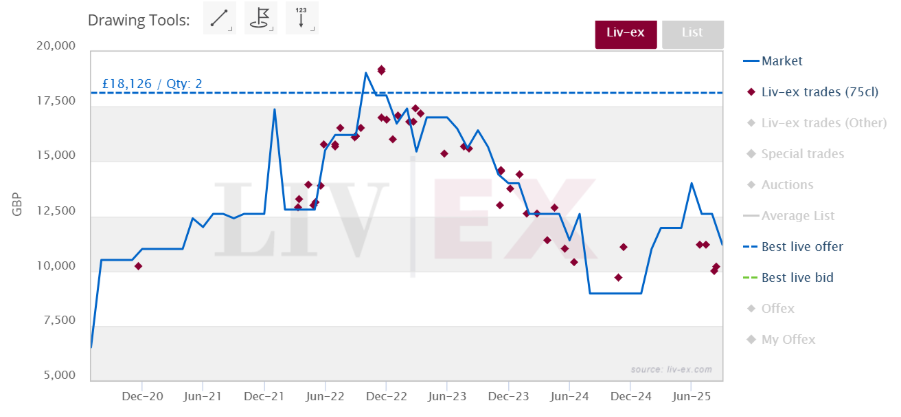

2019s top the list, in general faring worse than their more mature peers. Though it remains true that they were released at fairly reasonable prices, they physically entered the market at its peak, their prices rising immediately. L’Eglise Clinet 2019, the steepest faller overall provides an example. Released at £2,590 per 12×75, its price doubled as soon as stock landed and has steadily declined since. Those that have fallen furthest, however, may present an opportunity – being the ones that merchants have more happily dropped prices on, they may be the first to find their floors. Prices of EC 2019 have now stabilised around £2,200, with trades taking place close to Market Price with relative frequency.

Liv-ex trades of L’Eglise Clinet 2019

Largest upside potential and risk

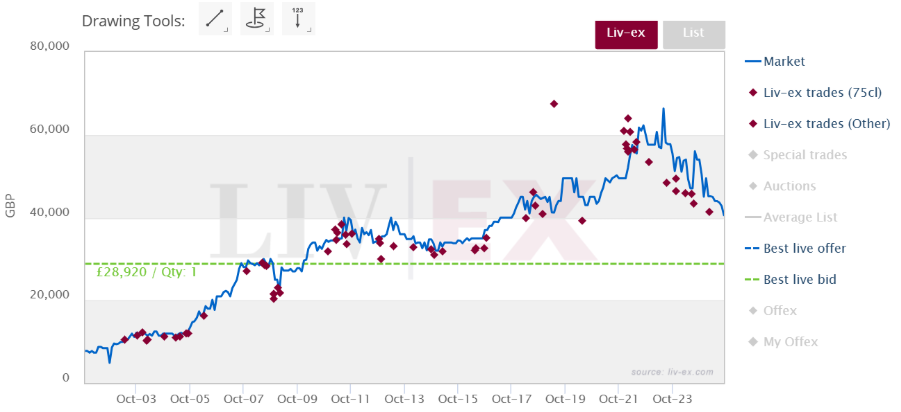

While older vintages have seen lighter falls, on average, than the 2019s, neither scores nor age have wholly protected these wines from the downturn – none are immune to market dynamics. For those seeking to capitalise, the highest value wines will offer the best returns. Buyers may turn, for example, to Petrus and Lafleur, or to the 2009 and 2010 First Growths. Some caution should, however, be exercised here – consistent trade at a given level gives weight to the view that a floor has been reached. Wines that are not trading actively or whose trade prices are consistently moving lower may have further yet to fall. Lafleur 2019, for example, has established a possible floor at £10,000 per 12×75, while the Market Price of Petrus 2000 has now crossed below its last trade.

Liv-ex trades of Lafleur 2019

Liv-ex trades of Petrus 2000

100-Pointers

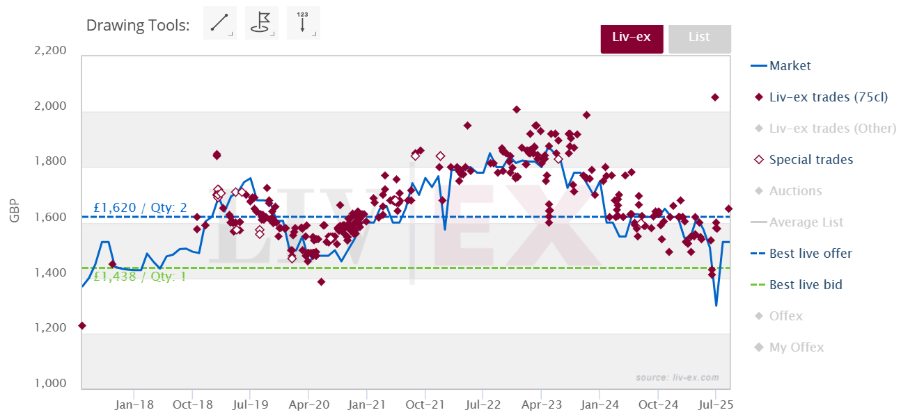

Of the 100-point wines included in this data set, Cos d’Estournel 2016, whose Market Price has fallen 18.4% since peak, looks particularly well positioned. With trades now taking place close to or above Market Price, it appears that its 2020 low is holding as a support level.

Cos d’Estournel 2016

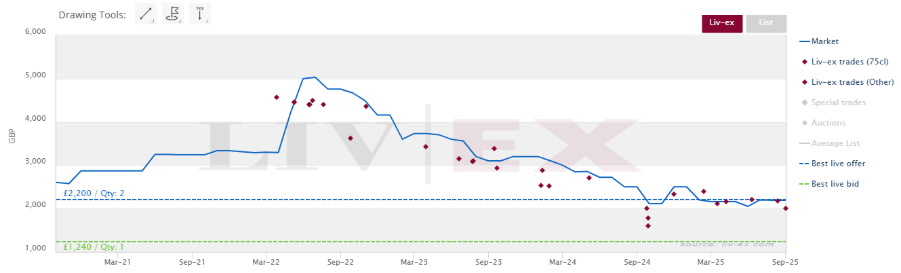

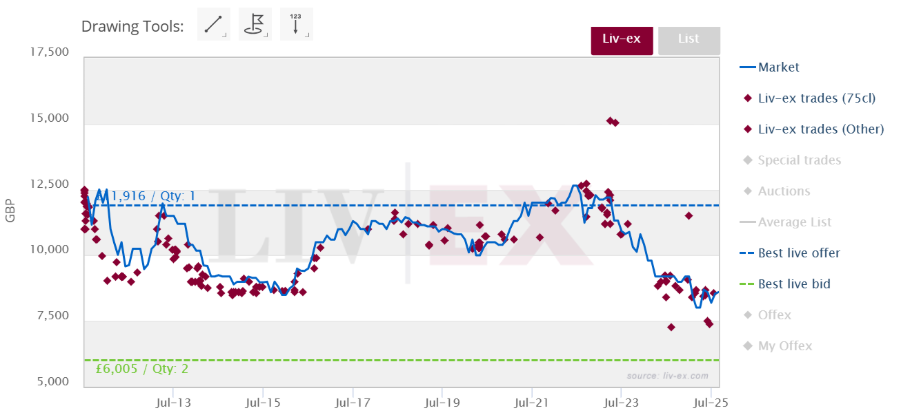

Prices of Latour 2010 also appear to have consolidated around £8,500, having briefly dipped to £7,500 earlier this year.

Liv-ex trades of Chateau Latour 2010

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.