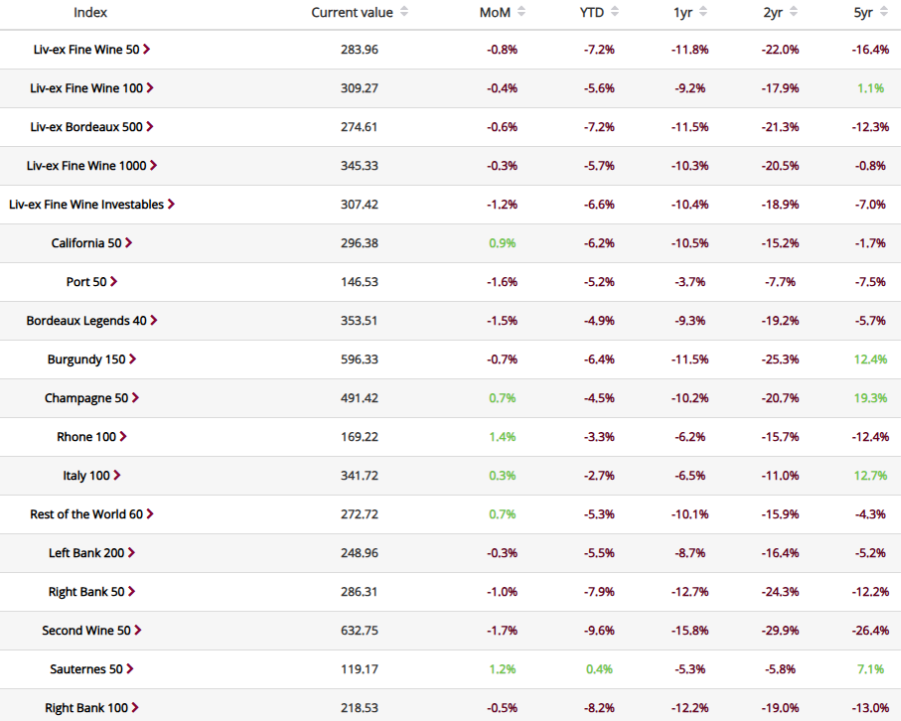

- Despite overall traded value falling by 1.2% on July, traded volume rose by 3.8%, with a marginally higher trade count.

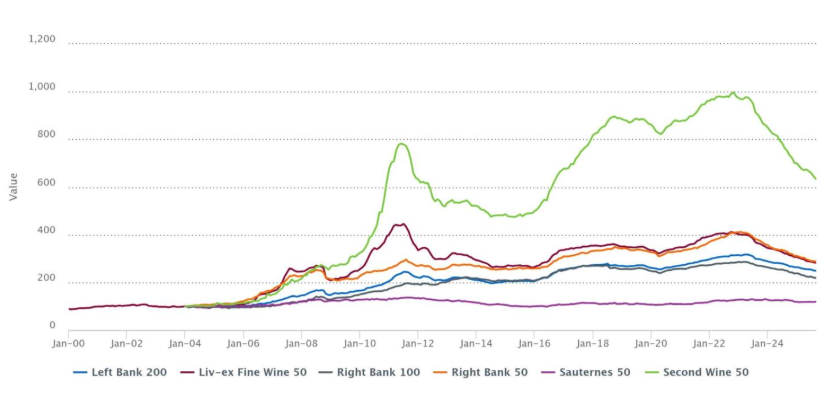

- While several indices rose month-on-month, Bordeaux saw continued weakness, with the Second Wine 50 worst affected.

- The Rhone 100 and Sauternes 50 were the best performing indices month-on-month, up 1.4% and 1.2% respectively, the Rhone 100 seeing stronger momentum behind its gains.

Though August is generally a quiet month, lack of demand giving rise to price declines, this was not necessarily the case this year. For the first time in months, several of the Liv-ex 1000’s sub-indices rose. Despite overall traded value falling by 1.2% on July, traded volume rose by 3.8%, with a marginally higher trade count.

The Liv-ex 100

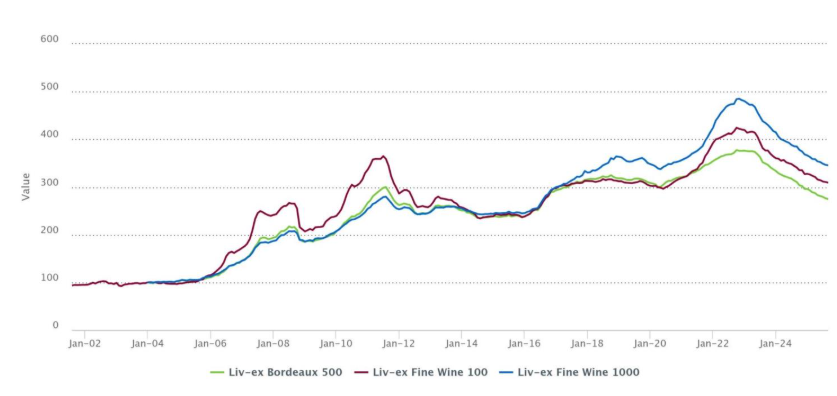

The Liv-ex 100 fell a modest 0.4% to close at 309.3. The index now sits 3.6% above its 2020 low – a level we have identified as the most probable support. Domaine des Lambrays, Clos des Lambrays Grand Cru, 2020; Harlan Estate 2019; and Domaine de la Romanee-Conti, Richebourg Grand Cru, 2020 saw the largest month-on-month Mid Price increases. Harlan 2019 may present an interesting opportunity. Having tested a low of £12,400 in April, trade prices have now risen above £13,500, its Market Price following suit.

Liv-ex trades of Harlan 2019

Domaine de la Romanee-Conti, La Tache Grand Cru, 2020; Domaine Francois Raveneau Montee de Tonnerre, 2021 ; and Chateau Lafleur 2019 fell the furthest.

The Liv-ex 1000 sub-indices

The Rhone 100 and Sauternes 50 were August’s top performing indices, recording 1.4% and 1.2% rises month-on-month. Though trade volumes of Sauternes were somewhat underwhelming, the Rhone saw its strongest month since March (pre-tariffs), indicating some momentum behind its price changes. Rayas, by far the top-traded producer of the month, saw 8 of its 10 included wines rise.

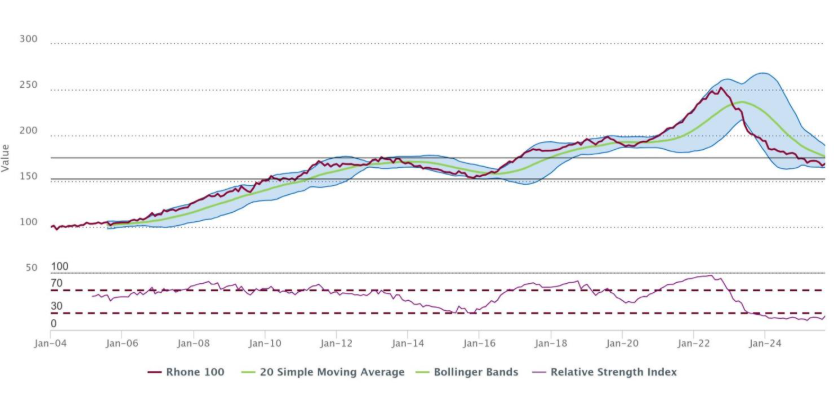

The Rhone 100 has not been the strongest long-term performer, but its return to the zone between its 2013 peak and 2015 may present buyers with an interesting entry point. With volatility narrowing, prices flattening and a bullish divergence arising between price and relative strength index, there is potential for the Rhone 100 to recover in the coming months.

Technical analysis of the Rhone 100

Italy 100 sustains its rise

The Italy 100 rose for the second consecutive month – a testament to the index’s resilience. Ornellaia performed particularly well, with only two vintages falling month-on-month.

The Rest of the World 60

The Rest of the World 60 had a strong month, up 0.7%, carried by its Californian components. The leaderboard was dominated by Screaming Eagle’s Oakville Cabernet Sauvignon, with the 2015, 2012 and 2018 vintages claiming the top three spots.

Market Prices of Screaming Eagle 2015, 2012 and 2018

The Bordeaux 500 sub-indices

Bordeaux continues to show signs of weakness, with all the 500’s sub-indices except for the Sauternes 50 falling month-on-month.

Perhaps unsurprisingly, the Second Wine 50 fell the furthest. As becomes clear when compared to other Bordeaux indices, its growth from 2016 onwards was sharp, prices rising beyond sustainable levels. Though there are some components that now look well-priced, it is likely that the index as a whole will face continued weakness.

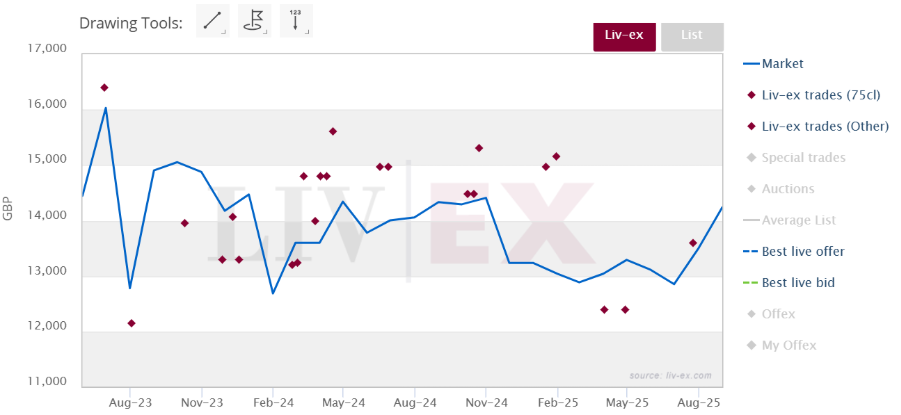

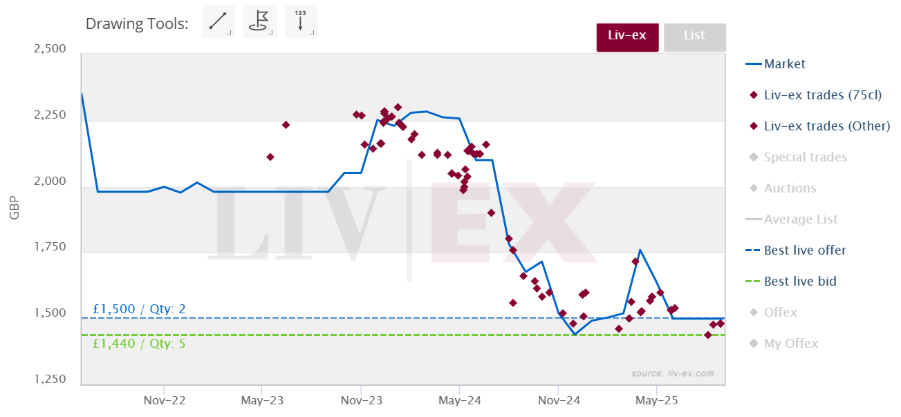

Amongst the Second Wine 50 wines to see month-on-month increases was Carruades de Lafite 2021. Having been released at £1,980 per 12×75, its price has fallen considerably. However, this fall has, at least, been short if not sweet – prices now appear to be consolidating around the £1,500 per 12×75 market, matching the 2024’s release price of £1,428 per 12×75.

Liv-ex trades of Carruades de Lafite 2021

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.