The fine wine market in H1 2025

Introduction

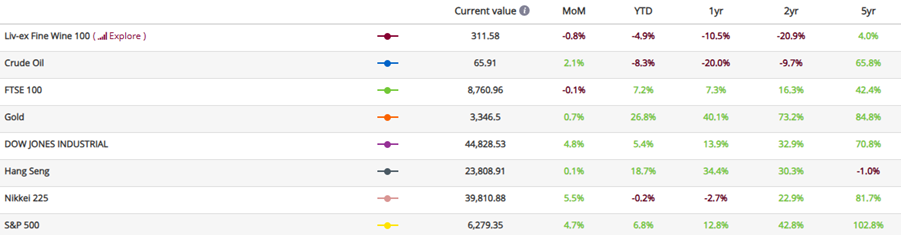

At the start of this year, Liv-ex members were ‘cautiously optimistic’ about the future of the fine wine market in 2025. On average, members predicted that the Liv-ex Fine Wine 100 would fall 1.9% from 326.1, to close at 320 in December. Already, at the close of H1, the Fine Wine 100 has fallen 4.4% to sit below this predicted level at 311.6.

The outlook in Q1 remained stoically positive – modest declines, strong trade levels, hope that the 2024 Bordeaux campaign would be a success and increasingly active US and Asian markets all pointed towards potential recovery. But, Trump’s threat of 200% tariffs in mid-March led to an overnight exodus of US buyers. These buyers had not only supported the less frequently traded regions, accounting for the lion’s share of Piedmont’s, the Rhone and Spain’s purchasing, but, prior to April, had likely prevented steeper declines. A largely unsuccessful En Primeur campaign followed, leaving each step of the supply chain in difficult positions.

While there exist pockets of stability and there are indeed some vintages that appear to be bottoming out, they are exceptions to the general rule. 2025 has not ushered in the stability the trade had hoped for. Understandably, uncertainty has prevailed.

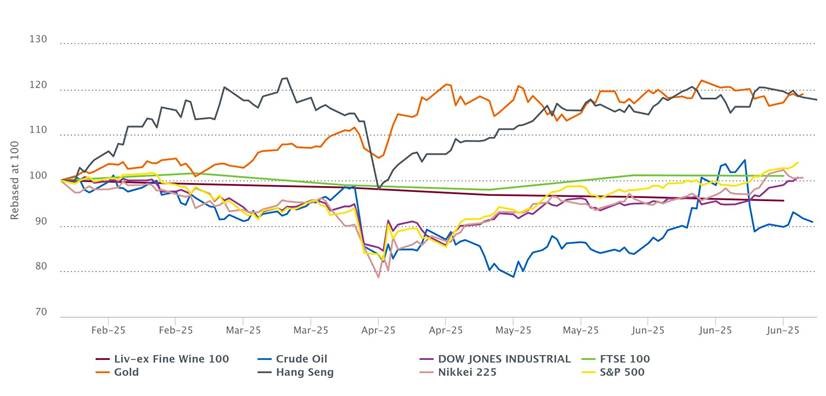

Liv-ex 100 vs. equities

*made using the Liv-ex Charting Tool. Data taken on 07.07.2025.

The fine wine market has not been alone in its tumult in H1 2025. Mainstream markets have been more volatile but quicker to recover from the various proposed policy changes and heightened geopolitical tensions. Tariff threats in March had immediate impact on all global stock markets. While, globally, growth has since been tepid, most indices have returned at least to February levels, with US, UK and German indices reaching all-time highs.

Year-to-date, the Fine Wine 100 has underperformed everything bar Crude Oil, which is down due to global economic slowdowns and OPEC’s production increase.

Liv-ex Fine Wine 50 in different currencies

The US Dollar has continued to weaken against the pound, which, minimising arbitrage opportunities for US buyers, has further encouraged their withdrawal from the market.

The Euro, on the other hand, has strengthened against the pound – an outcome that may not have worked in the favour of European market participants. A stronger Euro fanned the flames on an already tenuous Bordeaux En Primeur system, necessitating doubly aggressive price cuts for releases to present value throughout the global supply chain.

While the US withdrawal from this year’s En Primeur campaign – for many major merchants, the first year of abstinence – can be largely attributed to tariff uncertainty and growing disillusionment with the En Primeur system, the rapid weaking of the USD against the Euro no doubt had a role to play.

Price performance of the Liv-ex 1000’s sub-indices

While the Bordeaux 500 was the worst performing index in H1 2025, down 5.6% year-to-date, the Bordeaux Legends 40 was amongst the best performers, down a relatively modest 2.6%. The discrepancy between price performance of mature and young Bordeaux is a product of ambitious release pricing.

Mature vintages – those comprising the Bordeaux Legends 40 — even those released at outlandish prices (such as the 2009s and 2010s), have had sufficient time to correct. Recent vintages are not so lucky. It has become the norm to see the 2020s, 2021s and 2022s trade at their lowest-ever prices, rarely holding at ex-negociant or ex-château release prices.

Technical indicators suggest that, while the Bordeaux Legends 40 may soon find support, the Bordeaux 500 likely still has further to fall.

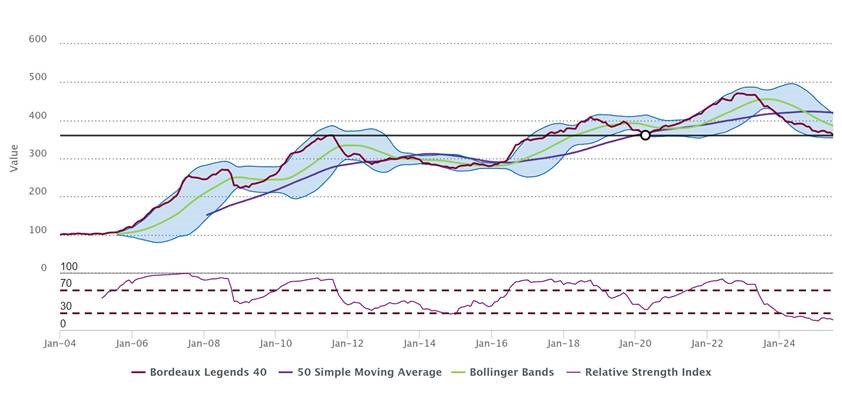

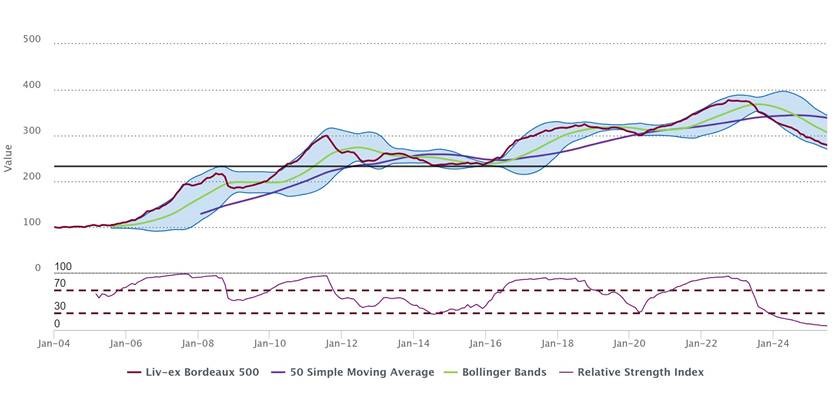

Technical analysis of the Bordeaux Legends 40

The Bordeaux Legends 40 is now resting on a critical support – its 2011 peak, upon which it found support in 2020. Volatility, as indicated by the Bollinger Bands, is decreasing, increasing the likelihood of a price break out in either direction. A bullish divergence arising between its price index and its Relative Strength Index (the former making lower lows and the latter making higher lows) signals that bearish momentum is losing steam, giving credence to the view that a breakout will more likely be in the upwards direction.

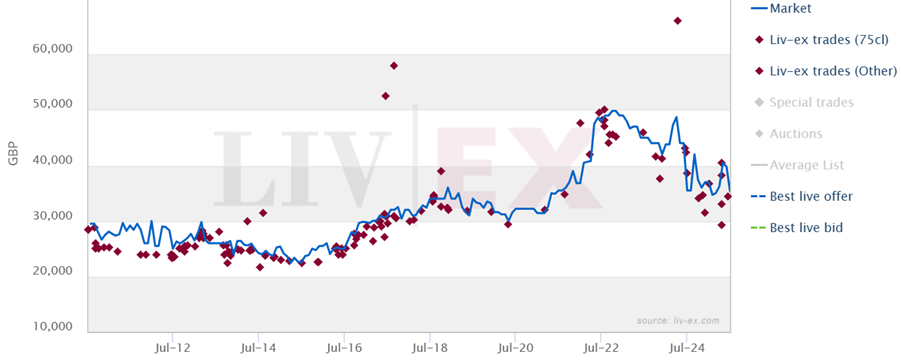

Petrus 2009, one of the top performers of the Legends 40 year-to-date, provides a representative example. In April, trade prices dipped to £30,000 per 12×75 – the same low as in 2020. Since then, however, trades have ticked up closer to £35,000 per 12×75, aligned with its 2018 peak. While there’s not yet a distinct price convergence, the bearish momentum that prevailed through 2024 has lost some of its strength.

Liv-ex trade of Petrus 2009

Technical analysis of the Bordeaux 500

The Bordeaux 500, in contrast to the Legends 40, has little support below it. With prices falling post release for the past decade (and with greater speed for recent vintages), it should come as no surprise that prices have found little support on recent horizontals (i.e. 2020 low), leaving the Bordeaux 500 in a tenuous position. With the 2022s (released at unrealistic prices) now trading more actively, already below ex-château in some cases, it would suggest that the decline may not yet be over.

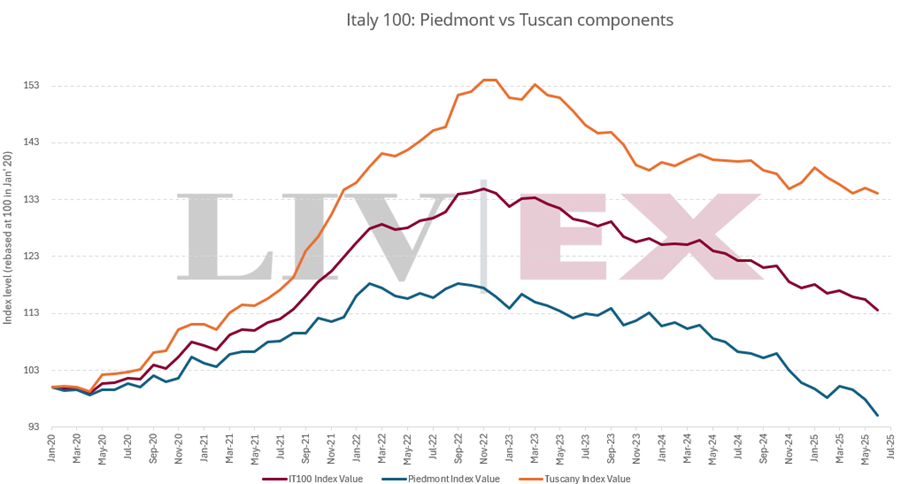

The Italy 100: a tale of two cities

The Italy 100 had differentiated itself as a beacon of stability as the broader market succumbed to selling pressure. Recent price performance, however, has cast some doubt on the index’s apparent safety. Having held steady through Q1, the index fell 3.4% in Q2. Splitting out the Tuscan components (Masseto; Ornellaia; Sassicaia; Solaia; Tignanello and Soldera Case Basse) from the Piedmontese components (Bartolo Mascarello, Barolo; Bruno Giacosa, Falletto Riserva; Gaja, Barbaresco; and Giacomo Conterno, Monfortino Riserva), two distinct stories come to light.

On average, the Tuscan components of the Italy 100 are down just 1.3% since the start of the year, while the Piedmontese components are down 5.6% — a sharper drop than that of the broader market (4.7%, as represented by the Liv-ex Fine Wine 1000).

This divergence, which formed prior to the downturn of the market, can likely be explained by the brand strength of the Super Tuscans relative to the Barolos and Barbarescos. The likes of Tignanello and Sassicaia carry similar weight as household names as the Grand Marques. While there are plenty of vintages of Gaja and Conterno’s Monfortino Riserva with perfect 100-point scores, they are less well known and come with a hefty price tag. The Super Tuscans, generally produced in large quantities and priced similarly to Bordeaux’s Second Growths, have garnered sufficient demand to support prices.

In recent months, the split between the two has widened. The bulk of Piedmont’s decline took part in Q2. In Q1, US buyers accounted for 44.0% of Piedmont purchasing, but in Q2 accounted for just 22.1%. With US buyers taking the backseat, prices of their favoured regions – particularly those that see less demand from other buying segments — have declined swiftly. While the Super Tuscans are popular amongst US buyers, the overall demand for the region is far more evenly split amongst buying segments, affording them more price protection than their Piedmont counterparts.

Trade overview

While prices have continued to fall, trade levels were all round higher in H1 2025 than in H2 2024 — volumes up 11.9% and value 4.2% higher. 58.6% of H1’s traded value, however, changed hands in Q1. Levels fell sharply in mid-April and have failed to return to pre tariff announcement levels.

Averaged over H1, regional share of trade by value has remained relatively consistent with 2024.

Champagne and Bordeaux appear to have been the most volatile, the former seeing a larger share of traded value in H2 2024 and the latter seeing a larger share in H1 2025. This is again partially explained by the change in behaviour of US buyers – when choosing which bids to reinstate, they were more likely to concentrate on Bordeaux than any other region.

Breakdown of buyer geography Unsurprisingly, H1 2025 saw a decline in US buyers’ share of the market. While this week’s tariff announcements may provide the market with some clarity, it is likely that discussions will remain ongoing. US wine businesses will eventually need to replenish stocks of European wines but doing so before costs are certain presents obvious risks. Even if tariffs land higher than expected, US buyers will be able to factor them into their margins and purchase accordingly. Until policy has been determined, we can expect US buyers to remain cautious.

Asian buyers, on the other hand, have made a cautious return, regularly accounting for c.18% of weekly traded value in Q2. Nominally, their spending increased by 55.1% from H2 2024 to H1 2025. These are promising numbers– particularly should the market no longer to be able to rely on US buyers.

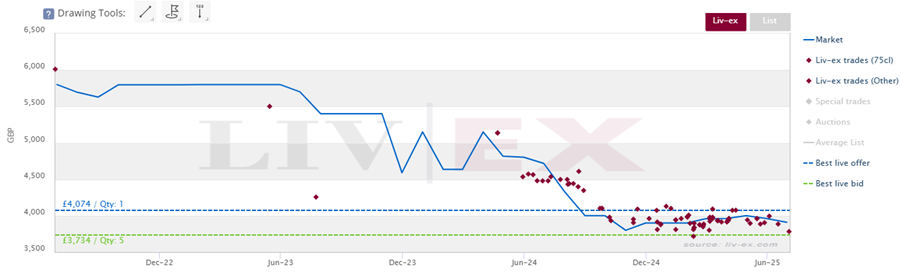

Top-traded wines in H1 2025

Château Lafite Rothschild 2021 was the top traded wines of H1 2025. Having faced a steep correction following its ex-London En Primeur release at £5,800 per 12×75, prices have consolidated around the £3,800 mark.

Liv-ex trades of Château Lafite Rothschild 2021

The 2021 vintages of Château Mouton Rothschild and Château Lynch-Bages also featured amongst the top-traded wines by value. Throughout this year’s Bordeaux En Primeur campaign, the releases of the 2024s were often bested by the 2021s (read more on the 21s here and on this year’s campaign here). Reports out of Bordeaux have noted the surplus of stock lining the halls of warehouses and tasting rooms. While the 2021s may be (at best) an annoyance to stockholders and merchants, they may also serve a more practical purpose – to provide examples of realistic price floors. In many cases, their prices now appear to be recovering, albeit slowly. Three appearances amongst the top ten wines by traded value of H1 2025 is no coincidence – at these levels, buyers are finding value.

What can we expect from H2 2025?

Expectations for the second portion of the year will no doubt have been tempered by a disappointing Q2. Nevertheless, as the market inches downwards, we can at least be certain that we are getting closer to the floor. As the Bordeaux 2021s have demonstrated, at the right price, there is demand, and enough of it to support price recoveries. If we are to see the end of the current downturn this year, there will need to be a shift in market sentiment. Though the tariff goal post seems to be moving continuously into the distance, certainty, should it eventually arrive, will provide the market with the necessary, solid starting block. Even then, we will likely have to sit tight for a catalyst – a strong resurgence of the Asian market or fire sales of surplus stock, for example — to reinvigorate the market.