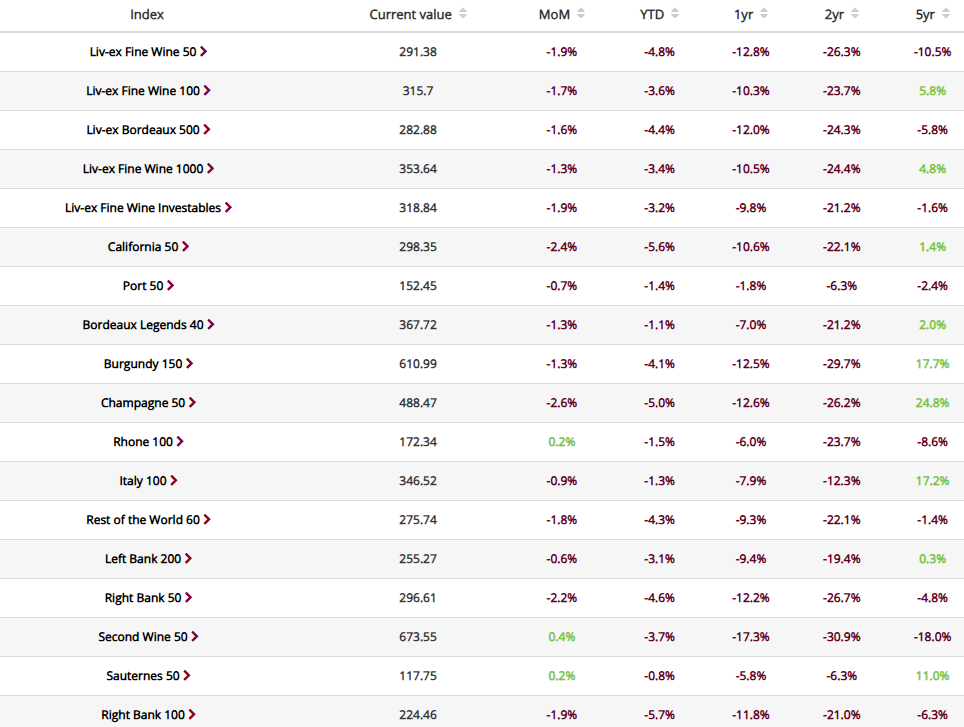

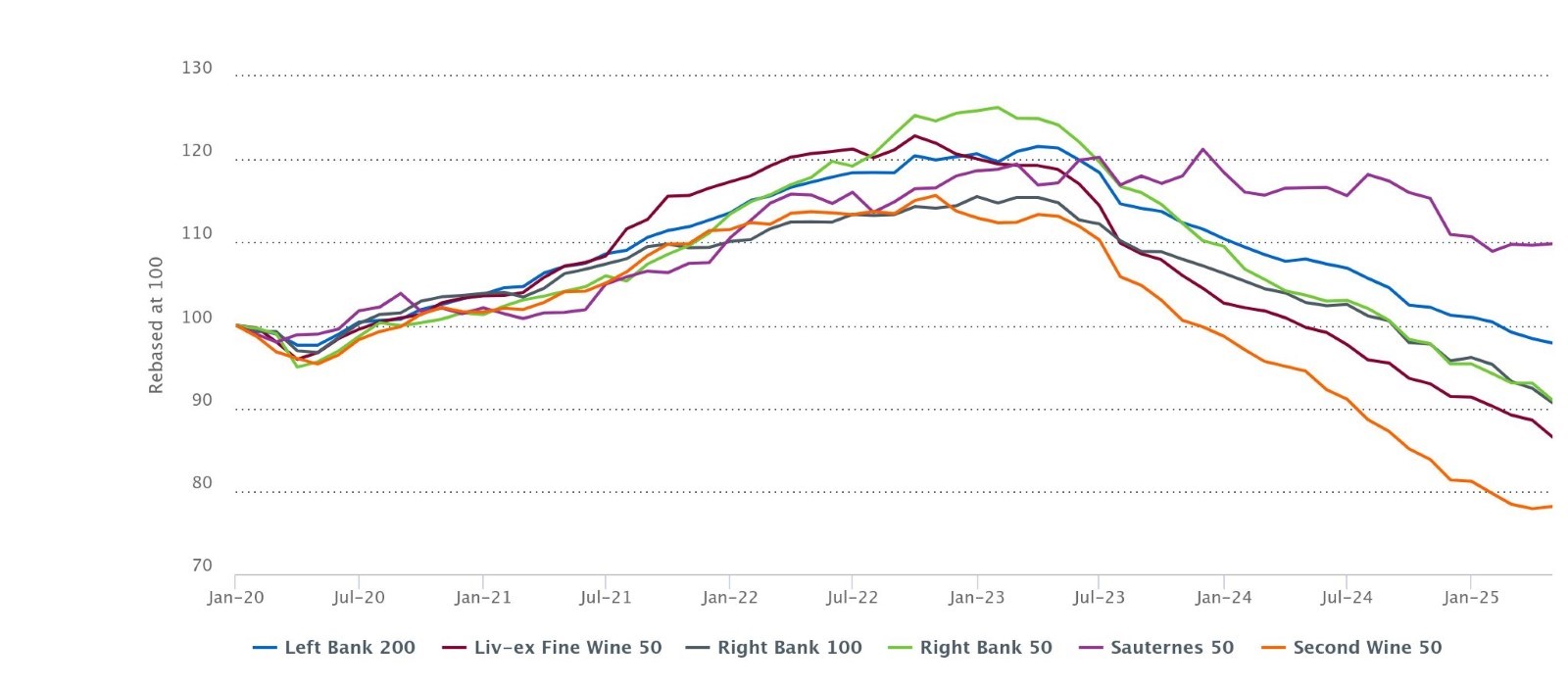

- All of Liv-ex’s major indices (except for the Second Wine 50 and Sauternes 50) saw declines in April, a likely consequence of tariff-based uncertainty.

- The Champagne 50 was hit hardest, down 2.6% month-on-month.

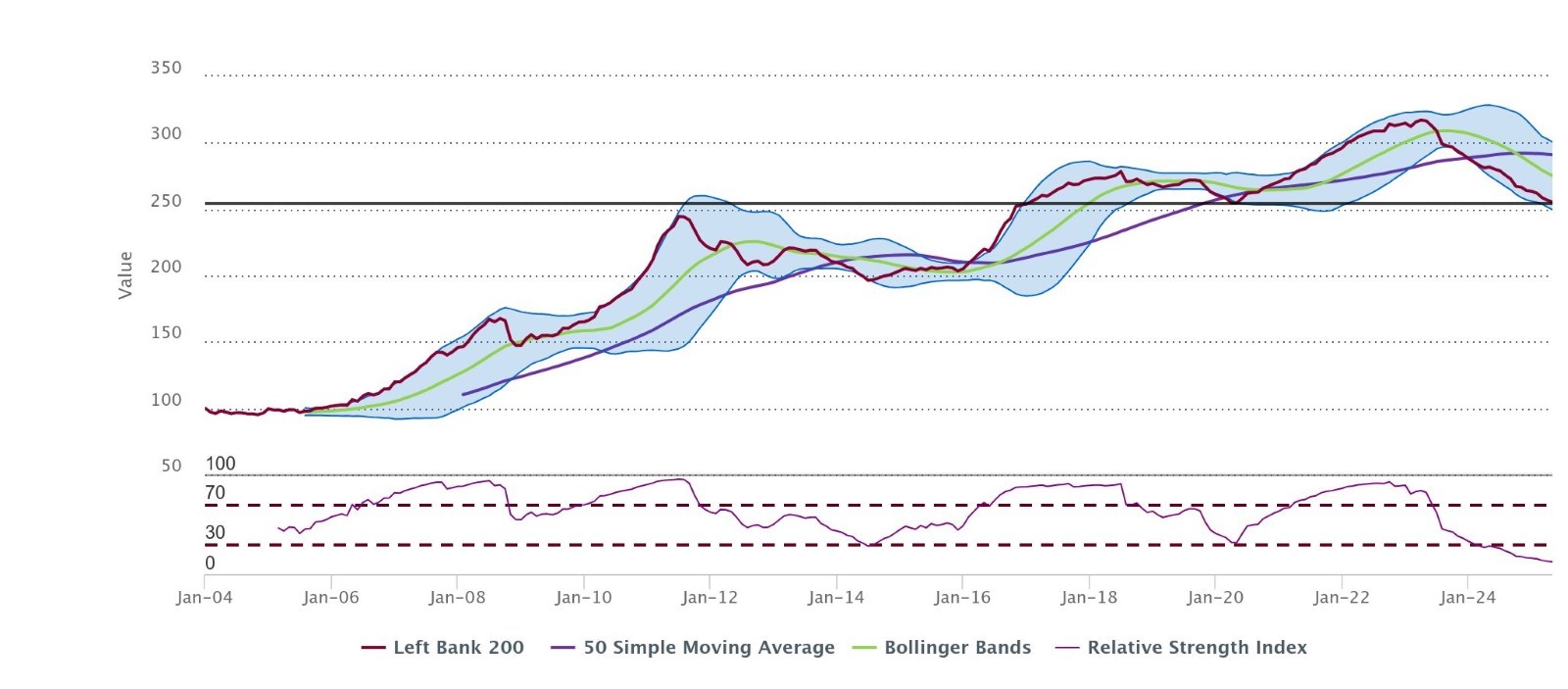

- Of the Bordeaux 500’s sub-indices, the Left Bank 200 shows the most promising signs of potential recovery.

April was not kind to the market – many Liv-ex indices saw their sharpest declines since 2023. The exceptions – the Second Wine 50, Sauternes 50 and Rhone 100 – have seen minimal trade.

The Champagne 50 was worst affected, down 2.6% month-on-month. US buyers – who are active players in the Champagne market – withdrew in March and April, following threats of high tariffs. While they have regained some of their foothold during the ‘90-day pause’ at 10%, Champagne prices have nonetheless suffered. Not only have US buyers been historically active in the Champagne market, but Dollar strength has also allowed for them to retain their margins while trading closer to Market Price. They have not needed to be as risk averse as their EU and UK counterparts.

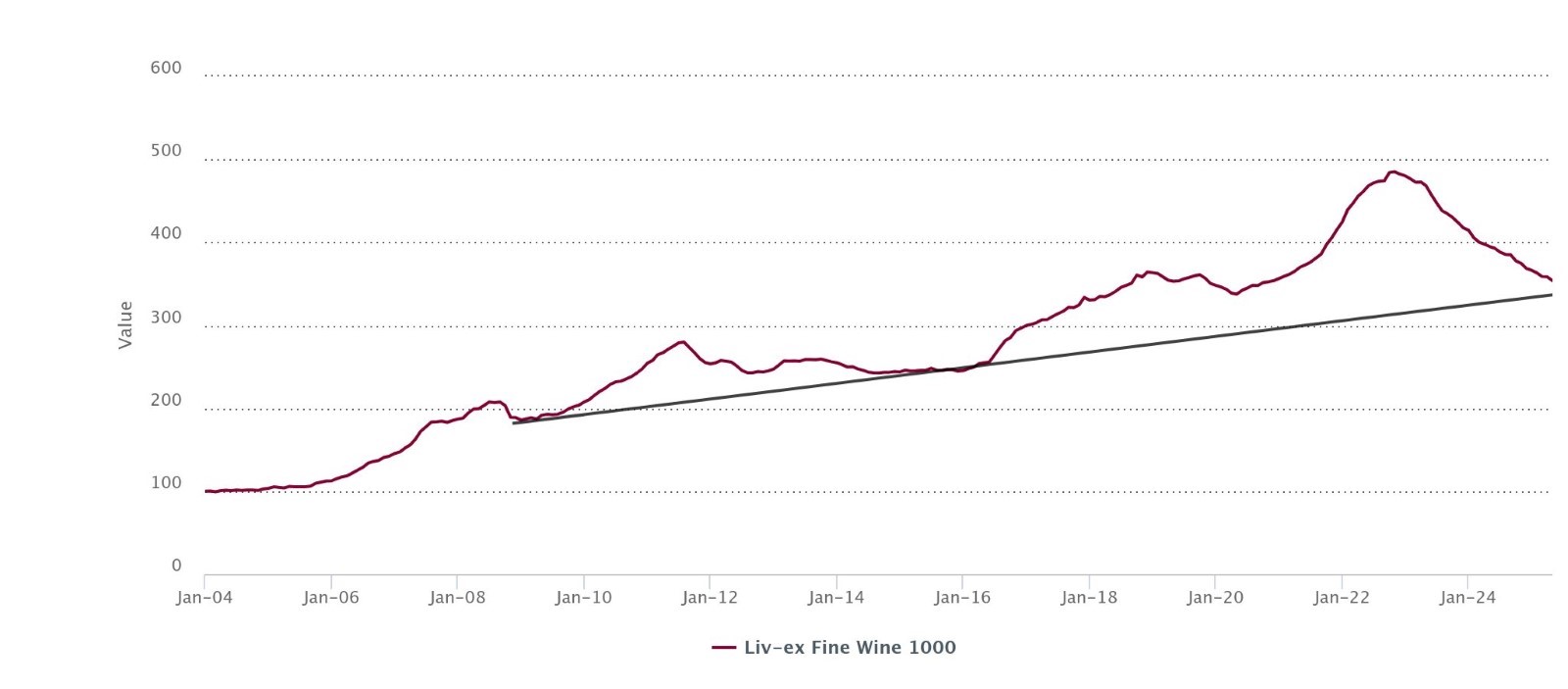

The Champagne 50 is certainly not alone in suffering the effects of uncertainty in the market – few have been spared. The Fine Wine 1000, the broadest measure of the market, fell 1.3%. This decline, however, is relatively mild, leaving the index well-positioned to find support on its long-term trend line.

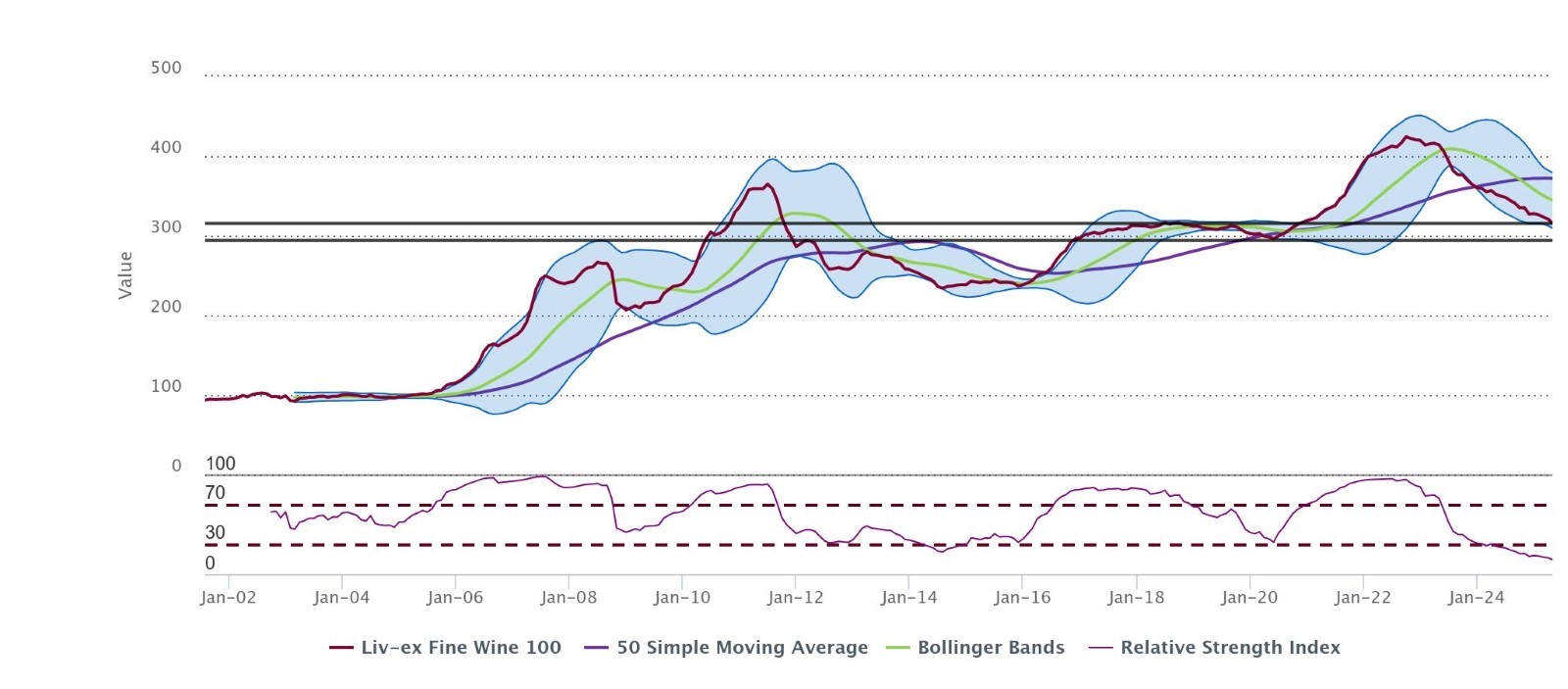

Fine Wine 100 down 1.7%

The Liv-ex Fine Wine 100, the industry leading benchmark, fell 1.7% in April to close at 315.7 — its sharpest decline since August 2023. Having now reached its 2018 high, with no other technical indicators pointing to recovery, a move towards 2015 lows now appears likely.

The top 10 performers of the Liv-ex 100 saw minimal trade over April. While offer prices have increased, they have not been matched by bids.

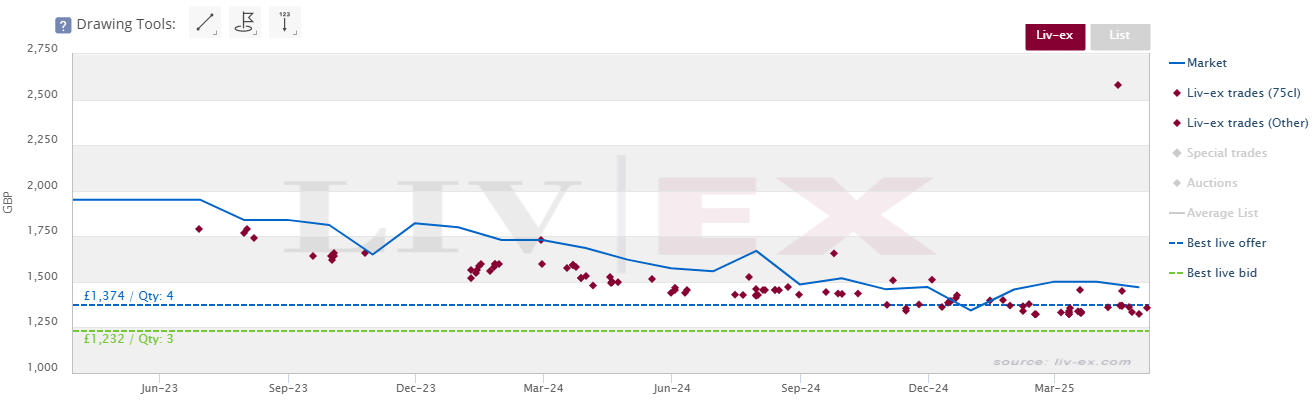

Despite the Champagne 50’s sharp downturn, Bollinger R.D. 2008 and Pol Roger, Sir Winston Churchill 2015 came in as the 14th and 15th best performers of the Fine Wine 100. Their Mid Price increases were modest (2.1% and 2.0% respectively), but trades over the month were consistently in line with these increases. Winston Churchill 2015 appears to be stabilising around £1,370 per 12×75.

Pol Roger, Sir Winston Churchill 2015

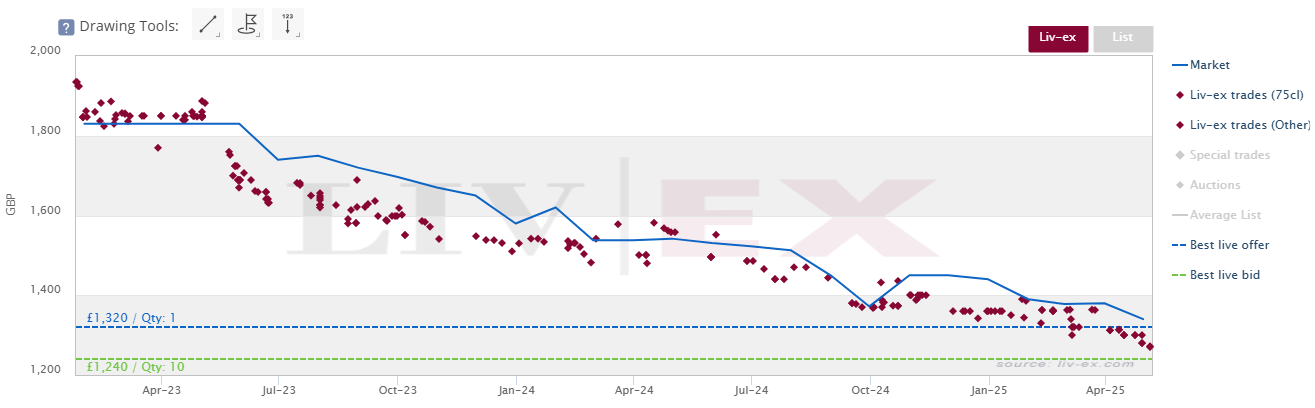

On the other hand, Dom Perignon 2013 – the top-traded wine of the Liv-ex 100 wine by both volume and frequency in April – recorded a price decrease of 3.7%. It now comes in as one of the least expensive vintages offered on the market.

Liv-ex trades of Dom Perignon 2013

Bordeaux 500’s sub-indices

With the 2024 En Primeur campaign well underway, Bordeaux has been in the spotlight, with a particular focus on its pricing. All of the Bordeaux 500’s sub-indices, except for the Sauternes 50 and Second Wine 50, saw declines. It may not yet be time, however, to bet on an imminent recovery for these two exceptions. The Second Wine 50 and Sauternes 50 saw 67.4% and 54.5% less trade (by volume) in April than in March.

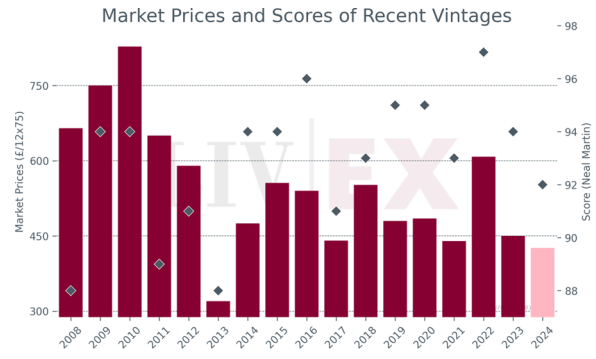

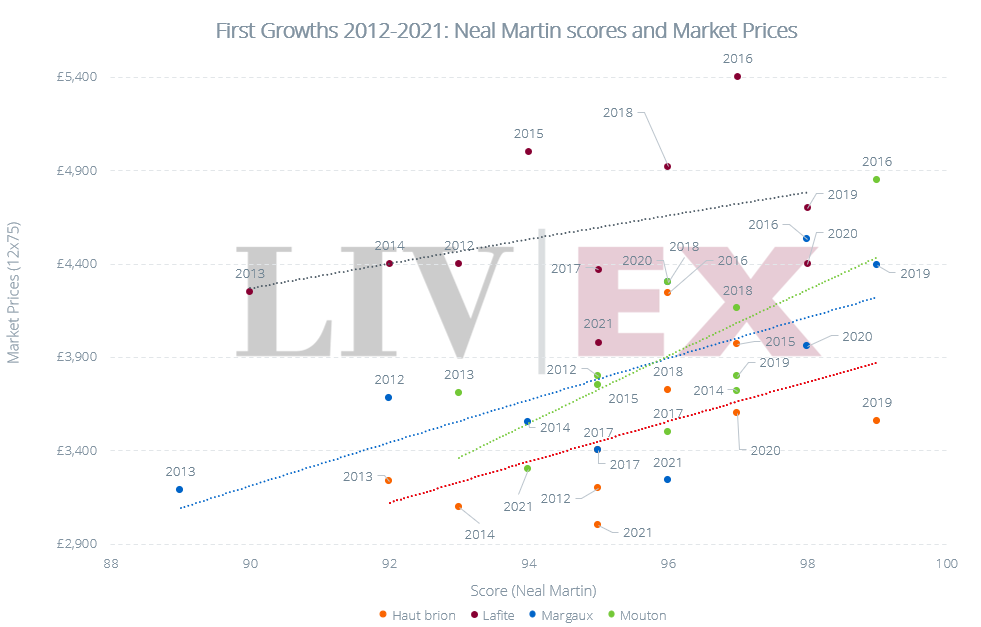

Considering the Fine Wine 50, on average, the 2014 and 2016 vintages have seen the harshest declines (3.9% and 3.8%). In the graph below (first published in March), we can see that the 2016 vintages sit well above the theoretical averages for their scores for each of the First Growths. The 2014s, while generally falling on or below their theoretical averages, received lower ratings, and saw price increases after optimistic re-scorings last year.

Private collectors have grown increasingly tired of Bordeaux price inflation. With the 2016s and 2014s in abundance on the market, buyers are standing their ground – even excellent wines must be well-priced, and if the quality is lacking, buyers are doubly reticent. The 2021s, in most cases priced lower than even the worse-quality 2013s, fared the best of the Fine Wine 50 in April – down, on average, by only 0.3% month-on-month. Their prices may be representative of the kind of price-to-quality ratio today’s buyers are willing to accept.

Left Bank 200 fares better

The Left Bank 200 performed well relative to the market (down 0.6%). Moreover, its performance was backed by a trade volume increase of 28.6% between March and April. Given a 25.4% decline in overall traded volumes (the combined effect of tariffs, Easter holidays and En Primeur), this is no small feat. As with the Fine Wine 1000’s success relative to the Fine Wine 100, this may represent an growing tendency of buyers to cast a broader net, to seek out quality at the expense of brand names. Again mirroring the Fine Wine 1000, it appears the Left Bank 200 may not have much further to fall. The index’s decline is slowing as it approaches its 2020 lows.

Is there a silver lining?

These declines are not exactly promising. But, prices will have to fall for the market to reset and reach a new equilibrium – one that factors in the added costs of tariffs, alongside global economic uncertainties. While not comfortable, sharp price decreases will allow for the market to reach this point faster.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real-time activity of Liv-ex’s 620+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £140m of bids and offers across 20,000 wines.