Author: Grace Geldard

Liv-ex H1 2026 Wine Market Report

The Liv-ex H1 2026 Wine Market Report reveals signs that the fine wine market is stabilising.

The topics covered in the report:

- US Buyers Account for More Than a Quarter of Purchase Value in Q2

- Older Bordeaux Finds Firmer Footing

- Outlook Improves as Price Stability Returns

Liv-ex is the exchange for fine wine, market data and insight. Membership brings wine professionals independent market data and insights and the ability to price, buy and sell wines through one point of contact.

Download the Report

Author: Grace Geldard

Liv-ex En Primeur Closing Report 2025

The Liv-ex En Primeur Closing Report looks back on the campaign and how it unfolded. En Primeur 2025 may well be better than we think.

The topics covered in the report:

- The backdrop and reception: The 2025s received very solid scores, generally ranking amongst the best of the past decade

- History repeats itself: En Primeur 2014, in many ways, lends itself to comparison with 2025.

- Best value releases

Missed the Liv-ex En Primeur Opening Report? Download your copy here.

Liv-ex is the exchange for fine wine, market data and insight. Membership brings wine professionals independent market data and insights and the ability to price, buy and sell wines through one point of contact.

Download the Report

Author: Grace Geldard

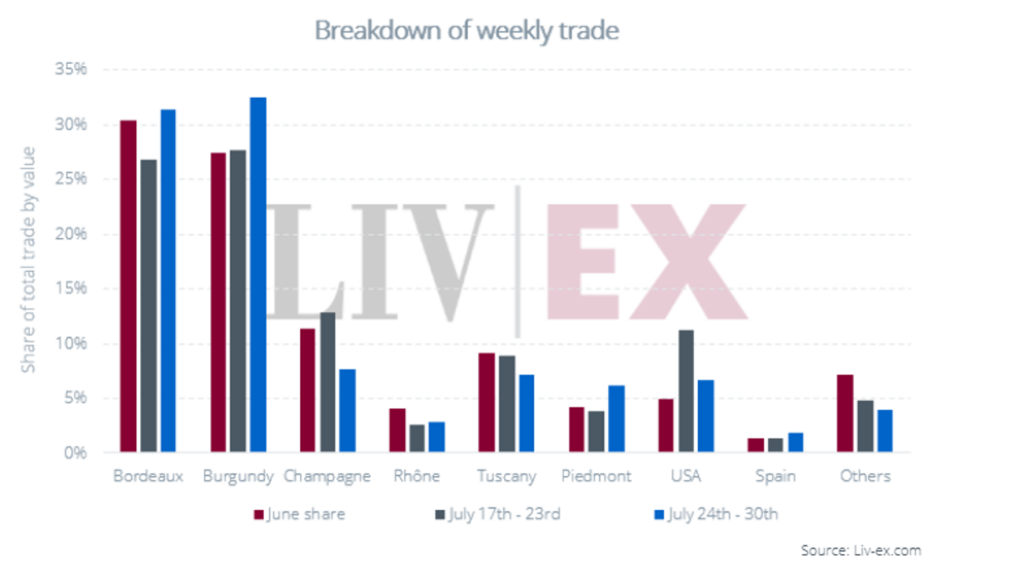

What Happened In Fine Wine This Week: Burgundy retains top spot as summer trading slows

Trading remained focused on a relatively narrow group of blue-chip producers and proven vintages, with Burgundy continuing to attract the greatest concentration of buyer interest…

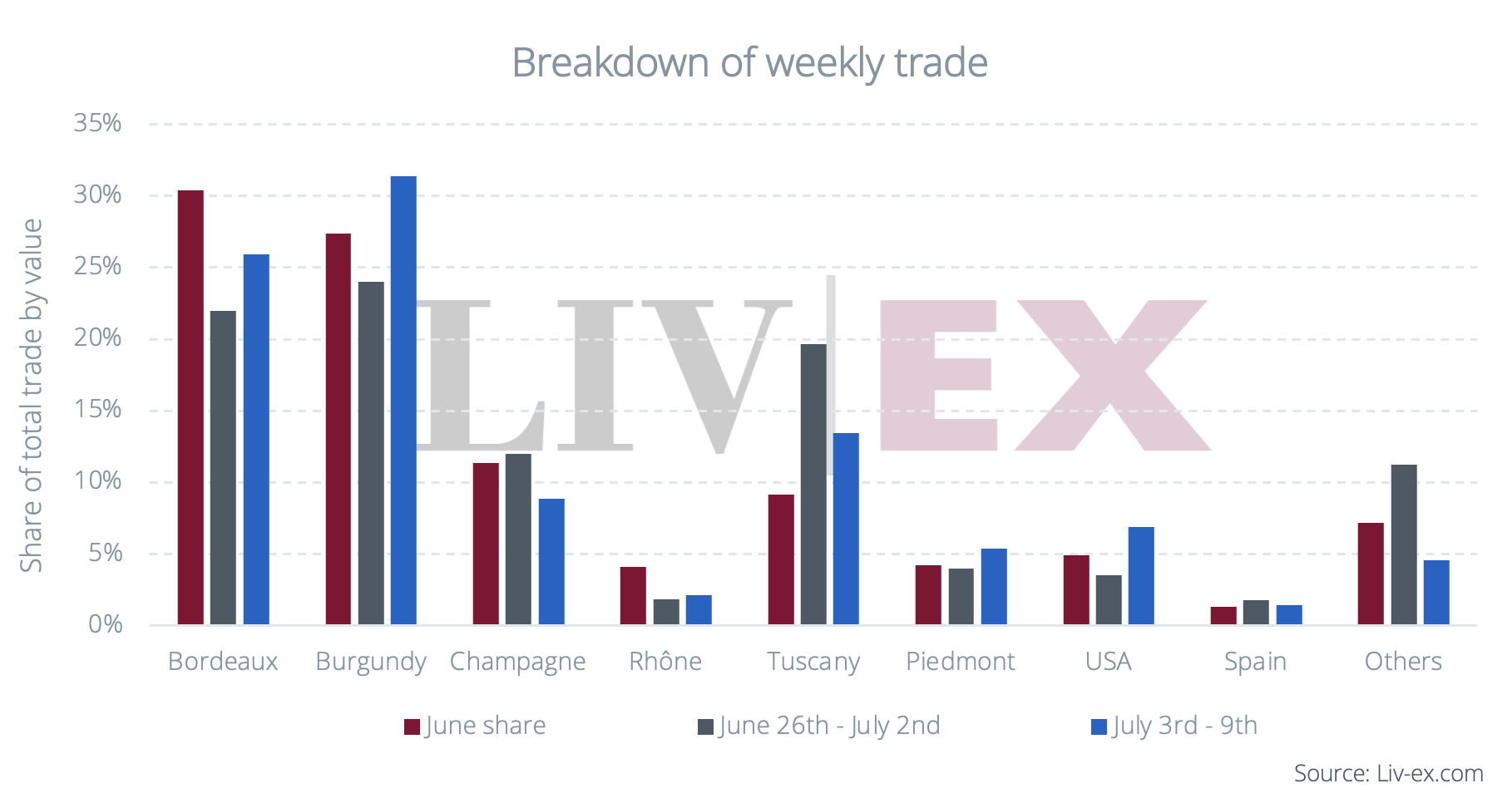

Burgundy remained the dominant force in the secondary market this week, accounting for 32.5% of traded value as seasonal trading volumes eased during the summer period.

The region’s leading producers, Leroy, Comtes Georges de Vogüé and Domaine de la Romanée-Conti (DRC), collectively represented around 10% of total market turnover, underlining continued demand for the category’s most sought-after names.

Bordeaux followed as the second most-traded region, driven by activity in established vintages. The 2005, 2015 and 2009 harvests attracted the greatest share of value traded, highlighting ongoing buyer preference for mature and highly rated wines.

At an individual wine level, Château Margaux 2005 emerged as the week’s most-traded wine by value, changing hands at £5,950 per 12x75cl case.

Asian buying activity rebounds

After a quieter showing the previous week, Asian buyers increased their purchasing activity, with demand concentrated around Burgundy. Roumier, Domaine des Lambrays and Arnoux-Lachaux were the region’s most-purchased producers by value among buyers in the region.

Champagne, meanwhile, ceded some ground. Its share of trade fell from 12.8% last week to 7.6% this week, although buying demand remained geographically diverse, split relatively evenly between the UK, the US and Asia. Asian buyers showed a particular preference for Jacques Selosse and Rare Champagne.

Italy supported by Piedmont

Activity in Italy was led by Piedmont rather than Tuscany, helping maintain the country’s share of market turnover. Giacomo Conterno was Italy’s most-traded producer by value, with Monfortino Riserva 2019 ranking among the five most-traded wines of the week.

In contrast, the United States saw its share of trade fall from 11.2% to 6.7%. Sine Qua Non and Opus One led activity within the category, while Screaming Eagle completed the top three US producers by value traded.

While overall market activity reflected the usual summer slowdown, trading remained focused on a relatively narrow group of blue-chip producers and proven vintages, with Burgundy continuing to attract the greatest concentration of buyer interest.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Author: Grace Geldard

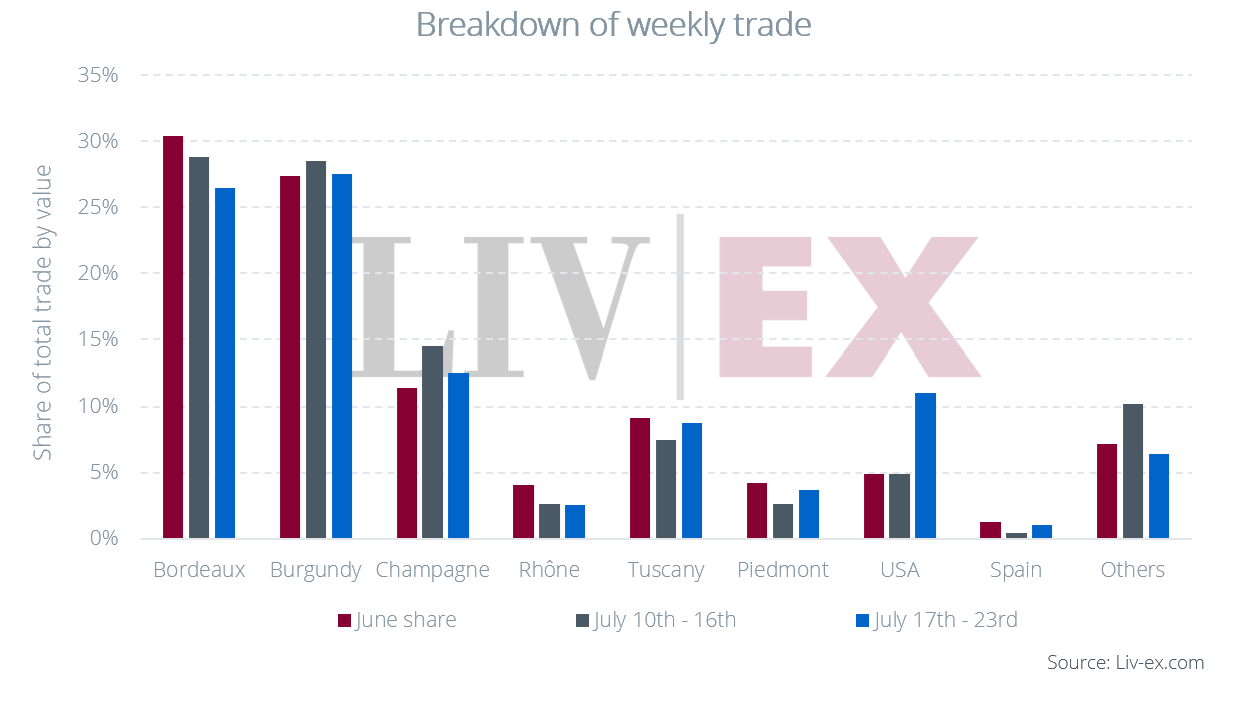

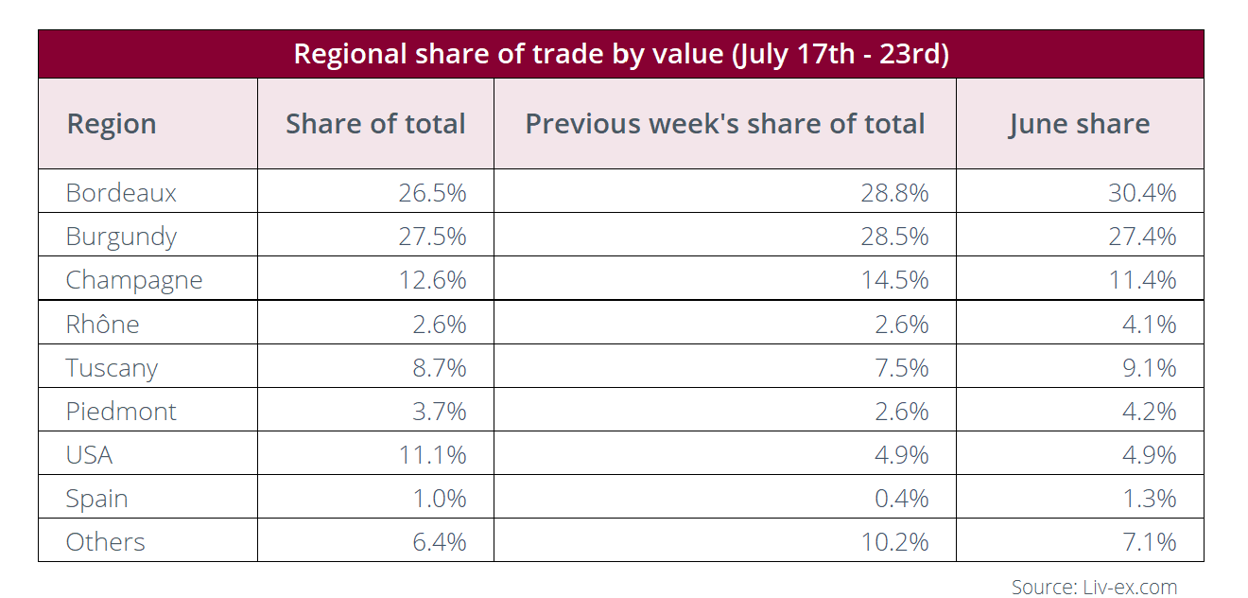

What Happened In Fine Wine This Week: Burgundy leads as Haut-Brion 2005 and 2010 trade at key support levels

Burgundy is back on top. Accounting for 27.5% of traded value this week, it surpassed Bordeaux to lead the fine wine market. Read the latest…

Burgundy edges ahead of Bordeaux

Burgundy reclaimed the top spot in the fine wine market this week, accounting for 27.5% of traded value and overtaking Bordeaux. Burgundy’s strong performance was driven by demand for high value, rare wines. Producers such as Domaine d’Auvenay and Leroy were particularly active, highlighting continued appetite for the region’s sought-after labels despite broader market caution.

Bordeaux remained close behind and was led by Château Haut-Brion. The estate’s 2005 and 2010 vintages featured among the market’s top-traded wines by value, highlighting demand for two of Bordeaux’s most highly regarded modern vintages.

Champagne slips, but buyer demand remains focused

Champagne accounted for 12.6% of traded value, down from 14.5% the previous week. US buyers were the dominant force in the region, responsible for 40% of Champagne trade by value.

Their activity centred on Bollinger, while European buyers favoured Jacques Selosse, highlighting differing Champagne preferences across buyer groups.

Italy gains momentum

Italian wines returned to prominence after a quieter period, with Tuscany and Piedmont together representing 12.0% of traded value.

While Sassicaia remained Tuscany’s most-traded wine by value, Brunello producers such as Biondi-Santi and Marroneto were particularly active. The shift suggests buyers are broadening their focus beyond Italy’s most established Super Tuscans towards other benchmark names in the category.

US record strong week

The United States was another notable mover. Its share of traded value more than doubled, rising from 4.9% last week to 11.1%.

Sine Qua Non emerged as the region’s leading traded producer, with demand coming from both European and Asian buyers. The performance highlights the increasingly global appeal of top-tier US fine wines as collectors continue to diversify beyond traditional European regions.

Market takeaway

This week’s trading highlighted continued demand for the market’s most established names. Burgundy reclaimed the top spot, driven by rare producers such as Domaine d’Auvenay and Leroy, while Château Haut-Brion’s 2005 and 2010 vintages featured among the week’s most-traded wines. In Italy, activity broadened beyond Sassicaia towards Brunello producers, while Champagne buying remained concentrated around leading names such as Bollinger and Jacques Selosse. Together, these trends suggest buyers remain selective, favouring proven producers and sought-after vintages in a cautious market.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Author: Grace Geldard

How a Japanese Wine Merchant Expanded Global Wine Sourcing Through One Fine Wine Trading Platform

Facing rising prices and limited supply, a Japanese wine wholesaler used Liv-ex to access global suppliers, streamline sourcing, and buy with greater confidence.

A Japanese fine wine wholesaler sources fine wines from suppliers across Europe and the United States, distributing them to retailers throughout Japan.

As demand grew, securing sufficient inventory through existing supplier relationships became increasingly challenging. Rising fine wine prices added further pressure, making it harder to source stock competitively while protecting margins.

To support continued growth, the business needed access to a broader fine wine market, enabling it to source competitively priced stock from a global network of suppliers while maintaining confidence in the provenance, condition and authenticity of every purchase.

Accessing a Global Network of Suppliers

The Liv-ex Exchange, a global wine trading platform, gives the business access to a global network of 500+ wine businesses through a single point of contact. Using Liv-ex, the team can:

- Discover new sourcing opportunities beyond existing suppliers

- Compare wine pricing easily across global markets and quickly identify stock that meets target margins

- Buy and sell efficiently through one trusted intermediary

Rather than relying solely on a limited network of regular suppliers, the business can access a broader fine wine market, uncover new opportunities, and source stock more efficiently. Liv-ex manages the trade, settlement, and logistics from end to end, reducing the operational complexity often associated with international trading.

Buying with Greater Confidence

When sourcing wine internationally, having confidence in the condition and quality of the stock is essential.

Robust wine authentication checks carried out by Liv-ex’s team of experts, together with detailed condition information – including pre-sale condition-check images – give greater transparency when evaluating opportunities.

The team also values the reliability of wines traded under Liv-ex’s Standard in Bond (SIB) contract, which sets clear requirements around condition and packaging. As a result, buyers can purchase from a wider range of international suppliers with confidence that wines will arrive in the expected condition.

The Result

Improved profitability

Greater visibility of market opportunities allows the business to purchase more strategically and better protect margins.

Increased access to inventory

Easy access to a large, global network of suppliers has expanded sourcing options and improved stock availability.

Greater efficiency

Pricing information, wine market data and live bids and offers are available in one place, making it easier to evaluate and compare opportunities. Liv-ex’s analysis tools help the team assess opportunities against market prices, recent trades and their own pricing, quickly identifying opportunities that meet target margins. Access to real-time wine industry data reduces the time and effort required to make purchasing decision.

Although the site is packed with a vast number of listings, once you get the hang of filtering out the wines you're looking for, there's no other platform where you can find products at such competitive prices so efficiently.

More confident buying

Access to reliable condition information gives the team confidence when buying wine from overseas, allowing it to broaden its sourcing strategy without compromising on quality standards.

I'm very satisfied not only with the platform's business efficiency, but also with the high level of reliability regarding the condition of the wines themselves, which allows me to purchase with confidence.

Learn how another Asian Liv-ex member streamlined ABV verification to speed up deliveries and save valuable time here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Author: Grace Geldard

Tom Burchfield: Head of Decision Intelligence

Our Head of Decision Intelligence, Tom Burchfield, discusses how data-driven decision-making can help businesses make better decisions and build a more transparent, efficient fine wine…

The future of the fine wine trade will be shaped not just by relationships and expertise, but by the ability to turn information into insight. Tom Burchfield discusses why a more data-led industry can help businesses make better decisions and create a more transparent, efficient market for all participants.

You were the Head of Market Intelligence, and your role has shifted to Head of Decision Intelligence – what exactly does that mean?

What it doesn’t mean is a shift away from the market, but instead an increased focus on bringing relevant Market Intelligence and, more broadly, data to each of our different customers and users. What is relevant and therefore helpful to one customer might not be so useful to another. We want to help all of our customers make more profitable decisions more efficiently. This move sets us up to be able to do just that (if I do it right!).

How has the role of data in the fine wine trade changed over the last 25 years?

The availability of data has exploded. Via the internet, data feeds and APIs there is now an almost overwhelming amount of data. Whereas 25 years ago the challenge was a lack of data – or the available data was very narrow and was not dynamic – now the challenges are knowing which data to trust and how to make sense of it all. The good news is that as we move further into the AI era, our ability to take that wealth of data, make it understandable, relevant and usable is increasing by the day.

Why do you think fine wine has been slower to adopt data-led decision making than some other markets?

The fine wine market moves at a much slower pace than other markets, having its own natural annual harvest and release rhythm, and is driven by both collectors and investment companies. We still see some buying decisions that the data doesn’t justify – some collectors will buy a wine because they love it, not because it makes complete rational sense. Adoption of data has thus naturally been slower.

But at a business level, we are definitely there now, with third party price, stock availability, critics ratings data amongst others being put at the heart of most fine wine companies’ strategic and tactical decision making.

What is the risk for businesses in fine wine that don’t shift towards a data driven model?

The risks are huge and reach across a business’ operations. A practical example is how different your decisions would have been in late 2022 to mid 2023 if you hadn’t been able to see the turn of the market. Demand had started to falter earlier in 2022, prices were starting to soften. It was a time to reduce risk by cutting buying (eg. Bordeaux EP 2022), liquidating any positions where you could maximise margin, thinking twice about any big investments. It’s just one example where not having access to market data would mean making some very different and potentially damaging decisions.

With the market now showing signs of recovery the same could be true but in reverse, and we are seeing certain merchants looking to buy the dip.

In short by not putting trustworthy data at the heart of your decision making you open yourself to all kinds of risk, including missing out on opportunities, and that’s not just at a fundamental strategic level.

At a more tactical level, not using reliable and dynamic data means you risk selling too low, buying too high, selling the wrong stock, selling the right stock at the wrong time, not giving your customers reliable advice. Each bad decision has a cost, and those costs add up pretty quickly over the course of a year. Conversely each good decision means more profit.

Where do you see the Liv-ex data offering going, what do you hope to bring wine merchants that they can’t access elsewhere?

Trade will always be fundamental to Liv-ex as it is trade that generates data. However, we know that the trade a member does on Liv-ex might account for only 5% of their turnover. Because we sit on the deepest set of transactional fine wine data (which continues to expand), we are best-placed to turn that data into a decision-making system that supports our customers across the other 95% of their business.

In short, we want to have all the data that a fine wine merchant needs presented in a personalised way that fits seamlessly into their day-to-day jobs. For example, we’re currently working with customers to build AI-driven tools to make key parts of their job easier to carry out – watch this space for more news in Q3.

In terms of data collection and generation, this means increasing the breadth and regularity of our mid-prices, expanding the number of publicly available lists we collect, building out supply and demand trends. But then making it easy for our customers to understand and act upon the data that is relevant to them.

Want to see how Liv-ex helps businesses spot market shifts and make more informed decisions? Learn how the Liv-ex Bid:Offer Ratio has historically signalled changes in market direction months in advance in our blog.

Author: Grace Geldard

What Happened In Fine Wine This Week: US buyers take a 41% share of purchase value; Burgundy maintains its lead

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions.

The latest Liv-ex exchange trading data shows US buyers accounted for 41.5% of purchase value this week, reinforcing their growing influence on the fine wine market. As highlighted in recent Liv-ex analysis, American buyers have been returning to the market throughout 2026, and this week their share of purchasing increased further, underlining sustained demand from investors and collectors alike.

Burgundy Leads Trade, DRC Tops Producer Rankings

Burgundy retained its position as the market’s leading region, accounting for 31.4% of trade value this week. Demand remained concentrated on the region’s most sought-after names, with Domaine de la Romanée-Conti (DRC) emerging as the top-traded producer overall, followed by Rousseau. Burgundy’s continued dominance highlights the enduring appeal of its most prestigious wines among global buyers.

Bordeaux’s Share Grows, 2010 Vintage in Focus

Bordeaux’s share of trade rose to 25.9%, although this remained below both the June average of 30.4% and the 2026 average of 31.6%. The standout vintage was 2010, which was the most traded by value during the week. The continued interest in mature, highly regarded vintages demonstrates ongoing demand for established Bordeaux wines with proven track records

Tuscany’s Ongoing Strength

Tuscany posted another strong week, capturing a 13.5% share of trade value. Tenuta San Guido was the region’s leading producer, reflecting continued interest in Italy’s most recognisable fine wine brands. Despite shifting market dynamics, Tuscany continues to attract buyers seeking both quality and diversification within their fine wine portfolios.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Author: Grace Geldard

What Happened In Fine Wine This Week: Trade value rises as each buying geography steps up

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions.

What this week’s wine market news tells us

After a quiet week last week, trade value rose 34.5% as each buying geography stepped up activity. While Burgundy remained the leading region by value traded, activity was spread across the market, with Tuscany, Bordeaux and the Languedoc all recording notable performances.

Tuscany shines as Valdicava tops the trading charts

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions. The region’s activity was driven by a cluster of trades in Valdicava wines, with the Brunello producer finishing as the overall top-traded producer of the week.

The performance highlights the continued prominence of Tuscany in the secondary market, where top producers can generate significant trading activity when multiple vintages and formats come to market.

Burgundy, meanwhile, retained its position as the top-traded region for the second consecutive week. Domaine de la Romanée-Conti led the way, while Coche-Dury ranked as the region’s second most-traded producer. Together, the two names helped Burgundy maintain its lead despite increased competition from other regions.

Bordeaux and the Languedoc make their mark

Bordeaux accounted for 22.0% of total trade value, although trading remained spread across a range of wines and vintages. Among them, 2016 emerged as the most actively traded Bordeaux vintage of the week. With prices continuing to show stability, the vintage remained a key contributor to the region’s share of market activity.

Elsewhere, one of the more notable regional performances came from the Languedoc. Increased trading across multiple vintages of Grange des Pères Rouge and Blanc pushed the region to a 5.5% share of total trade value.

That was enough to place the Languedoc ahead of several established fine wine regions, including the USA, Piedmont, Rhône and Spain. While the market’s largest regions continue to dominate overall trading, the week’s activity demonstrates how demand for a single sought-after producer can have a meaningful impact on regional trade patterns.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Author: Grace Geldard

Sophia Gilmour, Market Analyst: Reflections on En Primeur 2025

Sophia Gilmour, Market Analyst, shares her reflections from her time on the ground in Bordeaux, along with her key takeaways from the 2026 En Primeur…

An outstanding vintage in an uneasy year

Before heading to En Primeur this year, I was warned by colleagues who’d attended previous tasting weeks in Bordeaux to not expect to enjoy barrel samples. The wines, they said, would be too intense, too acidic, too tannic or not yet developed enough to give any pleasure. And I admit, stepping off the plane at 10am and driving straight to a Hangar for my first 40 wines was challenging. But they were not quite as unwieldly as I’d been told to expect; many wines that we tasted over the following days were generous, some borderline approachable. Though I’m far better placed to discuss the subsequent release pricing of these wines than their quality, I was not alone in my glowing overall assessment – the 2025 vintage, on the whole, has been near-unanimously declared by critics outstanding.

While there was little contention on quality, the mood in Bordeaux couldn’t quite have been described as jubilant. Even tasting delicious wine, it is not easy to be entirely upbeat as one stands surrounded by leaning towers of unsold cases of wine. It is no secret that the supply chain has been struggling. There was recognition – whether said aloud or not – that getting this years releases right could be make or break. In the words of one winemaker ‘I know, I know. Either I price low and upset the directors or I price high and kill En Primeur’.

It seems that over the past two decades, Bordeaux has found itself at more critical junctures, inflection points and pivotal moments than ought to be possible. What set this year’s apart from the rest was the wake of the 2024 campaign — a vintage that had brought into harsh reality the possibility that, unless private clients could be clawed back, long-standing supply chain relationships alone might fail to keep En Primeur alive.

Last year, following successive vintages of unrealistic pricing and deep into the decline of the broader market, it was not just private clients, but merchants and negociants that found themselves either unable or unwilling to take on stock of the (poorly rated but sometimes aptly priced) 2024s. Without sufficient demand from the rightly-dubious collector, there was neither warehouse space nor cash available to buy what could not be sold.

The campaign commences

Though I do love the excitement of En Primeur and relish in analysing releases, I am not exactly a morning person. But, if I am to be arriving to an empty office at 7am for six weeks straight, I’d at least like to be sharing exciting news. In the early days of the campaign, there were several such occasions. Batailley, Larcis Ducasse, Cheval Blanc and (once Kelley’s potential 100 point score had been released) Pontet-Canet were amongst the early successes.

Then came Lafite. Having come down significantly in 2024, they were able to raise the price by 15% year-on-year while keeping the 2025 the cheapest of similarly rated vintages on the market. The pricing was smart – it clearly drew on current Market Prices rather than release prices of back vintages. They also leveraged the supply-side. While not a popular decision amongst merchants who’d had their allocations squeezed, and possibly unsustainable in the long-run, this move did create an air of scarcity.

Unfortunately, ‘15%’ caught on. Where wines did not provide clear value, they did not sell. In most of these cases, the similarly or better rated 2019 or 2020 vintages came out on top. There were notable releases that bucked this trend, Gruaud Larose and Clinet worthy of mention.

The campaign lost steam after Vinexpo, though the strong releases from Leoville Las Cases and Montrose did inject some life into its final days.

EP sales

In general, Liv-ex members were disappointed with their sales over the course of this campaign. Of UK merchants we surveyed, sales this year were flat on last year by value. The majority of merchants we spoke to thought release prices were too high to overcome this year’s hurdles. There were others, however, who were genuinely surprised by the lack of demand, deeming these releases fair.

Conversations were dominated by complaints, but there were few who did not name at least a couple successes.

Lessons from the 2014 vintage

Take a moment to consider post-campaign coverage of the worse-rated 2014s, a vintage that is now regularly touted as the last well priced En Primeur:

Those who’ve been following this year’s coverage will no doubt feel a sense of Déjà vu. I’d draw attention to some other similarities between the 2014 and 2025 campaigns:

- Released after years of ambitious pricing (2009, 2010; 2021, 2022).

- Directly following a low yielding, poor quality vintage (2013; 2024).

- Released into stabilising markets.

While, at the time, there was discontent with 2014 pricing, they have fared well in the longer run. If we were to ask now if the 2014s were correctly priced, if with perfect hindsight one would have bought at those prices, many would say yes. With the Bordeaux market showing signs of stability, there is finally also reason to believe that, in two years time, when the 2025s reach shores, alternative vintages won’t be cheaper than they are now.

What now?

In short, this was not a knock-out campaign, but neither have those of the past that we now look fondly back on been either. This was perhaps not the make or break campaign we expected it to be, but one of okay prices and tepid sales. There remain reparations to be made to piqued En Primeur buyers of the past, but the 2025 vintage was not the death of En Primeur. I may have many more early wake ups ahead of me yet.