Tag: Market Intelligence

Haut-Brion 1989 claims 1st place; US share of buying climbs to 30%

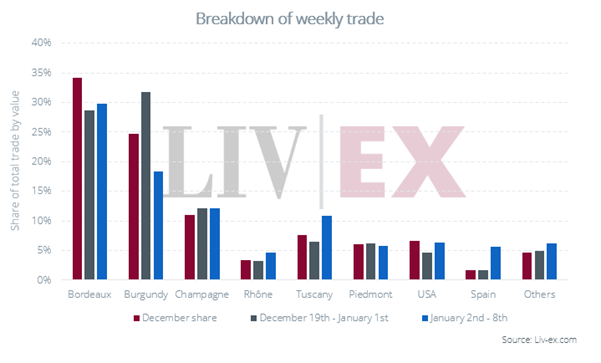

Bordeaux led the market this week, while Burgundy claimed the top spot over the festive period.

The latest Talking Trade is now live!

- Bordeaux led the market this week, while Burgundy claimed the top spot over the festive period.

- Haut-Brion 1989, Unico 2015 and Petrus 2021 were the top-traded wines of the week by value.

- US buying has held steady at 30% over the past three weeks, though trade levels (as expected) have dipped overall.

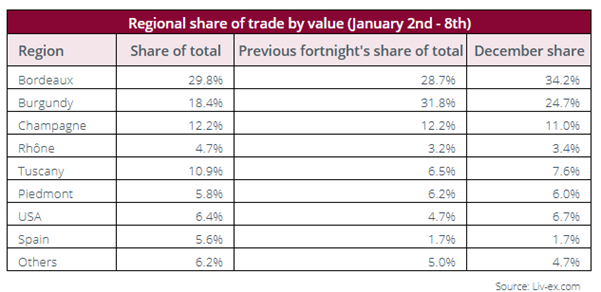

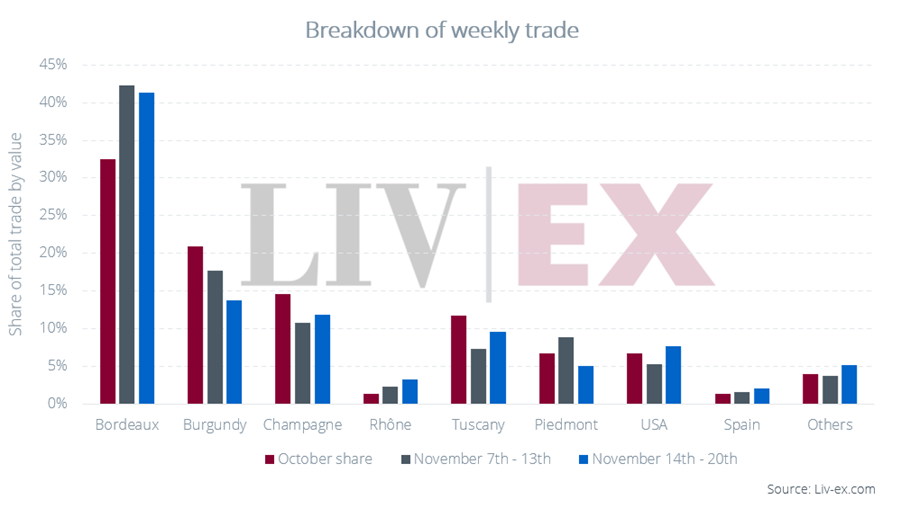

Bordeaux led the market this week with a 29.8% share of traded value. The 2019 and 2021 vintages were the top-traded by value.

Burgundy followed with an 18.4% share, down on its strong performance over the Christmas period. Clos de Tart 2016 was the top-traded wine by value, coming in fifth place overall.

Champagne came in third place, claiming 12.2% of traded value. While the 2015 vintage was the top-traded by value, 2008s changed hands most frequently. Dom Perignon dominated, though Louis Roederer and Krug also took substantial shares.

The Rhone took a 4.7% share, up from December’s 3.4%. While Rayas has been leading the Rhone 100’s recent upward price movement, E. Guigal was the top-traded producer this week, accounting for a third of its trade.

Both Tuscany and Piedmont had strong weeks, though the former dominated with a 10.9% share of overall trade value, San Guido and Masseto claiming the top positions.

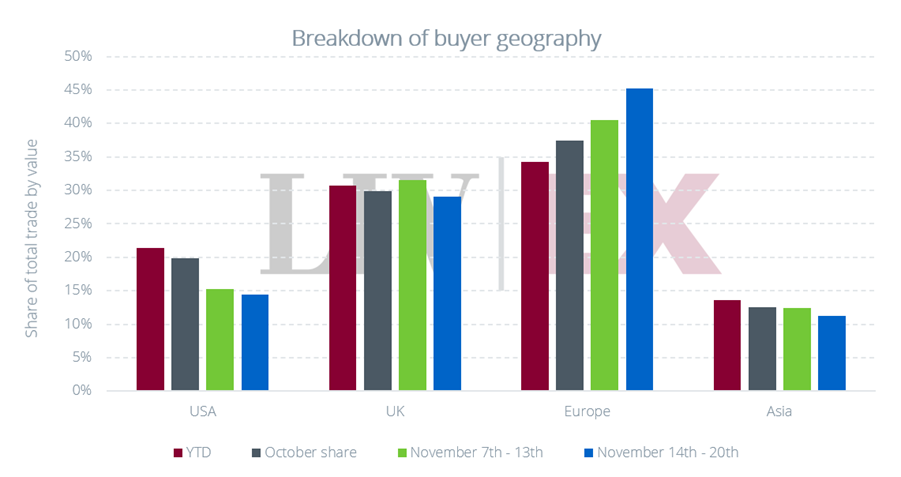

US wines performed relatively well, claiming a 6.4% market share. UK buyers led, taking over half of traded value.

Thanks to Vega Sicilia, making up 60% of trade, Spain’s share rose to 5.5%. Alongside trades of recent vintage Unico, Valbuena and Alion, a magnum of 1962 Unico – still within its drinking window — also changed hands.

Tag: Market Intelligence

Talking Trade 12th December: Bordeaux continues to dominate, Cos d’Estournel 21 in the lead

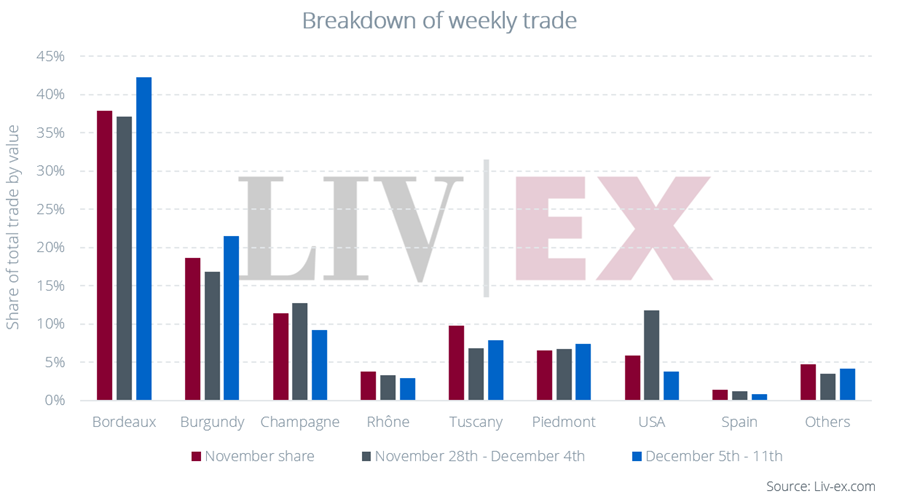

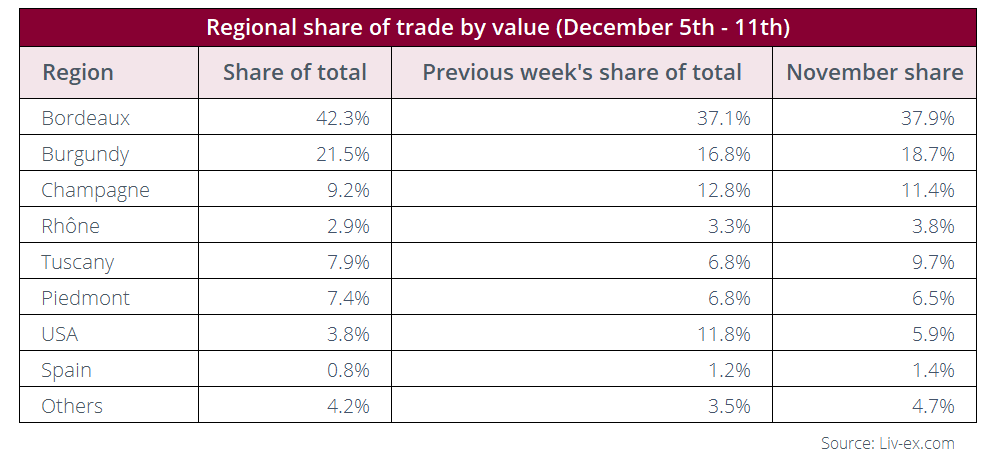

Bordeaux took a strong lead of the market with 42.3% share of the market, up from 37.1% last week. 2019s, 2021s and 2020s proved the…

The latest Talking Trade is now live!

- Bordeaux led the market with a 42.3% share of traded value. Burgundy followed with 21.5%.

- Cos d’Estournel 2021, Chateau Lafite Rothschild 2020 and Le Pin 2015 were the top-traded wines by value.

- Asian buyers pulled ahead of US buyers with a 19.7% and 14.5% share of purchasing respectively.

Bordeaux took a strong lead of the market with 42.3% share of the market, up from 37.1% last week. 2019s, 2021s and 2020s proved the top-traded vintages by value. Chateau Lafite Rothschild, Cos d’Estournel and Le Pin were the region’s top-traded producers.

Burgundy’s share of trade also rose, up from 16.8% last week to 21.5% this week, the 2022 and 2019 vintages changing hands most frequently.

Champagne’s share fell to 9.2%. Cristal and Dom Perignon dominated, together accounting for c.30% of the region’s trade.

Tuscany and Piedmont both increased their share of the market slightly, the latter region taking the edge over the former (7.4% vs. 7.5%). Giacomo Conterno and San Guido were Italy’s top-traded producers by value.

Following a strong close last week, the US’s share of trade fell substantially to 3.8%. Opus One continued to trade actively, accounting for 30% of the region’s trade, purchasing driven largely by US buyers.

Tag: Market Intelligence

Talking Trade 5th December: Petrus the top-traded producer as Champagne trade picks up

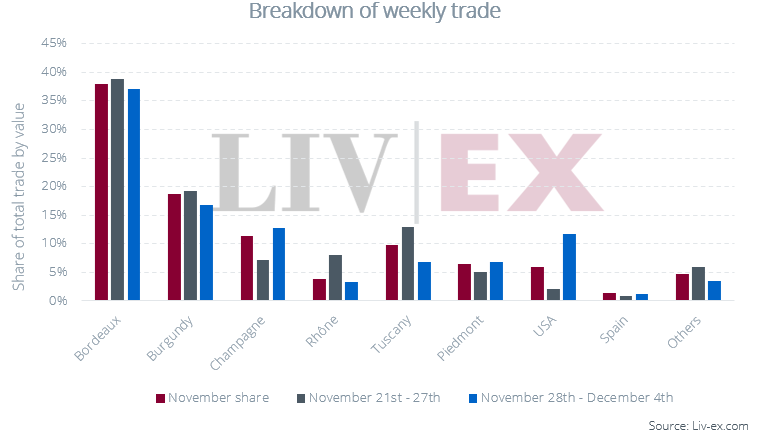

Bordeaux continued to take a higher share of trade value this week (38.9%). Château Mouton Rothschild was the region’s top-traded producer

The latest Talking Trade is now live!

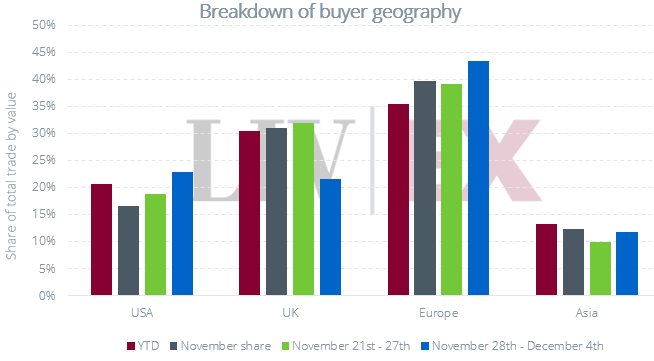

- European buyers accounted for 43.4% of trade

- Increased Opus One trade helps US wine to its largest share of trade in recent months

4,354.0 per bottle).

Breakdown of regional trade

Champagne and the USA both had stronger weeks. Taittinger, Comtes de Champagne Blanc de Blancs sold in good volume across the 2014 and 2013 vintages. While Champagne trade beyond that was relatively muted, the region took a 12.8% share of trade value, up from 7.8% last week and just above the November average (11.4%).

Opus One was the USA’s top-traded producer, with the 2021 vintage trading in decent volume at £2,740 / $3,664, equivalent to € 261.4 per bottle. The USA took an 11.8% share of trade value, compared to 2.1% last week and a November average of 5.9%.

Bordeaux took a 37.1% share. Petrus was the region’s top-traded producer, with the 2009 and 2015 among the week’s overall top-traded wines.

Breakdown of buyer geography

Tag: Market Intelligence

Talking Trade 28th November: Bordeaux maintains a healthy advantage with Mouton Rothschild the top-traded producer

Bordeaux continued to take a higher share of trade value this week (38.9%). Château Mouton Rothschild was the region’s top-traded producer

The latest Talking Trade is now live!

- Bordeaux continues to stretch ahead, taking 38.9% of trade value

- Bouchard La Romanée 2001 was the top-traded wine by value

- With Liv-ex indices due to be published next week, the Fine Wine 50 is currently up 2.0% month-on-month

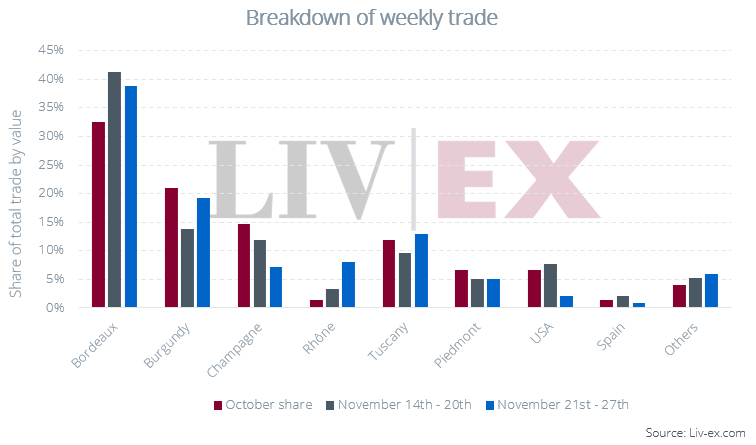

Bordeaux continued to take a higher share of trade value this week (38.9%). Château Mouton Rothschild was the region’s top-traded producer, while Petrus 2022 was the region’s top traded wine, last changing hands at £45,912 / $60,516 per 12×75 (€4,354.0 per bottle).

Burgundy’s share of trade ticked back up (19.2%), with US buyers focusing their attention on the region. 27.5% of US purchases were for Burgundy (the highest of any wine region), with high value d’Auvenay trades coming from US buyers.

With the news of Château Rayas’ Emmanuel Reynaud passing this week, the Rhône took its largest share of trade value in recent memory (8.0%), in the process leapfrogging Champagne which had a quiet week. Multiple vintages of Rayas and Fonsalette traded, accounting for 75% of all Rhône trade.

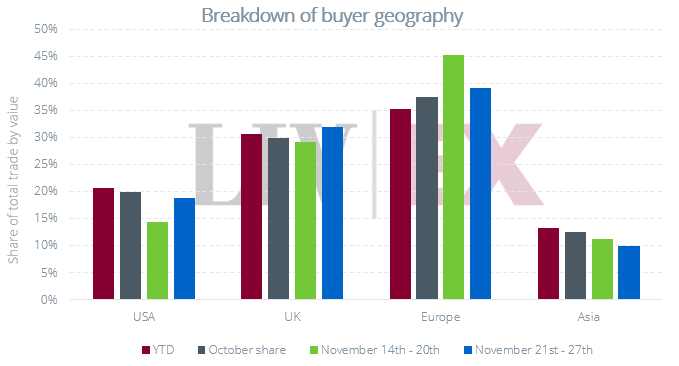

Breakdown of buyer geography

Tag: Market Intelligence

Talking Trade 21st of November: Bordeaux dominates with Petrus top-traded overall

Bordeaux led the market, claiming 42% of traded value and comprising four of the week’s top five wines.

The latest Talking Trade is now live!

- Bordeaux led the market, claiming 42% of traded value and comprising four of the week’s top five wines.

- Dom Perignon Rose 2009 was the top-traded wine by value, while Giscours 2022 (Wine Spectator’s new ‘Wine of the Year’) was the top-traded by volume.

Bordeaux retained its higher share of the market, taking 41.5% of traded value. The 2022s led the charge, with Giscours in the top position. Petrus saw substantial trade across vintages, coming in as the top-traded wine overall. While buyers hailed from the UK, Asia and Europe, the former two regions accounted for the bulk of purchasing. Burgundy’s share of trade fell from 17.7% last week to 13.8% this week.

Domaine de la Romanee-Conti was the top traded producer, accounting for almost a third of the region’s traded value. Though Dom Perignon Rose 2009 was the top-traded wine of the week by value, Champagne’s share of trade remained well below its October average (11.9% vs. 14.6%). Still, this marks an improvement on last week’s 10.8% share. Alongside Dom Perignon, Louis Roederer and Jacques Selosse also took substantial (10%+) shares of the region’s trade.

The Rhone’s standing continued to improve, up from 2.3% last week to 3.3% this week. Rayas accounted for 40% of traded value, with demand driven by UK buyers.

Tuscany again fell short of its October share of 11.8%, accounting for 9.6% of traded value this week. San Guido and Masseto remained strong, each taking just under a quarter of the region’s trade.

Piedmont took 5.1% of trade, down from a strong close at 8.9% last week. While Giacomo Conterno’s Monfortino Riserva 2019 fell out of the overall top five, it remained by far the region’s top traded wine by value. By volume, Produttori del Barbaresco’s 2021 Barbaresco came in first place. The US’s share of trade rose from 5.3% last week to 7.7% this week. Promontory and Harlan Estate led the charge, together accounting for 40% of Californian trade.

Breakdown of buyer geography

Tag: Market Intelligence

En Primeur Reflections from Tom Burchfield, Head of Market Intelligence

Tom talks to us about his experience of attending En Primeur; the Chateau he visited, the wines he tasted, and his expectations of pricing to…

En Primeur Reflections from Tom Burchfield, Head of Market Intelligence

Along with most of the UK trade, we boarded the first Easy Jet flight from Gatwick to Bordeaux on Sunday morning. Bleary-eyed, I travelled with our CEO James Miles, Chief Commercial Officer Anthony Maxwell, and our Broker for Europe, Paolo-Luca Rossi. There was a sense of nervous anticipation. Rumours had it that the wines in Bordeaux had turned out better than expected. Word on the street was that producers were ready to face the current market state. We would see…

We headed straight to the Ballande & Meneret tasting. A huge warehouse, almost devoid of human life greeted us. Stacks of 2021s lined the tasting space, hoping for another day in the sun. We tasted c.50 wines, organised by appellation, and mostly towards the lower end of the price scale. I tasted quite a lot of green and unripe tannins. There were a few successes (Rauzan-Segla was a team favourite), but we left fearing that this year may not be the turning point we’d hoped for. After a streak of bad vintages, and a tough growing season, we wondered what the rest of En Primeur week would bring?

Day two began with a trip up the Left Bank to Saint-Estephe, starting with Montrose. After the mixed bag at Ballande, Montrose lifted our spirits – it was a very delicious wine. A quick hop skip and a jump over to Calon where we had a chance to chat with the team around the vintage, the market, and their plans.

In advance of tasting week, the Liv-ex Market Intelligence team (Market Analyst Sophia Gilmour, Data Analyst Alex Chisholm and I) had published our En Primeur book. We included an opening ‘state of the Bordeaux market’ report and individual analyses on each major wine. I brought a copy of the book along to Bordeaux, with individual printouts of the wine analyses, which I offered to each producer we met.

When we showed the data, the response was generally consistent insofar as there really did appear to be a willingness to support the campaign (this gave me a boost). There was also talk about reducing the number of negociants they worked with. Among other things, we routinely ask:

- How many full-time employees do you have?

- What about producing more grand vin and less of the second and third wines?

- How much is one critics’ point worth to you?

- Will you release at a price that will make the 2024 the cheapest in the market?

In that very charming bordelais manner, our hosts managed to come across as both humble and confident, that the market would come around to their will.

Day three begins with a drive to Libourne for the Moueix tasting, followed by a mind-altering sequence at Le Pin, Lafleur, Petrus, and lunch at Cheval Blanc. Possibly the most fascinating meeting of the trip, the Cheval team appeared committed to releasing the 2024 at a ‘no-brainer’ price. This left us feeling confident that we’d touch down in the UK with a promising En Primeur campaign ahead….

We took the last flight back to London for the Easter break and the anticipation of Pontet-Canet kicking things off next week.

EP campaign – hard work

At Liv-ex, we send our members real-time analysis of each major release. As the campaign began, we hopefully asked each other the same question: ‘Do you think Chateau X will do enough’? The further the campaign went on, the more inevitable the answer became: ‘They’ll get close, but probably not do quite enough’.

En Primeur coverage had been too focused on the percentage increase or decrease from the previous year’s release. While this made for good marketing material and enticing news stories, it is largely insignificant. Moreover, comparing a decade of generally poor release prices to one another makes little sense at all.

The crux of whether a release represented a good buying opportunity was simple and boiled down to one question: Were there less expensive back vintages, of similar or better quality, available on the market?

If the answer was no, then it could have been a ‘buy’. You do need to factor in costs of carry, and with storage currently c.£15 per 12×75 a year, this is not insignificant. .

However, if the answer was yes, then the release could not be considered a no-brainer ‘buy’. If there were multiple better rated and considerably less expensive back vintages available, then it really wasn’t a buy.

Unfortunately, this year’s campaign had few instances where the price and quality presented a better offer than what was already available on the market from previous years. Lafite and Mouton spring to mind, and Carmes Haut-Brion ascent continued. While release price reductions were commendable, there were better alternatives available.

It’s was notable that, according to our members, even when a release appeared a no-brainer buying opportunity, it was often been met by disengaged end consumers. Buyer’s apathy had taken hold, or as one more forthright traditional EP buyer told me: ‘We’ve been ****** for too many years, why buy this middling vintage?’

It was interesting that the frustration with the system had reached a point where participants from across the supply chain were now daring to put their heads above the parapet. As the first releases came out, UK merchants publicly told their customers that they had hoped for better prices. This was quite remarkable. There couldn’t have been many other industries where sales emails told you that the price wasn’t great.

Similar stories emerged from La Place, where negociants had not been shy of showing their dismay at prices they knew wouldn’t sell. Reportedly, the courtiers were also shaking their heads in disbelief.

So what might the future hold?

Before the campaign kicked off, we had thought that the small crop of 2024s represented an opportunity for producers to reset and price at a level that would invigorate the market. There may not have been any price good enough to reinvigorate the market, but now we’ll never know… So what could 2025 hold?

We had to hope that 2025 would be a beautiful and bountiful vintage. One that was cheaper for producers to make, and theoretically gave the trade an easier thing to sell. While still 12 months away, we anticipated that the market could not stomach further price rises. It would have to be priced well below other back vintages. In a falling market, this was no easy feat, and one that might be hard to contemplate. But that’s what needed to be done. If the 2024 campaign had felt like last chance saloon, then for some another misstep might well result in closing time.

Tag: Market Intelligence

UK Wine Show x Liv-ex: Tom Burchfield: Episode 3: The State of the Fine Wine Market

In the final podcast of the three-part series, Tom and Chris talk about wines yet to be discovered by the secondary market

In the final podcast of the three-part series, Tom and Chris talk about wines yet to be discovered by the secondary market, from the likes of Spain and Australia, and Tom talks about his favourite regions for drinking wine.

Listen to the podcast to find out more:

Did you miss the second episode? The previous episode diving into Bordeaux En Primeur. Listen here.

Tag: Market Intelligence

UK Wine Show x Liv-ex: Tom Burchfield: Episode 2: The State of the Fine Wine Market.

In this second of a three-part episode, Tom and Chris pick up where they left off, this time diving deeper into Bordeaux En Primeur. Tom talks about the drop in…

In this second of a three-part episode, Tom and Chris pick up where they left off, this time diving deeper into Bordeaux En Primeur. Tom talks about the drop in En Primeur buying, sharing key stats; in 2009/2010 the UK bought around £240 million En Primeur, last year it was just £60 million.

Understand why in this episode. Listen here.

Did you miss the first episode? The previous dives deeper the sophistication of the fine wine market, Bordeaux pricing and the use of data and technology for decision making in the wine industry. Listen here.

Tag: Market Intelligence

UK Wine Show x Liv-ex: Tom Burchfield: Episode 1 – The Fine Wine Market

Tom Burchfield, Head of Market Intelligence at Liv-ex, joined Chris Scott on the UK Wine Show for the first of a three-part podcast series. In…

Tom Burchfield, Head of Market Intelligence at Liv-ex, joined Chris Scott on the UK Wine Show for the first of a three-part podcast series.

In this opening episode, Tom discusses sophistication of the Fine Wine market, Bordeaux pricing and the use of data and technology for decision making in the wine industry.

Tom kicked things off by outlining the value of Liv-ex for wine businesses, the role of Market Intelligence at Liv-ex, and his plans to bring greater personalisation to the insights his team delivers.

The next episode dives deeper into Bordeaux En Primeur. Listen here.