Resources

How a Japanese Wine Merchant Expanded Global Wine Sourcing Through One Fine Wine Trading Platform

Facing rising prices and limited supply, a Japanese wine wholesaler used Liv-ex to access global suppliers, streamline sourcing, and buy with greater confidence.

A Japanese fine wine wholesaler sources fine wines from suppliers across Europe and the United States, distributing them to retailers throughout Japan.

As demand grew, securing sufficient inventory through existing supplier relationships became increasingly challenging. Rising fine wine prices added further pressure, making it harder to source stock competitively while protecting margins.

To support continued growth, the business needed access to a broader fine wine market, enabling it to source competitively priced stock from a global network of suppliers while maintaining confidence in the provenance, condition and authenticity of every purchase.

Accessing a Global Network of Suppliers

The Liv-ex Exchange, a global wine trading platform, gives the business access to a global network of 500+ wine businesses through a single point of contact. Using Liv-ex, the team can:

- Discover new sourcing opportunities beyond existing suppliers

- Compare wine pricing easily across global markets and quickly identify stock that meets target margins

- Buy and sell efficiently through one trusted intermediary

Rather than relying solely on a limited network of regular suppliers, the business can access a broader fine wine market, uncover new opportunities, and source stock more efficiently. Liv-ex manages the trade, settlement, and logistics from end to end, reducing the operational complexity often associated with international trading.

Buying with Greater Confidence

When sourcing wine internationally, having confidence in the condition and quality of the stock is essential.

Robust wine authentication checks carried out by Liv-ex’s team of experts, together with detailed condition information – including pre-sale condition-check images – give greater transparency when evaluating opportunities.

The team also values the reliability of wines traded under Liv-ex’s Standard in Bond (SIB) contract, which sets clear requirements around condition and packaging. As a result, buyers can purchase from a wider range of international suppliers with confidence that wines will arrive in the expected condition.

Removing the Logistical and Operational Burden

Liv-ex also simplified settlement, handling, and delivery. Wines sourced through the platform are covered by standardised condition contracts (SIB), stored in-bond, and managed by Liv-ex through an end-to-end settlement process.

For Rue Pinard, this meant they could operate internationally without needing to manage logistics, compliance, or physical storage – removing significant barriers to growth.

The Result

Improved profitability

Greater visibility of market opportunities allows the business to purchase more strategically and better protect margins.

Increased access to inventory

Easy access to a large, global network of suppliers has expanded sourcing options and improved stock availability.

Greater efficiency

Pricing information, wine market data and live bids and offers are available in one place, making it easier to evaluate and compare opportunities. Liv-ex’s analysis tools help the team assess opportunities against market prices, recent trades and their own pricing, quickly identifying opportunities that meet target margins. Access to real-time wine industry data reduces the time and effort required to make purchasing decision.

Although the site is packed with a vast number of listings, once you get the hang of filtering out the wines you're looking for, there's no other platform where you can find products at such competitive prices so efficiently.

More confident buying

Access to reliable condition information gives the team confidence when buying wine from overseas, allowing it to broaden its sourcing strategy without compromising on quality standards.

I'm very satisfied not only with the platform's business efficiency, but also with the high level of reliability regarding the condition of the wines themselves, which allows me to purchase with confidence.

Learn how another Asian Liv-ex member streamlined ABV verification to speed up deliveries and save valuable time here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

Tom Burchfield: Head of Decision Intelligence

Our Head of Decision Intelligence, Tom Burchfield, discusses how data-driven decision-making can help businesses make better decisions and build a more transparent, efficient fine wine…

The future of the fine wine trade will be shaped not just by relationships and expertise, but by the ability to turn information into insight. Tom Burchfield discusses why a more data-led industry can help businesses make better decisions and create a more transparent, efficient market for all participants.

You were the Head of Market Intelligence, and your role has shifted to Head of Decision Intelligence – what exactly does that mean?

What it doesn’t mean is a shift away from the market, but instead an increased focus on bringing relevant Market Intelligence and, more broadly, data to each of our different customers and users. What is relevant and therefore helpful to one customer might not be so useful to another. We want to help all of our customers make more profitable decisions more efficiently. This move sets us up to be able to do just that (if I do it right!).

How has the role of data in the fine wine trade changed over the last 25 years?

The availability of data has exploded. Via the internet, data feeds and APIs there is now an almost overwhelming amount of data. Whereas 25 years ago the challenge was a lack of data – or the available data was very narrow and was not dynamic – now the challenges are knowing which data to trust and how to make sense of it all. The good news is that as we move further into the AI era, our ability to take that wealth of data, make it understandable, relevant and usable is increasing by the day.

Why do you think fine wine has been slower to adopt data-led decision making than some other markets?

The fine wine market moves at a much slower pace than other markets, having its own natural annual harvest and release rhythm, and is driven by both collectors and investment companies. We still see some buying decisions that the data doesn’t justify – some collectors will buy a wine because they love it, not because it makes complete rational sense. Adoption of data has thus naturally been slower.

But at a business level, we are definitely there now, with third party price, stock availability, critics ratings data amongst others being put at the heart of most fine wine companies’ strategic and tactical decision making.

What is the risk for businesses in fine wine that don’t shift towards a data driven model?

The risks are huge and reach across a business’ operations. A practical example is how different your decisions would have been in late 2022 to mid 2023 if you hadn’t been able to see the turn of the market. Demand had started to falter earlier in 2022, prices were starting to soften. It was a time to reduce risk by cutting buying (eg. Bordeaux EP 2022), liquidating any positions where you could maximise margin, thinking twice about any big investments. It’s just one example where not having access to market data would mean making some very different and potentially damaging decisions.

With the market now showing signs of recovery the same could be true but in reverse, and we are seeing certain merchants looking to buy the dip.

In short by not putting trustworthy data at the heart of your decision making you open yourself to all kinds of risk, including missing out on opportunities, and that’s not just at a fundamental strategic level.

At a more tactical level, not using reliable and dynamic data means you risk selling too low, buying too high, selling the wrong stock, selling the right stock at the wrong time, not giving your customers reliable advice. Each bad decision has a cost, and those costs add up pretty quickly over the course of a year. Conversely each good decision means more profit.

Where do you see the Liv-ex data offering going, what do you hope to bring wine merchants that they can’t access elsewhere?

Trade will always be fundamental to Liv-ex as it is trade that generates data. However, we know that the trade a member does on Liv-ex might account for only 5% of their turnover. Because we sit on the deepest set of transactional fine wine data (which continues to expand), we are best-placed to turn that data into a decision-making system that supports our customers across the other 95% of their business.

In short, we want to have all the data that a fine wine merchant needs presented in a personalised way that fits seamlessly into their day-to-day jobs. For example, we’re currently working with customers to build AI-driven tools to make key parts of their job easier to carry out – watch this space for more news in Q3.

In terms of data collection and generation, this means increasing the breadth and regularity of our mid-prices, expanding the number of publicly available lists we collect, building out supply and demand trends. But then making it easy for our customers to understand and act upon the data that is relevant to them.

Want to see how Liv-ex helps businesses spot market shifts and make more informed decisions? Learn how the Liv-ex Bid:Offer Ratio has historically signalled changes in market direction months in advance in our blog.

Resources

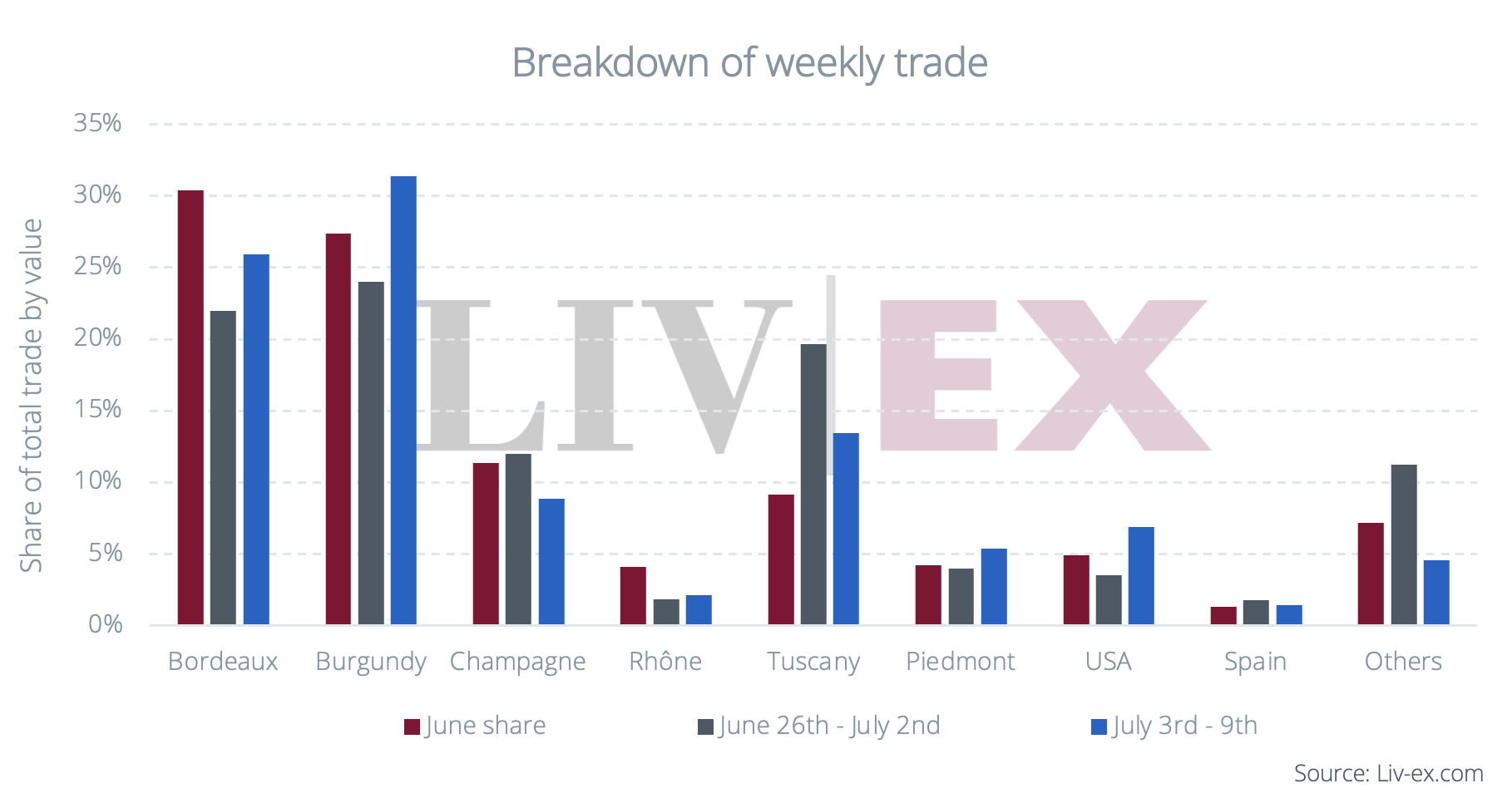

What Happened In Fine Wine This Week: US buyers take a 41% share of purchase value; Burgundy maintains its lead

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions.

The latest Liv-ex exchange trading data shows US buyers accounted for 41.5% of purchase value this week, reinforcing their growing influence on the fine wine market. As highlighted in recent Liv-ex analysis, American buyers have been returning to the market throughout 2026, and this week their share of purchasing increased further, underlining sustained demand from investors and collectors alike.

Burgundy Leads Trade, DRC Tops Producer Rankings

Burgundy retained its position as the market’s leading region, accounting for 31.4% of trade value this week. Demand remained concentrated on the region’s most sought-after names, with Domaine de la Romanée-Conti (DRC) emerging as the top-traded producer overall, followed by Rousseau. Burgundy’s continued dominance highlights the enduring appeal of its most prestigious wines among global buyers.

Bordeaux’s Share Grows, 2010 Vintage in Focus

Bordeaux’s share of trade rose to 25.9%, although this remained below both the June average of 30.4% and the 2026 average of 31.6%. The standout vintage was 2010, which was the most traded by value during the week. The continued interest in mature, highly regarded vintages demonstrates ongoing demand for established Bordeaux wines with proven track records

Tuscany’s Ongoing Strength

Tuscany posted another strong week, capturing a 13.5% share of trade value. Tenuta San Guido was the region’s leading producer, reflecting continued interest in Italy’s most recognisable fine wine brands. Despite shifting market dynamics, Tuscany continues to attract buyers seeking both quality and diversification within their fine wine portfolios.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

What Happened In Fine Wine This Week: Trade value rises as each buying geography steps up

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions.

What this week’s wine market news tells us

After a quiet week last week, trade value rose 34.5% as each buying geography stepped up activity. While Burgundy remained the leading region by value traded, activity was spread across the market, with Tuscany, Bordeaux and the Languedoc all recording notable performances.

Tuscany shines as Valdicava tops the trading charts

Tuscany accounted for 19.7% of total trade value this week, making it one of the market’s strongest-performing regions. The region’s activity was driven by a cluster of trades in Valdicava wines, with the Brunello producer finishing as the overall top-traded producer of the week.

The performance highlights the continued prominence of Tuscany in the secondary market, where top producers can generate significant trading activity when multiple vintages and formats come to market.

Burgundy, meanwhile, retained its position as the top-traded region for the second consecutive week. Domaine de la Romanée-Conti led the way, while Coche-Dury ranked as the region’s second most-traded producer. Together, the two names helped Burgundy maintain its lead despite increased competition from other regions.

Bordeaux and the Languedoc make their mark

Bordeaux accounted for 22.0% of total trade value, although trading remained spread across a range of wines and vintages. Among them, 2016 emerged as the most actively traded Bordeaux vintage of the week. With prices continuing to show stability, the vintage remained a key contributor to the region’s share of market activity.

Elsewhere, one of the more notable regional performances came from the Languedoc. Increased trading across multiple vintages of Grange des Pères Rouge and Blanc pushed the region to a 5.5% share of total trade value.

That was enough to place the Languedoc ahead of several established fine wine regions, including the USA, Piedmont, Rhône and Spain. While the market’s largest regions continue to dominate overall trading, the week’s activity demonstrates how demand for a single sought-after producer can have a meaningful impact on regional trade patterns.

If you missed last week’s post, read here.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

Inside NAWR New York: What’s Changing in US Wine Retail

Robbie Stevens, Head of Broking at Liv-ex presented at NAWR (National Association of Wine Retailers) to discuss where Bordeaux is, and where it’s heading.

NAWR is the National Association of Wine Retailers, and they hold an Annual Summit in the US each year. I’ve now attended and been invited to speak at the last five NAWR summits, and this years event was certainly one of the most memorable – strong attendance, coupled with excellent content, and most importantly, fantastic engagement from the US wine trade. To download Robbie’s presentation slides, please fill out the form here.

Around 100 people were in the room, representing 50 to 60 businesses. As expected, retailers dominated, but there was a mix: logistics providers, lawyers, tech platforms, ERP systems, and press.

For Liv-ex, it was a valuable audience with a mix of members, service providers as well as plenty of new faces.

A recurring theme: the wine industry continues to struggle with data

One of the standout sessions came from Andrew Sussmann, CTO and co-founder of Preferabli. Andrew’s keynote was centred around AI and its adoption within the wine trade. One of his principal points will be familiar to most: the wine industry still struggles with data standardisation -particularly naming conventions.

What was interesting was where the conversation went next.

An audience member asked whether Andrew had heard of LWIN, and asked why the industry hasn’t coalesced around it in the same way publishing settled on ISBN. Sussmann’s response was ‘we love LWIN, it is by far the best standardisation out there and we encourage all our users to adopt it, but coverage remains a constraint.”

It’s always nice to hear other people championing Liv-ex, without the need to weight in.

Regulation, restriction, and the shifting US retail landscape

NAWR’s focus remains consistent: tackling the inefficiencies and barriers created by interstate shipping restrictions and the three-tier system – bureaucratic legislature dating back to the post-prohibiltion era.

If anything, the urgency is increasing.

Alongside structural constraints, US retailers are now dealing with a broader cultural and regulatory shift. The rise of anti-alcohol lobbying continues to gather momentum, with increasingly visible campaigns – particularly in cities like New York. At the same time, changing consumer behaviours, partly influenced by GLP-1 drugs, are seemingly having an impact on demand.

Several retailers reported softness in lower price points, while fine wine remains comparatively resilient.

There’s also growing competition from adjacent categories. CBD drinks, currently operating under a much looser regulatory framework, are expanding quickly, creating an uneven playing field. That said, many expect tighter regulation to follow.

The net effect is a market that is becoming increasingly complex to operate in, particularly for businesses reliant on volume-driven models.

A market adapting to tariffs, and looking to what’s next

The broader mood across the US trade felt cautiously stable.

Tariffs remain in place, but with a big question mark over them. Businesses have largely adapted. Compared to 2024, there’s a sense that operators are finding ways to manage the impact. There is some optimism following the Supreme Court ruling earlier this year declaring certain tariffs illegal, although uncertainty remains around enforcement and refunds. Many also fear that with the liberation day tariffs in question, other tariff triggers such as Digital Services Taxes might resurface; there is also the question of the unresolved Boeing/Airbus dispute.

From a supply perspective, there are early indications the auction market is beginning to recover, suggesting that previously imported European stock has largely worked its way through the system. If sustained, that should be a positive signal for import demand as a gap in the market begins to appear, and then grow.

Bordeaux: a timely conversation

I joined a panel alongside Jeff Zacharia and Pierre Ogden de Rothschild to discuss where Bordeaux is, and where it’s heading.

As we were in the midst of a Bordeaux En Primeur campaign, it was a timely discussion.

For many in the room, this was an opportunity to engage more directly with market data and pricing dynamics. The level of audience participation suggested strong interest – not just in Bordeaux as a category, but in how it’s evolving within a broader global market context.

Encouragingly, the conversation didn’t stop when the panel ended. Over the following 24 hours, there were multiple follow-ups on the topic itself, and on how tools like Liv-ex can help inform decision-making.

To download Robbie’s presentation slides, please fill out the form here.

Lasting Takeaways

What NAWR reinforced is that US wine retail is becoming more nuanced:

- Regulation remains a defining constraint

- Consumer behaviour is shifting at the lower end

- Competition is broadening beyond traditional wine

- Data, and the ability to use it effectively, is increasingly critical

For businesses navigating this, access to accurate pricing, liquidity, and global supply is no longer a nice-to-have – it’s fundamental.

The US remains one of the most dynamic, and complex, wine markets globally. Events like this are a useful reminder that while the challenges are evolving, so too is the industry’s willingness to adapt.

Resources

Sophia Gilmour, Market Analyst: Reflections on En Primeur 2025

Sophia Gilmour, Market Analyst, shares her reflections from her time on the ground in Bordeaux, along with her key takeaways from the 2026 En Primeur…

An outstanding vintage in an uneasy year

Before heading to En Primeur this year, I was warned by colleagues who’d attended previous tasting weeks in Bordeaux to not expect to enjoy barrel samples. The wines, they said, would be too intense, too acidic, too tannic or not yet developed enough to give any pleasure. And I admit, stepping off the plane at 10am and driving straight to a Hangar for my first 40 wines was challenging. But they were not quite as unwieldly as I’d been told to expect; many wines that we tasted over the following days were generous, some borderline approachable. Though I’m far better placed to discuss the subsequent release pricing of these wines than their quality, I was not alone in my glowing overall assessment – the 2025 vintage, on the whole, has been near-unanimously declared by critics outstanding.

While there was little contention on quality, the mood in Bordeaux couldn’t quite have been described as jubilant. Even tasting delicious wine, it is not easy to be entirely upbeat as one stands surrounded by leaning towers of unsold cases of wine. It is no secret that the supply chain has been struggling. There was recognition – whether said aloud or not – that getting this years releases right could be make or break. In the words of one winemaker ‘I know, I know. Either I price low and upset the directors or I price high and kill En Primeur’.

It seems that over the past two decades, Bordeaux has found itself at more critical junctures, inflection points and pivotal moments than ought to be possible. What set this year’s apart from the rest was the wake of the 2024 campaign — a vintage that had brought into harsh reality the possibility that, unless private clients could be clawed back, long-standing supply chain relationships alone might fail to keep En Primeur alive.

Last year, following successive vintages of unrealistic pricing and deep into the decline of the broader market, it was not just private clients, but merchants and negociants that found themselves either unable or unwilling to take on stock of the (poorly rated but sometimes aptly priced) 2024s. Without sufficient demand from the rightly-dubious collector, there was neither warehouse space nor cash available to buy what could not be sold.

The campaign commences

Though I do love the excitement of En Primeur and relish in analysing releases, I am not exactly a morning person. But, if I am to be arriving to an empty office at 7am for six weeks straight, I’d at least like to be sharing exciting news. In the early days of the campaign, there were several such occasions. Batailley, Larcis Ducasse, Cheval Blanc and (once Kelley’s potential 100 point score had been released) Pontet-Canet were amongst the early successes.

Then came Lafite. Having come down significantly in 2024, they were able to raise the price by 15% year-on-year while keeping the 2025 the cheapest of similarly rated vintages on the market. The pricing was smart – it clearly drew on current Market Prices rather than release prices of back vintages. They also leveraged the supply-side. While not a popular decision amongst merchants who’d had their allocations squeezed, and possibly unsustainable in the long-run, this move did create an air of scarcity.

Unfortunately, ‘15%’ caught on. Where wines did not provide clear value, they did not sell. In most of these cases, the similarly or better rated 2019 or 2020 vintages came out on top. There were notable releases that bucked this trend, Gruaud Larose and Clinet worthy of mention.

The campaign lost steam after Vinexpo, though the strong releases from Leoville Las Cases and Montrose did inject some life into its final days.

EP sales

In general, Liv-ex members were disappointed with their sales over the course of this campaign. Of UK merchants we surveyed, sales this year were flat on last year by value. The majority of merchants we spoke to thought release prices were too high to overcome this year’s hurdles. There were others, however, who were genuinely surprised by the lack of demand, deeming these releases fair.

Conversations were dominated by complaints, but there were few who did not name at least a couple successes.

Lessons from the 2014 vintage

Take a moment to consider post-campaign coverage of the worse-rated 2014s, a vintage that is now regularly touted as the last well priced En Primeur:

Those who’ve been following this year’s coverage will no doubt feel a sense of Déjà vu. I’d draw attention to some other similarities between the 2014 and 2025 campaigns:

- Released after years of ambitious pricing (2009, 2010; 2021, 2022).

- Directly following a low yielding, poor quality vintage (2013; 2024).

- Released into stabilising markets.

While, at the time, there was discontent with 2014 pricing, they have fared well in the longer run. If we were to ask now if the 2014s were correctly priced, if with perfect hindsight one would have bought at those prices, many would say yes. With the Bordeaux market showing signs of stability, there is finally also reason to believe that, in two years time, when the 2025s reach shores, alternative vintages won’t be cheaper than they are now.

What now?

In short, this was not a knock-out campaign, but neither have those of the past that we now look fondly back on been either. This was perhaps not the make or break campaign we expected it to be, but one of okay prices and tepid sales. There remain reparations to be made to piqued En Primeur buyers of the past, but the 2025 vintage was not the death of En Primeur. I may have many more early wake ups ahead of me yet.

Resources

What Happened In Fine Wine This Week: Burgundy took the lead in fine wine this week, and US buying grows

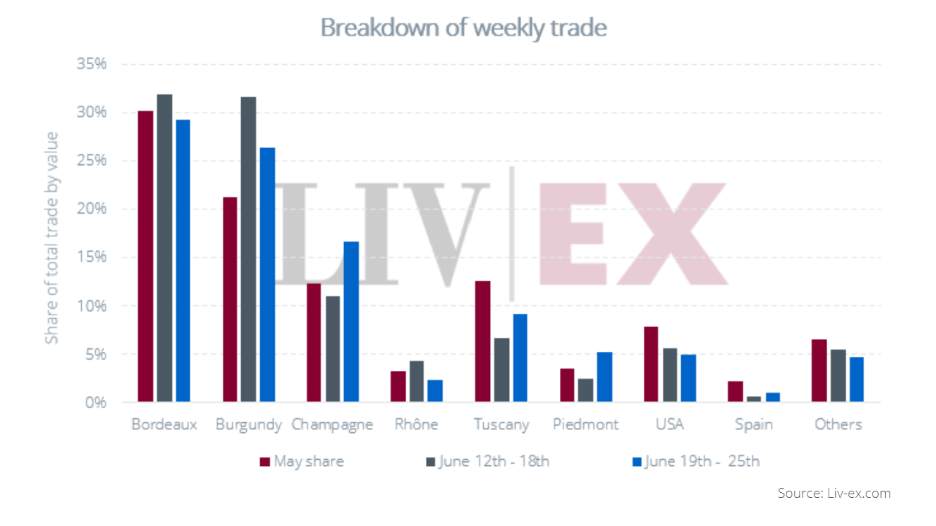

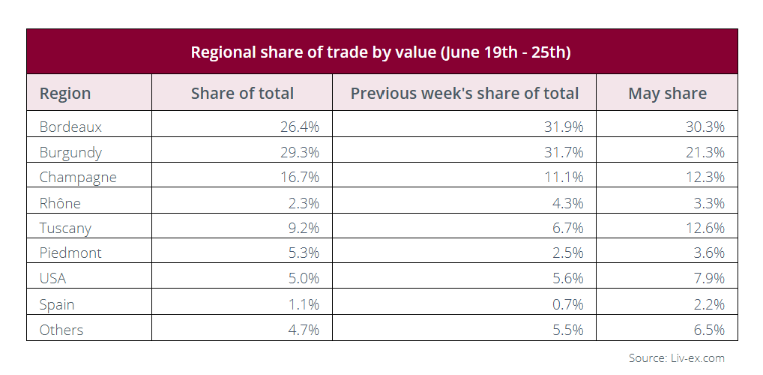

Burgundy has taken the lead, moving ahead of Bordeaux to become the largest contributor by value, accounting for 29.3% of the market

Burgundy has taken the lead, moving ahead of Bordeaux to become the largest contributor by value, accounting for 29.3% of the market. What’s driving that shift is not just demand for established names, but the growing liquidity in the latest available vintages. The 2023s alone make up around 40% of Burgundy’s traded value – a signal that buyers are actively deploying capital earlier in the wine’s lifecycle than in previous cycles.

For merchants, this is a notable change. Burgundy is not just trading strongly at the top end; it is becoming a more dynamic, two-speed market where both emerging and established wines are finding buyers.

Bordeaux remains resilient, but increasingly selective

Bordeaux still holds a significant share of the market, with 26.4% of traded value. But the nature of demand is evolving.

Rather than broad-based trading, activity is concentrating around mature, highly regarded vintages. First Growths from 2010 and 2005 are leading the way, with names such as Château Latour and Château Haut-Brion underpinning liquidity.

One example highlights this shift clearly: Château Latour 2016 was the most traded wine by value, yet it changed hands below its original release price.

Champagne and Italy: quiet gains, but strategic importance

Elsewhere, Champagne is seeing a meaningful uptick, rising to 16.7% of traded value, well above its recent averages. Leading houses such as Dom Pérignon and Krug continue to dominate activity.

In Italy, the picture is more mixed. Tuscany remains a key contributor, even as its share fluctuates, with producers like Poggio di Sotto continuing to draw attention. Piedmont also delivered a strong week, with top names such as Gaja and Bruno Giacosa attracting consistent demand.

Taken together, these regions highlight an important dynamic: buyers are maintaining diversified portfolios, but are highly targeted in where they deploy capital.

A more global market led by US demand

Perhaps the most striking development is geographic. US buyers accounted for 35% of traded value – the only group to increase their share week-on-week.

Access the full insight for a detailed breakdown of weekly trade, pricing movements and buyer activity by becoming a Liv-ex member.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

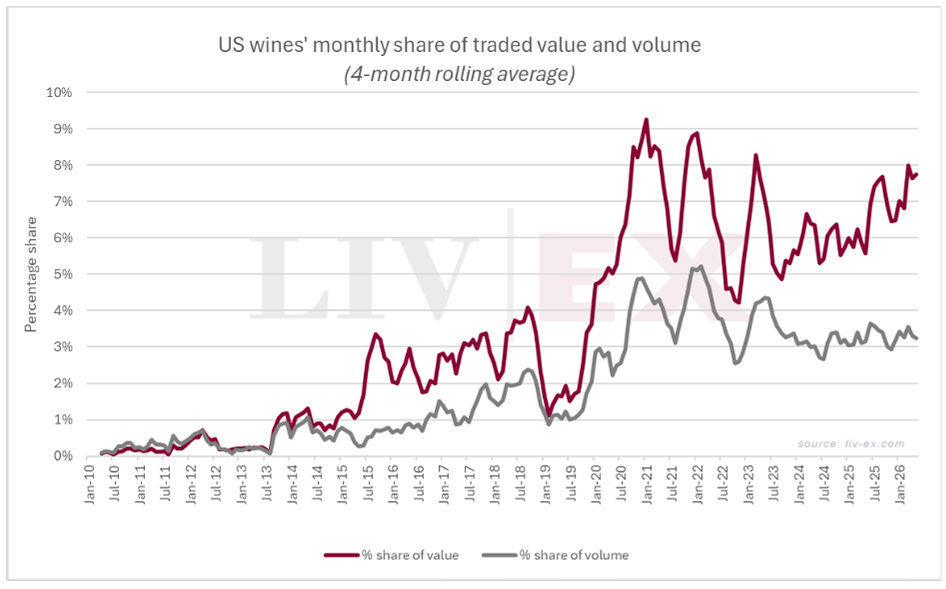

Rising value, shifting demand: US wines on the secondary market

The latest Liv-ex market update highlights a more structural – shift: the growing prominence of US wines within the secondary market itself.

Rising value, shifting demand: US wines on the secondary market

Much of the past year’s commentary has focused on how tariffs have shaped US demand for European wines. However, the latest Liv-ex market update highlights a different – and more structural – shift: the growing prominence of US wines within the secondary market itself.

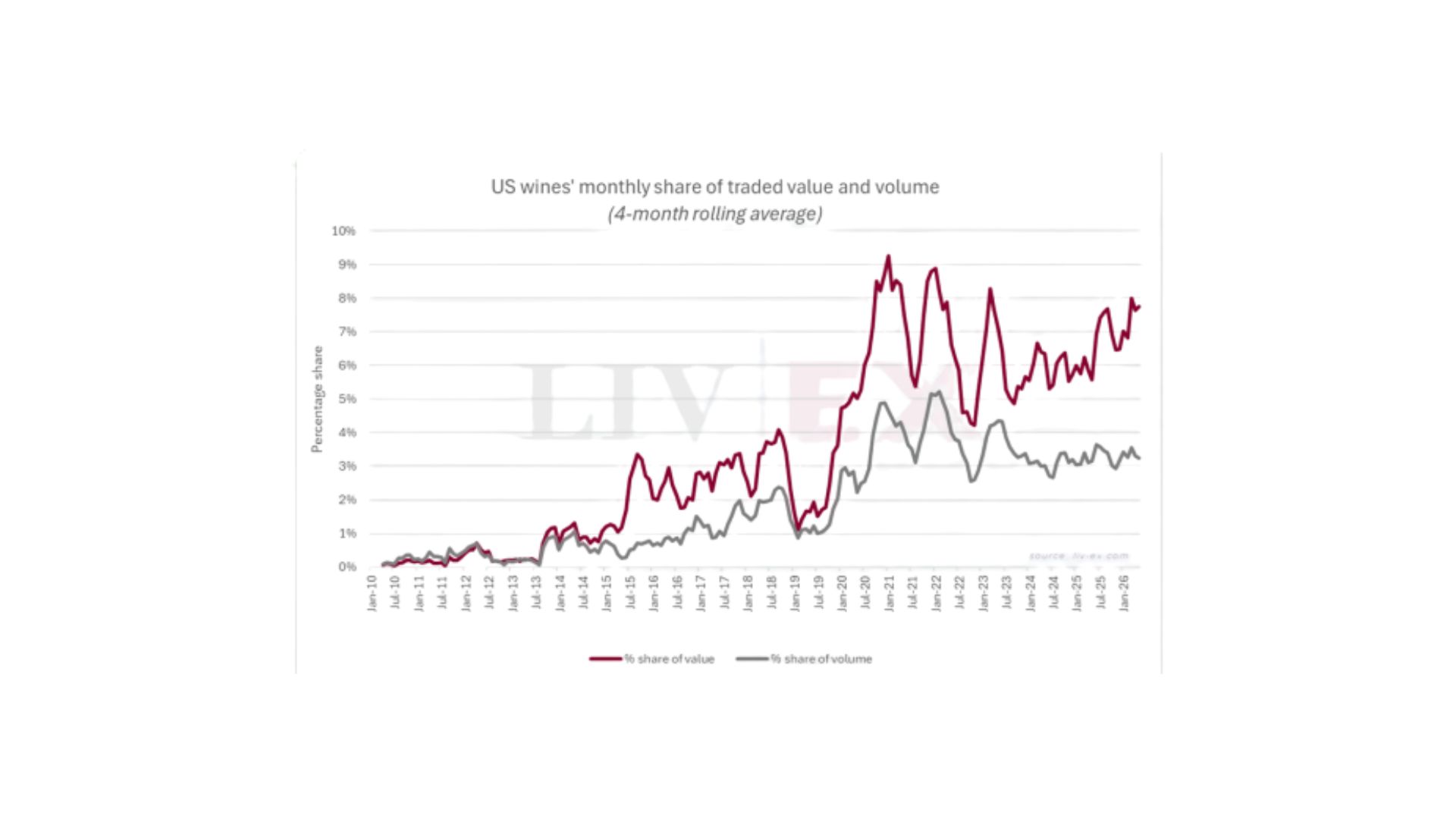

Data from Liv-ex shows that buyers are allocating a greater share of their spend to US wines than at any point over the past decade. While these wines accounted for less than 1% of trade on the platform ten years ago, they now represent more than 8%. For producers – particularly those in Napa Valley – this marks a meaningful change in how their wines are valued and traded internationally.

Liv-ex is the exchange for fine wine, market data and insight, providing a unique lens on secondary market behaviour. Crucially, wines listed on the platform must demonstrate resale value, meaning this growth reflects rising confidence in the investment and collectability credentials of US fine wine, rather than primary market supply.

The increase is overwhelmingly driven by Californian wines. While there is some representation from Oregon and Washington, activity remains concentrated in Napa and its leading producers.

The below graph compares the value of US wines traded (bought) on the platform, versus the volume. It shows that the value has increased more sharply than the volume. Demonstrating that people aren’t simply buying more (volume), they are spending more on US wines.

It’s also not the case that US wines are getting more expensive – Liv-ex tracks the price performance of the 50 most traded California wines. This data shows that buyers are opting for more expensive wines. This is thanks, in no small part, to Screaming Eagle, which makes up an increasingly high proportion of US wine trade.

Who is buying US wines?

The geographic profile of demand has also evolved. Prior to 2015, UK buyers dominated the secondary market for US wines. Since then, their share has declined as participation from European and Asian buyers has expanded.

“US buyers’ purchasing of US wines is notable. We might imagine that for US buyers it would be cheaper to acquire wine domestically. For those without initial allocations, this appears not to be entirely the case. US buyers’ increasing share of purchasing prior to tariff impositions is not the sole contributor to their increased share. Rather, since the start of 2023, the percentage of their total purchasing allocated to US wine has been steadily rising.’’ – Sophia Gilmour, Market Analyst, Liv-ex

This suggests a broader, demand-led shift rather than a short-term reaction to policy changes.

Conclusion

The growing share of US wines on the secondary market reflects a structural evolution. Increased participation from international buyers, combined with a clear tilt towards higher-value bottles, indicates that US fine wine is consolidating its position within the global fine wine market.

While activity remains concentrated among a relatively small group of benchmark producers, the direction of travel is clear: US wines are no longer marginal on the secondary market. Instead, they are becoming an increasingly established component of global fine wine portfolios.

About Liv-ex

Founded in 2000, Liv-ex is the global exchange for the fine wine trade, providing market data and insight. Headquartered in the UK with operations in France and Belgium, Liv-ex connects more than 550 businesses across 42 countries through its trading platform.

Resources

What Happened In Fine Wine This Week: Burgundy and Bordeaux go head-to-head supported by strong demand for First Growths

Chateau Margaux 2015, Domaine Leroy, Vosne-Romanee, Aux Genaivrieres 2017 and Carruades de Lafite 2022 were the top traded wines by value.

After a quieter week, activity on the fine wine exchange picked up, with all major buying geographies increasing their participation. Exchange data shows that Chateau Margaux 2015, Domaine Leroy Vosne‑Romanée Aux Genaivrières 2017 and Carruades de Lafite 2022 were among the top traded wines by value, with Bordeaux and Burgundy each accounting for around a third of total traded value.

Bordeaux holds a narrow lead

Bordeaux edged ahead with a 32.0% share of traded value, supported by strong demand for First Growths. Chateau Margaux and Chateau Lafite dominated activity, together accounting for over a third of the region’s trade. Haut-Brion and Mouton Rothschild also contributed meaningfully, although at lower volumes.

At a wine level, Chateau Margaux 2015 stood out as one of the most actively traded labels.

Burgundy keeps pace as top producers gain ground

Burgundy followed closely with a 31.5% share, with 2023 vintages leading both value and volume. Trading was concentrated among a small group of highly sought-after producers, including Domaine Leroy, Coche-Dury and Jean-Claude Ramonet, which moved ahead of Domaine de la Romanée-Conti in terms of activity this week.

Champagne gains momentum

Champagne saw a notable increase in share, rising from 9.5% to 11.3% week-on-week. Dom Perignon accounted for a significant proportion of this activity, with its P2 2008 emerging as the top-traded wine by value. Prices around £4,200 per case indicate continued demand for prestige cuvées.

Italy and the US take a step back

In contrast, Italian regions lost ground. Tuscany’s share fell sharply, while Piedmont also declined, suggesting a shift in buyer attention rather than a drop in liquidity. That said, key brands such as Tignanello and Sassicaia remained active, accounting for around a third of Italian trade.

US wines held steady at 5.7% of the market. Screaming Eagle led the region by value, with its 2021 Sauvignon Blanc among the most traded wines overall.

UK buyers return to the market

One of the more notable shifts this week was the resurgence of UK buyers, alongside increased participation from other key geographies. After a subdued period, this broad-based uptick suggests improving confidence and renewed engagement across the fine wine market.

Access the full insight for a detailed breakdown of weekly trade, pricing movements and buyer activity by becoming a Liv-ex member.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Copyright © 2026 Liv-ex Ltd. All rights reserved.