Resources

Talking Trade 16th of March: Burgundy takes the lead, DRC top-traded overall

Burgundy led the market with a 32% share of traded value. Domaine de la Romanee-Conti came out on top by traded value, Domaine Leflaive took the top spot by…

The latest Talking Trade is now live!

- Bordeaux ceded its lead of the market to Burgundy, which accounted for 31% of traded value.

- Valdicava Brunello Riserva Madonna Piano 2019, Petrus 2000 and Cristal 2008 were the top-traded wines by value.

- UK buyers’ share of purchased value rose while each other buying geography’s fell.

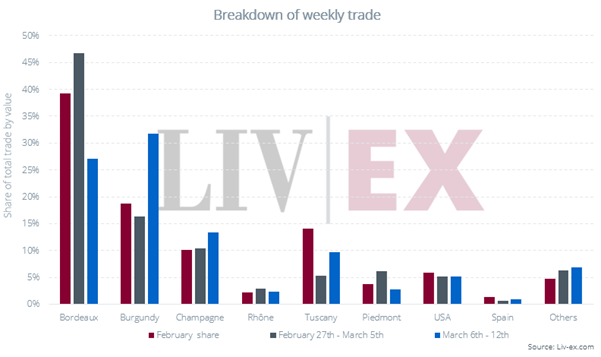

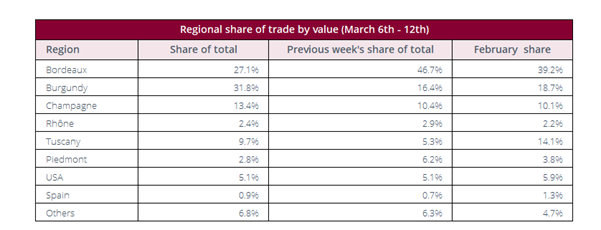

Bordeaux has dominated the market recently, peaking with a 47% share of traded value last week. This week, its share fell to 27%, ceding its first place position to Burgundy. Petrus led the region. Alongside more recent mature vintages, a case of the 1970, now in the final years of its drinking window, changed hands at £20,400/$27,132 per 12×75 /€1,972 per bottle.

Burgundy led the market with a 32% share of traded value. Domaine de la Romanee-Conti came out on top by traded value, Domaine Leflaive took the top spot by volume.

Champagne followed in third place, its share rising from 10% last week to 13% this week. Dom Perignon was the top-traded producer, led by the 2010, Oenotheque 1996 and P2 2008. All three have seen recent upticks in trade price, the 2010’s backed up by a significant increase in trade levels.

Tuscany had a stronger week, up from 5% to 10%. Brunello di Montalcino took the lead ahead of Bolgheri, with Valdicava and Fuligni seeing higher traded value than San Guido. Piedmont was less fortunate, its share falling to 3%.

The US’s share remained flat at 5%, Screaming Eagle taking the lion’s share of the region’s trade.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

Talking Trade 6th of March: Pavie leads again, Bordeaux’s share rises to 47%

Bordeaux’s share of the market rose to 47% — its strongest week in recent memory. For the second week running, Chateau Pavie dominated, with the…

The latest Talking Trade is now live!

- Bordeaux’s share of the market rose to 47% — its strongest week in recent memory. Burgundy and Champagne followed, with all other regions taking less than 10% of traded value.

- For the second week running, Chateau Pavie dominated, with the 2018 and 2017 vintages in the top positions.

- US buyers’ share of purchased value rose to 27%, strengthening their position in second place behind European buyers.

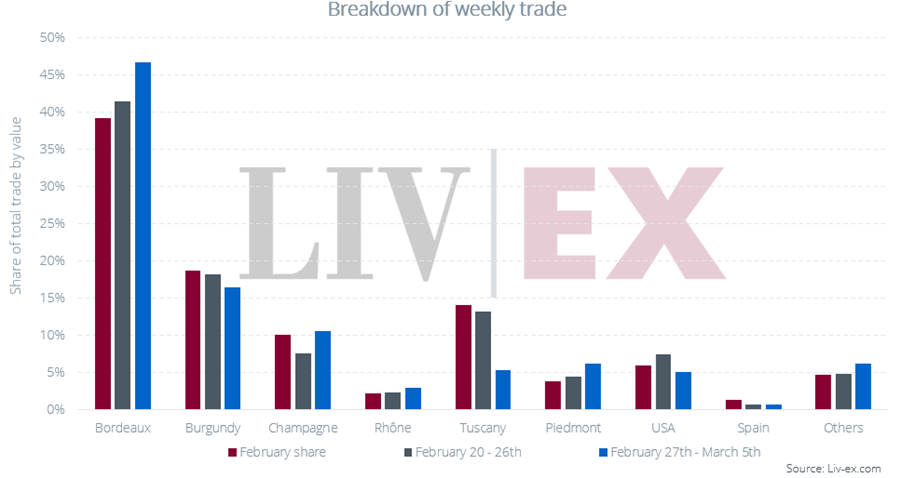

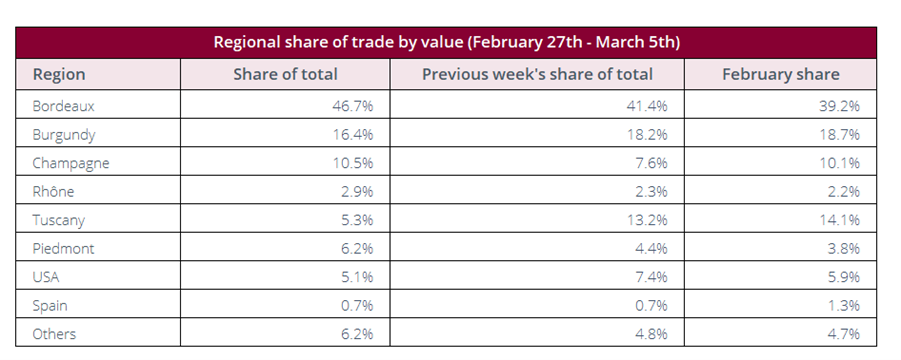

Bordeaux enjoyed another strong week, its share of the market rising from 41% last week to 46.7% this week. For the second week in a row, Chateau Pavie dominated, this time joined by Petrus, Beychevelle and Ausone.

Burgundy held its position in second place, though its share of traded value fell from 18% to 16%. Domaine Leflaive was the top-traded producer. Alongside recent vintage Puligny-Montrachet and Meursault, a single bottle of 1998 Montrachet changed hands at £10,075.

Champagne’s share increased from 7.6% to 10.5%. While the 2015 and 2016 vintages were the top-traded by value, the 2008 traded most frequently.

Tuscany’s share of trade fell to 5.3%, Piedmont overtaking with 6.2%. Still, Super Tuscans came out on top, with Tignanello and Sassicaia the top-traded Italian wines by value. Bartolo Mascarello’s Barolo came in third place.

The US’s share fell to 5.1%, down from 7.3% last week. Screaming Eagle led the region, with the 2022 Cabernet Sauvignon trading at £16,800 per 12×75. Promontory and Opus One followed.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

Talking Trade 2nd of March: Pavie leads trade; US and Asian buyers increase market share

Bordeaux extended its lead of the market, claiming a 41% share of traded value. The 2020 vintage claimed the top position by both value and…

The latest Talking Trade is now live!

- Bordeaux extended its lead of the market, thanks largely to trades of recent vintage Chateau Pavie. Burgundy and Tuscany followed in second and third place.

- Alongside Pavie 2020, 2019 and 2017, Ornellaia 2022 and Chateau La Mission Haut-Brion 2016 featured amongst the top five wines by traded value.

- With Asian buyers returning to their desks following Lunar New Year and US buyers’ share creeping back up, both UK and EU buyers’ share fell.

Bordeaux extended its lead of the market, claiming a 41% share of traded value. The 2020 vintage claimed the top position by both value and volume, followed by the 2019 and 2016 vintages. Pavie, La Mission Haut-Brion and Cos d’Estournel were the top-traded producers, First Growths taking a back seat this week.

Burgundy’s share fell from 27.4% last week to 18.2% this week. Armand Rousseau pulled ahead of Domaine de la Romanee-Conti as the region’s top-traded producer, thanks largely to US buyers.

Champagne’s share fell to 7.6%. While the 2013 and 2008 vintages traded most frequently and in the highest volumes, this week also saw trades of higher value, mature wines such as the 1998 vintage of both Dom Perignon P2 and Krug.

Tuscany’s share rose slightly from 12.2% to 13.2%. Ornellaia was by far the top-traded wine, claiming just over 40% of the region’s traded value. Fuligni Brunello di Montalcino joined Bolgheri’s heavy hitters amongst the top five.

The US’s share rose from 5.3% to 7.4%. Promontory was the top-traded wine by value, UK buyers accounting for around two thirds of purchasing and US buyers the remaining third.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

February Market Report

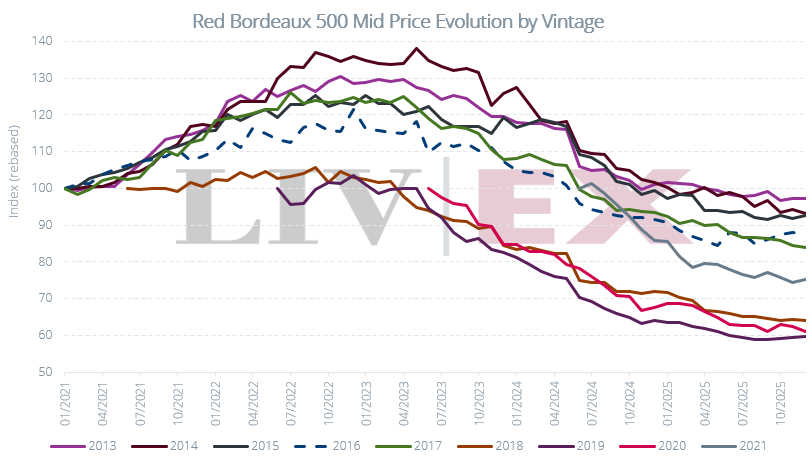

The Liv-ex February Market Report 2026 examines how Bordeaux 2016 wines have performed a decade on.

The Liv-ex February Market Report 2026 examines how Bordeaux 2016 wines have performed a decade on.

The topics covered in the Liv-ex February Market Report 2026:

- Seven of the top ten 2016 wines according to Neal Martin record gains: Even wines that saw sharper declines at the start of 2025, such as Vieux Château Certan and La Mission Haut-Brion Rouge, appear to have halted their downward trend and begun to recover.

- Cheval Blanc and Haut-Brion 2016 emerge as lower-risk options: Current mid prices show that 14 of the 45 red Bordeaux wines in the Bordeaux 500 2016 are trading below their ex-négociant release price

Liv-ex members receive comprehensive analysis of the market every month.

Download the Full Report

Resources

Talking Trade 20th of February: Burgundy and Bordeaux level at 28% share of market, Leflaive takes the lead

Burgundy’s share rose from 15.0% to 27.5%, pushing the region into a close second place. Though the 2019s were the top traded by value.

The latest Talking Trade is now live!

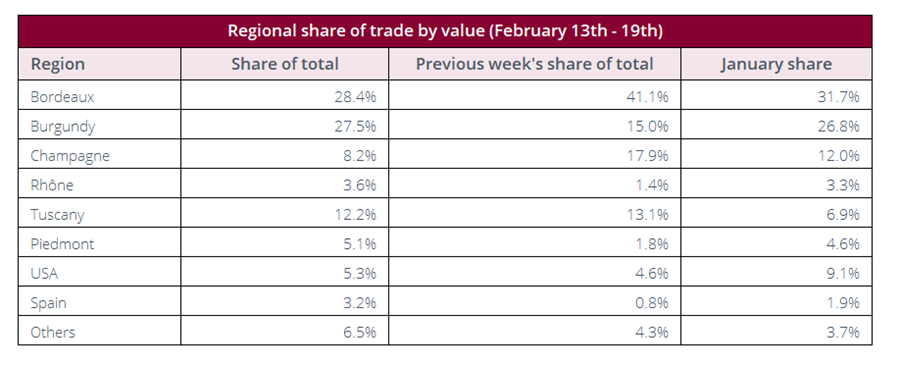

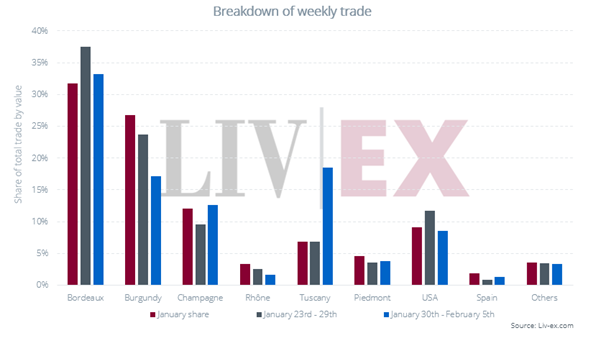

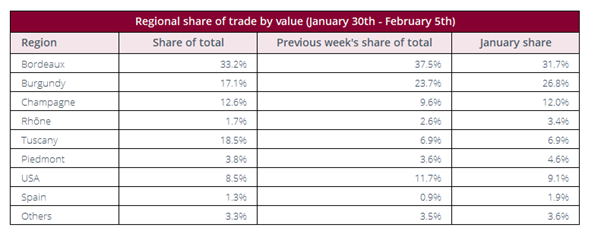

- Bordeaux’s share of trade declined to 28.4%, just taking the edge over Burgundy with 27.5%.

- Domaine Leflaive’s Puligny-Montrachet, Clavoillon 2019, Guado al Tasso 2023 and Tignanello 2022 were the week’s top-traded wines by value.

- While the US’s share of traded value remains low, they are more active on the market (by number of trades) than both Asian and UK buyers.

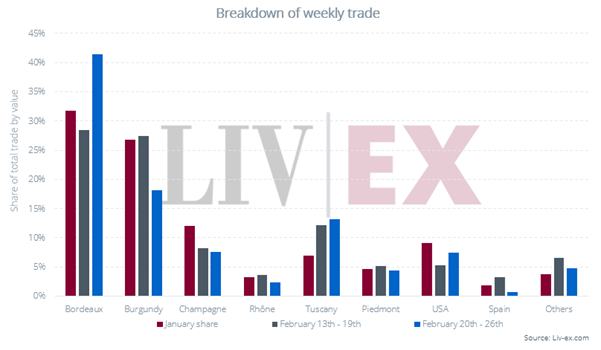

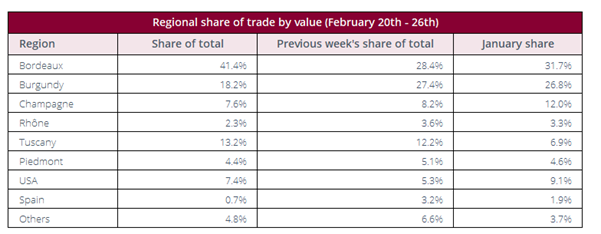

Though retaining its lead, Bordeaux’s share of traded value fell from 41.1% last week to 28.4% this week. Aromes de Pavie 2016 was the region’s top-traded wine by value, changing hands in decent volumes several times at £430 per 12×75 – a 49% discount to its ex-London release price.

Burgundy’s share rose from 15.0% to 27.5%, pushing the region into a close second place. Though the 2019s were the top traded by value, the 2023s claimed the top position by volume. Leflaive led the region, claiming 30% of its traded value. Domaine de la Romanee-Conti and Armand Rousseau followed.

Champagne’s share fell from 17.9% to 8.2%. Dom Perignon and Krug claimed the top positions amongst the region’s producers; trades of recent vintage (2015 and 2018) Winston Churchill pushed Pol Roger into third place ahead of Louis Roederer.

Tuscany held steady at 12.2% while Piedmont regained some of the ground it had lost last week, its share rising from 1.8% to 5.1%. Tignanello and Ornellaia were Italy’s top wines, though Bruno Giacosa and Gaja also traded actively, claiming third and fourth place.

The US, while falling short of its January share of 9.1%, saw an increase from 4.6% to 5.3% this week. Screaming Eagle continues to lead, with both the Sauvignon Blanc and Cabernet Sauvignon changing hands.

Spain, following weeks of diminished trade, saw a slight improvement, its share rising to 3.2%. While Vega Sicilia led by value, La Rioja Alta traded most frequently.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

Talking Trade 13th of February : Bordeaux and Champagne lead, US buyers take a step back

Champagne had a strong week, overtaking Burgundy to claim second place. Though Selosse Millesime 2013 was the top-traded individual wine Krug fared best across vintages

The latest Talking Trade is now live!

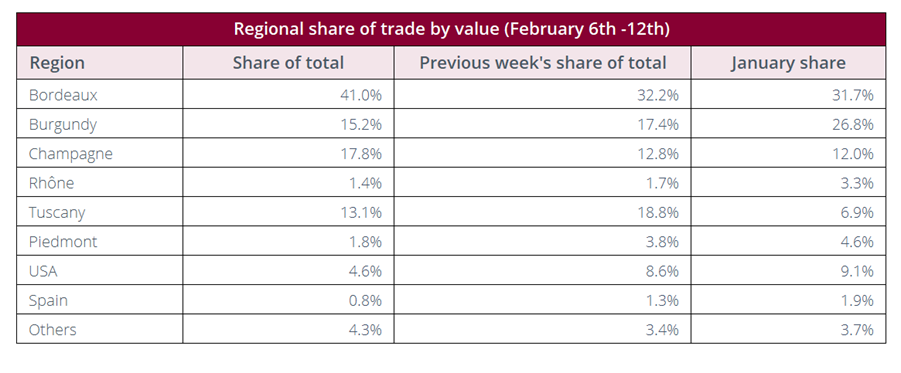

- Bordeaux extended its lead of the market, claiming 41% of traded value

- The newly released Sassicaia 2023 led the market. Chateau Troplong Mondot 2022 and Angelus 2021 followed in second and third place.

- US buyers took a backseat, their share of traded value falling from 20% to 13%.

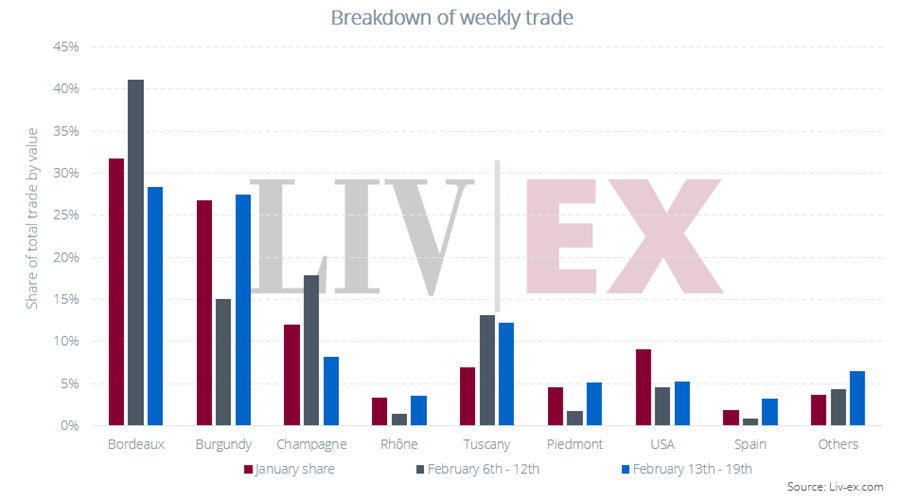

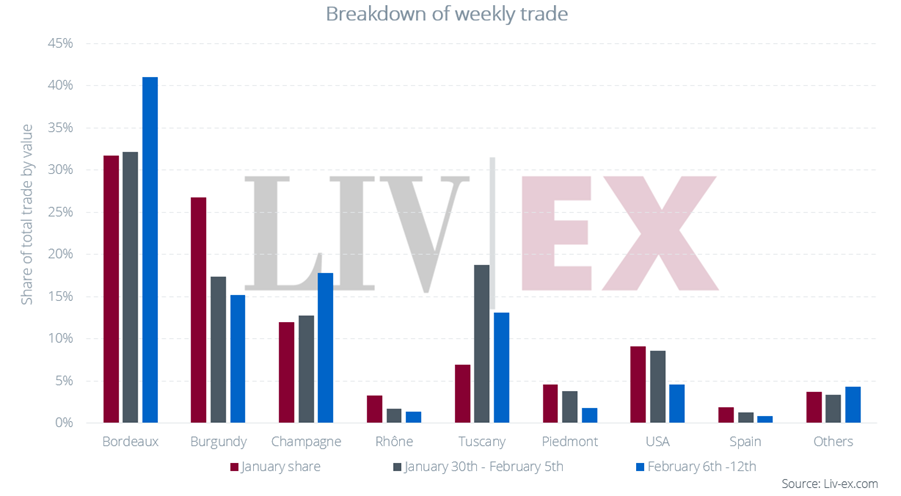

Bordeaux extended its lead of the market, its share of traded value up from 32.2% last week to 41.0% this week. Buyers concentrated their efforts on the 2022 vintage; prices generally having now fallen below ex-negociant levels.

Champagne had a strong week, overtaking Burgundy to claim second place. Though Selosse Millesime 2013 was the top-traded individual wine Krug fared best across vintages, accounting for a third of the region’s trade. The 2013 vintage will be released in the coming week.

Burgundy’s share fell from 17.4% last week to 15.2% this week, both weeks short of its January share of 26.8%. Domaine Leflaive was the top-traded producer, with several cuvees changing hands.

Though Tuscany’s share of trade fell from last week, San Guido continued to dominate, coming in as the broader market’s top traded wine of the week.

Following a strong few weeks, the US’s trade share fell to 4.6%. Though Screaming Eagle continued to lead the market, it was the Sauvignon Blanc rather than the Oakville Cabernet Sauvignon that traded most actively this week.

Copyright © 2026 Liv-ex Ltd. All rights reserved.

Resources

The Impact of Macro Economics on the Fine Wine Market

Fine wine prices rise and fall, not just in line with quality or reputation, but in response to economic forces shaping demand around the world.…

What’s the relationship between the global economy and the fine wine market?

Despite thousands of years of production, distribution, consumption and culture, fine wine is not abstract from modern economies. Like all product classes, its prices are impacted by the surrounding economic landscape.

Fine wine prices rise and fall, not just in line with quality or reputation, but in response to economic forces shaping demand around the world. For wine businesses navigating today’s environment and understanding that relationship has never been more important.

A Market Defined by Dual Demand

Unlike many luxury products, fine wine is sought for two very different purposes: consumption and investment. This dual demand makes fine wine even more susceptible to macro-economic patterns and cultural phenomena, because it’s impacted by consumption trends, as well as investment behaviour and wealth more broadly.

When consumer confidence is high, discretionary spending grows. When investors feel optimistic, alternative assets attract interest. When either shift, the fine wine market feels it.

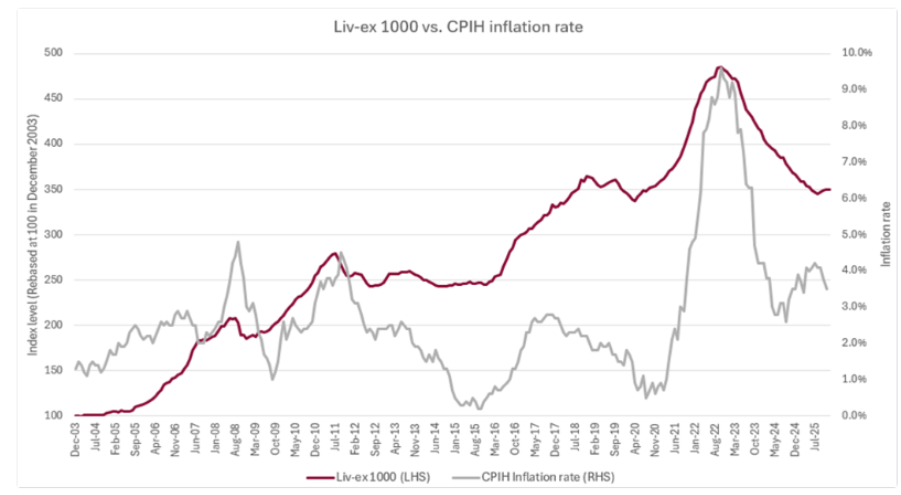

Interest Rates: More Than a Simple Cause and Effect

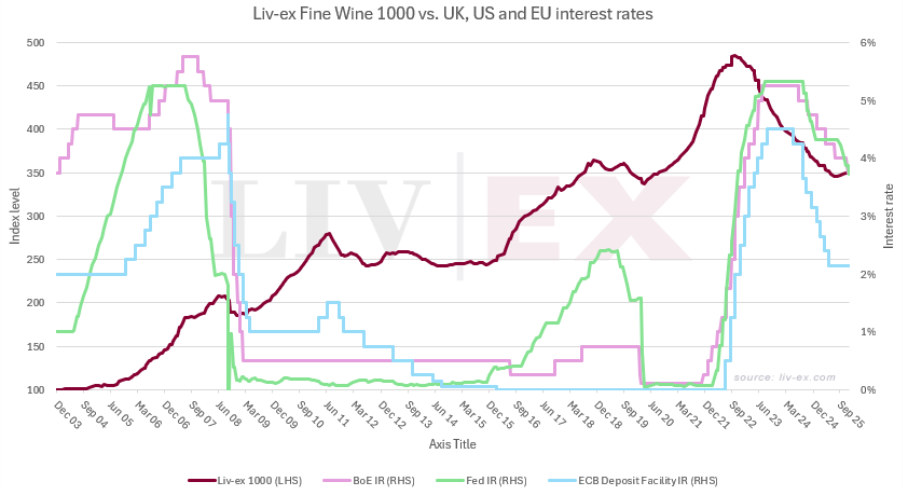

Interest rates are often used as an indicator of overall economic health, and while their relationship with fine wine is often discussed, its rarely quantified. In theory, low rates should lead to increased demand.

The chart shows that in periods of ultra-low rates, such as the COVID-19 lockdowns and the 2008 financial crisis, fine wine prices immediately rose. Conversely, fine wine has also performed well during moments of relatively high rates, such as in 2018. This suggests that it’s not the headline rate that matters, but the underlying conditions policies are responding to.

Inflation, growth expectations, investor appetite and access to capital all play interconnected roles in shaping demand for fine wine and subsequent price performance.

Inflation: A More Direct Link to Fine Wine Prices

Inflation has shown a more consistent relationship with fine wine pricing. Not because it’s part of the consumer shopping basket. The factors impacting the price of eggs, petrol and milk are different from those impacting fine wine. Although production costs are affected, most of the wine traded on the secondary market was manufactured years ago.

During periods of high inflation, tangible assets often gain appeal as investment opportunities. Fine wine can benefit from this as investors look to diversify beyond public markets.

Wine differs from housing and even luxury goods, such as watches and bags, in the nature its collected and the scale of its production. Traditionally, a fine wine collector will buy cases of six or more bottles of wine and continue to do so year after year. While release pricing is a product of labour, materials and perceptions of quality, and will in turn rise with inflation. Therefore, production costs are more relevant compared to other asset classes.

Recent years, however, have highlighted the risks: release prices have been set beyond what the market has been willing to pay, creating a mismatch between cost expectations and investor appetite.

As inflation has normalised over the past year, stability has returned, reducing volatility and helping rebuild confidence. For merchants, importers and producers, these dynamics underline a key point: inflation doesn’t just affect costs, it shapes behaviours.

The full article explores the interaction between real interest rates and fine wine prices, accessible only to Liv-ex Members.

What This Means for the Fine Wine Trade Today

After three years of disruption; marked by high inflation, rising rates and overly confident release prices – the environment is shifting.

Inflation has eased. Monetary policy is stabilising. And prices for many recent vintages have corrected to more appealing levels for buyers.

But monetary policy alone cannot reset the fine wine market. The stock cycle must play out. Vintages produced during periods of high cost and high expectation still need to be absorbed before the next growth phase can begin.

Why Market Intelligence Matters

For businesses operating in the fine wine industry, the lesson is clear – fine wine does not exist in isolation. Its performance is tied to the same macroeconomic factors influencing global wealth, investor sentiment, consumption patterns and financial stability.

To make informed decisions, whether in pricing, buying, inventory management or strategy, wine businesses need visibility into these relationships.

This is where intelligence becomes indispensable.

Liv-ex Market Intelligence helps wine businesses:

- Understand the market you operate in

- Act early on emerging trends

- Optimise your commercial performance

- Empower your whole team

Resources

January Market Report

The Liv-ex January Market Report 2026 explores the state of play as we enter 2026.

The Liv-ex January Market Report 2026 explores the state of play as we enter 2026.

The topics covered in the Liv-ex January Market Report 2026:

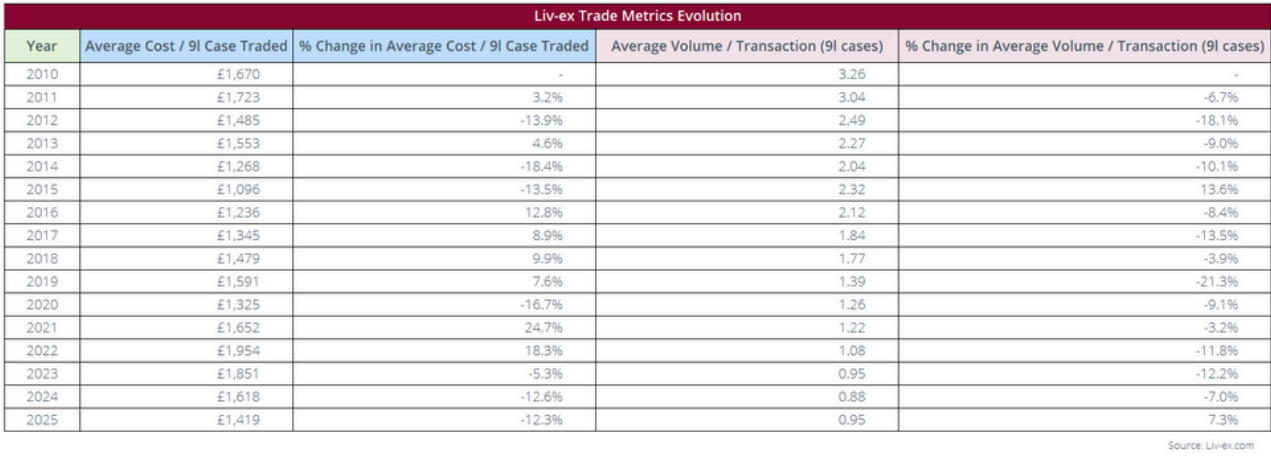

- Major Liv-ex indices remained stable in December :The Fine Wine 100 rose 0.4% and the Fine Wine 1000 held on November

- Buyers shifted toward lower-priced wines, driving higher trade volumes :The Fine Wine 1000 closed 2025 down 4.5% however the avg. cost per case traded is down 12.3%.

- European buyers stepped up in 2025 :With total European purchase value up 48.2% year-on-year.

Liv-ex members receive comprehensive analysis of the market every month.

Download the Full Report

Resources

Talking Trade 6th of February: Tuscany overtakes Burgundy by market share, Sassicaia leads

Bordeaux pulled further into the lead, claiming 37.5% of traded value. The 2022 vintage was the top-traded by both value and volume

The latest Talking Trade is now live!

- Though Bordeaux continues to lead, Tuscany displaced Burgundy as the second top-traded region by value.

- Sasssicaia 2021, ahead of the release of 2023 today, was the top-traded wine by value and volume.

- US buying continues to hold at around 22% of purchasing, buyers focusing largely on back vintage Bordeaux.

Bordeaux led the market with a 33.2% share of traded value, down on a strong close last week at 37.5%. Buyers concentrated their efforts on top vintages this week, with the 2016s, 2019s, 2020s and 2022s trading most frequently.

Taking 18.5% of trade, Tuscany pulled ahead of Burgundy as the second top-traded region by value. Sassicaia was by far the top-traded wine, accounting for over half of the region’s trade. Brunello di Montalcino, which has fallen by the wayside with reduced US purchasing, re-entered the fold, Fuligni coming in as Tuscany’s second top-traded producer.

Burgundy followed in third place with a 17.1% share. Buyers tended towards slightly lower value wines in higher volumes, with Domaine de la Tour, Robert Groffier and Comtes Georges de Vogue coming in as the top three producers by trade value.

Champagne claimed 12.6% of trade, up slightly from 9.6% last week. Jacques Selosse 2008 was the top traded wine by value, changing hands between £26,160 and £27,300, a marked increase from its low of £20,064 in April 2024. Recent upward price movement has been confirmed by rising trade frequency.

The US had another strong week (8.5%), again led by Screaming Eagle. Opus One also traded actively, with demand led largely by Europe and the UK.

Copyright © 2026 Liv-ex Ltd. All rights reserved.