Talking Trade 2nd of March: Pavie leads trade; US and Asian buyers increase market share

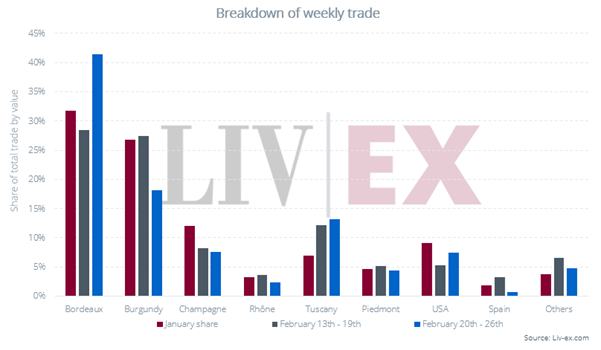

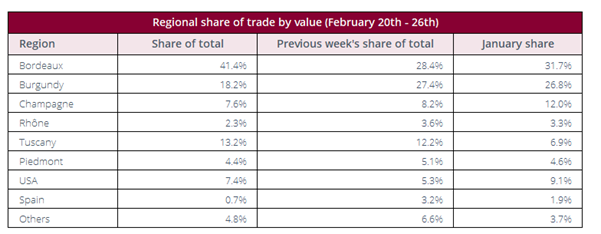

Bordeaux extended its lead of the market, claiming a 41% share of traded value. The 2020 vintage claimed the top position by both value and…

Market Intelligence

The latest Talking Trade is now live!

Bordeaux extended its lead of the market, thanks largely to trades of recent vintage Chateau Pavie. Burgundy and Tuscany followed in second and third place.

Alongside Pavie 2020, 2019 and 2017, Ornellaia 2022 and Chateau La Mission Haut-Brion 2016 featured amongst the top five wines by traded value.

With Asian buyers returning to their desks following Lunar New Year and US buyers’ share creeping back up, both UK and EU buyers’ share fell.

Bordeaux extended its lead of the market, claiming a 41% share of traded value. The 2020 vintage claimed the top position by both value and volume, followed by the 2019 and 2016 vintages. Pavie, La Mission Haut-Brionand Cos d’Estournel were the top-traded producers, First Growths taking a back seat this week.

Burgundy’s share fell from 27.4% last week to 18.2% this week. Armand Rousseau pulled ahead of Domaine de la Romanee-Conti as the region’s top-traded producer, thanks largely to US buyers.

Champagne’s share fell to 7.6%. While the 2013 and 2008 vintages traded most frequently and in the highest volumes, this week also saw trades of higher value, mature wines such as the 1998 vintage of both Dom Perignon P2 and Krug.

Tuscany’s share rose slightly from 12.2% to 13.2%. Ornellaia was by far the top-traded wine, claiming just over 40% of the region’s traded value. Fuligni Brunello di Montalcino joined Bolgheri’s heavy hitters amongst the top five.

The US’s share rose from 5.3% to 7.4%. Promontory was the top-traded wine by value, UK buyers accounting for around two thirds of purchasing and US buyers the remaining third.

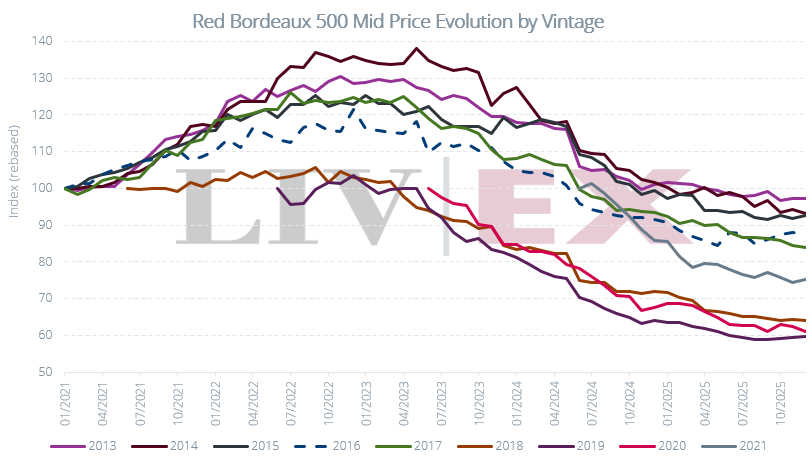

The Liv-ex February Market Report 2026 examines how Bordeaux 2016 wines have performed a decade on.

The Liv-ex February Market Report 2026 examines how Bordeaux 2016 wines have performed a decade on.

The topics covered in the Liv-ex February Market Report 2026:

Seven of the top ten 2016 wines according to Neal Martin record gains: Even wines that saw sharper declines at the start of 2025, such as Vieux Château Certan and La Mission Haut-Brion Rouge, appear to have halted their downward trend and begun to recover.

Cheval Blanc and Haut-Brion 2016 emerge as lower-risk options: Current mid prices show that 14 of the 45 red Bordeaux wines in the Bordeaux 500 2016 are trading below their ex-négociant release price

Liv-ex members receive comprehensive analysis of the market every month.

Download the Full Report

Submit the form below for access to our February Market Intelligence report, and see what our members received at the start of February.

Author: Grace Geldard

Liv-ex Reports

Talking Trade 20th of February: Burgundy and Bordeaux level at 28% share of market, Leflaive takes the lead

Burgundy’s share rose from 15.0% to 27.5%, pushing the region into a close second place. Though the 2019s were the top traded by value.

Market Intelligence

The latest Talking Trade is now live!

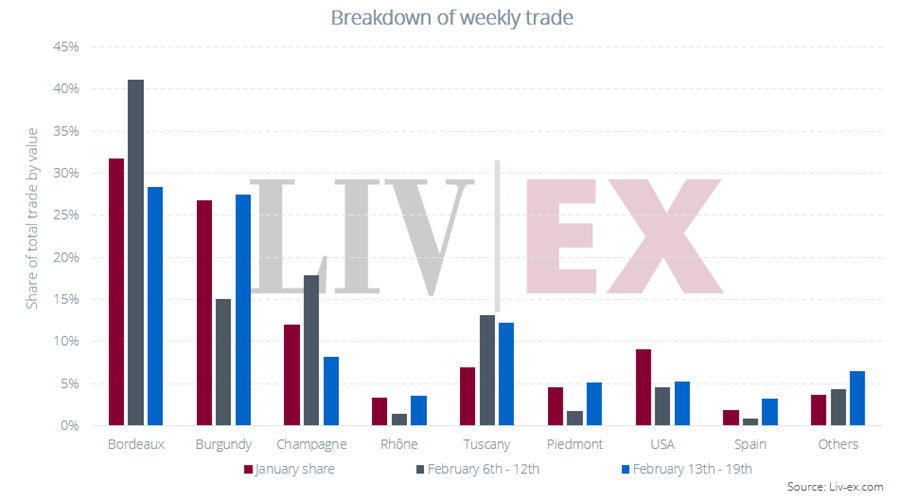

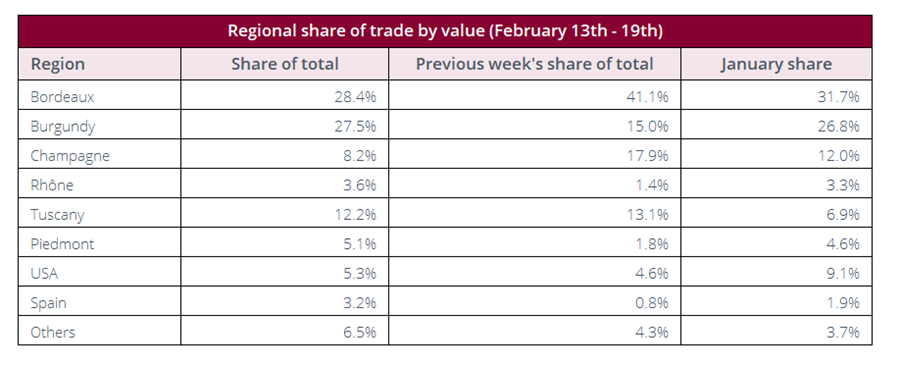

Bordeaux’s share of trade declined to 28.4%, just taking the edge over Burgundy with 27.5%.

Domaine Leflaive’s Puligny-Montrachet, Clavoillon 2019, Guado al Tasso 2023 and Tignanello 2022 were the week’s top-traded wines by value.

While the US’s share of traded value remains low, they are more active on the market (by number of trades) than both Asian and UK buyers.

Though retaining its lead, Bordeaux’s share of traded value fell from 41.1% last week to 28.4% this week. Aromes de Pavie 2016was the region’s top-traded wine by value, changing hands in decent volumes several times at £430 per 12×75 – a 49% discount to its ex-London release price.

Burgundy’s share rose from 15.0% to 27.5%, pushing the region into a close second place. Though the 2019s were the top traded by value, the 2023s claimed the top position by volume. Leflaiveled the region, claiming 30% of its traded value. Domaine de la Romanee-Contiand Armand Rousseaufollowed.

Champagne’s share fell from 17.9% to 8.2%. Dom Perignonand Krugclaimed the top positions amongst the region’s producers; trades of recent vintage (2015 and 2018) Winston Churchillpushed Pol Rogerinto third place ahead of Louis Roederer.

Tuscany held steady at 12.2% while Piedmont regained some of the ground it had lost last week, its share rising from 1.8% to 5.1%. Tignanelloand Ornellaiawere Italy’s top wines, though Bruno Giacosaand Gajaalso traded actively, claiming third and fourth place.

The US, while falling short of its January share of 9.1%, saw an increase from 4.6% to 5.3% this week. Screaming Eaglecontinues to lead, with both the Sauvignon Blancand Cabernet Sauvignonchanging hands.

Spain, following weeks of diminished trade, saw a slight improvement, its share rising to 3.2%. While Vega Sicilialed by value, La Rioja Altatraded most frequently.

Talking Trade 13th of February : Bordeaux and Champagne lead, US buyers take a step back

Champagne had a strong week, overtaking Burgundy to claim second place. Though Selosse Millesime 2013 was the top-traded individual wine Krug fared best across vintages

Market Intelligence

The latest Talking Trade is now live!

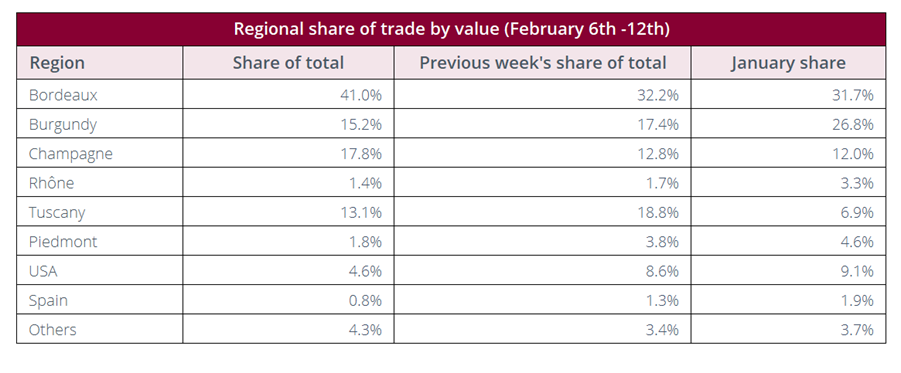

Bordeaux extended its lead of the market, claiming 41% of traded value

The newly released Sassicaia 2023 led the market. Chateau Troplong Mondot 2022 and Angelus 2021 followed in second and third place.

US buyers took a backseat, their share of traded value falling from 20% to 13%.

Bordeaux extended its lead of the market, its share of traded value up from 32.2% last week to 41.0% this week. Buyers concentrated their efforts on the 2022 vintage; prices generally having now fallen below ex-negociant levels.

Champagne had a strong week, overtaking Burgundy to claim second place. Though Selosse Millesime 2013was the top-traded individual wine Krug fared best across vintages, accounting for a third of the region’s trade. The 2013 vintage will be released in the coming week.

Burgundy’s share fell from 17.4% last week to 15.2% this week, both weeks short of its January share of 26.8%. Domaine Leflaivewas the top-traded producer, with several cuvees changing hands.

Though Tuscany’s share of trade fell from last week, San Guidocontinued to dominate, coming in as the broader market’s top traded wine of the week. Following a strong few weeks, the US’s trade share fell to 4.6%. Though Screaming Eaglecontinued to lead the market, it was the Sauvignon Blancrather than the Oakville Cabernet Sauvignonthat traded most actively this week.

Fine wine prices rise and fall, not just in line with quality or reputation, but in response to economic forces shaping demand around the world.…

Automation

What’s the relationship between the global economy and the fine wine market?

Despite thousands of years of production, distribution, consumption and culture, fine wine is not abstract from modern economies. Like all product classes, its prices are impacted by the surrounding economic landscape.

Fine wine prices rise and fall, not just in line with quality or reputation, but in response to economic forces shaping demand around the world. For wine businesses navigating today’s environment and understanding that relationship has never been more important.

A Market Defined by Dual Demand

Unlike many luxury products, fine wine is sought for two very different purposes: consumption and investment. This dual demand makes fine wine even more susceptible to macro-economic patterns and cultural phenomena, because it’s impacted by consumption trends, as well as investment behaviour and wealth more broadly.

When consumer confidence is high, discretionary spending grows. When investors feel optimistic, alternative assets attract interest. When either shift, the fine wine market feels it.

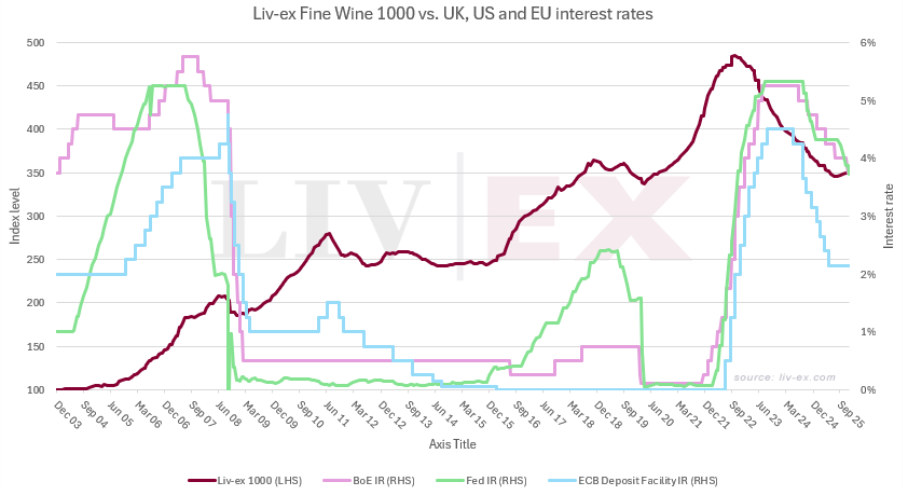

Interest Rates: More Than a Simple Cause and Effect

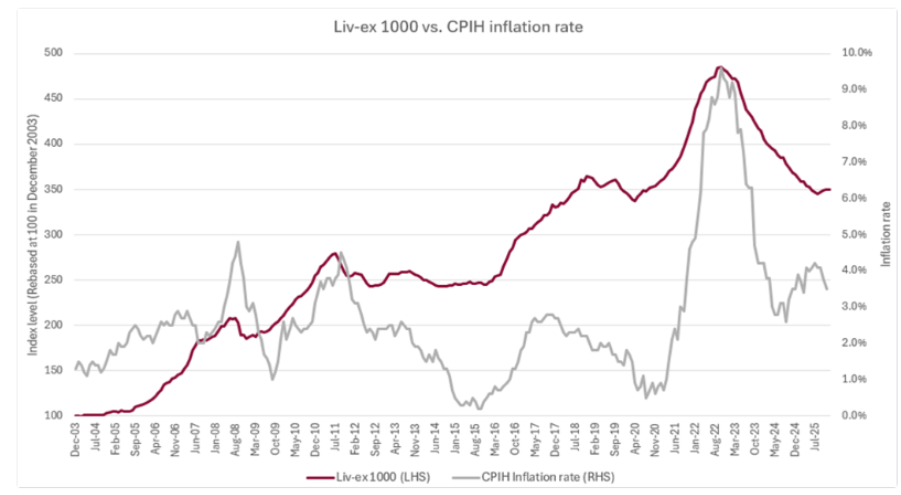

Interest rates are often used as an indicator of overall economic health, and while their relationship with fine wine is often discussed, its rarely quantified. In theory, low rates should lead to increased demand.

The chart shows that in periods of ultra-low rates, such as the COVID-19 lockdowns and the 2008 financial crisis, fine wine prices immediately rose. Conversely, fine wine has also performed well during moments of relatively high rates, such as in 2018. This suggests that it’s not the headline rate that matters, but the underlying conditions policies are responding to.

Inflation, growth expectations, investor appetite and access to capital all play interconnected roles in shaping demand for fine wine and subsequent price performance.

Inflation: A More Direct Link to Fine Wine Prices

Inflation has shown a more consistent relationship with fine wine pricing. Not because it’s part of the consumer shopping basket. The factors impacting the price of eggs, petrol and milk are different from those impacting fine wine. Although production costs are affected, most of the wine traded on the secondary market was manufactured years ago.

During periods of high inflation, tangible assets often gain appeal as investment opportunities. Fine wine can benefit from this as investors look to diversify beyond public markets.

Wine differs from housing and even luxury goods, such as watches and bags, in the nature its collected and the scale of its production. Traditionally, a fine wine collector will buy cases of six or more bottles of wine and continue to do so year after year. While release pricing is a product of labour, materials and perceptions of quality, and will in turn rise with inflation. Therefore, production costs are more relevant compared to other asset classes.

Recent years, however, have highlighted the risks: release prices have been set beyond what the market has been willing to pay, creating a mismatch between cost expectations and investor appetite.

As inflation has normalised over the past year, stability has returned, reducing volatility and helping rebuild confidence. For merchants, importers and producers, these dynamics underline a key point: inflation doesn’t just affect costs, it shapes behaviours.

The full article explores the interaction between real interest rates and fine wine prices, accessible only to Liv-ex Members.

What This Means for the Fine Wine Trade Today

After three years of disruption; marked by high inflation, rising rates and overly confident release prices – the environment is shifting.

Inflation has eased. Monetary policy is stabilising. And prices for many recent vintages have corrected to more appealing levels for buyers.

But monetary policy alone cannot reset the fine wine market. The stock cycle must play out. Vintages produced during periods of high cost and high expectation still need to be absorbed before the next growth phase can begin.

Why Market Intelligence Matters

For businesses operating in the fine wine industry, the lesson is clear – fine wine does not exist in isolation. Its performance is tied to the same macroeconomic factors influencing global wealth, investor sentiment, consumption patterns and financial stability.

To make informed decisions, whether in pricing, buying, inventory management or strategy, wine businesses need visibility into these relationships.

The Liv-ex January Market Report 2026 explores the state of play as we enter 2026.

The Liv-ex January Market Report 2026 explores the state of play as we enter 2026.

The topics covered in the Liv-ex January Market Report 2026:

Major Liv-ex indices remained stable in December :The Fine Wine 100 rose 0.4% and the Fine Wine 1000 held on November

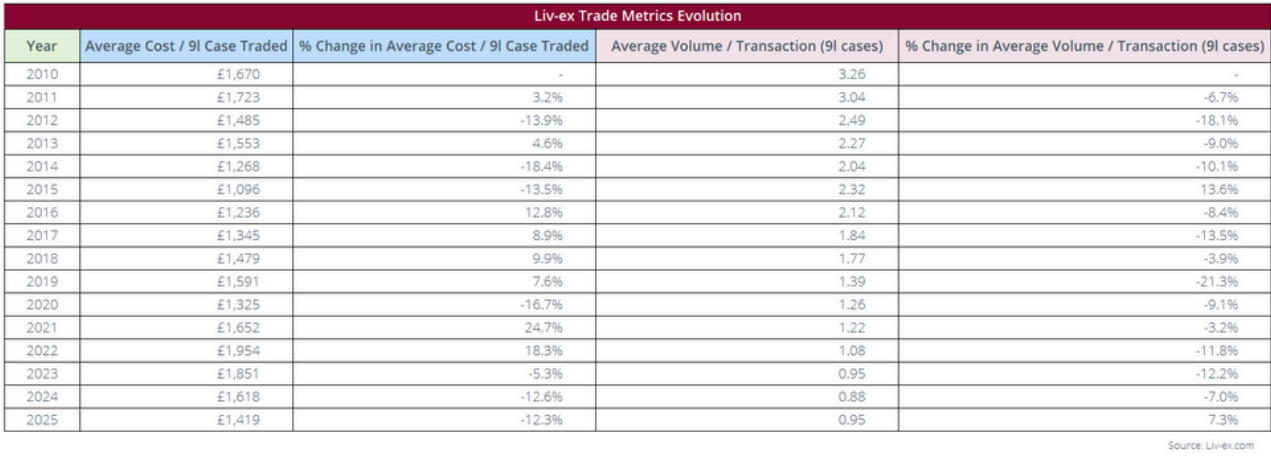

Buyers shifted toward lower-priced wines, driving higher trade volumes :The Fine Wine 1000 closed 2025 down 4.5% however the avg. cost per case traded is down 12.3%.

European buyers stepped up in 2025 :With total European purchase value up 48.2% year-on-year.

Liv-ex members receive comprehensive analysis of the market every month.

Download the Full Report

Submit the form below for access to our January Market Intelligence report, and see what our members received at the start of January.

Author: Grace Geldard

Liv-ex Reports

Talking Trade 6th of February: Tuscany overtakes Burgundy by market share, Sassicaia leads

Bordeaux pulled further into the lead, claiming 37.5% of traded value. The 2022 vintage was the top-traded by both value and volume

Market Intelligence

The latest Talking Trade is now live!

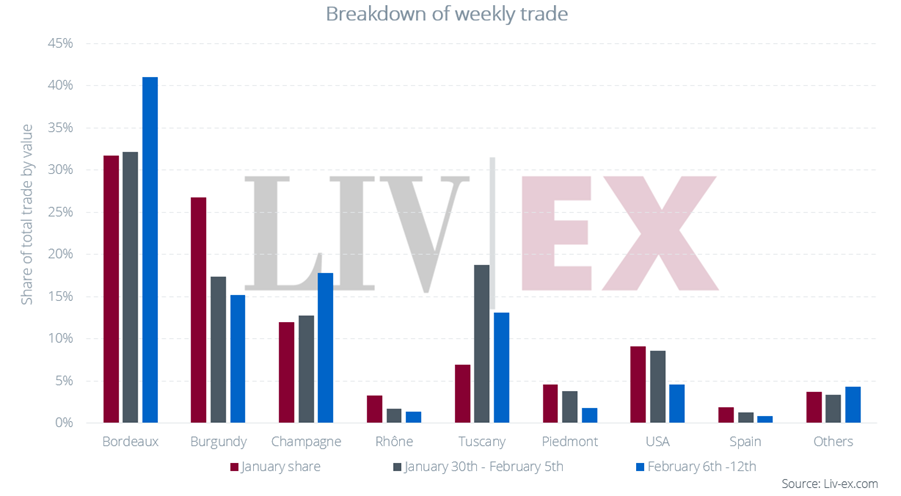

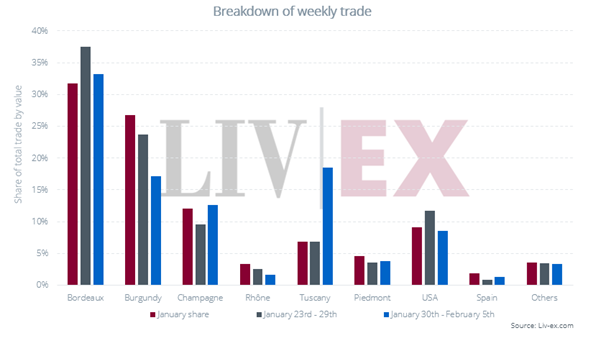

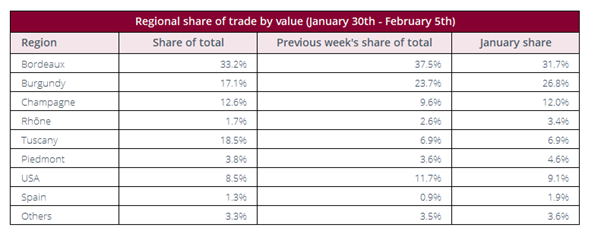

Though Bordeaux continues to lead, Tuscany displaced Burgundy as the second top-traded region by value.

Sasssicaia 2021, ahead of the release of 2023 today, was the top-traded wine by value and volume.

US buying continues to hold at around 22% of purchasing, buyers focusing largely on back vintage Bordeaux.

Bordeaux led the market with a 33.2% share of traded value, down on a strong close last week at 37.5%. Buyers concentrated their efforts on top vintages this week, with the 2016s, 2019s, 2020s and 2022s trading most frequently.

Taking 18.5% of trade, Tuscany pulled ahead of Burgundy as the second top-traded region by value. Sassicaiawas by far the top-traded wine, accounting for over half of the region’s trade. Brunello di Montalcino, which has fallen by the wayside with reduced US purchasing, re-entered the fold, Fulignicoming in as Tuscany’s second top-traded producer.

Burgundy followed in third place with a 17.1% share. Buyers tended towards slightly lower value wines in higher volumes, with Domaine de la Tour, Robert Groffierand Comtes Georges de Voguecoming in as the top three producers by trade value.

Champagne claimed 12.6% of trade, up slightly from 9.6% last week. Jacques Selosse 2008was the top traded wine by value, changing hands between £26,160 and £27,300, a marked increase from its low of £20,064 in April 2024. Recent upward price movement has been confirmed by rising trade frequency.

The US had another strong week (8.5%), again led by Screaming Eagle. Opus Onealso traded actively, with demand led largely by Europe and the UK.

Identify market shifts ahead of time with independent data and insight that you can trust

Liv-ex Market Intelligence is analysis of the fine wine market. It’s built on the industry’s most comprehensive pool of transactional data. It gives members the clarity, context, and confidence…

Automation

The fine wine industry has undergone some seismic shifts… In recent years, businesses have had to navigate shifting demand, changing global consumption, unpredictable En Primeur campaigns, and tariff‑related uncertainty. Even in 2025, early signs of recovery were disrupted by renewed trade tensions and a challenging Bordeaux EP.

In this environment, intuition and experience alone are no longer enough. To protect margins and stay ahead of changing demand, fine wine businesses need timely, unbiased intelligence.

Access to these insights gives members a clear competitive advantage – by enabling them to see market shifts well before others they can maximise opportunity and minimise risk.

What is Liv‑ex Market Intelligence?

Liv-ex Market Intelligence is analysis of the fine wine market. It’s built on the industry’s most comprehensive pool of transactional data. It gives members the clarity, context, and confidence to make informed commercial decisions, across buying, selling, pricing, and strategy.

It is:

Timely: Highly responsive and where possible, forward-looking analysis

Detailed: Combining high‑frequency trading data with in‑depth regional analysis

Independent: Not swayed by any position, speculation or bias

Personalised: Custom reports tailored to your business activity

How Market Intelligence Helps Fine Wine Businesses

1. Understand the market you operate in

Access the industry’s clearest view of fine wine dynamics, from real-time shifts to deep dives into regions and wines driving broader market trends. See what’s moving, where demand is shifting, and which wines are falling out of favour.

2. Act early on emerging trends

Spot demand up to six months before it’s reflected in list prices. Liv‑ex’s transactional data reveals real buying appetite before pricing changes appear publicly, giving you time to adjust strategy, stock, and pricing.

3. Optimise your commercial performance

Benchmark your own buying, selling, and stock list performance against the wider market. Understand where you are outperforming, and where margin opportunities are being missed.

4. Empower your whole team

Give your sales, buying, and leadership teams access to trustworthy data they can confidently share with customers and use equally in boardroom reporting as purchasing negotiations.

Why Independent Transaction Data Matters

Liv-ex Market Intelligence reports on transactional exchange data; this is the genuine price a wine has been sold at and bought for on the Liv-ex exchange. To further contextualise, it also uses the Liv-ex Market Price, which is data gathered from listed prices that is cleaned, standardised and categorised by Liv-ex.

Transactional exchange data is a leading indicator of market shifts. The graph below shows how changes in the Liv-ex bid:offer ratio precedes the mid price for Lafite.

Bid:offer ratio being the total value of bids against the total value of offers – or simply a measure of demand and supply

Mid price being the middle point between the highest bid and lowest offer – ie. the point at which a wine is most likely to transact

This is why members rely on Liv‑ex Market Intelligence to understand where the market is heading.

What types of Market Intelligence do Liv-ex member receive?

Personalised Market Report: A tailored monthly report analysing the most important market movements alongside your own buying, selling, and stock list activity – helping you identify new opportunities and respond to risk

Extended Reports: Comprehensive research into global regional dynamics, supply‑demand trends, pricing behaviour, and brand positioning

Market Updates: In‑depth analysis of regions, producers, trade flows, and brand performance – vital for businesses embedding data‑driven decision making into buying and sales strategies

Release Analysis: Independent evaluation of new releases – quickly see whether a wine is attractively priced, how it compares to back vintages, and whether it represents a buying opportunity

Talking Trade: Weekly, high‑frequency updates showing which wines, regions, and trends are driving market activity in the moment – essential for spotting emerging demand early.

“Liv-ex Market Intelligence is incredibly useful for tracking price evolution and assessing purchasing decisions. I sell wines on Liv-ex and regularly use the platform to check prices, but the Market Intelligence reports take it to the next level. They provide real support for my decision-making.”

Rodolphe de Noose, Ovinia

Ready to Stay Ahead of the Market?

Liv‑ex Market Intelligence helps fine wine businesses anticipate shifts, protect margins, and make confident decisions.

If you’d like to explore becoming a Liv‑ex member or would like to see examples of our latest reports, please reach out to our business development team.

Author: Grace Geldard

Liv-ex Reports

Talking Trade 30th of January: Asian buying picking up; US holding strong

Bordeaux pulled further into the lead, claiming 37.5% of traded value. The 2022 vintage was the top-traded by both value and volume

Market Intelligence

The latest Talking Trade is now live!

Bordeaux pulled further into the lead of the market, claiming 37.5% of traded value. Burgundy and the US followed in second and third place.

Domaine de la Romanee-Conti, Romanee-Conti 2022, Cos d’Estournel 2005 and Screaming Eagle 2023 were the top traded wines by value.

Asian buying picked up this week, accounting for 18.5% of traded value.

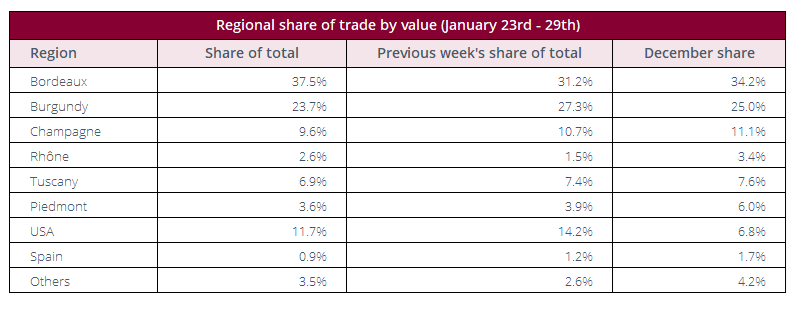

Bordeaux pulled further into the lead, claiming 37.5% of traded value. The 2022 vintage was the top-traded by both value and volume, with Second and Fifth Growths trading more actively than Firsts.

The US held strong in third place with Screaming Eagle– both the not-yet-physical 2023 and back vintages – pulling its weight. Dominusand Sine Qua Nonalso took significant shares of the region’s trade.

Champagne’s share fell slightly to 9.6%. The recently released Dom Perignon P2 2008held its position as the region’s top traded wine, though it fell short of the overall top five. It is trading consistently around £3,500 per 12×75, double the price of the regular 2008.

Tuscany and Piedmont remained consistent, but relatively subdued, together accounting for 10.4% of traded value. Tignanellopulled ahead of Sassicaiaas the country’s top traded wine.

The Rhone’s share of trade rose from 1.5% to 2.5% this week, thanks largely to US buyers, who accounted for over 60% of the region’s trade.