Bordeaux 2022: A double-edged sword

Introduction

As we approach the Union des Grand Crus En Primeur tastings, the 2022 vintage is hotly anticipated by critics and the trade alike, with some already dubbing it (another) vintage of the century. But like all vintages before it, the market into which it is released will play a key role in the success of this campaign.

Bordeaux’s secondary market has changed considerably over the past decade. With it, the En Primeur system has also evolved, becoming more a more complex and nuanced affair for all.

The changing influence of critics, the introduction of Recommended Retail Prices and the greatly increased retention of stock by the chateaux are three key changes of recent years. Some producers are navigating this changing world successfully and are reaping the rewards, while others are coming under fire for strategies that some commentators have likened to price control.

The wine trade has become increasingly risk-averse in the lead up to this year’s En Primeur campaign, as a result of the troubling macroeconomic headwinds. Both prices and volumes have been under pressure, particularly for recent vintages.

While 2022 may well be considered one of the truly great vintages (we will know more in a few weeks’ time), the chateaux will want to keep the broader economic picture in mind. Many of the great vintages of recent years have proved poor investments for collectors who are increasingly questioning their part in the En Primeur process.

This year’s report takes an in-depth look at the current state of the Bordeaux market and considers recent changes to the En Primeur process and what they might mean for the current and future campaigns.

Bordeaux’s 2022 vintage

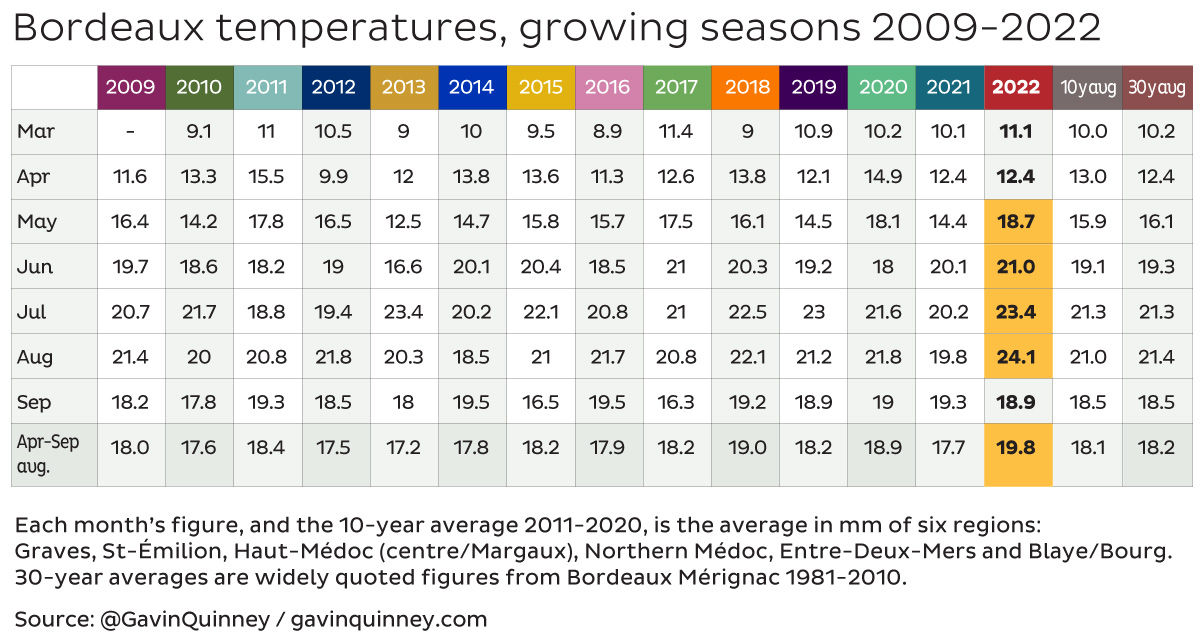

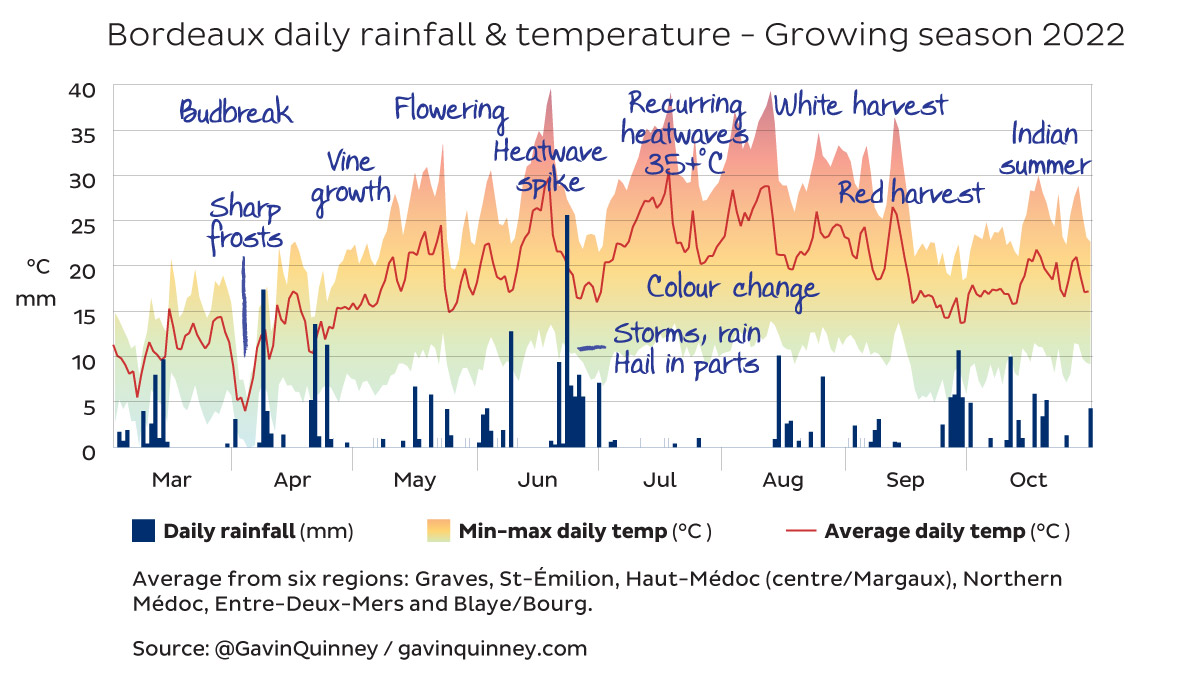

Overall, 2022 was ‘a year of highs and lows’ according to Gavin Quinney’s Bordeaux 2022 Weather Report. Unlike its predecessor, the upcoming vintage suffered from extremely high temperatures, and exceptionally low rainfall.

Saturnalia’s Bordeaux report identified 2022 as one of the hottest years on record, featuring severe droughts and record-breaking heatwaves. Average temperatures recorded in the region were higher than the 10-year average on 83 days between May and August.

Rain was remarkably absent from winter and into summer. The extended period of drought from July to September was interrupted only by storms on June 20th, which in some domains even brought hail.

While it’s too soon to pass a definitive judgement on the vintage, the intense heat combined with low amounts of rain will undoubtedly have an effect on the wine produced, both in terms of quality and quantity.

A hot and dry growing season

Gavin Quinney’s weather report found that the average temperatures recorded in May, June, July, August and September were higher than their 5-, 10- and 30-year averages. As shown in the table below, temperatures recorded were higher than every year since at least 2009 and marked a considerable increase from 2021.

January brought a wave of cold, perceived in hindsight as a welcome break from the incessant heat of the following months. A spell of sharp frosts in early April impacted some vineyards, but mercifully came after budbreak.

Summer was defined by recurring heatwaves over 35°, with a record-breaking peak in June when temperatures went over 40° in many regions. Saturnalia’s report notes the sudden increase in temperatures in May (seen in the table above) instead of a usual more gradual accumulation.

There is concern that the thermal shock could have inhibited berry growth. Quinney, however, remained positive, stating ‘the vines, not least in the better-placed vineyards, held up incredibly well despite the ongoing drought and protracted summer heatwaves’.

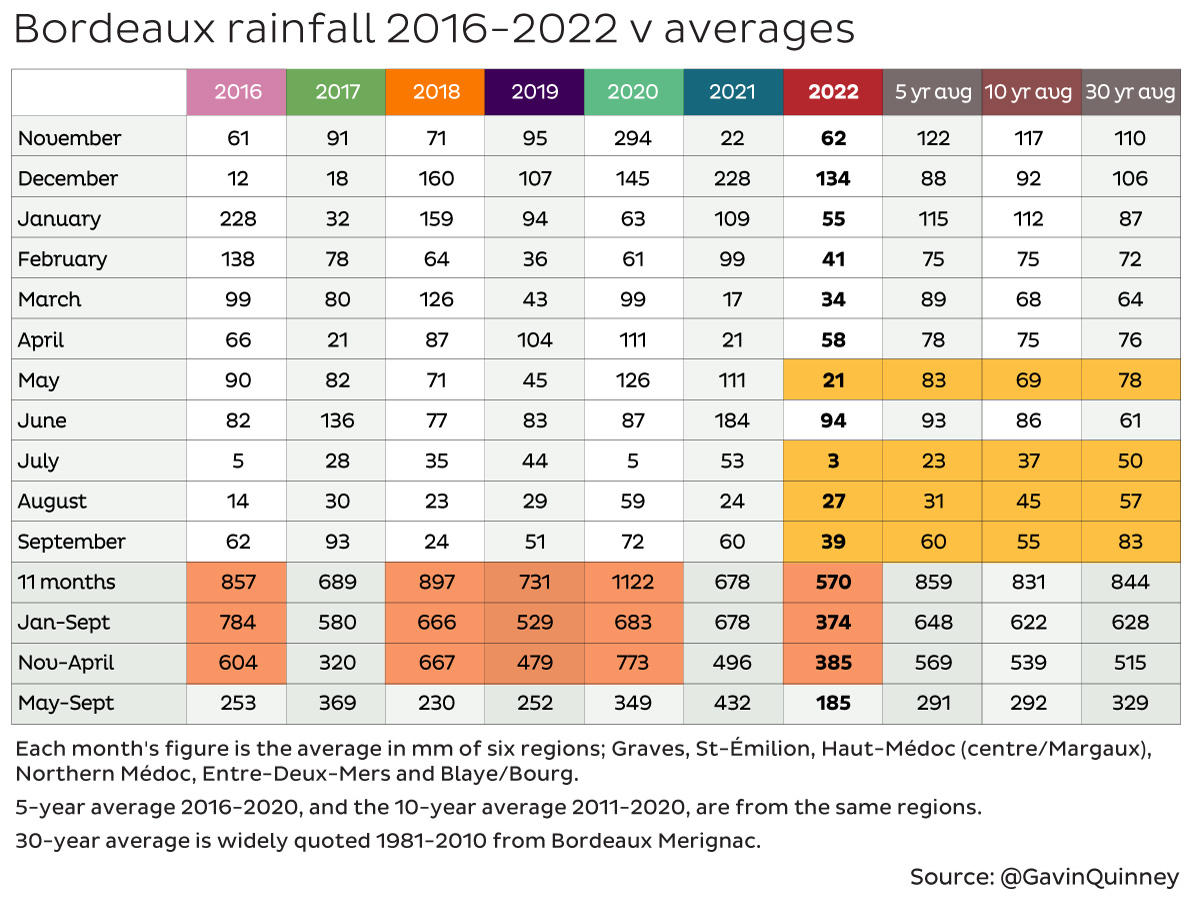

This is especially surprising considering the lack of water throughout the growing season. The year started with a comparatively dry January and February, which as the table below shows benefitted from about half of the rainfall experienced in 2021.

June was the only month when rainfall was up on the 5-, 10-, and 30-year averages, but that was mostly due to two flash storms following the heatwave spike. As the Saturnalia report highlights, sudden events like summer storms are less beneficial to vegetation growth than more regular rainfall; if the soil is too dry, its absorption capability is reduced.

The table above shows just how dry the months of May, July, August and September were compared to recent years, with July in particular only benefitting from 3mm of rain. While irrigation is not usually permitted in the Bordeaux region, growers in Pomerol and Pessac-Leognan obtained a late derogation from the INAO (Institut national de l’origine et de la qualité) which allowed them to water their vines under strict conditions.

Regional weather patterns can be fairly informative, but the impact of rainfall – or lack thereof – can vary hugely between estates. For example, the storms in the week of June 20th were disastrous for some domains due to the hail, but a blessing for others that needed heavy rain after the heatwaves and drought. Two corridors of hail travelled through the region, affecting domains both on the Left and the Right Banks, with variable impact recorded.

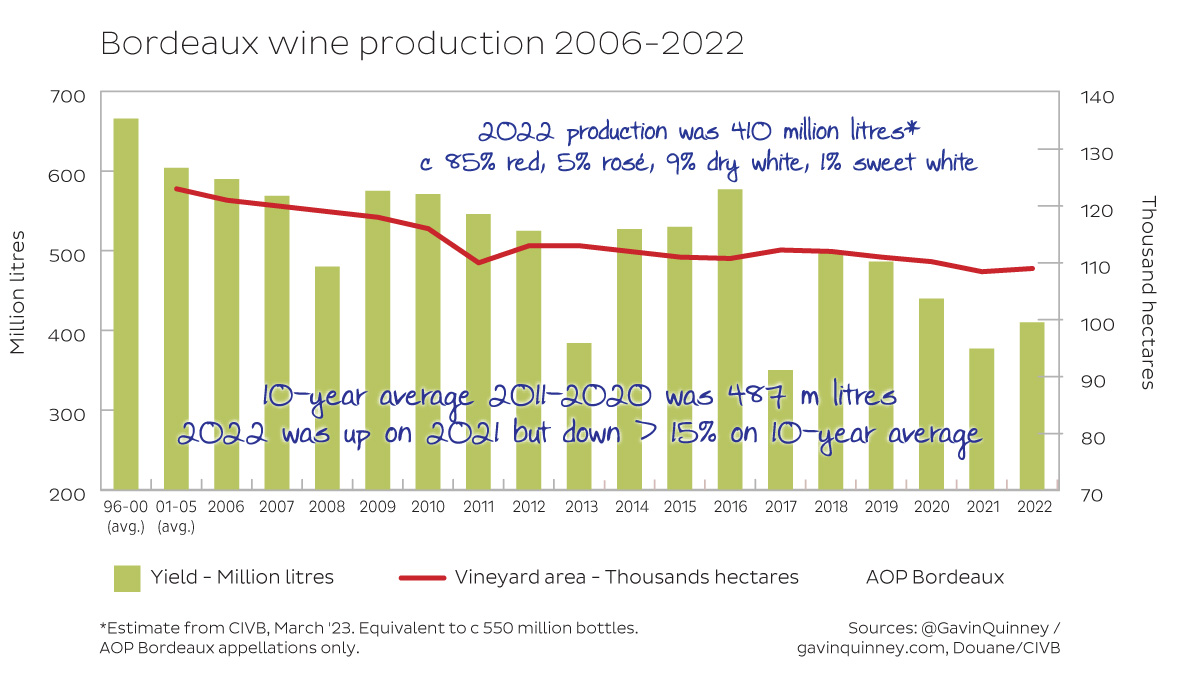

Crop size and yield

Total wine production was of 410 million litres in 2022, down more than 15% compared to the 10-year average of 487 million litres. However, it marks an improvement on 2021, when production was just 377 million litres. It is also notably higher than 2013 and 2017 yields, which were notoriously average vintages.

The split was 85% red, 5% rose, 9% dry white and 1% sweet white. At the time of writing, the full details were not yet available due to customs software issues.

The majority of wines in the region were harvested in September, at similar times than the 2018 and 2020 vintages, which means few vineyards benefitted from the balmy October temperatures.

Vintage summary

The picture from 2022 is vastly different to the one presented by its predecessor. Instead of a cool and wet vintage, we have one marked by heat and drought. While there are concerns that the extreme heat and weather events in June might have damaged the vines in some domains, the outlook is bright for this vintage.

Colin Hay of the drinks business remarks that the weather conditions all point to a promising vintage, at least on par with the likes of 2018, 2019 and 2020. Jane Anson concurs in her 2022 Vintage Overview. She highlights that flowering took place in good conditions, fruit set was variable but overall successful, ripening of grapes was also mostly a success despite the hot conditions, and that harvest conditions were near perfect, with no rain and little illness such as rot.

Rainfall levels in 2022 were very similar to 2010, a particularly good vintage, but the temperatures considerably higher. The dry summer is reminiscent of conditions experienced in 2016, 2018 and 2020, but spring in 2022 was also much dryer than previous years.

While it is difficult to make predictions before En Primeur tastings truly begin, we can expect very concentrated wines from 2022. Jane Anson’s tasting notes so far describe ‘wines that are richly coloured with plenty of tannic heft’. The extreme weather conditions (both heat and storms) also imply a low yield and an exclusive vintage, though this will vary greatly from one domain to the next.

The high temperatures and low rainfall yielded ‘small grapes, thick skins, and clear concentration’, according to Jane Anson. This also means the wines produced are high in tannins, which is a good indicator that they will age well.

Liv-ex is the global marketplace for the wine trade. The fastest way to price, buy and sell wine.

Bordeaux’s secondary market

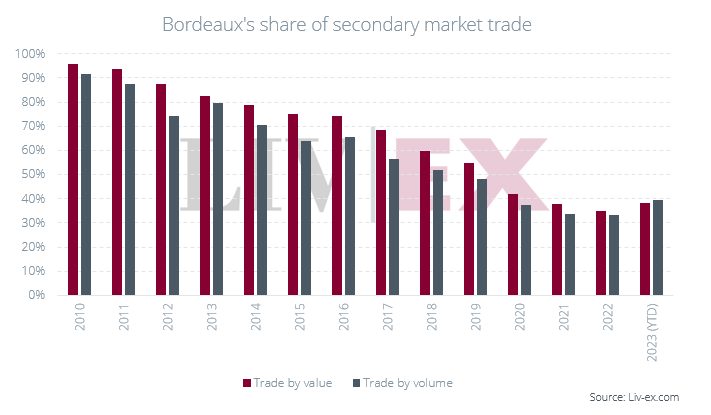

Bordeaux has long dominated the secondary market, but not to the degree it once did. Back in 2010, at the height of the China-led market boom, it accounted for 95.7% of trade by value. Since then, its trade share has fallen to 35.1% in 2022.

However, in absolute terms, volume of Bordeaux trade on the market has increased since 2010 (+47.5%). The reason its share by value and volume has declined is because the fine wine market has broadened considerably – more wines are being traded than ever before. The market has not fallen out of love with Bordeaux – far from it – it just has more choice than ever before

*data taken on 18.04.23.

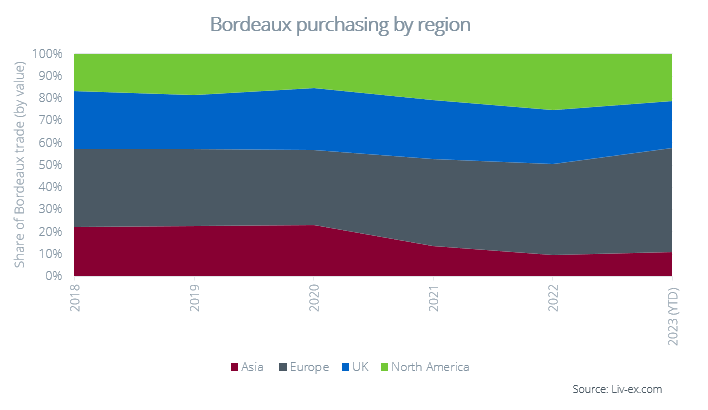

Bordeaux buying by region and country

When it comes to demand, Europe is the biggest buyer of Bordeaux. Year-to-date, the continent accounts for 46.8% of all Bordeaux trade (as a percentage of total value), up from 33.6% in 2020. North America has also been a growing region, with 21.4% (previously 15.5% in 2020).

As a result, traditional Bordeaux markets like Asia and the UK have seen their trade shares squeezed. The UK now sits at 20.8% (although it remains the single largest buyer of EP globally) while Asia is at 11.0%. In 2020, their shares accounted for 27.8% and 23.1% respectively.

*numbers taken on 31.03.23.

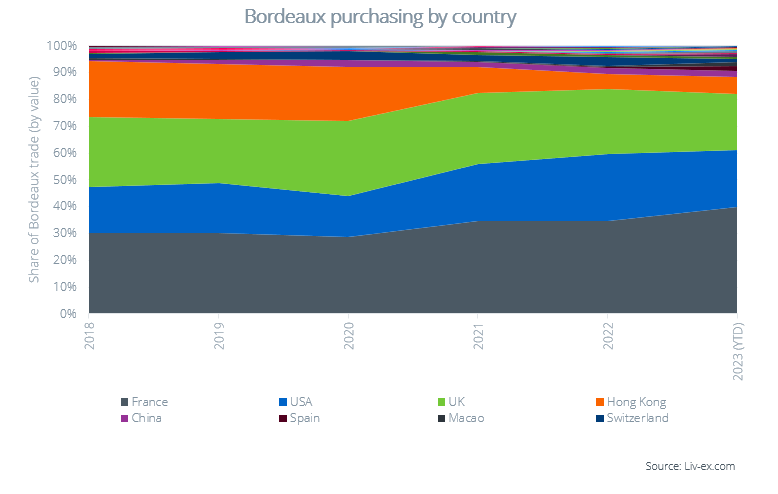

When broken down by country, France is the biggest buyer of wines from the region, at 39.9% of total trade in 2023. The USA follows with 21.4%, then the UK with 20.8%.

The most notable rise is the increase in other countries buying Bordeaux (shown at the top of the chart below). These countries have risen to account for 9.5% of Bordeaux trade in 2023.

This comprises trading activity from Denmark, Belgium, Austria, Czech Republic, Portugal, Luxembourg, the Netherlands, Slovenia, Korea, Norway, Malta, Ireland, Taiwan, Sweden, Japan, Canada, and more.

*numbers taken on 31.03.23.

Bordeaux’s price performance

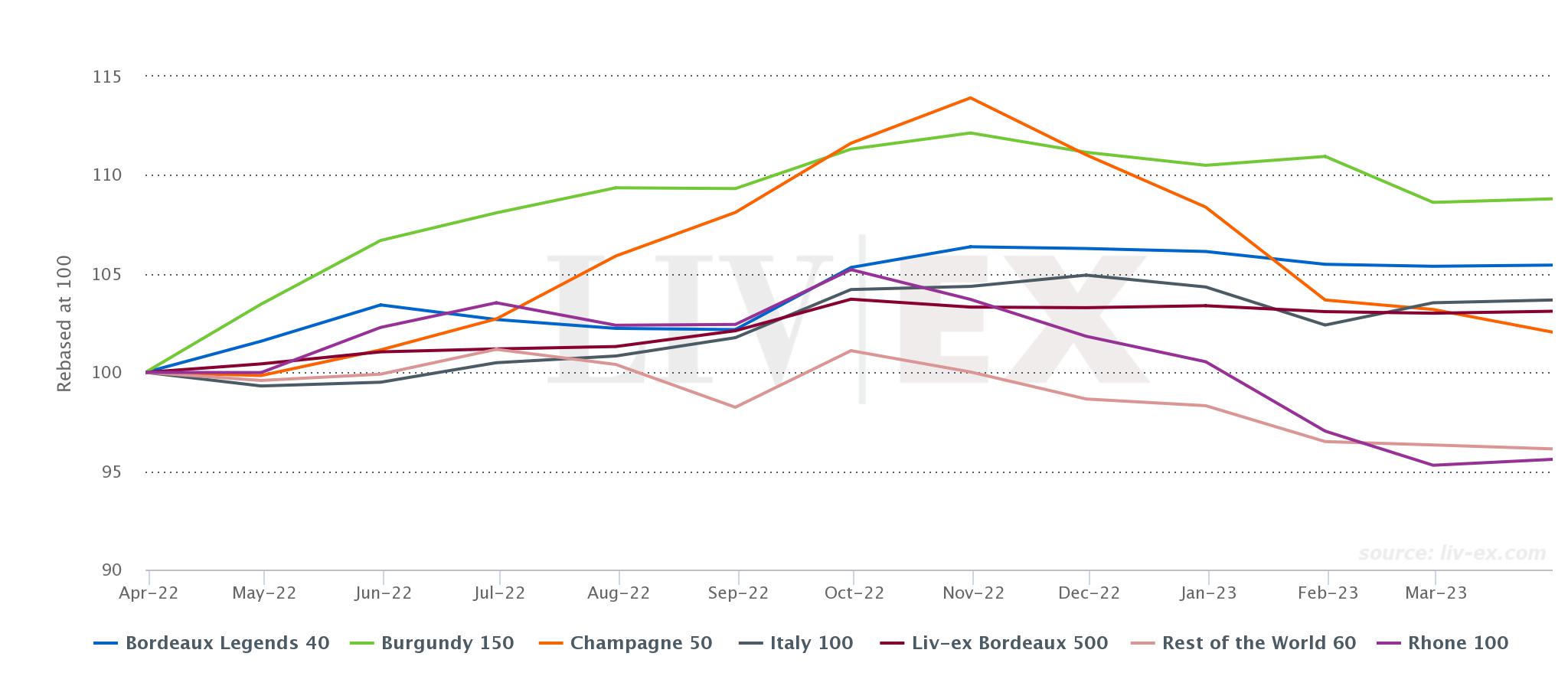

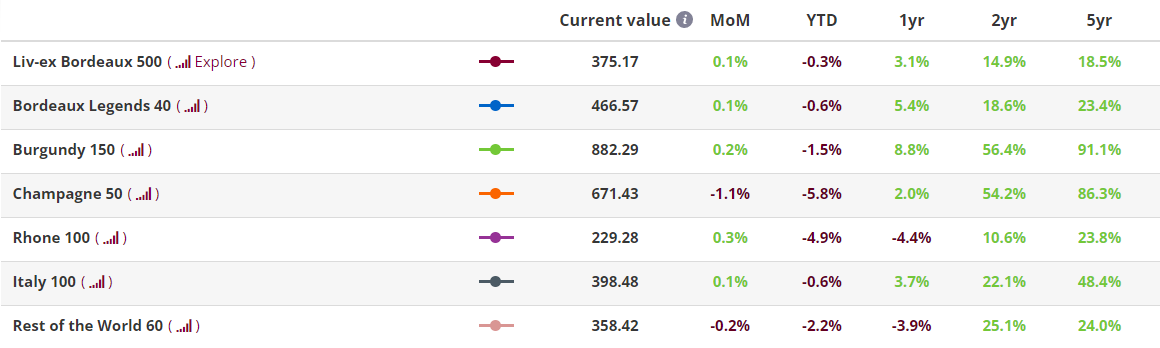

The Liv-ex Fine Wine 1000 index tracks 1,000 wines from across the world and is our broadest measure of the market. It comprises seven sub-indices which represent the most traded wines from regions around the world: the Bordeaux 500, the Bordeaux Legends 40, the Burgundy 150, the Champagne 50, the Rhone 100, the Italy 100 and the Rest of the World 60.

*Made using the Liv-ex Charting tool. data taken on 12.04.23.

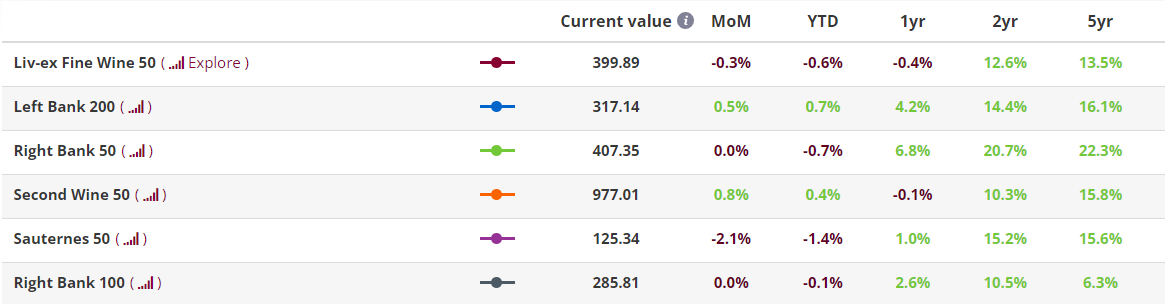

Compared to the wider market, Bordeaux has remained relatively stable in terms of price performance. Although the Burgundy 150 sub-index rose the most over the past year (8.8%), its performance is largely explained by a strong Q2 in 2022 (the index has fallen 3% since October 2022).

However, it is notable that the Bordeaux Legends 40 sub-index (which tracks a selection of 40 Bordeaux wines from exceptional older vintages), is the second-best performer over one year, up 5.4%. The Bordeaux 500 is also up 3.1% over the same period.

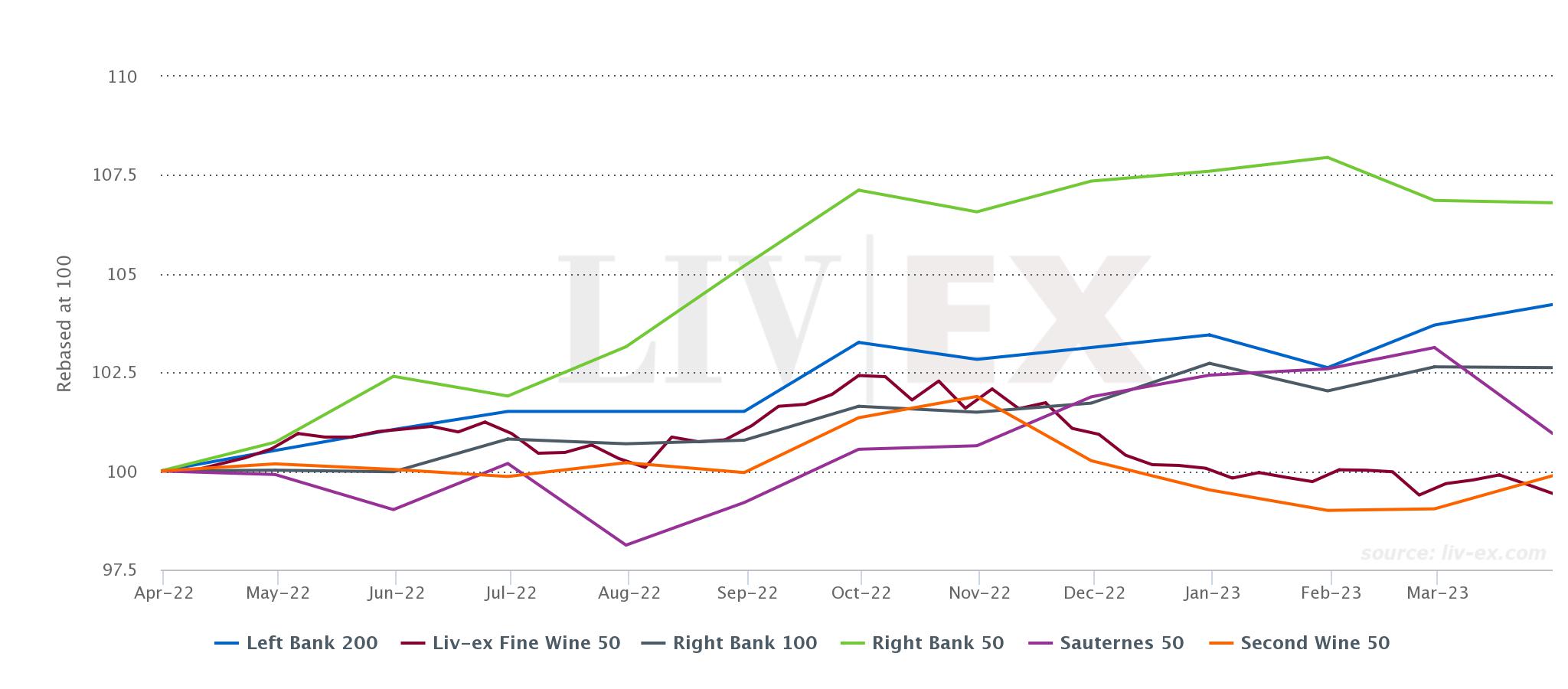

Like the Liv-ex 1000, the Bordeaux 500 index is also comprised of several sub-indices. Of these, the Right Bank 50 has been driving its performance over the past year and is up 6.8%. It is followed by the Left Bank 200, which rose 4.2% over the same period.

You can download the list of wines included in each index here.

Year-to-date, all Liv-ex 1000 sub-indices are down. However, the Bordeaux 500, which tracks the price movement of 500 leading wines from the region, has fallen the least (-0.3%).

*Made using the Liv-ex Charting tool. data taken on 12.04.23.

What’s driving the Bordeaux 500 indices

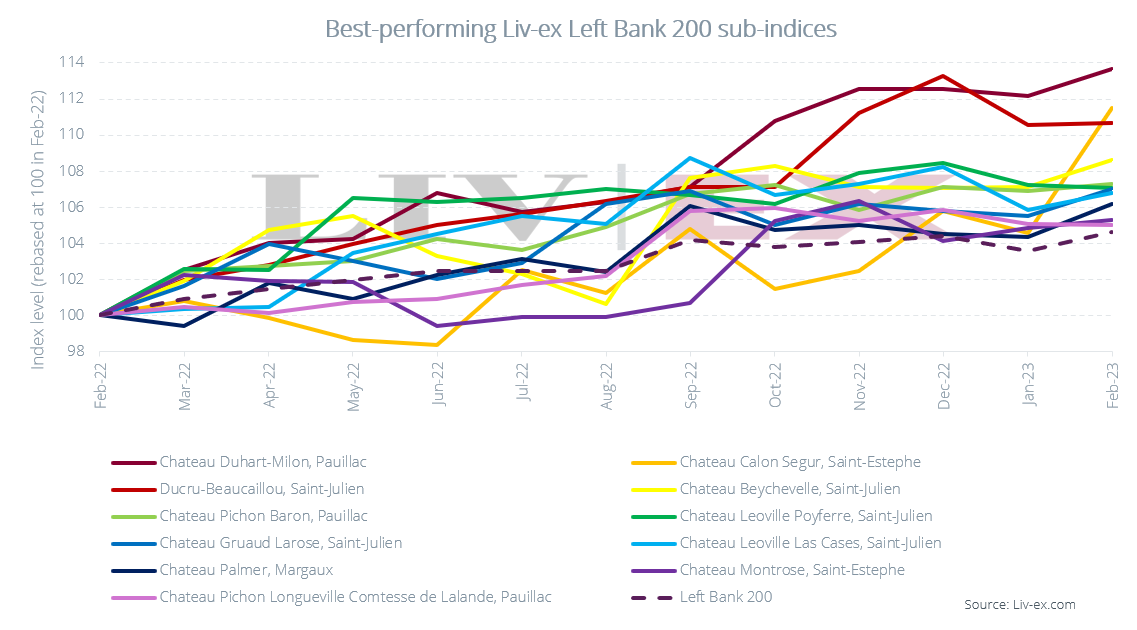

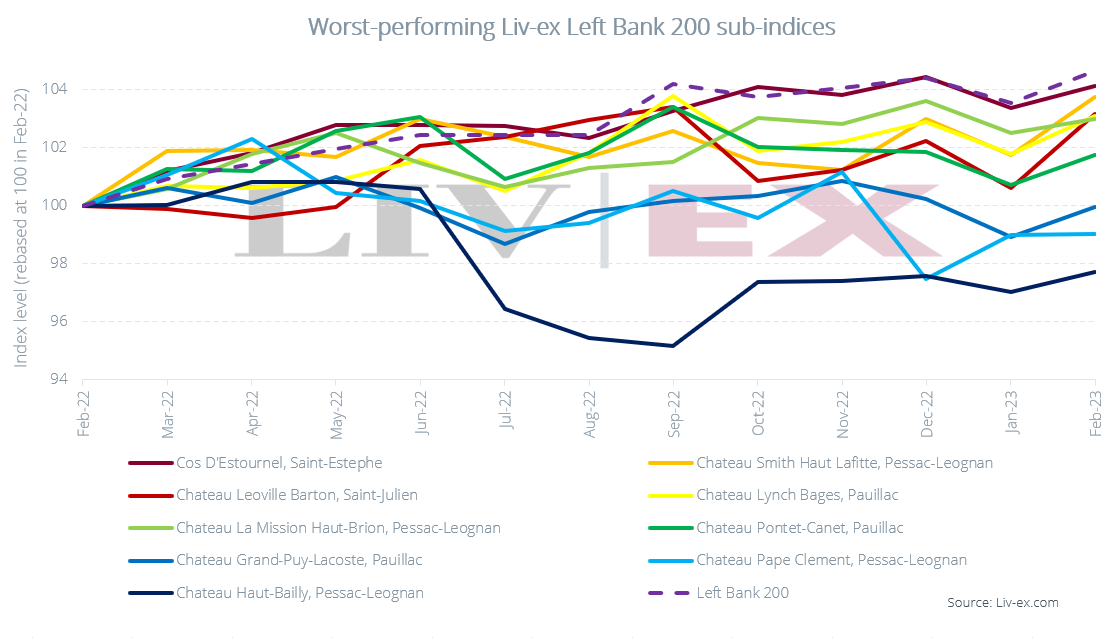

Among the Bordeaux 500 sub-indices there have been several standout performers over the past year. The charts below show the price performance of the wines included in the Left Bank 200 along with the Right Bank 50 and Right Bank 100 indices.

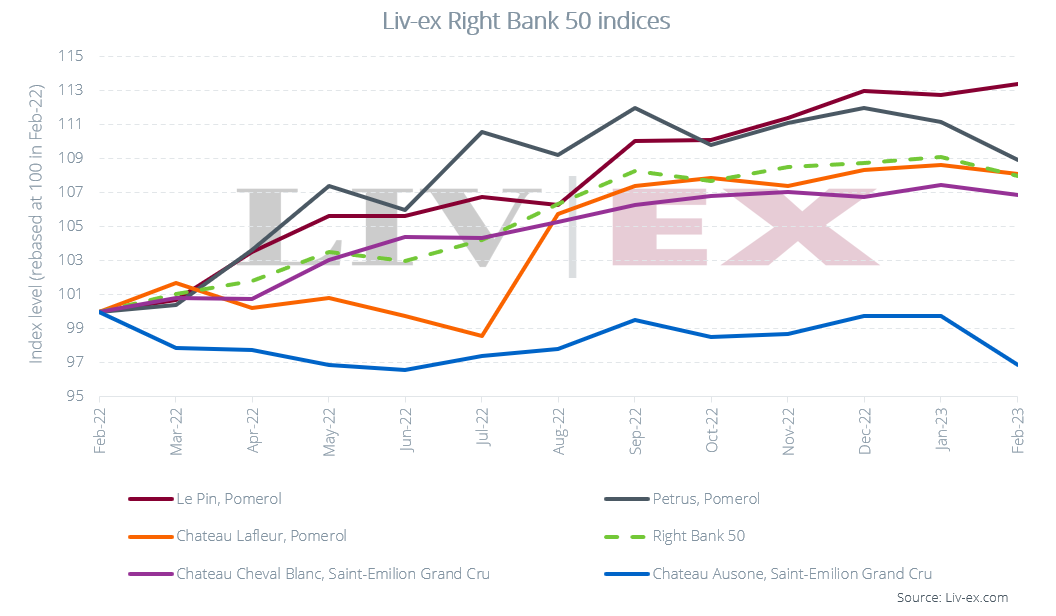

As mentioned above, the Right Bank 50 has been the top-performing sub-index of the Bordeaux 500 over the past year (6.8%). Among its components, Le Pin has seen the greatest price increases on average (13.4%), followed by Petrus (9.0%). As the chart below shows, both of these wines have outperformed the broader Right Bank 50 index.

*the indices in the chart above are calculated using the Liv-ex Mid Price.

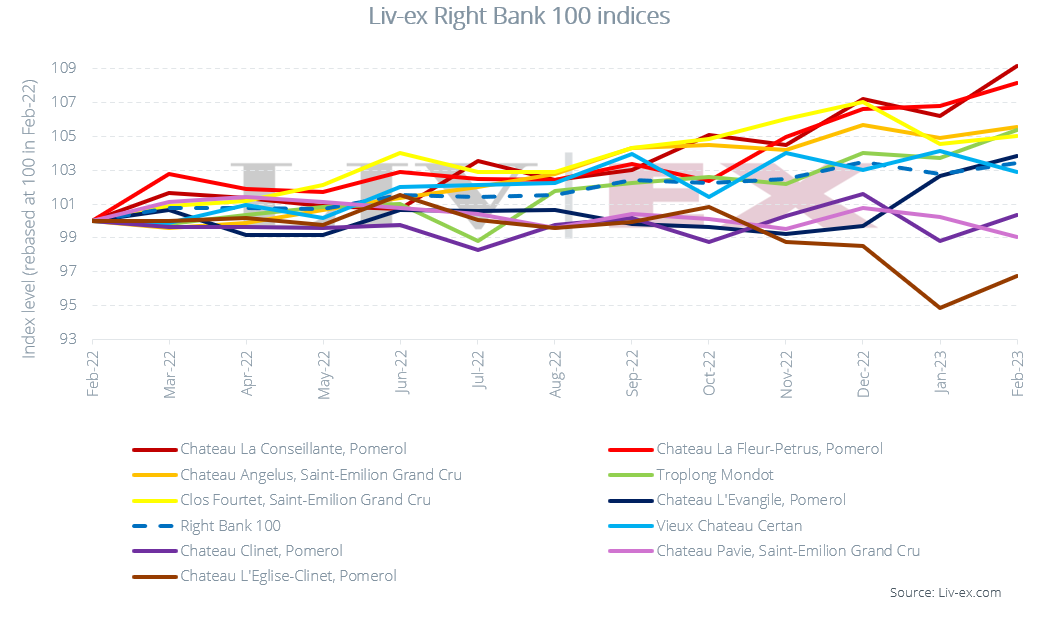

In the Right Bank 100 index, La Conseillante (9.2%), La Fleur-Petrus (8.2%), Angelus (5.6%), Troplong Mondot (5.4%), Clos Fourtet (5.0%) and L’Evangile (3.8%) have all outperformed their parent index over the past year.

Due to the number of wines in the Left Bank 200 index, we have split their component wines across two charts: those that outperformed their parent index and those that didn’t.

Among the top-performers, Duhart-Milon (13.7%), Calon-Segur (11.5%) and Ducru-Beaucaillou (10.7%) stand out. All these wines have significantly outperformed their parent index, which is up 4.7% over the same period.

Meanwhile, several wines have not seen the same price rises as their peers. The chart below shows the wines that have been lagging behind the Left Bank 200 index over the past year.

Although these wines are underperforming compared to their parent index, they might point to potential value within the region.

Looking at the chart below, Grand-Puy-Lacoste (0.0%), Pape Clement (-1.0%) and Haut-Bailly (-2.3%) are the wines to keep on the radar.

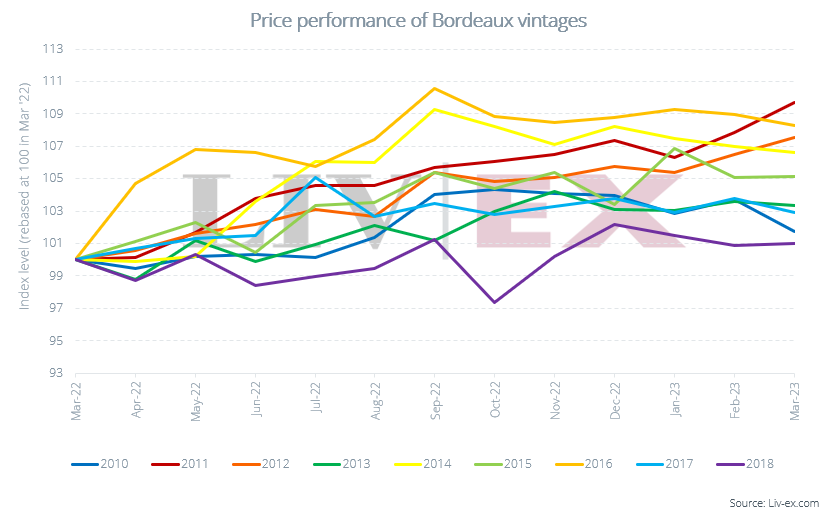

How have recent vintages performed?

Over the past year, all the Bordeaux vintages shown in the chart below have risen in value. The 2011 vintage has seen the biggest price rise, up 9.6%. It is closely followed by the 2016 vintage (8.2%) and 2012 (7.5%).

By comparison, the 2018 and 2010 vintages have risen the least. Both vintages are up 1.0% and 1.7% respectively.

En Primeur – a changing system

Importance of Critics

Critic scores have always played a significant role during En Primeur, especially since the invention of Robert Parker’s 100-point system in the 1970s. Due to the colossal influence that Parker had over the Bordeaux market (and by extension En Primeur), the news in 2015 that he would give up tasting en primeur left uncertainty in the trade.

As a result, Neal Martin (Wine Advocate’s Burgundy, Oregon, South African and Beaujolais critic) was announced as Parker’s En Primeur replacement. But after two years as the Wine Advocate’s leading Bordeaux critic, news broke in late 2017 that Neal Martin would be joining rival publication Vinous as their senior editor. However, in the press release, Vinous noted that both Martin and Galloni would ‘each write separate, independent reports on the wines of Bordeaux, including en primeur’.

In 2019, Parker finally announced his retirement from the Wine Advocate. At the time of the news, Meininger’s International wrote that it is ‘unlikely that any critic will ever again have such enormous power’. Wine Anorak also reported that ‘the future lies with a range of critics, each with their own audience, rather than one kingmaker.’ Indeed, the critical landscape around En Primeur has evolved from one kingpin to several key voices. Today, Liv-ex monitors the En Primeur scores of 16 leading critics (via our critics scores grid).

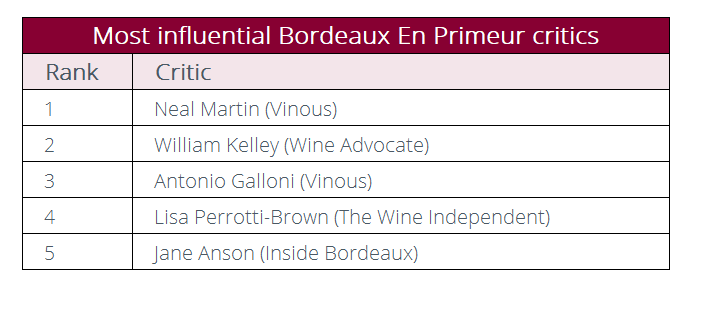

The most influential Bordeaux critics

In last year’s annual En Primeur survey, we asked Liv-ex members to list in order of preference the critics that will have greatest influence on their – and by extension their clients’ – buying decisions.

Neal Martin (Vinous) topped the rankings as the most trusted Bordeaux En Primeur critic. The second spot was taken by William Kelley, who wrote his first Bordeaux En Primeur report for the Wine Advocate in 2022 after Lisa Perrotti-Brown MW (the Wine Advocate’s previous Bordeaux reviewer and Editor-in-Chief) moved to her new venture, The Wine Independent.

Antonio Galloni (founder of Vinous and previously at the Wine Advocate) ranked third, while Lisa Perrotti Brown MW ranked fourth. Another newly-independent critic, Jane Anson (previously at Decanter), took the fifth spot.

*taken from the results of last year’s Bordeaux En Primeur survey.

With Liv-ex APIs, your system can instantly receive the most up-to-date scores and tasting notes from leading critics

Liv-ex’s ‘Fair Value’ methodology

Liv-ex’s ‘Fair Value’ methodology is a useful approach to pricing wines. It uses regression analysis to measure the relationship between price and quality and establish the fair price of a wine based on its critic score and vintages already available in the market.

Historically, it showed ‘Benchmark Critic’ scores (i.e. Robert Parker from 2005-2012 and Neal Martin from 2013-present) which were designed to consider both Parker’s continued influence and the changing face of wine criticism.

But with Robert Parker now long retired and considering Neal Martin’s position as the most influential Bordeaux En Primeur critic, this year our release posts and the Fair Value Tool will cover the most recent Neal Martin scores from the 2012-2022 vintages.

That said, to reflect the ever-increasing critical landscape, our Fair Value Tool has been updated so that members can filter between their favourite critics.

The tool now includes the following critics and publications: Neal Martin (Vinous), Jane Anson (Inside Bordeaux), Wine Advocate, Wine Spectator, Antonio Galloni (Vinous), James Suckling, Jeb Dunnuck, Lisa Perrotti-Brown MW (The Wine Independent).

We also refer to multiple opinions in our release analysis posts to give a broad and balanced context for understanding new releases.

*taken from the Liv-ex Fair Value Tool.

The Fair Value tool also allows you to view the charts in real-time and in multiple currencies: GBP (12×75), EUR (1×75) and USD (1×75). The tool is exclusively available to Liv-ex members on Silver packages or higher.

The world’s most comprehensive database of fine wine prices at your fingertips…

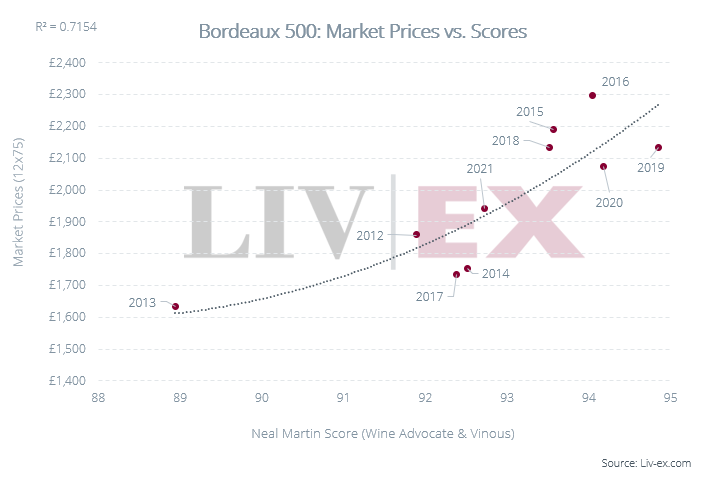

Where to find value in Bordeaux

The following chart assesses the wines in the Bordeaux 500 index using our ‘Fair Value’ methodology. As you can see, the average Neal Martin scores for these 500 wines are 71.5% correlated to their average Market Prices.

The methodology hypothesises that, over time, wines will converge toward their ‘Fair Value’ price. Typically, though not always, the most ‘undervalued’ wines provide the best returns as the price moves up to ‘Fair Value’ in the secondary market, whereas ‘overvalued’ wines provide the worst return.

As the chart shows, several vintages fall below the trendline, indicating that they might provide the best returns. With average scores of 92 and 93 points respectively, the 2017 and 2014 vintages offer relative value. By contrast, the 2015, 2016 and 2018 vintages all lie above the line.

Both the recently released 2020 and 2019 vintages also fall below the line. Given their higher average scores of 94 and 95 respectively, buyers might want to compare the hotly-anticipated 2022 releases to these vintages when pondering their value.

*Average scores are the most recent Neal Martin scores (from Vinous and the Wine Advocate) for the 500 wines found in the Bordeaux 500 index. Prices shown are the average Liv-ex Market Prices. The Market Price is the best listed price for a wine in the secondary market. Unless otherwise stated, it is standardised to 12x75cl.

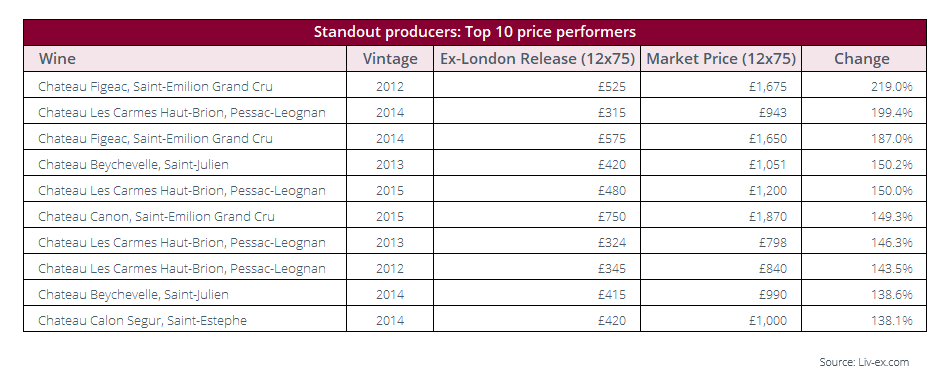

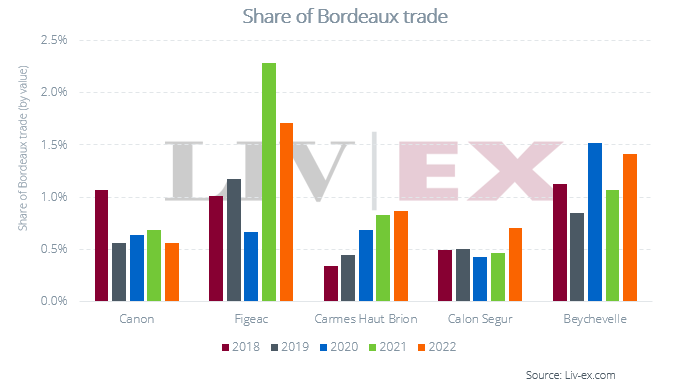

Standout producers from recent campaigns

There is a general sense amongst the trade that certain Chateaux have become increasingly popular in recent campaigns due to their successful release pricing. Indeed, in recent conversations with several Liv-ex members*, the following wines were listed as ‘strong sellers every year’.

These producers include, but are not limited to; Chateaux Canon, Figeac, Carmes Haut Brion, Calon Segur and Beychevelle.

Without doubt a major reason for their success is due to investments the estates have made in recent years. In 2015, Figeac started a major renovation and modernisation of its cellars which allowed for the complete plot-by-plot vinification, which was completed in 2018.

Similarly, Les Carmes Haut-Brion ‘instigated a long-term investment program’ in 2010 following its purchase by Patrice Pichet. In a recent article for Vinous, Neal Martin wrote that the program ‘might be considered extravagant for such a bijou estate with a modest reputation. But it paid dividends since Les Carmes Haut-Brion became a hotbed of new ideas and an alternate way of thinking’.

The increase in the quality of wines produced at these estates, combined with carefully considered release prices, has been crucial to their success. The result has been impressive price rises post release, building an enthusiastic and loyal collector base.

When looking at their past 10 vintages, some of the top-performing vintages from these labels are up over 150%. Figeac 2012 and 2014, for example, are both up 219% and 187% respectively, while Les Carmes Haut-Brion 2014 is up 199%.

It is interesting that the majority of the top-performers are from the 2012, 2013 and 2014 vintages, not considered amongst the great vintages, but judged, over time, to offer relative value.

* Seven Liv-ex members from four countries were questioned about their thoughts on the upcoming En Primeur campaign.

*Based off the 2012-2021 vintages of the following wines: Chateau Canon, Figeac, Carmes Haut Brion, Calon Segur, and Beychevelle. Market Prices taken on the 31.03.2023.

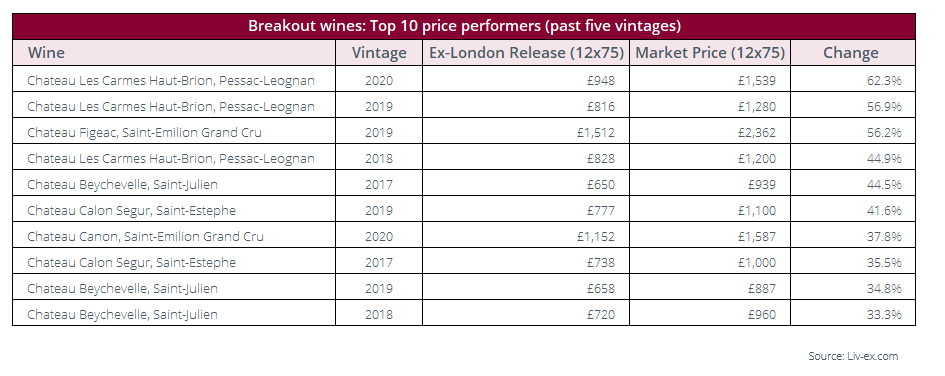

But top vintages too, have performed well. Looking back at our closing reports from the five most recent campaigns, several of these producers released at prices below the Fair Value line, offering their growing collector base a continued incentive to buy. As such, many of their 2018, 2019 and 2020 vintages have also seen strong returns.

*Based off the 2017-2021 vintages of the following wines: Chateau Canon, Figeac, Carmes Haut Brion, Calon Segur and Beychevelle. Market Prices taken on the 31.03.2023.

It is worth noting that several of these wines have seen increased secondary market trade as a result of a string of successfully-priced En Primeur campaigns. Calon Segur and Beychevelle saw noticeable jumps in their secondary market trade in 2022. Meanwhile, Carmes Haut Brion has seen consecutive year-on-year increases.

RRPs and supply chain margin

The uneven distribution of margin

Historically, En Primeur was designed to provide Chateaux with much needed cashflow. The idea was that by selling the wines before they were ready, the Chateau would have enough cash to sustain its business should the upcoming vintage prove difficult.

While the system remains hugely important for most of the region, for some of the top Growths, cashflow is less of an issue these days – especially given that many are now owned by global businesses.

LVMH, for example, owns Chateau d’Yquem and Cheval Blanc, while French insurance company AXA Millesimes owns Chateau Pichon Baron. The companies reported 2022 full-year revenue of €79.2 billion and €102 billion respectively.

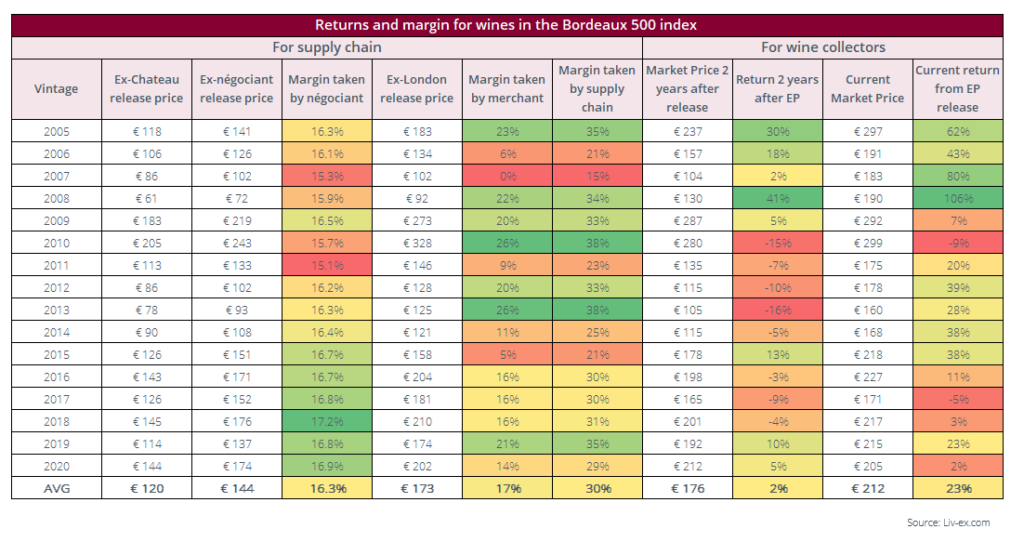

The table below shows the average returns and margins found at each point in the supply chain. Prices have been converted to euros per bottle, with the exchange rate taken at the time of the campaigns (June) to avoid currency fluctuations.

*Prices shown are Liv-ex prices converted to € per bottle. The exchange rate was taken at the time of each campaign (June) to avoid currency fluctuations. For more on Liv-ex prices, click here.

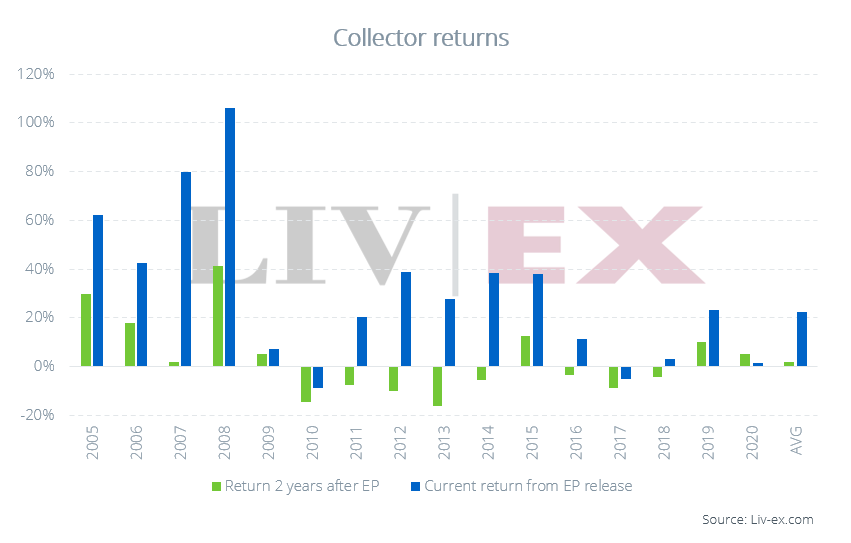

On average, En Primeur returns have been positive, with collectors taking average returns of 2% (when their wines were sold two years after each campaign) and 23% (if sold today) over the past 16 campaigns.

However, as the colour scale shows, not every campaign has been successful. In fact, collectors have seen only modest returns since the 2008 vintage. The numbers do not include the cost of insurance and storage.

Of the 2010-2020 vintages, the best ones to buy were the 2012 (39%), 2013 (28%), 2014 (38%), 2015 (38%) and 2019 (23%). 2012-2014 were released into the gloom following China’s withdrawal from the EP market, while the 2019 vintage was released into the eye of the Covid storm when uncertainty stalked the globe.

By comparison, 2009 (7%), 2010 (-9%) 2017 (-5%), 2018 (3%) and 2020 (2%) saw losses or very poor returns, despite relatively benign market conditions.

Introduction of Recommended Retail Prices (RRPs)

Along with the evolving critical landscape, a noticeable change to En Primeur in recent years has been the introduction of Recommended Retail Prices (RRPs).

RRPs were introduced by the Chateaux with the 2017 vintage in an attempt to control the price that their wines were sold at throughout the supply chain. In theory, the Chateaux set the price that trade can sell on the wines to the consumer.

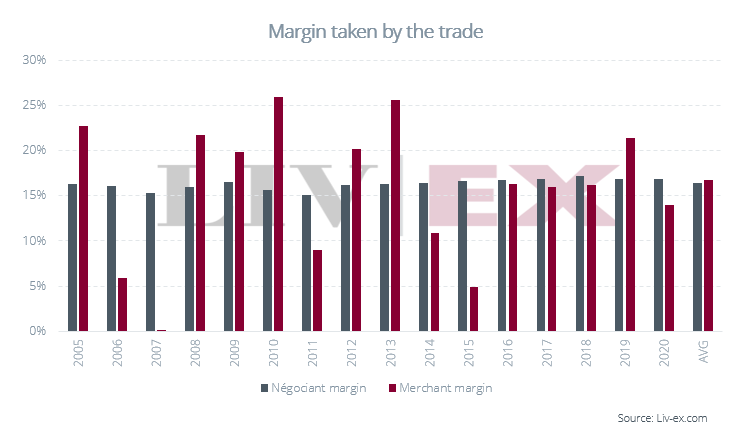

This introduction has been a victory for the trade but not necessarily so for the collector. As the charts below show, there has been a clear shift since the 2016 vintage (just before RRPs were introduced). Since then, merchants in the supply chain have taken average margins of 17%. Négociants’ margin has remained stable since 2005.

In a recent article on Jancis Robinson’s website, RRPs were linked to price fixing in the UK. They wrote that:

‘RRPs and MRPs appear regularly in en primeur offers or on exclusive wines issued by many importers. And while an importer may not take any action to ensure it is adhered to, many retailers do not dip below the RRP/MRP because they do not recognise the unenforceability and illegality of such a floor price and stay above that price ‘in fear’, when, in many cases, they could sell far more if they dipped below. Indeed, what they do not realise (but the CMA make very clear) is that a retailer complying with an MRP is also breaking the law – this is effectively the first step to a cartel.’

The collector (the ultimate provider of capital to the EP system) has been less fortunate when it comes to returns on their capital. The story since 2016 has been one of particular concern. Buying each vintage has yielded an average return of 7% (without 2019 it would be closer to 3%). By contrast, since 2016 the SP500 has risen 75%, Gold 57% and the CAC 47%.

Anecdotal feedback from merchants* suggests that the Bordelais are confused as to why retailers are selling wines below their designated RRPs even though the trade is making higher margins. But many are forgetting that the consumer doesn’t always want to buy at this price. Indeed, wines from the 2021 campaign found their way onto the secondary market with reductions of up to 15% on their original offers. It is also worth noting that the average bid prices for the wines were 23.7% lower than the release prices.

* Seven Liv-ex members from four countries were questioned about their thoughts on the upcoming En Primeur campaign.

Buy and sell with speed and confidence from and to the largest pool of trusted merchants worldwide…

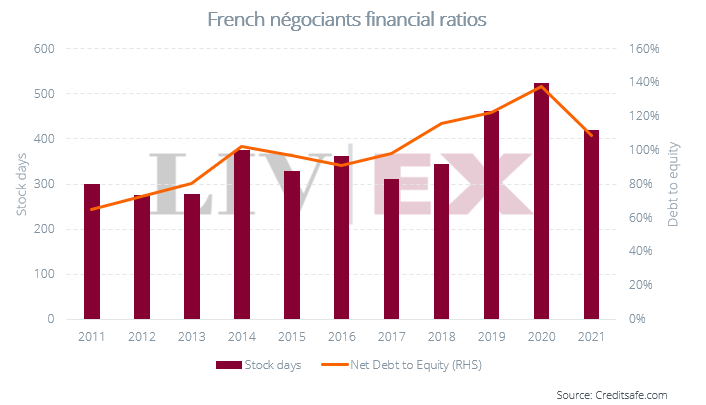

Varying risk profiles for négociant and merchants

Whilst the margins have remained strong, the balance sheets of negociants and merchants demonstrate materially different risk profiles.

One on hand, although there have been improvements compared to 2019 and 2020, négociants remain highly levered (109% debt to equity ratio in 2021) on the back of significant stock holdings (stock holding days of 420 days in 2021).

Over the past 15 years, with the benefit of low interest rates, these leverage levels were of little concern. However, with interest rates in the Eurozone currently at 3.5% and forecast to rise further, large stock holdings and low stock turn may no longer be the profitable strategy it once was.

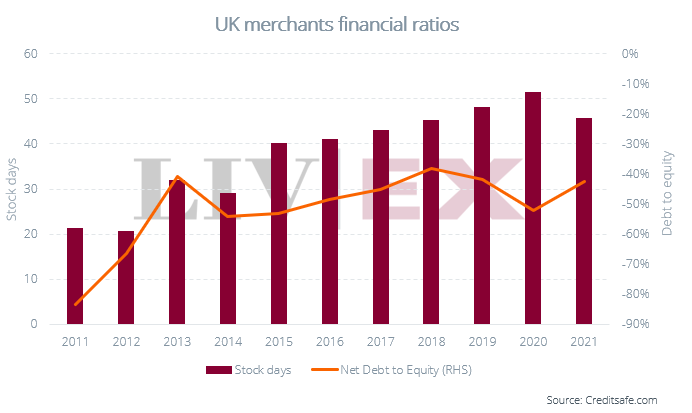

UK merchants by contrast have remained in a net cash position (negative 42% debt to equity ratio in 2021) with a low stock holding (stock holding days of 46 days in 2021). Engaging the UK merchants (and their client bases) would certainly seem a sensible strategy for this upcoming campaign.

Stock retention

Another ongoing En Primeur trend in recent years is the declining volume of wine released onto the market by the Chateau.

Even back in 2016, Liv-ex noted the shift in producer strategy in our En Primeur closing report:

‘There has been a sea change in strategy amongst the owners of top chateaux in the last 10-15 years. Priorities have shifted from making sales and generating cash flow to trying to maximise prices (of the grand vin in particular) and by extension the capital value of their properties. Indeed, with top Bordeaux real estate earning yields of less than 1%, the motivation to generate profits is dwarfed by that of keeping land values high. This has been challenging in the face of falling demand.

Owners have achieved this by releasing smaller quantities onto the market and spreading their production across a second and sometimes a third label. This trend which started with the First Growths, has spread to almost all labels, with Batailley and Clos Marquis being the latest to adopt the idea.’

Summary of changes

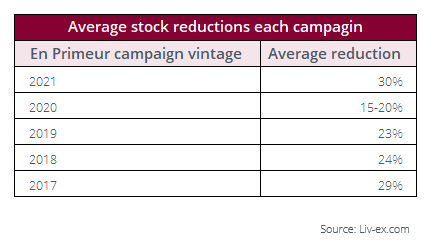

We went back through the past seven ‘closing reports’ that Liv-ex publishes after each En Primeur campaign and collated the changes in stock coming to the market each year.

The table below shows the average and/or a rough estimate of the volume of stock that came to market during each En Primeur campaign.

As you can see, the volume of stock coming to market has dropped roughly between 15-30% every year for the past five years.

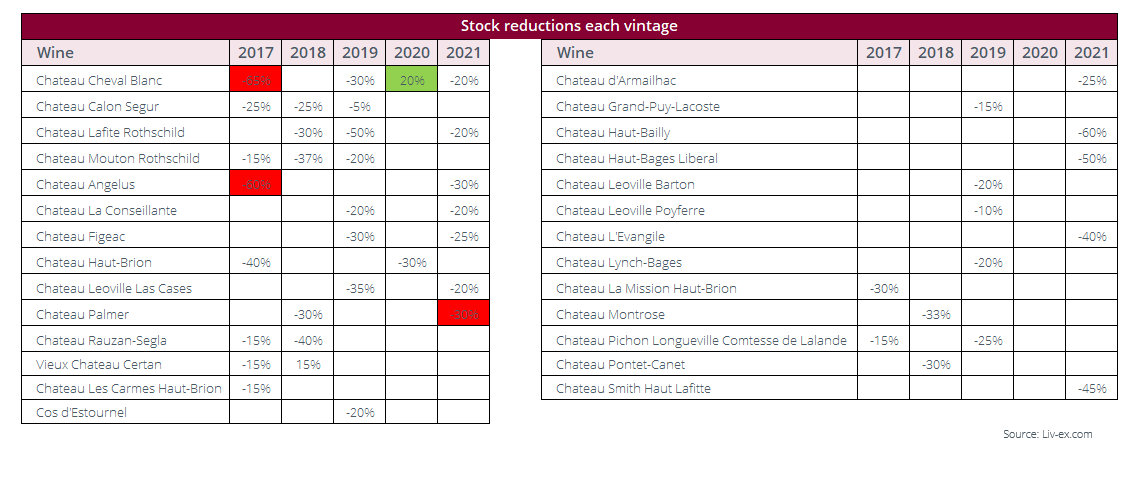

The next table is far from comprehensive but increasingly indicative of the strategy adopted by many producers. The producers are included in the table below in no particular order but happened to feature in the closing report Liv-ex produced that year (with the exception of the 2021 vintage where internal data was collected by Liv-ex throughout the campaign). It is important to note that in some instances stock reductions were a result of low yields.

*reductions shown in red were due to drops in production volume. The green shows an increase in stock coming to market that year.

Rising costs of production

So why have some Chateaux adopted this new strategy? For some it is necessary to protect themselves from the rising costs of production. The impact of inflation on input costs has been felt across the industry – whether it be staff, packaging or services. The rising cost of energy has meant that glass prices have increased. Some U.S producers reported that glass bottles had risen by as much as 20%, while mixer producer Fever-Tree expects to pay £20 million in energy-related glass fees in 2023. According to ProWein’s Business Report, supply of glass bottles is the dominant problem in the wine industry in 2023 and caused problems for 92% of producers.

Wine News Italy also reported that the increased cost of all ‘dry’ raw materials (glass, paper, capsules, cages, cartons, corks and so on) was impacting the industry more than the energy crisis. They reported that by the end of 2022, the production chain will have incurred costs 83% over budget and that in 2023, an additional 20% increase is already planned to cover glass.

However, it is worth noting that the average bottle of AOC Bordeaux is estimated to cost around €2.88 to make (sources: Vineyard intelligence and Jancis Robinson). Given the 50 producers that make up the Bordeaux 500 index are selling their wine (on average) for €120 per bottle ex-Chateau, their margin is still the greatest of them all – at roughly 97.6%.

As such, this inflationary impact mentioned above is felt far more severely at the lower end of the market where margins for the grower are already tight. It is of far less relevance to those producers at the very top end of the tree.

Volatile production volumes

The past few years have also seen volatile production figures for many growers. In 2016 Bordeaux recorded its largest harvest since 2006, but in 2017 many saw their crops decimated by frosts, leading to the smallest harvest in France since 1945. As shown in the table above, Cheval Blanc and Angelus released 65% and 60% less stock respectively that year as a result of the frost.

In 2018, production was back to its 10-year average, but hailstorms caused damage in some unlucky areas. Gavin Quinney reported that it would be remembered as one of the greatest vintages by some but with dismay by others. Yields then fell in 2020 due to heat and drought and again in 2021 as a result of mildew.

As Gavin Quinney’s 2022 harvest report highlights, Bordeaux’s wine production has taken a marked hit over the past six years since its high in 2016 (see chart below).

Risk-averse business strategies

From a business perspective, it perhaps makes sense for the chateaux to withhold stock.

If they can afford to hold the stock for ten plus years they can then release their wine at its current market value, which in the case of the 2008, 2007 and 2005 vintages, is between 60-100% higher than the original release price. By doing this, the chateaux pocket the price increase rather than the collector.

But holding wine can be an expensive game. Not only does one have to factor in the costs of insurance and storage, but also one needs to have the capital required for 5-10 years of limited (to no) cash flow. If holding the stock is debt financed then the cost of debt (until recently, negligible) becomes an important factor. And then of course, prices need to rise consistently. Between 2011 and 2015 they fell consistently.

Criticism of the strategy

The withholding of stock from the market has been discussed in numerous reports and has become a regular debate amongst the international trade. Merchants who miss out on Bordeaux sales need to look to other regions to fill the void. This in turn negatively impacts the secondary market performance of Bordeaux, which in turn leads collectors to seek opportunities elsewhere.

Overpriced campaigns also have a detrimental effect. Several wines from the 2021 campaign found their way onto the secondary market with reductions of up to 15% on their original offers. Many of the 2010 releases are still under water. Several of the merchants we surveyed reported that they have reduced their involvement in En Primeur in recent years: one noted that they would be taking as little of 2022 as possible without tarnishing their relationships with négociants, while another agreed that for consumers it makes more sense to buy back vintages, which represent better relative value.

Some even go so far as to suggest the strategy is a form of price manipulation. As Neal Martin put it in his 2019 Bordeaux report, the consumer and the trade are in the dark as to how much stock the chateaux are holding:

‘Châteaux rarely if ever disclose the percentage of production released onto the market. How do you know whether 10% or 50% of this year’s crop remains unreleased? Which properties sell everything apart from bottles for their own private use and which keep back a large proportion to sell later at price where they don’t have to grit their teeth? Your guess is as good as mine. It is designed to create an illusion of scarcity when Bordeaux is anything but. For sure, some properties are sitting on half their production, which they are perfectly entitled to do. I just wish they would be open about it.’

Whatever the truth, it seems that there is a continued belief among the chateaux that by squeezing supply, prices will rise. The problem here becomes one of market perception. If the market knows (or simply feels) that the supply exists but is not being offered, it will see it as an overhang and prices will struggle to rise.

Markets thrive on transparency. They are much diminished by opacity.

The future of En Primeur

So what does this mean for the future of En Primeur? The current system is very much geared towards the chateaux (it is their wine after all), who in turn are keeping the supply chain (relatively) happy by allocating them profits. But perversely, the ultimate supplier of capital to the system, the collector, is the ‘loser’ as the returns from buying and storing wines are gradually eroded.

Changing reasons for buying En Primeur

Feedback from Liv-ex members is that collectors are increasingly taking part in EP campaigns through habit, for the ‘experience’ or simply to request big bottle formats. Some noted that the next generation of buyers, far more used to transparency and free flowing information, are already growing skeptical of the process, particularly given the limited upside and opportunity cost involved.

There has been of course, a renewed interest in alternative assets in recent years. The rise of trading apps has opened the door to a much wider base of investors looking for alternative assets. But again, alternative asset classes do best when transparency and liquidity are present.

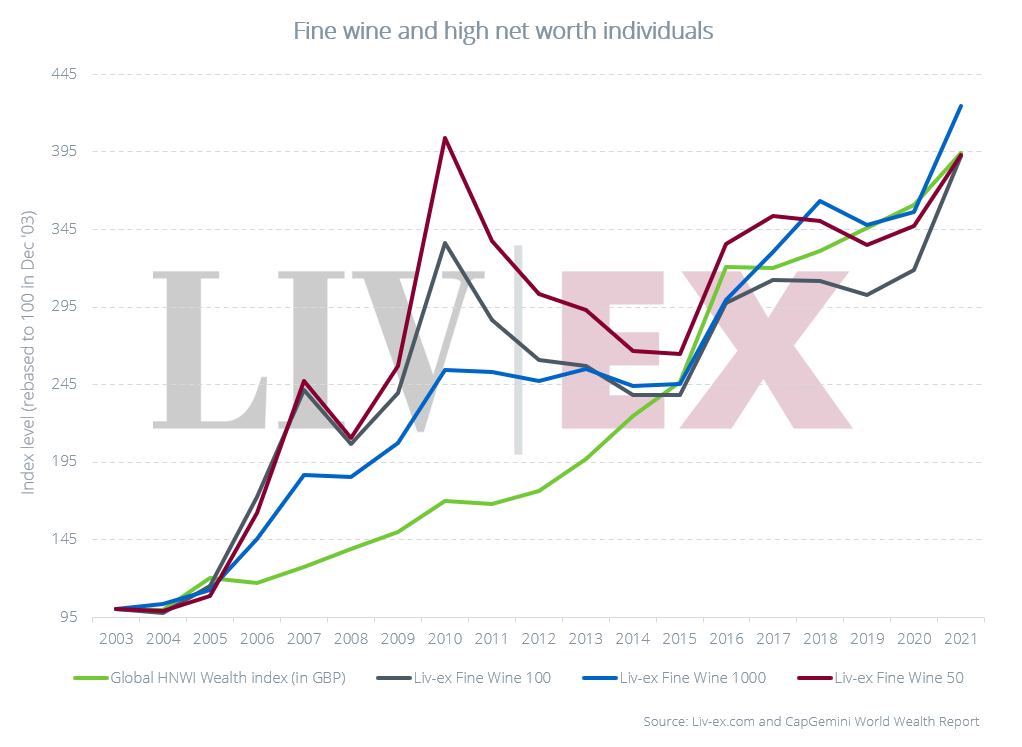

The combination of a massive injection of liquidity from central banks and the emergence of new technologies in 2020 and throughout 2021 bought a fresh influx of players – on a level not seen since the China-driven bull run of 2010.

This period saw enormous wealth creation and a significant increase in the number of high-net-worth individuals (HNWIs) who spent some of their new wealth on fine wine both as a genuine passion and as a viable investment.

Although the number of 2022 high net worth individuals is not yet available, 37% of Liv-ex members reported an increase in new customers in 2022.

The importance of this year’s campaign

If we assume that the consumer’s sole motivation for En Primeur is no longer to make a return, and the chateaux, négociants and the trade are all happy because they have been allocated margin, then what’s the problem?

Sentiment is everything. One only needs to look at the impact it plays in financial markets (especially of late with the collapse of SVB). Just as greed dominates during a boom, fear prevails following its bust.

As detailed in our Q1 2023 report, the fine wine market is currently in a delicate position. While the Liv-ex indices only suffered small declines in Q1, their performance masked some potential causes for concern. The Rhone 100 index, which is often considered one of the most stable regions in the fine wine market, recorded the second-biggest fall in the first quarter, at -4.9%.

With this uncharacteristic volatility in the market, it is perhaps unsurprising that the trade has been quite risk-averse year-to-date. The steady price action and rising trade for Bordeaux’s wines might suggest that buyers are returning to more familiar regions known for their stability and liquidity.

But caution remains the buzzword. As we enter the 2Q there are tentative signs that the fine wine market is emerging from its 1Q funk. Whether the Bordeaux 2022 campaign gives impetus to this sense of new life or stops it in its tracks is yet to be seen. The quality looks certain to be there. It now just becomes a question of price.

Early thoughts on this year’s campaign

When the global wine trade was asked for their predictions about 2023, their views on Bordeaux were mixed. An equal amount of respondents predicted that Bordeaux would have a successful or not-so-successful 2022 En Primeur campaign. One noted that high release prices will kill the campaign and drive demand for older vintages.

When questioned about their thoughts on the upcoming campaign, two respondents mentioned that they were taking part less and less in recent years simply because collector demand had diminished. Another would buy only against orders received, keeping company stock to a minimum.

By contrast, one merchant, who has been a long-term buyer of EP, saw no reason not to buy 2022. Indeed, quite the opposite, given the expected quality. Another noted that they were hiring a new Private Client Manager and doing more marketing for this year’s campaign.

Stay tuned. Liv-ex will also be publishing the findings of its annual En Primeur survey in early May with further analysis and feedback.

* Seven Liv-ex members from four countries were questioned about their thoughts on the upcoming En Primeur campaign.

How the secondary market can help price En Primeur wines

With excitement building around the quality of the 2022 vintage, this year’s campaign already seems to be holding more significance for the market than recent years. A well-priced campaign will be a boost to sentiment. However, an ill-judged one could add to the market’s broader concerns about the sustainability of prices going forward.

The secondary market is a vital tool for those wanting to price their wines successfully. Indeed, a recent article in the Journal of Wine Economics proposed an efficient pricing model for Bordeaux En Primeur wines, in which they exploit information from the secondary market to estimate efficient and effective release prices.

Chateau Cheval Blanc also reported that they use two main resources for pricing their wines during En Primeur, including secondary market data:

‘We rely on two main resources. Liv-ex data accurately reflects the business-to-business market. Specifically, we used the Liv-ex Fair Value tool. It helped us to position the release price against our other vintages in the market. We also received advice from Bordeaux brokers from La Place de Bordeaux, which is responsible for distributing the largest share of wine around the world. It is interesting how the two can differ when the market is shaken, or can tie in when the market knows where it is heading. We also look at retail prices online’.

The importance of pricing releases correctly

Cheval Blanc noted that‘a successful En Primeur campaign should combine commercial success with communication success. It should generate demand across geographies and lay the foundations for long-term price appreciation of our wines’.

Indeed, as we saw earlier in the report, those that price correctly can weather the storm of a ‘bad year’. Calon-Segur and Carmes Haut-Brion, for example, have seen strong price performance and their secondary market trade increase as a result of a string of successfully-priced En Primeur campaigns.

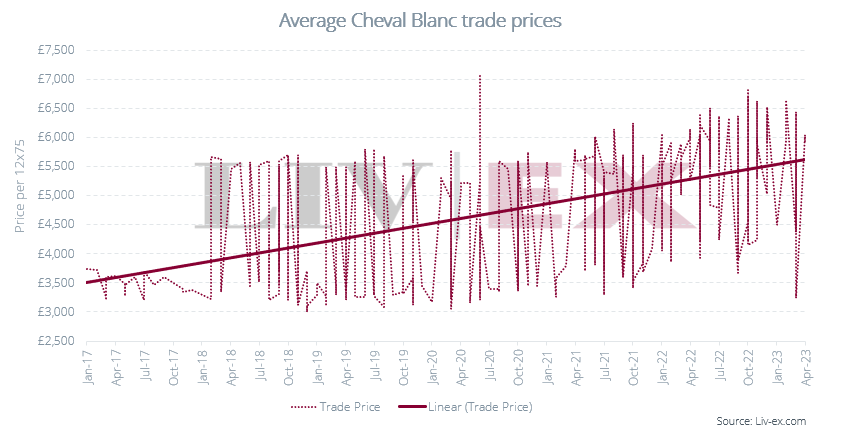

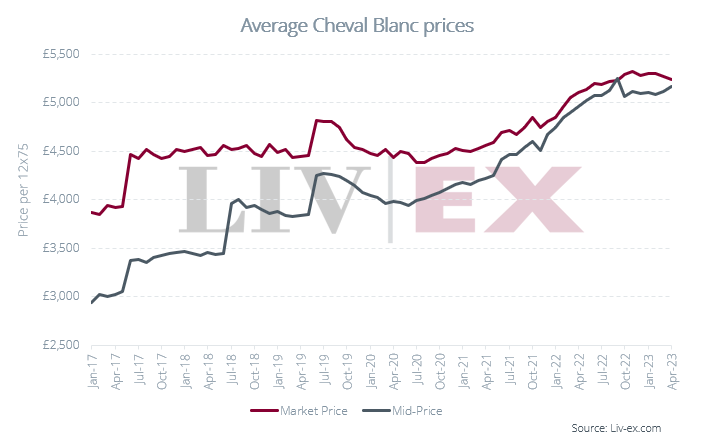

Since using the secondary market to benchmark their releases, Cheval Blanc’s secondary market trade has also increased. In 2020, Cheval Blanc accounted for 2.1% of Bordeaux trade by value. By 2021, this number stood at 2.4% and by 2022, at 2.6%.

Since 2017, Cheval Blanc’s average Trade, Market and Mid Prices have also steadily increased, as the charts below show.

Conclusion

2022 was a year of highs and lows for Bordeaux. While production was down 10% on the 10-year average, it marked an improvement on 2021 numbers and was notably higher than 2013 and 2017 yields.

Although heat and drought characterised the growing season, the vintage looks set to be one of the greats with many alluding to a vintage at least on par with 2010, 2016, 2019 and 2020. Some have even suggested 1961!

But like every year before it, market sentiment and pricing will be a key determinant in the success of this campaign.

Bordeaux’s secondary market has evolved considerably in recent years. Europe now accounts for almost half of all Bordeaux bought on the secondary market, with France leading the charge.

Bordeaux prices have remained remarkably stable over the past year or two while other regions have seen sharp rises and subsequent declines. While all the Liv-ex 1000 sub-indices are down year-to-date, the Bordeaux 500 has fallen the least (just 0.3% compared to the Champagne 50, which has fallen 5.8% so far this year).

Bordeaux’s performance has been buoyed by leading wines on the Right Bank and the Left Bank as a whole. Vintages that are entering their drinking windows have seen the greatest price increases.

However, the well-oiled machine that is En Primeur is evolving. Great change has been seen in the critics’ sphere since Robert Parker’s retirement from the Wine Advocate ten years ago. Today, rather than a single king maker, chateaux, negociants, merchants and collectors can choose from a wide variety of voices.

Thus, pricing En Primeur has become more challenging, as multiple voices impact release prices and buying decisions. This said, Liv-ex’s Fair Value methodology offers a useful guide to help navigate the releases, highlighting value (or not) in both the new releases and back vintages.

Growers whose wines offer value at release have been rewarded. In recent years, a select group of ‘breakout producers’ have won both the trade and the collector’s favour because of well-judged releases. Their wines have subsequently thrived in the secondary market.

The recent introduction of RRPs by chateaux in an effort to maintain margin throughout the supply chain has proved to be a double-edged sword. While their introduction guarantees profits for the trade, it does so at the expense of the collector. But the collector is becoming more savvy. As such, wines are going unsold, forcing merchants to quietly (post campaign) undercut these RRPs to reduce the risk of holding poorly priced stock.

Stock retention has become a more common strategy used by chateaux to create scarcity and hold prices up in less desirable vintages. While there are merits to this strategy from a grower’s point of view, it does not come without risk. It has come under scrutiny in recent years from well-regarded commentators and critics. And as far as behavioural economics is concerned, if the market knows (or simply suspects) that excess supply exists, it will be perceived as an overhang and prices will subsequently struggle to rise. Indeed, they might fall.

Ultimately the choice of whether to buy or stand aside lies with the collector. Those that are in it for the experience (and the choice of bottling format) might not be phased by all this, but to a new generation of informed collector who has experience and access to other markets and to whom transparency is not just commonplace, but fundamental to confidence, this might all seem too complex and risky an affair. Do they need to buy today, or can they afford to wait? Much of the data suggests the latter.

Even if the collector does bite, the Bordelais need to consider the impact that pricing could have on future campaigns. Already the generally over-priced release of Bordeaux 2021 has reduced the chateaux’ room for manoeuvre. With market sentiment mixed and the trade showing a high degree of risk aversion, even a great vintage such as 2022 is purported to be, will be no slam dunk.

The tools are there for the chateaux to price the wines with the collector in mind and provide a shot-in-the-arm to the fine wine market more generally. Not all will get it right, but collectors will be hoping the majority do. After all, it seems certain to be a vintage all serious collectors would like to own.

Find out how Liv-ex helps businesses enhance efficiency and improve margins…