Liv-ex January Market Report

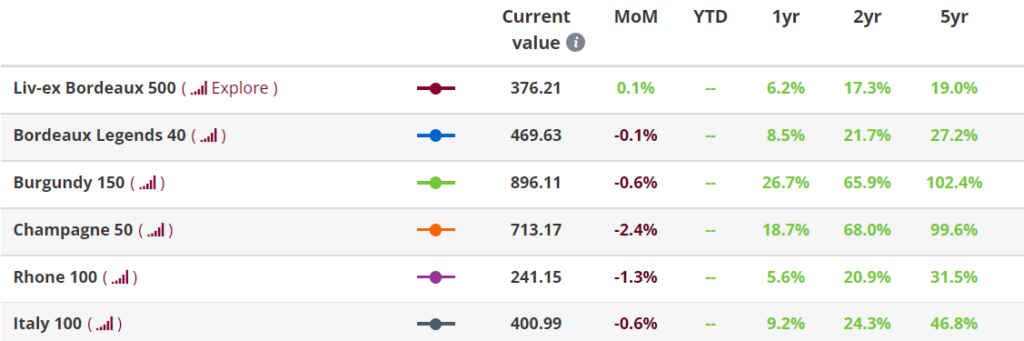

- All major Liv-ex indices drifted in December, bar the Bordeaux 500.

- The ‘Rest of the World’ (6.5%) and the USA (7.1%) saw substantial increases in trade share.

- Some of the best price performers came from Bordeaux’s 2011 vintage.

- Lisa Perrotti-Brown MW awarded Château Haut-Brion Blanc 2017 a 100-point score in a recent vintage retrospective report.

- The booming Champagne market in 2022 showed end-of-year jitters.

- The current bid-offer ratio, combined with indices declines, points to waning market sentiment in the beginning of the year.

Fine wine prices decline in December

2022 was a year of losses for mainstream equities. The S&P 500 fell around 20%, recording its worst year since 2008. The tech-heavy Nasdaq Composite Index closed at its lowest level since July 2020, while European stocks saw their worst annual run since 2018. This prompted investors to look for safe havens and fine wine once again proved its worth as an alternative asset. All Liv-ex indices rose in 2022, led by the broadest measure of the market, the Liv-ex 1000, up 13.1%.

However, fine wine did not manage to escape the wider economic reality entirely, suffering losses in Q4. The Liv-ex 100 drifted 0.2% in December, marking its third consecutive month of declines. The Fine Wine 50, which tracks the performance of the Bordeaux First Growths, dipped 0.8%.

The Liv-ex 1000 index fell 0.4% in December for second month in a row. All of its sub-indices declined, bar the Bordeaux 500, which rose just 0.1%. The Champagne 50 sub-index was the worst performer, down 2.4%. After months of gains on the back of soaring demand a pullback was perhaps inevitable.

Chart of the Month

Strong market share gains for RoW and the USA

The ‘Rest of the World’ (6.5%) and the USA (7.1%) saw some of the most substantial increases in trade share in December. Napa Valley was the main driver behind the USA, with Harlan Estate 2018 and Opus One 2019 being the most active wines.

Meanwhile, trade for the ‘others’ was led by Spain (0.8%) and Australia (0.6%). For the first time ever, a rum changed hands on Liv-ex – Trois Rivieres Vieux Rhum de Plantation de la Martinique 1953. In 2022, secondary market trade of spirits rose 131.5% on the previous year.

Bordeaux also increased its trade share, from 30.8% in November to 38.3% last month. Its 2019 and 2005 vintages were the most active by value.

Piedmont (3.0%) and the Rhône (3.5%) registered small rises, while Burgundy (22.8%), Tuscany (5.8%) and Champagne (13.0%) dipped.

Major Market Movers

‘Off’ vintage Bordeaux leads the market in December

As the only Liv-ex 1000 sub-index that stayed afloat in December, the Bordeaux 500 included some of the top price performers last month. The majority of these came from ‘off’ vintages 2011 and 2013. Château Clinet 2013 led the way within the region, with an increase of 14.3%.

A Sauternes also featured in the rankings, Château Rieussec 2010, up 13.6%. The wine last traded at £338 per 12×75.

The rest of the risers were Bordeaux 2011s: Vieux Château Certan, Calon Segur and Pichon Baron.

Overall, the 2011 Bordeaux vintage rose 9.4% in 2022, compared with a 6.2% move for the Bordeaux 500 index for the year.

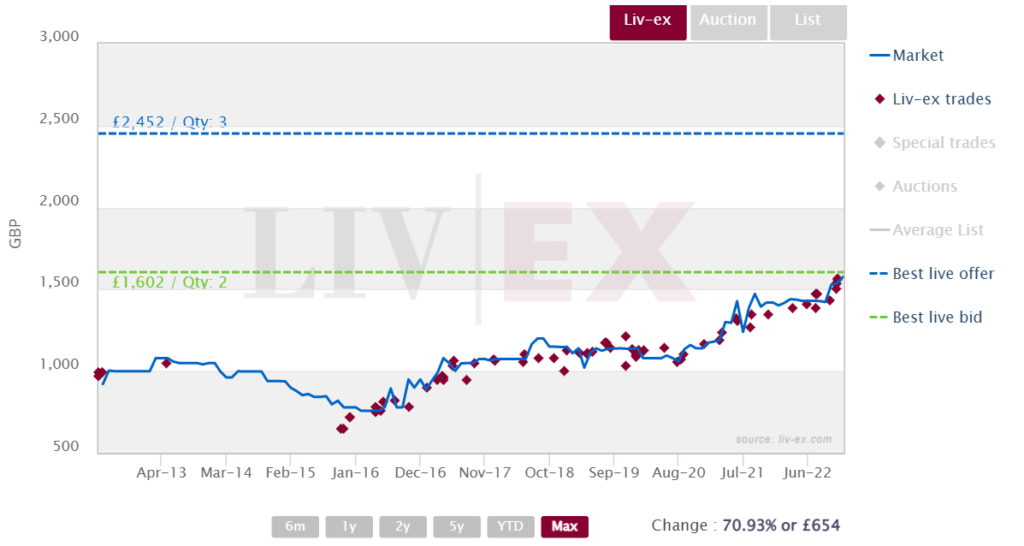

Vieux Château Certain 2011 also set a new trading high in December, when it changed hands at £1,562 per case. This represents a 47.4% increase on the wine’s release price.

Vieux Château Certan 2011 trades on Liv-ex

Critical Corner

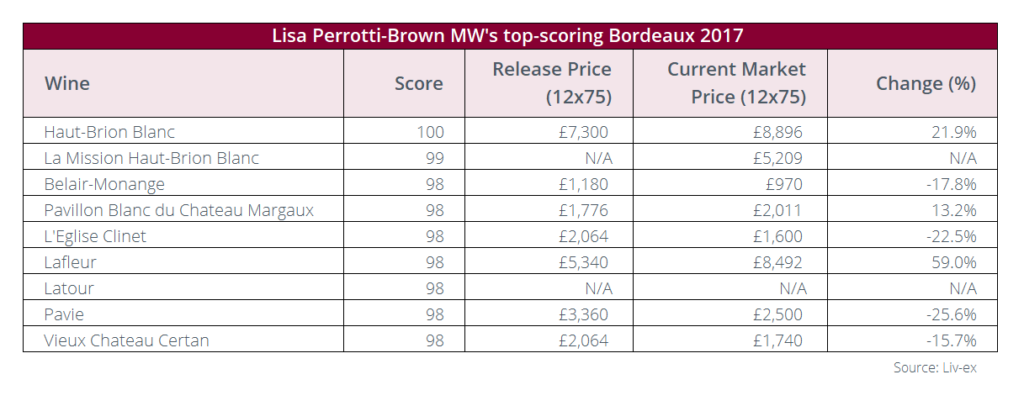

Lisa Perrotti-Brown MW’s Bordeaux 2017 retrospective

In 2022, Lisa Perrotti-Brown MW (The Wine Independent) conducted a series of retrospective Bordeaux tastings. Her latest report revisited the 2017 vintage, which she described as ‘the biggest surprise’ and ‘a face of Bordeaux that we have not seen in many years’.

According to her, ‘2017 is all about finesse and aromatic intensity, as opposed to brute power—a style some Bordeaux wine lovers will not want to miss’. Perrotti-Brown explained that ‘2017 is a far cry from either 2015 or 2016, both significantly warmer, sunnier vintages’.

While she found that ‘2017 is less consistently great than 2016, 2018, 2019, or 2020,’ she said that ‘dry white Bordeaux wines generally need a colossal shout-out this year’.

Indeed, her highest-scoring wines includes three whites, amongst which the only 100-pointer: Château Haut-Brion Blanc. The wine has risen 21.9% in value since release.

However, not all of her favorites have seen price increases. For instance, the 98-point Vieux Château Certan remains available at a 15.7% discount to release. The 2017 is one of the best value opportunities from the château on the market today.

Overall, 2017 was the ninth-most traded Bordeaux vintage by value and fourth-most active by volume last year. The most traded 2017s were Château Les Carmes Haut-Brion and Château Mouton Rothschild, while the best price performers – Pétrus and Château Suduiraut.

News Insights

Booming Champagne sales reflected in secondary market activity

2022 was the second-highest year on record for Champagne sales, with 331 million bottles sold, after 2007’s 338 million bottles. In December, David Chatillon, chairman of the Union of Champagne Houses (UMC) told Reuters that 2022 is expected to set a new record for turnover.

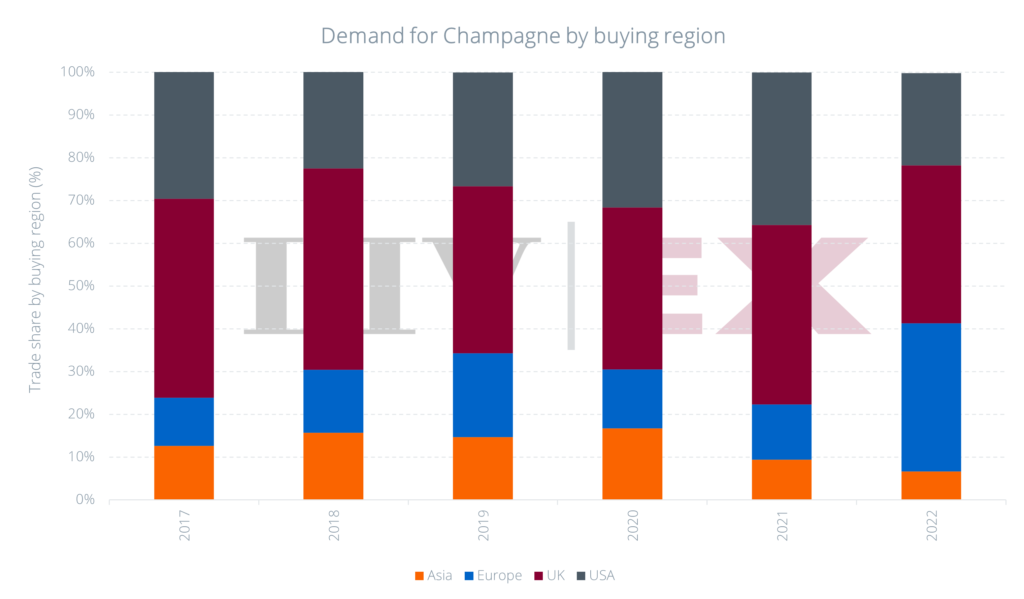

This booming demand was reflected in secondary market activity. Champagne’s annual trade share rose from 8.8% in 2021 to 13.6% in 2022, while prices increased 18.7%, as measured by the Chamapagne 50. Over the past 15 years Champagne trade by value on the secondary market has risen 32-fold.

According to a Liv-ex survey among its merchant member base, 40% of the respondents named Champagne as the most in-demand region in 2022. Its relative value compared to other regions and building momentum in the market were listed as key factors adding to its desirability. The majority noted low supply and high demand for its top vintages, a theme which featured in a recent article by the drinks business.

Over the last five years, the main markets for Champagne have changed. Europe has emerged as a strong Champagne buyer, accounting for 34.7% of the total regional trade in 2022, bettered only by the UK at 36.9%. Asia’s share has halved to 6.6% since 2017. The USA accounted for a fifth of Champagne trade in 2022, down from 30% in 2017.

Final Thought

Fine wine market sentiment into the new year

The fine wine market in 2022 was a game of two halves. The year started with strong secondary market sentiment. The bid-offer ratio, which compares the total value of bids (firm commitments to buy) to the total value of offers (firm commitments to sell), stood at 1.86 in December 2021, reflecting increased buying appetite and strong investor confidence.

Historically, a bid-offer ratio above 0.5 tends to indicate an uptrend in the market, or at the very least acts as a sign of price stability. In the first six months of the year, fine wine prices, as measured by the industry benchmark, Liv-ex 100 index, rose 7.1%. Prices for some wines hit record highs this year, but the number of active buyers at these levels dwindled as the year progressed.

By December 2022, the bid-offer ratio had fallen to 0.37. The year also finished with declines for fine wine prices. The Liv-ex 100 dipped 1.1% in Q4 while the Liv-ex 1000 fell 0.9%.

In a survey of Liv-ex members, which represent the largest pool of professional fine wine traders in the world, the outlook for the market in 2023 was mixed. 21% of the respondents said they were ‘quite pessimistic’ about the direction of the market, 34% were neutral.

Main market challenges

The market faced increasing headwinds as 2022 rolled on. Just as most of the world emerged from two years of Covid-19 restrictions, the war in Ukraine further disrupted the creaking global supply chain, sent energy prices souring and exacerbated already rising inflation. Bond and Equity markets fell. By the end of the year, USD$30tn of market value had been wiped out.

Over half (54%) of the Liv-ex survey respondents said they expect the global economy to pose further challenges to fine wine in the year ahead. Most (30%) noted recession and a global economic downturn, while 20% cited currency weaknesses and volatility.

Wine industry-specific factors will also play a role in fine wine market demand and the direction of prices. Merchants saw stock shortages as one of the biggest issues, particularly in reference to the upcoming release of Burgundy’s 2021 vintage. They also referenced limited volumes of vintage Champagne.

The two regions were at the forefront of market activity in 2022.

Regions to watch

High prices and reduced allocations might force buyers to look elsewhere. While Burgundy and Champagne were the stars of 2022, they are could be the first to suffer from a market downturn. Indeed, the Champagne 50 has now been the worst-performing Liv-ex 1000 sub-index for two consecutive months. However, this might shift demand within the region itself – a phenomenon previously seen in Burgundy – with Liv-ex merchants expecting demand for grower Champagne to pick up pace.

Survey respondents also predicted a price correction for Burgundy in 2023, especially for the more speculative brands which might fail to sustain their sky-high prices in the long term.

Meanwhile, 7% forecast a rebound for Bordeaux, but with a caveat. Views on the region’s En Primeur campaign remain mixed, with equal amounts of merchants predicting both a successful and an unsuccessful (some used stronger language) 2022 En Primeur launch. California was also singled out as a region expected to be in greater demand.

As last month’s Market Report pointed out, on the back of a muted performance in 2022, Italy and the Rhône are two regions offering stability, increasing diversity and relative value. Might 2023 see the re-emergence of these more recently subdued market players?

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.